Sales tax changes, IFRS adoption concern transportation CFOs

•

0 likes•967 views

CFOs at transportation companies are wary of potential sales tax changes to service transactions, as well as International Financial Reporting Standards (IFRS) implementation. This infographic is based on our semiannual CFO Survey and focuses in on the industry’s state of mind. View the survey - http://gt-us.co/1xFWKsw

Recommended

Recommended

More Related Content

Viewers also liked

Viewers also liked (15)

Similar to Sales tax changes, IFRS adoption concern transportation CFOs

Similar to Sales tax changes, IFRS adoption concern transportation CFOs (20)

More from Grant Thornton LLP

More from Grant Thornton LLP (20)

Recently uploaded

Recently uploaded (20)

Sales tax changes, IFRS adoption concern transportation CFOs

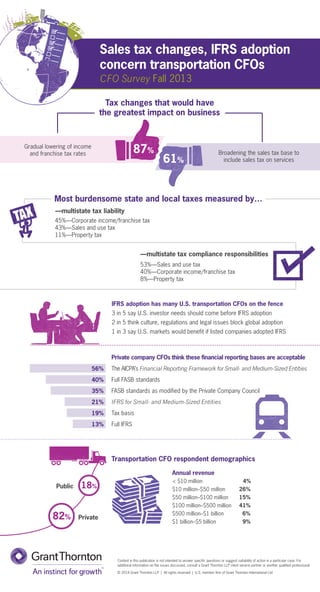

- 1. Sales tax change s, IFRS adoption concern transportation CFOs CFO Survey Fall 2013 Tax changes that would have the greatest impact on business Gradual lowering of income and franchise tax rates Broadening the sales tax base to include sales tax on services 87% 61% Most burdensome state and local taxes measured by… —multistate tax liability 45%—Corporate income/franchise tax 43%—Sales and use tax 11%—Property tax —multistate tax compliance responsibilities 53%—Sales and use tax 40%—Corporate income/franchise tax 8%—Property tax IFRS adoption has many U.S. transportation CFOs on the fence 3 in 5 say U.S. investor needs should come before IFRS adoption 2 in 5 think culture, regulations and legal issues block global adoption 1 in 3 say U.S. markets would benefit if listed companies adopted IFRS ................................................................................................................................................................. Private company CFOs think these financial reporting bases are acceptable The AICPA’s Financial Reporting Framework for Small- and Medium-Sized Entities Full FASB standards FASB standards as modified by the Private Company Council IFRS for Small- and Medium-Sized Entities Tax basis Full IFRS ................................................................................................................................................................. Transportation CFO respondent demographics Annual revenue < $10 million 4% $10 million–$50 million 26% $50 million–$100 million 15% $100 million–$500 million 41% $500 million–$1 billion 6% $1 billion–$5 billion 9% Public 18% Private 82% 56% 40% 35% 21% 19% 13% Content in this publication is not intended to answer specific questions or suggest suitability of action in a particular case. For additional information on the issues discussed, consult a Grant Thornton LLP client service partner or another qualified professional. © 2014 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd