1. C O M P A N Y R E P O R T

India

31 Oct 2012

KPIT Cummins Rs 123.9

Sector: IT/TECH A shining star in mid-cap IT sector

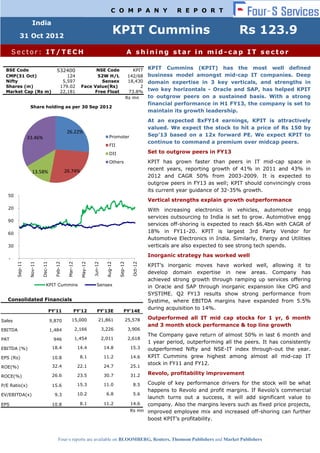

BSE Code 532400 NSE Code KPIT KPIT Cummins (KPIT) has the most well defined

CMP(31 Oct) 124 52W H/L 142/68 business model amongst mid-cap IT companies. Deep

Nifty 5,597 Sensex 18,430 domain expertise in 3 key verticals, and strengths in

Shares (m) 179.02 Face Value(Rs) 2

Market Cap (Rs m) 22,181 Free Float 73.8% two key horizontals - Oracle and SAP, has helped KPIT

Rs mn to outgrow peers on a sustained basis. With a strong

financial performance in H1 FY13, the company is set to

Share holding as per 30 Sep 2012

maintain its growth leadership.

At an expected 8xFY14 earnings, KPIT is attractively

valued. We expect the stock to hit a price of Rs 150 by

26.22%

Promoter Sep’13 based on a 12x forward PE. We expect KPIT to

33.46%

continue to command a premium over midcap peers.

FII

DII Set to outgrow peers in FY13

Others KPIT has grown faster than peers in IT mid-cap space in

26.74% recent years, reporting growth of 41% in 2011 and 43% in

13.58%

2012 and CAGR 50% from 2003-2009. It is expected to

outgrow peers in FY13 as well; KPIT should convincingly cross

its current year guidance of 32-35% growth.

150

Vertical strengths explain growth outperformance

120 With increasing electronics in vehicles, automotive engg

services outsourcing to India is set to grow. Automotive engg

90

services off-shoring is expected to reach $6.4bn with CAGR of

60 18% in FY11-20. KPIT is largest 3rd Party Vendor for

Automotive Electronics in India. Similarly, Energy and Utilities

30 verticals are also expected to see strong tech spends.

Inorganic strategy has worked well

-

Sep-11

Sep-12

Feb-12

Aug-12

Oct-12

Nov-11

Dec-11

May-12

Mar-12

Jun-12

KPIT’s inorganic moves have worked well, allowing it to

develop domain expertise in new areas. Company has

achieved strong growth through ramping up services offering

KPIT Cummins Sensex in Oracle and SAP through inorganic expansion like CPG and

SYSTIME. Q2 FY13 results show strong performance from

Consolidated Financials Systime, where EBITDA margins have expanded from 5.5%

during acquisition to 14%.

FY'11 FY'12 FY'13E FY'14E

15,000 21,861 25,578 Outperformed all IT mid cap stocks for 1 yr, 6 month

Sales 9,870

and 3 month stock performance & top line growth

EBITDA 1,484 2,166 3,226 3,906

The Company gave return of almost 50% in last 6 month and

PAT 946 1,454 2,011 2,618

1 year period, outperforming all the peers. It has consistently

EBITDA (%) 18.4 14.4 14.8 15.3 outperformed Nifty and NSE-IT index through-out the year.

EPS (Rs) 10.8 8.1 11.2 14.6 KPIT Cummins grew highest among almost all mid-cap IT

stock in FY11 and FY12.

ROE(%) 32.4 22.1 24.7 25.1

26.6 23.5 30.7 31.2 Revolo, profitability improvement

ROCE(%)

P/E Ratio(x) 15.6 15.3 11.0 8.5 Couple of key performance drivers for the stock will be what

happens to Revolo and profit margins. If Revolo’s commercial

EV/EBITDA(x) 9.3 10.2 6.8 5.6

launch turns out a success, it will add significant value to

EPS 10.8 8.1 11.2 14.6 company. Also the margins levers such as fixed price projects,

Rs mn improved employee mix and increased off-shoring can further

boost KPIT’s profitability.

Four-s reports are available on BLOOMBERG, Reuters, Thomson Publishers and Market Publishers

2. Company Report: KPIT Cummins 31 Oct 2012

Investment Rationale

Fastest growing mid-cap IT player

KPIT Cummins is the fastest growing mid-cap IT player in India.

KPIT grew at an outstanding CAGR of 50% in the period 2003-2009.

It has maintained superior performance with USD revenue growth of

41% in FY11 and 43% in FY12.

Consistently It has witnessed similar growth in its bottom line too. In FY12 it

growing at registered PAT growth of 54% to Rs 1,449mn, along with 43%

CAGR of above growth in EBITDA and EPS growth of 47% y-o-y. These numbers are

40% better than almost all other mid-cap IT peers.

Company FY12 Rev Growth Rev Growth

Name Rev EBITDA PAT in Fy12 in Fy11

Hexaware

Technologies 15,347 3,354 2,670 37% 3%

Infotech

Enterprises 15,707 2,866 1,514 29% 22%

Mindtree Ltd 19,537 3,315 2,185 27% 12%

NIIT

Technologies 16,068 3,005 1,964 29% 35%

Persistent

Systems 10,339 2,580 1,418 28% 32%

Polaris FT 16,568 2,730 2,023 21% -2%

KPIT

Cummins 15,138 2,304 1,450 52% 35%

(Rs mn)

This extraordinary growth is the result of successful execution of its

chosen strategy of vertical focussed growth and successful inorganic

expansion. This growth is driven by three major verticals, Auto &

transportation, Manufacturing and Utilities. While working in these

verticals the company has developed strong horizontal service

offerings in Auto & Electronics, IES and SAP.

Differentiated vertical-focus strategy driving growth

While the rest of the IT industry started talking about vertical-focus

in the last 2 years, KPIT very early on decided to focus on a few

select verticals to be able to compete better. This company can be

Vertical-focus considered as the pioneer of this differentiating strategy among the

strategy sets it IT mid-caps.

apart

The company has focused from early days on automotive and

manufacturing verticals. This has resulted in deep domain expertise

in its focus verticals. KPIT Cummins is the largest 3rd party vendor

for automobile electronics in India. KPIT has developed a strong

domain expertise in the manufacturing segment and specifically in

automobile sector. In its last more than 20 years of operations it has

Four-S Research 2

3. Company Report: KPIT Cummins 31 Oct 2012

been working mainly in its niche segment i.e. Automotive-

manufacturing. This resulted in high domain expertise and strong

clientele in the segment.

This gives KPIT advantage among not only their Indian competitors

but also with most of their global competitors. Till now, KPIT has

developed technology solutions for more than 120 global automotive

companies which include 8 out of top 10 global original equipment

manufacturers (OEMs).

Successful inorganic growth strategy

KPIT Cummins has successfully kept firing the growth engine by

supporting strong organic growth with carefully chosen inorganic

acquisitions. These acquisitions have helped the company to grow at

Highly effective a rapid space of 40-50% CAGR in the last decade, resulting in one of

inorganic the fastest growing company in the mid-cap IT space. It has also

growth track been successful in smooth integration of these acquisitions. Through

record these acquisitions it has developed expertise in various services

offering in the likes of ERP implementation, Oracle and SAP services.

These acquisitions were done with focus on gaining ground in terms

of geography entry, or service offering expertise or gaining

important client clusters. For example, KPIT has developed expertise

in SAP practice with the successful acquisitions of Panex Consulting

and Sparta Consulting whereas Oracle practise has been

strengthened with recent CPG and Systime acquisition. It did 10

such strategic acquisition in the last decade with focus on driving the

growth through strong practice offerings in SAP, ERP and Auto

electronics and developed strong client base across the globe.

Systime has given scale in Oracle

If one takes the example of latest acquisition, SYSTIME ($50mn

rev), the largest acquisition till date by KPIT, it gives KPIT strong

Oracle practice, with JDE specialisation. This has helped KPIT

improve its offering to its key manufacturing clients as clients in this

industry prefer JDE solutions. Systime is the largest JD Edwards

solution provider globally. It also gave the company foothold and

strong client base in Brazil where Systime has good chunk of

revenue coming.

Innovation focused and R&D driven company

Unlike most IT companies in India, KPIT invests significantly in R&D.

The investment in these efforts has now increased to ~3% of its

revenue. From these initiatives, the Company has applied for 40

patents in last 18 months.

Four-S Research 3

4. Company Report: KPIT Cummins 31 Oct 2012

Innovation to KPIT has many innovation based R&D projects, designed to develop

lead non linear new technologies and solution for their customers. This has resulted

growth in growing revenue contribution from its non-linear projects.

It has a department named ‘Center for Research in Engineering

Services and Technology’ (CREST), which is totally dedicated to

these initiatives. It focuses on research in areas such as System

engineering, parallel computing, program analysis tool, security and

surveillance and Energy. These R&D initiatives are again industry

focussed which helps the company to maintain its edge in the

industry and provide best service with IP led solution to its

customers.

Revolo a unique R&D initiative

Revolo is one of the key results of this initiative. Revolo is plug-in,

parallel hybrid solution for the automobiles which converts a regular

vehicle into hybrid vehicle. It has filed 16 patents till date for Revolo

only.

Robust performance in H1 FY13

Top line expands strongly

The company has given strong results in H1FY13 with revenue

growing by 72% yoy from Rs 6,411mn in H2FY12 to Rs 11,054mn

driven by revenue growth from latest acquisition, Systime, and

strong momentum in all verticals. This was supported by outstanding

growth in the US market where it grew by almost 100% from Rs.

4,243mn in H1FY12 to Rs 8,434mn in H1FY13, whereas it witnessed

Strong H1

a flat European market with 11% growth and in ROW it grew by

performance

35%. Manufacturing and energy & utilities verticals grew at strong

sets the tone

265% and 127%, respectively, in H1FY13 whereas Automotives

vertical grew at 30%. All the SBUs showed good growth in this

period with 94% growth in IES and 77% growth in SAP SBU and

53% growth in Auto & engg. Its PAT grew by good 60.8% from Rs.

605mn in H1FY12 to 974mn in H1FY13.

The company also witnessed strong growth on client level with top

client account (Cummins) growing by 60% whereas top 5 clients

grew at 60% and top 10 clients account grew by 55%. The company

added 7 new customers in this period and has 69 >$1mn clients

compared to 59 at the start of the year.

Increases margins as well, helped by Systime

The company has also managed to push up the EBITDA margin from

13% to 14% despite lower EBITDA margins of Systime. Systime has

Four-S Research 4

5. Company Report: KPIT Cummins 31 Oct 2012

Systime also shown strong performance, with 11.6% and 15.7% revenue

margins are growth q-o-q in Q1 and Q2FY13, respectively, along with EBITDA

moving up margin improvement from 5.5% at the time acquisition to 14% in

Q2FY13.

Q2 Q2 % Q1FY1 % H1 H1 %

FY13 FY12 Change 3 Change FY13 FY12 Change

Net Sales 5,672 3,250 74.5 5,383 5.4 11,055 6,412 72.4

Total Expenditure 4,943 2,808 76.0 4,576 8.0 9,500 5,575 70.4

EBITDA 729 442 65.0 806 -9.6 1,554 837 85.8

Other Income 22 109 -79.5 30 -25.8 34 132 -74.2

Operating Profit 752 552 36.3 837 -10.2 1,589 969 63.9

Interest 32 11 199.9 30 8.2 62 19 224.3

Exceptional Items 55 27 104.7 81 0 100.0

PBDT 774 541 43.2 834 -7.1 1,608 950 69.3

Depreciation 114 116 -1.0 113 0.8 228 210 8.5

PBT 660 425 55.2 720 -8.4 1,380 740 86.5

Tax 191 88 118.3 185 3.6 376 159 137.1

Profit After Tax 468 338 38.8 536 -12.5 1,004 581 72.7

Minority Interest -12 -1 -936.4 -12 0.4 -25 -4 -482.2

Shares of Associates 5 28 -82.4 -10 147.9 -5 28 -119.1

Net Profit 461 365 26.4 513 -10.1 974 606 60.8

(Rs mn)

Four-S Research 5

6. Company Report: KPIT Cummins 31 Oct 2012

Peer Benchmarking

Strong top-line performance

Company Market EV Sales Sales 3 EBITDA PAT

Cap yr CAGR

Infotech 21,252 21,746 15,531 20% 2,691 1,614

Hexaware 32,005 32,005 14,505 8% 2,513 2,670

Persistent 18,792 18,869 10,003 19% 2,244 1,418

NIIT 16,468 16,593 15,765 17% 2,701 1,972

Mindtree 27,505 27,576 19,152 16% 2,930 2,185

Average 23,204 23,358 14,991 16% 2,616 1,972

KPIT 21,765 22,954 15,000 24% 2,166 1,454

(Rs mn)

KPIT has shown significant growth in last few years over its peers. It

has 3 yr CAGR for sales of 24% despite having not so good

performance in FY10 due to recessionary environment. KPIT grew

Better growth faster than most of the mid-cap IT company in the period with

than peers decent performance on margins level. Such strong growth was

showcased earlier too by KPIT when it grew 50% CAGR in 2003-

2009 period and above 40% growth in FY11 and FY12.

Scope to improve profitability

FY12 Margins

Company EBIDTA PAT

Infotech 17% 10%

Hexaware 17% 18%

Persistent 22% 14%

NIIT 17% 13%

Mindtree 15% 11%

Average 18% 13%

KPIT 14% 10%

KPIT’s profit margins are on the lower side amongst its peers. Its

profitability was also recently impacted by acquisition of Systime.

Systime was a strategic acquisition, but it had the lower margins

(5.5%) compared to company’s margins. The key will be to push up

Four-S Research 6

7. Company Report: KPIT Cummins 31 Oct 2012

the margins of the business coming from such low margin acquisitions

while striving for the growth through these acquisitions. Higher

margins can also be achieved by various operational levers such as off-

Strong balance shoring, pyramid restructuring etc.

sheet helps in

In H1 FY13, Systime’s margins have started moving up. Systime

inorganic

margins have expanded substantially with 10% and 14% EBITDA

strategy

margin in Q1 and Q2 FY13, respectively.

Liquidity ratios on Par

Current Ratio (x) Cash Ratio (x)

Company

FY10 FY11 FY12 FY11 FY12

Infotech 2.57 6.19 4.81 3.16 2.36

Hexaware 2.08 2.84 2.15 1.56 1.01

Persistent 2.10 1.88 1.82 0.40 0.45

NIIT 1.81 1.93 1.74 0.32 0.41

Mindtree 1.79 2.47 1.75 0.21 0.16

Industry

Average 2.07 3.06 2.45 1.13 0.88

KPIT 2.39 1.82 1.39 0.77 0.30

The company has strong balance sheet with strong cash ratio and

current ratio. Due to strong performance in the past, the company has

managed to continue the inorganic expansion without much strain on

its balance sheet.

Debt Equity (x) Interest Coverage (x)

Company

FY11 FY12 FY11 FY12

Infotech 0.04 0.04 137.15 299.28

Hexaware 0.01 0.00 10.57 74.02

Persistent 0.02 0.01 NA NA

NIIT 0.01 0.01 92.86 60.85

Mindtree 0.03 0.01 266.50 447.00

Average 0.02 0.01 126.77 220.29

KPIT 0.05 0.17 28.40 23.50

Four-S Research 7

8. Company Report: KPIT Cummins 31 Oct 2012

Valuation

Valuation: Growth momentum to drive valuation up

The company is continuing its growth momentum from last two years

into this year. Revenues grew 72% in yoy in H1 FY13 and 74% yoy in

Q2FY13. The Company is expected to maintain this growth momentum

in the rest of the year and should easily cross its higher range of

guidance of 35% this year.

Given the strong growth environment in its focus verticals, the

Company is expected to carry forward this momentum to the next

year. We expect KPIT to overshoot its guidance of 35% growth in FY13

and to achieve about 17% growth in FY14.

TTM Price Market Price EV/ MCap/

Company Name Sales (Rs) Cap PE /BV EBITDA Sales

Hexaware

Technologies 17,363 112 33,160 10.0 3.1 6.8 1.9

Infotech Enterprises 17,672 188 20,961 10.3 1.7 4.1 1.2

Mindtree Ltd 22,047 660 27,145 9.3 2.9 8.1 1.4

Persistent Systems 11,659 478 19,120 11.4 2.0 5.9 1.6

Polaris FT 22,480 120 11,917 5.0 1.0 3.1 0.5

KPIT Cummins 19,643 124 22,181 11.8 2.8 7.9 1.1

(Rs mn)

Premium valuations imply one year price target of Rs 150

We expect KPIT Although company is traded at premium compared its peers, it will

to command a continue to demand this premium based on its growth prospects and

premium over vertical growth strategy. Currently stock is trading at Rs 124, implying

peers a PE of 10.9x and 8.4x for FY13 and FY14, respectively. We expect

KPIT to reach 150 by Sep’13 based on a forward PE of 12x Sep’13. We

believe KPIT deserves a continuing premium over the midcap space.

1 yr forward PE band chart

160

16x

140

120 13x

100

10x

80

60

40

20

0

Four-S Research 8

9. Company Report: KPIT Cummins 31 Oct 2012

KPIT’s Business

Differentiated Strategy : Strong Vertical Focus

KPIT has organised its efforts around 3 key verticals: auto and

transportation, manufacturing and energy and utilities. KPIT tries to

provide industry specific holistic solutions to its clients with best in

class service offerings.

With high domain expertise, the company is in a position to provide

Differentiated full range of services to its customers. The company is also investing

strategy sets in R&D to develop and maintain domain excellence in automotive

company apart segment.

Revenue Spread – Verticals

71.38%

11.22%

1.68%

15.72%

Automotive & Transportation

Manufacturing

Energy & Utilities

Others

Automotive and transport vertical contributed more than Rs 10.7bn,

i.e. 71% of FY12 revenue, up from Rs 6.39bn or 64.77% of revenue

in FY11. The contribution from Manufacturing increased from

10.48% in FY11 to 11.22% in FY12. This largely helped drive 41%

and 43% growth in FY12 and FY11, respectively.

Increased outsourcing in Auto industry

With increasing competition in the Auto industry, OEMs are facing

intense pressure to bring in the new models at a quicker pace, with

increased electronics in them. This has worked as a booster to the

Auto industry outsourcing industry as outsourcing helps in bringing down the total

more inclining time required to develop the product and bring it in the market.

towards out-

sourcing Outsourcing helps OEMs and other auto vendors to bring down the

lead time in product development and imparts flexibility to them to

easily adjust to market dynamics. Also growing electrification of the

vehicles and its increasing criticality in product success has further

Four-S Research 9

10. Company Report: KPIT Cummins 31 Oct 2012

pushed the outsourcing market in auto engineering and Auto

industry.

Technology development in Automotive space to drive top

line

With focus on fuel efficiency, safety, cost cutting and hybrid

technology increasing, auto companies are more and more

incorporating electronics into their vehicles. As OEMs are not looking

to get into technology development, especially IT, which is not their

Technology core domain, this development mainly gets outsourced to company’s

development in working in this domain. KPIT has benefitted in this trend with

Auto to push for increasing projects from Auto OEMs.

more As per Nasscom, the engineering services space is currently

electrification of exploding, thanks to robust growth across Europe, Asia and the US.

vehicles According to the report, the total engineering services market was

worth $746 billion in 2004 and will touch $1,100 billion by 2020. Of

this the outsourced component could be worth around $200 billion.

Currently, the engineering services outsourcing (ESO) market is

worth around $15 billion with India garnering a healthy

12%share. Automotive is second largest contributor in this with 19%

share

US market on the recovery path

US constituted around 70% of revenue in FY12; its share increased

to 76% in Q1FY12. With US economy showing signs of recovery,

prospects US car sales are expected to improve going forward.

US Auto Sales (in mn)

16

15

14

13

12

11

10

9

8

Source:Ycharts.com, Bureau of Economic Analysis and Four-S

Four-S Research 10

11. Company Report: KPIT Cummins 31 Oct 2012

With improving US car sales numbers, KPIT is expected to get good

demand from its US based clients along with Japan and emerging

markets with improving overall sector condition.

Increasing electronics in Automotives

As the technology is developing, more and more electronics is used

in automotives to improve vehicle’s safety, fuel efficiency. Power-

train, infotainment, interiors, tele/diagnostics. As per databeans,

Increasing roughly 25% of vehicle cost accounts for electronic products which

electronic goes up-to 30% in luxury cars. This will soon reach to 50%. Micro

components in controllers based ECUs are increasing in vehicles with increasing

vehicle, booster features in the vehicle. ECUs per vehicles range from 25 to 35 in an

for KPIT average vehicle to as many as 70 in luxury cars up from single digit

micro controllers few years back. The

automotive microcontroller market is expected to expand to Rs.

328bn ($7 billion) by 2015.

Niche specialisation in other focused verticals driving the

growth

KPIT is now expanding into emerging verticals like Energy & Utilities

and Industrial equipments. Energy & Utilities vertical is expected to

attract large technology investments in the coming years which the

company looking to leverage with domain specialised offerings. In

cognizance with this core sector strategy, KPIT has recently moved

Emerging focus

out of BFSI sector which contributed around 2% to its revenue.

vertical: Utilities

This niche specialisation helps the Company to win larger deals with

the existing and new customers and improves customer mining.

Company moving ahead should also improve the profitability with

plans to improve business mix and increase in offshore services.

IT investment in Utilities on rise

With increasing concerns all over the world over climate changes and

environment issues, and depleting natural conventional energy

Huge

resources, there is rising demand in improving overall efficiency in

opportunity in

this sector with the help of information technology. The opportunities

utilities sector

vary from smart grid applications to billing solutions to customer

management.

For utilities vertical, north America is a vital vertical, where the

company will gain advantage with its strong presence through Sparta

Consulting. Sparta Consulting is one of the fastest growing SAP

services partners in North America, having received the 2012 SAP

Partner Impact Award as the SAP Services Partner of the Year for

Momentum in North America. Sparta has delivered over 250

Four-S Research 11

12. Company Report: KPIT Cummins 31 Oct 2012

successful projects based on SAP solutions, which have included over

25 leading energy and utilities companies.

Strong positioning in horizontal SBUs pushing up the growth

IES, Automotive & Engg and SAP constitute company’s key SBUs.

IES (INTEGRATED ENTERPRISE SOLUTIONS)

IES is the largest SBU in the company contributing 40% revenue to

company’s top-line and is largely driven by Oracle practice. It grew

57% last year along with new customers deal worth $60mn. IES

IES: Enterprise includes ERP implementation, support and e-biz. In IES, Oracle is the

consulting key practice which includes Business Intelligence (BI), Manufacturing

Execution Systems (MES), JD Edwards (JDE), Oracle Transportation

Management (OTM) and Supply Chain Management (SCM). Through

organic skill developments and acquisitions KPIT has strengthen its

offering. It is third largest partner in Oracle in North America in

Industrial manufacturing and eight largest across the industries.

With latest Systime acquisition, the Company’s standing is further

strengthened in Oracle-JDE offering.

Auto & Engineering

KPIT is the largest third party vendor for automotive embedded

electronics in India. With 50% growth from last year A&E contributes

26% of revenue. Auto & Engg is the highest margin SBU in the

Auto & engg: company with margins ranging in 19-20%.

Strong domain

With increasing electronics in Automotives the company is getting

expertise

good traction from Powertrain, Infotainment, AUTOSAR, MEDS,

Diagnostics and Telematics. This is niche market service line offering

from KPIT with high domain expertise, offering embedded software

and automotive electronics related practices to OEMs and tier I & II

vendors. To further improve its competence in the vertical lot of R&D

work is done in this SBU which results in IP based solutions to its

clients.

SAP

KPIT has strong presence in SAP ERP implementation services for

energy and utilization sector along with manufacturing sector with

SAP: strong

North America as major geography. The SAP SBU grew 57% last

pipeline with

year with the company getting traction across the industries. The

many multi-

SAP SBU is seeing good traction in Core ERP implementation,

million deals

Business Intelligence (BI) & Analytics, Customer Relationship

Four-S Research 12

13. Company Report: KPIT Cummins 31 Oct 2012

Management (CRM), Human Capital Management, Mobility and

Application Maintenance & Support (AMS) projects. It closed three

deals in SAP with more than $20mn size last year. With technology

reset happening with in SAP company sees good opportunity HANA,

mobility and Success factors in the coming days.

The company is also looking to increase non linear business in SAP

by developing industry specific templates targeted for mid size

business in its focused industries. These templates can be deployed

at much lower cost and time than traditional methods.

SAP is lowest margin SBU in the company with Q2FY13 margins at

7%. Increased bench due to shift in technology and more onsite

implementation projects are one of the key reasons for lower

margins.

Revenue Distribution: SBU wise

3%

IES

31% 40%

Auto & Engg

SAP

Semiconductor

26% Solutions Group

Revolo: A hybrid solution

Revolo is a major output of the Company’s R&D efforts. This could be

a major lever to push up non linear revenue for the company in the

near future. Revolo is a plug-in, parallel hybrid solution for the

automobiles which converts a regular vehicle into hybrid vehicle

using company’s innovative development in power-train technology.

It has filed 16 patents till date for Revolo only.

The solution will be developed and manufactured by 50:50 JV

Revolo: between KPIT and Bharat Forge. Here KPIT will license its technology

Opportunity to whereas Bharat forge will bring in support for manufacturing and

create hybrid kit distribution.

market

As per Automotive Research Association of India (ARAI) tests, this

technology improves fuel efficiency by 40-50% and reduces green

house gas emission by 30%. The kit can be fitted to a vehicle in 4-6

hrs at the cost of 65k-150K depending on type of vehicle. The

Company is currently doing testing on 200 vehicle fitted with the kit

Four-S Research 13

14. Company Report: KPIT Cummins 31 Oct 2012

and should come up with results near the year closing.

After testing and concluding govt regulatory requirements the

company should be able to launch the product in FY14 commercially.

Revolo was earlier expected to launch in FY13 but due to battery

problems it got delayed. The company expects Rs 3-5bn revenue

from this product.

Revenue Distribution: Geographically

Though KPIT has strong presence across globe, it has strong

dependency on US market like many other IT cos. Another reason

for this could be attributed to its large client Cummins, based out of

US is the key USA, which attributes 20-22% of revenue. In FY12, the US market

market contributed almost 70% of company’s revenue, up from 67% in FY11

and 60% in FY10. This is working in favour of the company, as the

US economy and auto & manufacturing sector is showing the signs of

recovery.

Geographical Revenue Spread

18.20% USA

69.56%

12.24% Europe

Rest of World

Due to lower European market exposure, the Company is

comparatively sheltered from current European crisis. It is looking to

further diversify its geographical reach by gaining market share in

Emerging emerging market like APAC, China and Brazil. The emerging market

market showing grew 56% in FY12 with growth coming from countries like India,

strong growth China, Japan and Korea.

To support good growth in China in automotive business, KPIT has

set up a subsidiary in China. Similarly it has set up subsidiaries in

Brazil and Netherlands too to strengthen its operations in Latin

American nations, Scandinavian and other European regions. With

the acquisition of Systime it has good positioning in the Brazil

market of JDE offerings.

Successful inorganic strategy to plug gaps in business model

The company has successfully implemented its inorganic growth

strategy to plug in gaps in its customer offerings. With 10

Four-S Research 14

15. Company Report: KPIT Cummins 31 Oct 2012

acquisitions in as many years the company has managed to increase

its top line by 28x in the last 10 years. With these acquisitions

company has increased its foothold geographically and improved its

client base.

Revenue growth strongly supported by acquisitions

16000

14000

Strategic

12000

acquisitions

10000

playing big role 8000

in exponential 6000

growth 4000

2000

0

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Consol Revenue Standalone revenue

(Rs mn)

KPIT’s acquisitions are driven by any of the 3 considerations: domain

expertise, geographical presence, or service expansion. Be it

Cummins at the initial stage which gave them auto-mfg domain

expertise or be it the latest $50mn SYSTIME acquisition which has

strong hold in Oracle and JDE practice.

Acquisitions

Company Year Size Rationale

Anchor Customer – Cummins,

Cummins Infotech 2002 $1mn Vertical Focus - Manufacturing

Panex 2003 $ 7.2 Mn SAP Practice, Anchor Customer

SolvCentral 2005 $ 3.5 Mn BI Practice, Anchor Customer

Direct Presence in France,

Pivolis 2005 $ 1.5 Mn Geography

Auto Electronics Domain, Auto

10 years: 10 CG Smith 2006 $ 6.2 Mn OEM & Tier I Customers

acquisition Harita TVS 2008 $ 1.0 Mn MEDS Practice

SAP Practice, US Geography

Sparta Consulting 2009 $ 3.5 Mn presence in SAP

Vehicle Diagnostic & Telematics,

In2Soft 2010 $ 4.0 Mn German Frontline

CPG 2010 $ 11 Mn Oracle Consulting

SysTime 2010 $ 50 Mn Oracle Consulting, JDE Specialist

With these acquisitions KPIT has developed a strong offering in SAP,

Auto engg and Oracle. This helps KPIT in cross-selling their

Enterprise application services to their existing customer.

Four-S Research 15

16. Company Report: KPIT Cummins 31 Oct 2012

Though these acquisitions have boosted company’s growth,

organically also the company has shown good growth. Organically

company has grown at 40% rate for last few years.

SYSTIME acquisition

SYSTIME is the largest acquisition till date of KPIT Cummins in its

decade long acquisition history. At the time of acquisition in 2010,

Systime:

SYSTIME had revenue of $50mn. Systime is the world's largest JD

Biggest bet till

Edwards solution provider, with manufacturing industry focused

now

offerings. This has further strengthened manufacturing and energy &

utilisation vertical of company as JDE is highly preferred in these

verticals.

With Systime's strong client base in manufacturing sector, including

large manufacturers such as France's Lafarge SA and U.S.-based

industrial gases maker Praxair Inc, it provides strong cross-selling

opportunity to the company.

This acquisition adds-up to the company’s Oracle-based consulting

and services business, making it a $125mn business for FY12. Also

company gets head-start in emerging geography, Brazil, where

Systime is an established player.

Although Systime has lower EBITDA margins compared to company’s

margins, KPIT could improve those with operational levers like off-

shoring, pyramid restructuring and other cost cutting majors. Also it

represents good cross-selling opportunity to KPIT and Systime

customers.

Strong and diversified customer portfolio

KPIT has strong client portfolio with more 176 active clients and 69

clients with run rate more than $1mn. It has been adding 3-4 active

clients every quarter from different verticals and service portfolio.

Include values in the chart below

180 80

69

65

175 70

59

170 54 60

51

48

165 40 40

50

160 40

176

172

155 169 30

163 165

150 159 20

155

152

145 10

140 0

Q3FY11 Q4FY11 Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2Fy13

No. of Active Customers Customers with run rate of >$1Mn

Four-S Research 16

17. Company Report: KPIT Cummins 31 Oct 2012

Dependency on its top client, Cummins, is also drastically come

down in last 1-2 years. From almost 25% business coming from

Cummins in Q3FY11 it has come down to 19.7% in Q2FY13.

Strong growth potential with $1bn target for FY17

32-35% growth expected in FY13…

The company has the guidance of 32-35% growth in FY13 which is

better than most of major-mid cap IT companies expected growth in

current environment. KPIT plans to achieve this with maintaining

Company edge in auto, mfg and utility sector and driving the growth with

expected to service offering with domain expertise as a differentiator.

outperform its

The company has recently (in last 9 months) closed 3 $20mn+ deals

guidance

and expects similar deal flow from their focused verticals in the

future. The company more than doubled the growth the top-line in

last two years from $154mn in FY10 to $309mn in FY12 with major

boost coming from SAP and auto segments.

FY17 vision to reach $1bn

KPIT has set a vision to become $1bn revenue company by FY17,

with target to achieve EBITDA margin of 18% up from 14.5%. With

strong vertical focused growth and best in class practices in Auto

embedded, SAP and Oracle, company should achieve the target with

the help of inorganic means and organic growth.

Four-S Research 17

18. Company Report: KPIT Cummins 31 Oct 2012

Operational performance

Focus on productivity improvement, Systime margins improve

The company is showing positive developments in productivity

factors. Systime had EBITDA margins of 5.5% at time of acquisitions

compared to the company’s 15% which had impacted on company’s

Systime margins. But as Systime integration is happening one can see

integration positive trend in its margins.

pushing its

In Q4FY12 without SYSTIME EBITDA margin was ~17%, but

margins up

SYSTIME itself had margin of 10%, bringing down overall EBITDA

margin to 16%. With continued successful integration and increased

offshore revenue from SYSTIME the productivity should move up.

Also the company also has other levers available with them to

increase the margins. By flattening the organisation pyramid further

i.e. increasing fresher/experience ratio and improved utilisation on

organisational level could further increase in profitability of the

company.

Improvement in the utilization visible

Utilisation

100%

94.5% 94.7%

95% 90.7% 91.3%

90.2% 90.6%

89.1%

90%

85%

80%

74.3% 74.1%

75% 72.8% 71.9%

71.2%

69.9%

70% 67.6%

65%

60%

Q3FY11 Q4FY11 Q1 FY12 Q2FY12 Q3FY12 Q4 FY12 Q1 FY13

Onsite Utilisation Offshore Utilisation

KPIT is on the mid to lower side of utilisation level if one compares it

to its peers (NIIT 78-79%, Polaris 80%, Persistent 73%, Mindtree

72%). But the company is trying to improve this shortcoming with

Utilisation rate increasing utilisation on both onsite and offshore side.

seen uptrend

Company’s efforts are getting some positive results as offshore

utilisation has gone up from 67.6% in Q3FY11 to 74.1% in Q1 GY13

and 89.1% onsite utilisation in Q3FY11 to 94.7% in Q1 FY13.

Although company is showing this positive trend, it still has plenty of

Four-S Research 18

19. Company Report: KPIT Cummins 31 Oct 2012

ground to catch to come close to its top peers.

Increased Off-shoring required

KPIT has high amount revenue coming revenue coming from onsite

which is in the ratio of 52-53% in recent quarters. This ratio has

Off-shoring to

improve been on growing trend lately increasing from 43% in Q4 FY11 to

more than 53% in Q2 FY13. This growth is has major contribution

margins

from SAP SBU which had most of the project in the implementation

phase. Also acquired company has more onsite revenue compared to

any KPIT.

In the coming days company is expected to improve onsite:offshore

revenue ratio with increasing offshoring. And existing onsite

implementation project going into maintainance phase will also help.

Onsite Revenue

55% 54%

53%

53% 52%

51%

49% 48%

47%

47%

44%

45% 43%

43%

41%

39%

37%

35%

Q4FY11 Q1 FY12 Q2FY12 Q3FY12 Q4 FY12 Q1 FY13 Q2 FY13

Improvement in organisational pyramid

The Company can also use some other majors to improve the

productivity such as flattening the organisational pyramid. As of now

it has more laterals working in the projects and fewer freshers as

compared to its peers. Company is looking to improve this ratio with

increasing fresher recruitment.

Four-S Research 19

24. Company Report: KPIT Cummins 31 Oct 2012

About Four-S Services

Founded in 2002, Four-S Services is a financial boutique providing Research, Financial

Consulting and Investment Banking services. We have executed more than 100+ mandates

across diverse range of industries for Indian as well as global companies, investment firms

and private equity and venture capital firms.

Our clients value our focused, actionable advice which is based on deep domain expertise in

Education, Financial Services, Media & Entertainment, Healthcare, Consumer Goods,

Automotive, Energy, Logistics and Manufacturing. For further information on the company

please visit www.four-s.com

Disclaimer

The information contained herein has been obtained from sources believed to be reliable but is not

necessarily complete and its accuracy cannot be guaranteed. No representation, warranty, guarantee

or undertaking, express or implied, is made as to the fairness, accuracy or completeness of any

information, projections or opinions contained in this document. Four-S Services Pvt. Ltd. will not

accept any liability whatsoever, with respect to the use of this document or its contents. This company

commissioned document has been distributed for information purposes only and does n ot constitute or

form part of any offer or solicitation of any offer to buy or sell any securities. This document shall not

form the basis of and should not be relied upon in connection with any contract or commitment

whatsoever. This document is not to be reported or copied or made available to others.

Four-S may from time to time solicit from, or perform consulting or other services for any company

mentioned in this document.

For further details/clarifications please contact:

Alok Somwanshi Ajay Jindal

Alok.somwanshi@four-s.com Ajay.jindal@four-s.com

Tel: +91-22-42153659 Tel: +91-22-42153659

Four-S Research 24