1. FINANCIAL TIMES WEDNESDAY DECEMBER 9 2009 ★ 13

Analysis

The G2: the key to CO2

ChinaUS

5,880m

Share of global

emissions

19.9%

6,414m

Share of

global

emissions

15.9%

Europe

(OECD)

4,405m

4,519m

India

1,311m

2,115m

Russia

1,729m

1,978m

Africa

1,008m

1,409m

Japan

1,227m

1,157m

Canada

614m

731m

Brazil

390m

682m

South

Korea

536m

680m

Mexico

416m

557m

530m

Passenger cars per 1,000 people

2005

Domestic and international civil aviation

2004 (passenger km)

2007

CO2 emission intensity in iron and steel production

2007 (tonnes of CO2 equivalent per tonne of output)

World share of CO2 emissions from iron and steel sector

2007

Electricity generation from coal (%)

CO2 emissions per kWh of electricity and heat output

2007 (grammes of CO2 per kilowatt hour)

Estimated emissions created by manufacturing traded goods

US China

World share of CO2 emissions

from road transport

2007

Electricity generation from renewable energy (%)

Energy demand per capita (tonne of oil equivalent)

461 15

5.7%31.6%

1,160bn 176bn

8.5%57.2%

2007 (tonnes of CO2)

39m

2.5%

549

1.4bn

758

Radical changes required

CO2 emissions (tonnes)

6,319m

Share of global

emissions

21.4%

2005

7.3bn

tonnes of

CO2 equivalent of all

greenhouse gases

(including CO2)

2005

7.1bn

tonnes of

CO2 equivalent of all

greenhouse gases

(including CO2)

0.96

54.2%

2.51

Australia &

New Zealand

455m

China’s emissions created by manufacturing goods exported to the USUS emissions created by manufacturing

goods exported to China

Sources: Energy Information Administration; Ecofys; IEA/OECD; UN; IMF; World Bank; Yungfeng Y and Laike Y,‘CO2 Emissions Embodied in China-US Trade’, Chinese Journal of Population, Resources and Environment (2009, vol 3) Graphic: Natalie Croker

All references to CO2 emissions are energy related

The US pledge

China’s pledge

World share of CO2 emissions from domestic aviation

2007

Top bar in each chart

2030 IEA

‘business-as-usual’

forecast

US

China

US

China

US

China

2030 EIA

‘business-as-usual’

forecast

20072007

Key

World total

Key

49%

7.6

5.7 2.0

1.5

9%

81%

15%

50% 75%

16% 33%

46%

18%

2.66.5

23%

26%

To cut greenhouse gases by 17%

of its 2005 levels by 2020

With 8% annual

growth in GDP

2020

14.2bn

tonnes of

CO2 equivalent

2020

5.9bn

tonnes of

CO2 equivalent

Reduction of emission intensity

(greenhouse gas emissions per

unit of gross domestic product)

by 40-45% in 2020 compared

with 2005 levels*

11,730m

Share of global emissions

29.0%

* The chart shows GHG emissions forecasts

assuming a 45% cut in emissions intensity; International

Monetary Fund growth forecasts for 2009-2011; and 8%

annual average GDP growth for 2011-2020

Rest of

the world

World total

5,223m

29,513m

7,883m

40,385m

2007

2030

forecast

Big hitters, big emitters

* Curbs keep atmospheric concentrations

of greenhouse gases at 450 parts per million, the

level believed consistent with a global average

temperature increase of about 2˚C

2030 IEA forecast

if emissions

curbs in place*

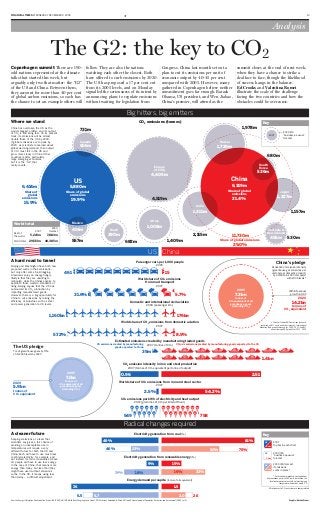

China has overtaken the US as the

world’s biggest emitter, and its output

of CO2 is still rising fast. On its present

track, its emissions will be almost

double those of the US by 2030.

If global emissions are to peak by

2020, as scientists concerned about

global warming demand, then output

of CO2 must fall in the US and

grow more slowly in China. Other

countries matter, particularly

large emerging economies,

but it is the “G2” that

really counts.

Where we stand

Beijing and Washington have both now

proposed curbs in their emissions –

but only after some footdragging.

Americans enjoy an energyhungry

lifestyle that they are unwilling to

relinquish; while the Chinese aspire to

approach those western standards of

living. Beijing argues that the US has

outsourced its CO2 production by

importing manufactured goods.

However, there is a big opportunity for

China to cut emissions by raising the

efficiency of industries such as steel

and power generation to US levels.

A hard road to travel

Copenhagen summit There are 190

odd nations represented at the climate

talks that started this week, but

arguably only two that matter: the “G2”

of the US and China. Between them,

they account for more than 40 per cent

of global carbon emissions, so each has

the chance to set an example others will

follow. They are also the nations

watching each other the closest. Both

have offered to curb emissions by 2020.

The US has proposed a 17 per cent cut

from its 2005 levels, and on Monday

signalled the seriousness of its intent by

announcing plans to regulate emissions

without waiting for legislation from

Congress. China last month set out a

plan to cut its emissions per unit of

economic output by 4045 per cent

compared with 2005. However, many

gathered in Copenhagen believe neither

commitment goes far enough. Barack

Obama, US president, and Wen Jiabao,

China’s premier, will attend as the

summit closes at the end of next week,

when they have a chance to strike a

deal face to face, though the likelihood

of success hangs in the balance.

Ed Crooks and Valentina Romei

illustrate the scale of the challenge

facing the two countries and how the

obstacles could be overcome.

Keeping emissions at a level that

scientists say gives a fair chance of

avoiding an unacceptable rise in

temperatures will require a very

different future for both the US and

China. Each will have to use much less

coalfired electricity, for example, and

opt instead for more renewables. Above

all, people will have to use less energy.

In the case of China, that means more

energy than today, but less than they

might have used without emissions

curbs. In the US, it means using less

than today – a difficult adjustment.

A cleaner future