1. Human Capital

Reward Advisory

EBA consults on updated remuneration

guidelines

On 4 March 2015, the European Banking Authority (EBA) published a Consultation Paper

EBA/CP/2015/03 providing updated guidelines on sound remuneration policies. It is intended that

the new guidelines, once finalized, will apply from 1 January 2016, when the current guidelines

published in 2010 by the EBA’s predecessor, the Committee of European Banking Supervisors

(CEBS), will be repealed.

The proposed guidelines are significant and contain a number of key changes in response to

regulatory developments and the industry’s response to these since 2010. Some of the proposals

will have a significant impact on firms beyond those regulated under the Capital Requirements

Directive (CRD), and therefore all regulated institutions should be encouraged to respond to the

consultation process.

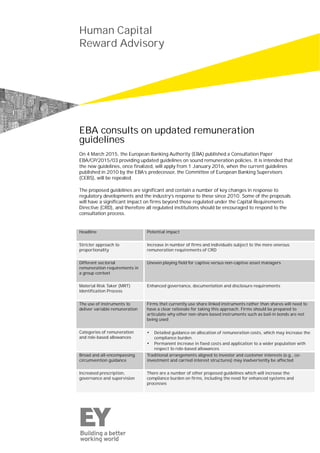

Headline Potential impact

Stricter approach to

proportionality

Increase in number of firms and individuals subject to the more onerous

remuneration requirements of CRD

Different sectorial

remuneration requirements in

a group context

Uneven playing field for captive versus non-captive asset managers

Material Risk Taker (MRT)

Identification Process

Enhanced governance, documentation and disclosure requirements

The use of instruments to

deliver variable remuneration

Firms that currently use share linked instruments rather than shares will need to

have a clear rationale for taking this approach. Firms should be prepared to

articulate why other non-share based instruments such as bail-in bonds are not

being used

Categories of remuneration

and role-based allowances

• Detailed guidance on allocation of remuneration costs, which may increase the

compliance burden.

• Permanent increase in fixed costs and application to a wider population with

respect to role-based allowances

Broad and all-encompassing

circumvention guidance

Traditional arrangements aligned to investor and customer interests (e.g., co-

investment and carried interest structures) may inadvertently be affected

Increased prescription,

governance and supervision

There are a number of other proposed guidelines which will increase the

compliance burden on firms, including the need for enhanced systems and

processes

2. EBA consults on updated remuneration guidelines 2

Background

The CEBS guidelines were published in 2010. The updates contained in the draft EBA guidelines

are particularly broad in scope as they are intended to cover the following key changes since

2010:

• Updates to CRD

• Bonus caps

• Stricter rules on the application of malus and clawback

• More granular disclosure requirements

• Regulatory Technical Standards (RTS)

• MRT identification

• Instruments that can be used for variable remuneration

• Other developments in the way remuneration policies and practices have evolved, including

experiences from regulatory supervision

• Approach to proportionality

• Definitions of fixed and variable remuneration

• The use of allowances

• The impact of sectorial remuneration principles following the publication of the

Alternative Investment Fund Managers Directive (AIFMD) and Undertakings for Collective

Investment in Transferable Securities V (UCITS V)

Scope

The draft guidelines apply to competent authorities (national regulators) and credit institutions,

including branches of credit institutions whose head offices are outside the EU and who are subject

to CRD (credit institutions and investment firms). They apply on an individual, sub-consolidated

and consolidated basis, including subsidiaries that are not themselves subject to CRD.

It is important for firms that are not subject to CRD to be aware of these proposed guidelines

and the dialogues now taking place, as they are likely to have a bearing on future remuneration

requirements under AIFMD and UCITS V.

Key points

Proportionality

• The current CEBS guidelines allow for some of the more onerous remuneration provisions of

CRD (deferral, payment in instruments, malus and clawback provisions) to be disapplied on the

grounds of proportionality. The EBA does not believe that this disapplication is permitted under

the terms of CRD, and has received the European Commission (EC)’s interpretation indicating

that the remuneration requirements need to be applied to all institutions without exception or

exemption.

• The draft guidelines also appear to suggest that the bonus cap provisions cannot be disapplied

on the grounds of proportionality if someone has been identified as an MRT.

Such an interpretation would have a significant impact on both the number of firms and

individuals subject to the more onerous remuneration requirements outlined above.

3. EBA consults on updated remuneration guidelines 3

• The EBA is asking for responses from the industry to support the advice they are intending to

provide to the EC, suggesting legislative amendments for a broader application of the

proportionality principle.

A number of firms impacted by AIFMD have used proportionality arguments to disapply the

more onerous aspects of the remuneration requirements, as currently supported by the

European Securities and Markets Authority (ESMA) guidelines on remuneration. These firms

should monitor the consultation closely and be aware of how proportionality will work for CRD

firms as it is likely to indicate how other regulations will develop.

Sectorial remuneration principles

• The draft guidelines recognize the impact of current sectorial remuneration guidelines for

AIFMD firms and the fact that ESMA is mandated to issue remuneration guidelines under

UCITS V.

• Currently, there is uncertainty on how the remuneration provisions of the various Directives

operate within a group context where one firm (and its staff) could be subject to multiple

regulatory requirements depending upon the nature of its business and the Directives it needs

to comply with.

• The draft guidelines suggest that the strictest set of requirements will apply, taking account of

the rules that the group is subject to and then adding on any specific sectorial requirements.

• There is concern from firms that are not currently subject to CRD, that some of the stricter

remuneration requirements of CRD could spread to their firms to address consistency and

uneven playing field arguments.

Clarification from ESMA would be welcome, to the extent it adds more certainty. Firms should

ensure they respond to the consultation process to ensure their views and the impact on the

industry are fully recognized.

Concerns around an uneven playing field will resurface where; for example, those individuals

working for a captive asset manager are subject to the bonus cap rules, while those who work

for stand-alone non-CRD firms are not.

MRT identification process

• The draft guidelines make it clear that, in a group context, the identification of MRTs needs to

take place at a consolidated and sub-consolidated level and within subsidiaries that may

themselves not be subject to CRD.

• Firms will be required to use additional criteria, beyond those in the RTS, in their self-

assessments to ensure a complete identification of all MRTs.

• The draft guidelines also emphasize the need for a documented and transparent self-

assessment process that is periodically updated. The self-assessment also needs to be updated

throughout the year with at least the results of the qualitative criteria of the RTS.

• The importance of the MRT identification process is highlighted by the degree of governance

and disclosure suggested by the guidelines and the active involvement of the remuneration

committee, where one is established.

4. EBA consults on updated remuneration guidelines 4

Firms will need to ensure that they have the requisite process, policies and governance in place

to identify their MRTs on an ongoing basis and to seek any regulatory approvals to exclude staff

who meet the quantitative thresholds.

• The guidelines attempt to provide further clarity on the identification process in a group

context, but would seem to imply that an individual who is in the management body of a

significant subsidiary could be excluded (provided all other criteria are also met), if he or she is

not in the management body of the parent institution.

• The draft guidelines also suggest that those subsidiaries that are subject to CRD need to carry

out their own solo-level identification process, unless they are small and less complex. This

may have a number of practical implications depending on the nature of the organization

and how it is structured and managed.

Instruments that can be used for variable remuneration

• The draft guidelines prioritize the use of instruments, such as bail-in bonds and shares over

share-linked instruments. They indicate that other instruments (e.g., instruments subject to

bail-in) should be used where available.

• As part of their consultation process, the EBA has requested information from listed firms on

the impact of using shares and, where possible, other instruments set out in the RTS. Given

the current limited use of other such instruments, the rationale for this will need to be

clearly articulated.

• It would appear that the draft guidelines would prohibit the payment of dividends and interest

on deferred elements of variable remuneration, even if they are paid after the end of the

deferral period. This is contrary to the current CEBS guidelines and there would appear to be

no basis for this restriction. These payments are common practice, and therefore clarity

should be sought through the consultation process on the rationale for this exclusion.

Categories of remuneration and role-based allowances

Given the importance of the bonus cap ratio, the EBA has sought to clarify what should be

included as part of remuneration and how various remuneration elements should be categorized

between fixed and variable remuneration.

Firms will need to review the guidance given and ensure that their processes capture all aspects

of remuneration to include in their calculations and reporting. For instance, the treatment of

expatriate compensation and benefits previously varied across the industry.

The proposed guidance on Long Term Incentive Plans and when they should be included in

variable remuneration seem at odds with other parts of the requirements and will require

clarification through the consultation process.

The circumstances in which guaranteed bonus payments can be made remains restricted. But it

is interesting to note that the draft guidelines indicate that, in certain circumstances, these

awards do not need to be included in bonus cap calculations and also that they can be paid

entirely in cash.

5. EBA consults on updated remuneration guidelines 5

The draft guidance on allowances is consistent with the EBA opinion issued in October 2014.

Firms should therefore review this guidance in relation to their own allowances and consider any

necessary changes, and their timings, given that this is likely to be an area of focus. In

particular, those who have used allowances only for those individuals who are identified as

MRTs and are subject to the bonus cap, or those who have used instruments to deliver the

allowances, may need to reconsider their approach.

Circumvention

The draft guidelines contain more granular information on what constitutes circumvention. Under

these proposals, firms will need to review these criteria against their own arrangements and pay

special attention to any co-investment and carried interest type arrangements to ensure that they

are in line with regulatory expectations.

It would appear that carried interest structures, whereby staff receive a return solely based on

their investment in the vehicle can still be excluded from the definition of remuneration. If the

return to staff is not solely a return on their investment it should be included as variable

remuneration. For staff receiving such remuneration arrangements that are subject to the

bonus cap, plans will need to be reviewed and potentially changed. This may be in conflict with

investor interests and requirements.

Disclosure

The draft guidelines call for enhanced disclosure in line with the requirements of the Capital

Requirements Regulation. Key new items that need to be disclosed are:

• Explanations of any differences between the remuneration policy that is applicable at a group

level and what is applied at other levels in the organization.

• Details of how the MRT identification process has been applied, including the additional criteria

used in the self-assessment process.

• How variable remuneration reacts to performance changes in the institution.

• The most important design characteristics of the remuneration system; these have now been

prescribed under eight separate headings in the draft guidelines.

• Granular disclosure on the ratios between fixed and variable remuneration.

6. EBA consults on updated remuneration guidelines 6

Other points of interest

There are a number of other points in the draft guidelines that give an indication of the EBA’s

thinking and the trend toward greater governance and regulatory supervision. Firms may wish

to review these to ensure that current policies, processes and governance arrangements are in

line with the currently published regulatory thinking.

• There is more focus on all risk types when aligning the remuneration policy with the firm’s risk

strategy and appetite.

• There is an increased focus on business unit involvement in the development of the

remuneration policy.

• The need for a separate remuneration committee for all significant institutions within a group.

However, if the subsidiary is subject to specific sectorial legislation, then it is the sectorial

legislation which will determine the need for a separate remuneration committee.

• The proposed requirement for the remuneration committee to review a number of possible

scenarios to test how the remuneration policies and practices react to external and internal

events and back-test the criteria used for determining the award and the ex-ante risk

adjustment based on the actual risk outcomes is now more specific. In addition, there now

appears to be a requirement to provide significant detail on how variable remuneration reacts

to performance changes. This transparency appears to be aimed at providing staff with clear

direction on the circumstances under which remuneration could be significantly reduced (to

zero) due to performance or conduct issues. Close cooperation between different internal

functions (e.g., HR, finance, risk and strategic planning) will be required to design the

parameters for the reward stress testing against different performance criteria and conduct

failures.

• The EBA has stated that they may choose to consult further on the remuneration requirements

applicable to staff whose conduct could affect, directly or indirectly, consumers. Some national

regulators have already increased the scrutiny on such remuneration arrangements and we

anticipate that this will be an ongoing trend.

• The definition of staff has been expanded to include any other person acting on behalf of the

institution and its subsidiaries. Firms will need to ensure their internal processes capture

certain contractors and clarification will be required through the consultation process on the

extent to which others (e.g., advisors) acting on behalf of the firm need to be captured.

• The draft guidelines mention staff behavior in the context of the remuneration policy, which is

in line with current focus of a number of regulators on the behavioral impact of remuneration

design. The compliance function would also be tasked with assessing the impact of the

remuneration policy on risk culture.

• The need for an annual independent review of remuneration policies is emphasized further

together with guidance on how (including documentation requirements) and who should

conduct these reviews in different types of organization.

• Further emphasis is placed on the need for documentation underpinning reward governance,

policy and process, including the decision-making process.

• A framework for role descriptions is identified as a key component of the remuneration policy.

While a fundamental part of any remuneration framework, this had not been specifically

referenced by the current CEBS guidelines.

7. EBA consults on updated remuneration guidelines 7

• Firms may now need to demonstrate that the remuneration arrangements for control functions

are distinct from other roles by evidencing a higher fixed to variable ratio compared to other

roles in the business.

• Given the bonus cap limits, firms will now need to document their policy on the ratio between

fixed and variable remuneration in a far more granular fashion.

Regulatory sanctions have been added to the criteria that need to be reviewed in the ex-post risk

adjustment malus and clawback process.

Next steps

The EBA is consulting on these guidelines for three months and the consultation period will end on

4 June 2015.

It is intended that the new guidelines, once finalized, will be applicable from 1 January 2016.

EY will be responding to this consultation paper and we would be happy to discuss any issues

you may have, from your institution’s perspective, when formulating our response.