1. (200)

0

200

400

600

800

1,000

1,200

1,400

2009 2010 2011 2012 2013 2014

Total Revenue Gross Profit Operating Income

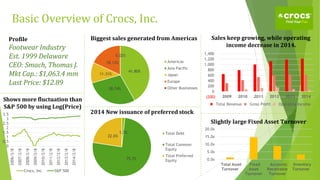

Basic Overview of Crocs, Inc.

41.80%

28.74%

11.31%

18.13%

0.02%

Americas

Asia Pacific

Japan

Europe

Other Businesses

Biggest sales generated from Americas Sales keep growing, while operating

income decrease in 2014.

1.7%

75.7%

22.6%

Total Debt

Total Common

Equity

Total Preferred

Equity

2014 New issuance of preferred stock

0.0x

5.0x

10.0x

15.0x

20.0x

Total Asset

Turnover

Fixed

Asset

Turnover

Accounts

Receivable

Turnover

Inventory

Turnover

Slightly large Fixed Asset Turnover

0

0.5

1

1.5

2

2.5

3

3.5

2006/2/8

2007/2/8

2008/2/8

2009/2/8

2010/2/8

2011/2/8

2012/2/8

2013/2/8

2014/2/8

Crocs, Inc. S&P 500

Shows more fluctuation than

S&P 500 by using Log(Price)

Profile

Footwear Industry

Est. 1999 Delaware

CEO: Smach, Thomas J.

Mkt Cap.: $1,063.4 mm

Last Price: $12.89

2. Potential Synergies

Revenue Perspective:

• Since two company focus a little

differently on casual shoes for Crocs

and sporty shoes for Under Armour,

the customer base does not overlap

too much and therefore the total base

could increase.

• Under Armour does not have much

sales portion in foreign countries.

Hence, through the distributors of

Crocs, Under Armour could have

bigger sales; on the other hand, Under

Armour could provide competitive

brand name for Crocs.

Cost Pespective:

• Crocs has big amount of sales in

United States and thus Under Armour

could integrate some operation.

• In Asia Pacific region, since Crocs

already has some distribution and

retailers, Under Armour could use

little capital to invest in Asia market.

• Since Crocs already has some patents

such as rubber materials, which may

provide Under Armour some base in

R&D and thus saves R&D costs.

• Remove inefficient departments or

products.

RevenueIncrease

CostReduction

3. Valuation of Crocs, Inc. and Recommendation

$0 $5 $10 $15 $20 $25 $30 $35

Precedent Transaction

Public Traded Comparable

Discounted Cash Flow

Valuation

• DCF: $20.19-$29.39

• Public Traded Comparable

companies: $10.56-$26.67

• Precedent Transaction:

$8.61-$20.19

Suggest Price and Accretion

• Price: $17.74-$23.97

• Accretion/Dilution: will

generate dilution for first

year, but accretion in

following year and grow fast

Reason

• Synergies after merger

could drive up buying price

even more

• Advantages of strong brand

name and American market