Paradip CALL GIRL❤7091819311❤CALL GIRLS IN ESCORT SERVICE WE ARE PROVIDING

Sales management

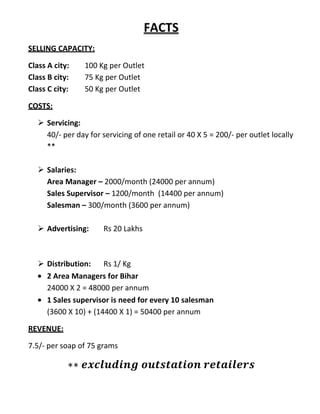

1. FACTS

SELLING CAPACITY:

Class A city: 100 Kg per Outlet

Class B city: 75 Kg per Outlet

Class C city: 50 Kg per Outlet

COSTS:

Servicing:

40/- per day for servicing of one retail or 40 X 5 = 200/- per outlet locally

**

Salaries:

Area Manager – 2000/month (24000 per annum)

Sales Supervisor – 1200/month (14400 per annum)

Salesman – 300/month (3600 per annum)

Advertising: Rs 20 Lakhs

Distribution: Rs 1/ Kg

2 Area Managers for Bihar

24000 X 2 = 48000 per annum

1 Sales supervisor is need for every 10 salesman

(3600 X 10) + (14400 X 1) = 50400 per annum

REVENUE:

7.5/- per soap of 75 grams

2. FINDINGS

Class A City: 200,000 Kg

100 Kg per Outlets 200,000/100 = 2000 Outlets

Class B City: 80,000 Kg

75 Kg per Outlets 80,000/75 = 1067 Outlets

Class C City: 260,000 Kg

50 Kg per Outlets 260,000/50 = 5200 Outlets

Total Production: 5,40,000 Kg for 8267 Outlets

Total Possible Revenue: 5,40,000 X 100 = 5,40,00,000

(1 kg=7.5 X 1000/75=100/-)

Expenditure =

20,00,000 (Advertising cost) + 540,000 (Distribution Cost) + 2 X 24,000

(2 Area Mgr. yearly salary) + 200 X 8267 (Servicing Cost for Outlets) =

42,41,400

Marketing Expenditure:

For 10% of turnover i.e., 54,00,000

54,00,000 – 42,41,400 = 11,58,600

For 15% of turnover i.e., 81,00,000

81,00,000 – 42,41,400 = 38,58,600

Total no. 0f Squads the company can afford is

11,58,600/50400 = 23 Approx. to 38,58,600/50400 = 76 Approx.

* 1 Squad = 10 Salesmen and 1 Supervisor.

3. Solutions of the questions:

To minimize the cost we take least possible no. of Squad 23 (i.e., 230

Salesmen and 23 Supervisors) and divide it by total no. of Outlets

8267 / 230 = 36 Outlets (Approx)

So, every Salesmen is ready to manage 36 Outlets than Salesforce is ready for

8,280 Outlets.

Territories:

Class A city = 2000/36 = 5 Squad

Class B city = 1067/36 = 3 Squad

Class C city = 5200/36 = 14 Squad

* Total = 23 Squad for 8267

Cost to Management:

230 X 3600 + 23 X 14400 = 11,59,200

* Total Management Expenditure = 42,41,400+ 11,59,200 = 54,00,200 which

is 10.0003 % of Total Revenue 5,40,00,000.

Sales Target per Salesman:

Class A city 200,000 Kg / 50 (Salesman) = 4000 kg

Class B city 80,000 Kg / 30 (Salesman) = 267 kg

Class C city 260,000 Kg / 140 (Salesman) = 1587 kg