1. IIAM ERM & IA - DSK Leong

2016

1

ERM AND INTERNAL AUDITING

INTERNAL AUDIT DIVISION

David S K Leong

BCA ,CA(NZ), CA (M), ACIB (UK), MBA

(Henley), CIA(US), CMIIA.

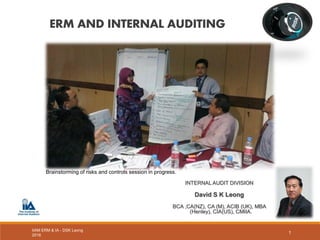

Brainstorming of risks and controls session in progress.

2. Brief Introduction & Background

David S K Leong

BCA ,CA(NZ), CA (M),ACIB (UK), MBA (Henley), CIA(US), CMIIA.

IIAM ERM & IA - DSK Leong

2016

2

HSBC Malaysia Bhd. (1980-2005) serving as Risk Manager, Strategic

Planner, Chief Internal Auditor & Head, Sarbanes-Oxley Project.

Kuwait Finance House (Malaysia) Bhd. (2005-11) – Chief Officer, Internal

Audit.

Bank Islam Malaysia Bhd. (2012-2014)– Chief Internal Auditor. (Senior

General Manager)

Credit Guarantee Corporation Malaysia Bhd. – Director, Internal Audit.

(Total of 35 years in banking of which 12 years as Chief Internal Auditor.)

Additional :

Member of Board of Governors, Institute of Internal Auditors, Malaysia.

Deputy Chairman, IIAM’s Research, Technical & Advisory Committee..

Examiner, Asian Institute of Chartered Bankers.

3. OIC Current Accounts/Savings, HSBC, Johor Bahru. 4 years

OIC, Trade Finance, HSBC Kuching, Sarawak -4 years.

Assistant Manager Marketing, HSBC Kuching, Sarawak - 2years

Credit Manager, HSBC, Kota Kinabalu, Sabah - 4 years

Bank Branch Manager HSBC Bank, Labuan -2.5 years

Manager Risk & Policy, HSBC Malaysia, Kuala Lumpur. -4 years

Head of Strategy, HSBC Malaysia, Kuala Lumpur -1 year

CIA, HSBC Malaysia -3 years.

IIAM ERM & IA - DSK Leong 2016 3

HSBC Work Experience 1980 - 2005

4. Risk Management Experiences

The Nightmares!

IIAM ERM & IA - DSK Leong

2016

4

No risk management !

Want to go own way (i.e. no way)!

No definition of risk. (i.e. don’t know)

Don’t know what is risk!

Uses new unproven model risk.

Ad hoc and unorganized approach/incomplete coverage.

No monitoring/follow-up of controls.

Inadequate risk staffing and skills

Excessive power/arrogance

Lack of power!

Very defensive!

Don’t want to be audited.

Any more?

5. SIMPLE SURVEY

How many don’t have Risk Management function?

How many have not audited Risk Management?

How many have audited Risk Management?

How many of these are really happy with their Risk Management

Audit?

How many are really comfortable with the Risk Management activities?

How many have Risk Management Divisions that really manage

important risks effectively?

IIAM ERM & IA - DSK Leong 2016 5

6. IIAM ERM & IA - DSK Leong

2016

Page 6

1. Your internal audit findings are challenged 70 % of the time?

2. Your internal audit findings are 95% accepted all the time?

3. Your internal audit recommendations get implemented only 50% of the time?

4. Your internal audit recommendations are implemented 90 % even before

presentation to the Board.

5. Your internal auditors’ performance and remuneration are assessed by

management.

6. Your internal auditors’ performance and remuneration are assessed by the

Board.

7. You have a higher than average attrition rate among your internal auditors

than in the organization.

8. You have several other staff requesting to join internal audit department.

HONESTLY, WHAT SITUATION ARE YOU IN?

7. IIAM ERM & IA - DSK Leong

2016

Page 7

Most Frequent Experience:

CRO says, “We have Enterprise-wide Risk

Management!” –when actually he does not even

know what is risk.

CRO says, “CIO will look after IT Risk Management.

RM don’t have the IT expertise.”

CRO says: “ We have a ERM Policy.” But on paper

and in name only but not practiced. No

development.

CRO says: “We cannot introduce ERM because

Head Office overseas should lead such an

initiative.”

8. IIAM ERM & IA - DSK Leong

2016

Page 8

1. Must be Enterprise –wide (From Top to Bottom)

2. There must not be any “Golden Boy” unit.

3. Includes All Risks (Strategic/Operational/Financial/Compliance/Governance)

4. Focuses on Key Risks. ( Not more than 30-50 Biggest Risks)

5. Integrates Across All Risk Types. (Not Siloed-approach)

6. Aggregated at the Enterprise Level (based on the Risk Appetite/HEAT Map).

7. Decision-making Required to Reduce/Treat Risk.

8. Appropriate Risk Disclosures. (Show how much shareholder value can be

damaged.)

9. Measure Value Impacts and Opportunity Impact.

10.Focuses on Main Stakeholders (Shareholders).

Source: Adapted from Jared Wade

10 Absolute Essential Features of ERM

9. IIAM ERM & IA - DSK Leong

2016

9

In other words,

Do you have these?

10. Benefits in Layman’s Language to the Company with an

Integrated Risk Framework and ERM Program

IIAM ERM & IA - DSK Leong

2016

Page 10

Risk Management becomes easy to apply. We will have substance instead of

form.

ERM gives the Board better real assurance over internal controls

All departments work on the same internationally recognized methodology.

Risk registers are easily available online to all users.

We have less work and less stress (no duplicated controls).

Each entity will know their main risks and controls. This leads to more

focused work.

Entities will pass internal audits.

Internal audits reports will be comprehensible.

Company will suffer less losses make higher profits and be competitive.

Company has more time for strategy and be more focused.

Company will have compliance with Law, regulations and policies.

11. IIAM ERM & IA - DSK Leong

2016

11

1. Must be Enterprise–wide.

1. Led by the Board and CEO. And have a Project Champion.

2. Must Involve all Risk Areas.

3. Participation and Buy-in from all material areas on Initial Risk

Universe Assessment.

4. Participation and Mind-set must be integrated into operations,

remuneration and culture.

5. Supported and complemented by Internal Audit.

6. All use common methodology and be solution oriented.

12. 2. There must not be any “Golden Boy” unit

IIAM ERM & IA - DSK Leong

2016

12

All are Included without Exception.

No “Special Treatment” even for “star performers”.

(This is exemplified by the case in Barings Bank in 1996 in which

the Bank eventually collapsed. Barings

Singapore was so profitable that Risk Management

and Internal Audit were told to go lightly on Nick

Leeson, the “Wonder Boy”. Loss:GBP860 Million.

Another tell-tale sign:

The “only expert” in complicated derivatives trading

in the 2008 Societe Generale Bank case – a

GBP3.7 Billion loss).

Enron 2004 –”The Smartest Guys in the Room.”

13. 3. Includes All Risks (Strategic/Operational/Financial/

Compliance/Governance)

Aligning All the Main Components –Making Sure We All look at the

Same Things to Achieve Corporate Objectives.

Vision,

Strategy,

Corporate

Objectives

Risk

Manage-

ment

Training/

HR

Key

Performance

Indicators

Internal

Audit

Performance

Measure-

ment

IIAM ERM & IA - DSK Leong 2016 Page 13

Achieve

Corporate

ObjectivesSTRATEGIC DIRECTION

YEARLY BUDGETS

RISK APPETITE

14. IIAM ERM & IA - DSK Leong

2016

14

Where are

your risks?

All these

have to be

coordinated!

15. IIAM ERM & IA - DSK Leong

2016

15

5. Integrates Across All Risk Types. (Not Siloed-

approach)

Definition of Risk / What is Risk?

“ The possibility of an event occurring that will have an impact

on the achievement of objectives. Risk is measured in terms of

impact and likelihood.”

IPPF Glossary

In ISO 31000-2009 – “Risk is Uncertainty Over Objectives.”

By having the same methodology, everyone speaks the same

language and allows for aggregation of the enterprise’s risk.

16. IIAM ERM & IA - DSK Leong

2016

16

4. Focuses on Key Risks. (30-50 Biggest Risks)

These should be the risks that keep you awake at night.

Once these risks are identified using a collaborative brain-storming

session for all units using a common methodology measuring risks in

terms of impact and probability.

Are All Risks Covered? The ERM method prescribes inclusion of all

major risks and measures effectiveness of their treatment. This

requires workers’ participation.

Are you having excessive procedures? Board and Management

attention followed by action are aligned on real risks; and their

treatment and the monitoring. The process will find many traditional

processes are actually redundant. Therefore SOPs can be

streamlined/processes become efficient.

Are your operations guys clueless and dissatisfied?

Implementers of ERM and workers often find more meaning in what they

do and are motivated because they now understand how to get real value

for their time. They know what and why they had to do and what auditors

will audit them on.

17. IIAM ERM & IA - DSK Leong

2016

17

Use the “HEAT MAP” tool to help disseminate risk

assessment methodology.

18. 6. Aggregated at the Enterprise Level (Set the Risk Appetite/

HEAT Map). HEAT MAP. Where the Risks are!

TABLE A:

HEAT MAP (Operations)

<RM1000/

INSIGNIFICANT)

RM1000-9,999

(MINOR)

RM10,000-49,999

(MODERATE)

RM50,000-199,999

(MAJOR)

>RM200,000

(Catastrophic)

Key

Catastrophic/High

Low IMPACT Very High

Medium

1 2 3 4 5

Low

ALMOST CERTAIN (1-6 months)

LowLIKELIHOODVeryHigh

5 5.1 5.2 5.3 5.4 5.5

VERY PROBABLE (every 6-12 Months) 4 4.1 4.2 4.3 4.4 4.5

PROBABLE (Every 1-3 years 3 3.1 3.2 3.3 3.4 3.5

UNLIKELY (Every 4-10 years 2 2.1 2.2 2.3 2.4 2.5

RARE (Every more than 10 Years) 1 1.1 1.2 1.3 1.4 1.5

2..1

2..2

2..4

2.3

2

1.3

2

1.1

1.2

2

3.1

IIAM ERM & IA - DSK Leong

2016

18

Finding 2.4 is

plotted on

Heat Map

5.4: Denotes

probability 5,

Impact of 4.

19. 7. Decision-making by Management to Reduce/Treat

Risk.

IIAM ERM & IA - DSK Leong

2016

19

Once a material risk is identified, there are 4 “T s” of Risk

Mitigation.

I. Treat (Implement Control to reduce/prevent the occurrence)

II. Transfer ( Reduce impact by transferring risk to another entity

or take out insurance/outsource.)

III. Terminate ( Abandoning /selling the business if risk impact is

deemed unbearable or cannot be controlled.)

IV. Tolerate – Accept the risk if within Risk Tolerance limits.

Action is taken is to ensure all risks accepted are within the risk appetite

(green) as shown in the following HEAT Map.

ERM is not to report risks only but to ensure correct control action is

taken.

Appraisal of performance is on action taken effectively.

20. IIAM ERM & IA - DSK Leong

2016

20

7. IMPACT OF CONTROLS ON TREATED RISKS (RESIDUAL RISK)

TABLE A:

HEAT MAP (Mill Operations)

<RM1000/

INSIGNIFICANT)

RM1000-9,999

(MINOR)

RM10,000-49,999

(MODERATE)

RM50,000-199,999

(MAJOR)

>RM200,000

(Catastrophic)

Key

Catastrophic/High

Low IMPACT Very High

Medium

1 2 3 4 5

Low

ALMOST CERTAIN (1-6 months)

LowLIKELIHOODVeryHigh

5 5.1 5.2 5.3 5.4 5.5

VERY PROBABLE (every 6-12 Months) 4 4.1 4.2 4.3 4.4 4.5

PROBABLE (Every 1-3 years 3 3.1 3.2 3.3 3.4 3.5

UNLIKELY (Every 4-10 years 2 2.1 2.2 2.3 2.4 2.5

RARE (Every more than 10 Years) 1 1.1 1.2 1.3 1.4 1.5

Inherent

Risk

Residual

Risk

21. IIAM ERM & IA - DSK Leong

2016

21

OVERALL COMPANY:

HEAT MAP

<RM1000/

INSIGNIFICANT)

RM1000-9,999(MINOR)

RM10,000-49,999

(MODERATE)

RM50,000-199,999

(MAJOR)

>RM200,000

(Catastrophic)

Key Catastrophic

/High

Low IMPACT

Very High

Medium

1 2 3 4 5Low

ALMOST CERTAIN

(1-6 months)

LowLIKELIHOODVeryHigh

5 5.1 5.2 5.3 5.4 5.5

VERY PROBABLE

(every 6-12 Months)

4 4.1 4.2 4.3 4.4 4.5

PROBABLE (Every 1-

3 years

3 3.1 3.2 3.3 3.4 3.5

UNLIKELY (Every 4-

10 years

2 2.1 2.2 2.3 2.4 2.5

RARE (Every more

than 10 Years)

1 1.1 1.2 1.3 1.4 1.5

OVERALL COMPANY:

HEAT MAP

<RM1000/

INSIGNIFICANT)

RM1000-9,999

(MINOR)

RM10,000-

49,999

(MODERATE)

RM50,000-

199,999

(MAJOR)

>RM200,000

(Catastrophic)

Ke

y Catastrophic/High

Low IMPACT

Very High

Medium

1 2 3 4 5

Low

ALMOST CERTAIN (1-6

months)

LowLIKELIHOODVeryHigh

5

5

.

1

5

.

2

5

.

3

5

.

4

5

.

5

VERY PROBABLE (every 6-

12 Months)

4

4

.

1

4

.

2

4

.

3

4

.

4

4

.

5

PROBABLE (Every 1-3

years

3

3

.

1

3

.

2

3

.

3

3

.

4

3

.

5

UNLIKELY (Every 4-10

years

2

2

.

1

2

.

2

2

.

3

2

.

4

2

.

5

RARE (Every more than 10

Years)

1

1

.

1

1

.

2

1

.

3

1

.

4

1

.

5

OVERALL COMPANY:

HEAT MAP

<RM1000/

INSIGNIFICANT)

RM1000-9,999

(MINOR)

RM10,000-

49,999

(MODERATE)

RM50,000-

199,999

(MAJOR)

>RM200,000

(Catastrophic)

Ke

y Catastrophic/High

Low IMPACT

Very High

Medium

1 2 3 4 5

Low

ALMOST CERTAIN (1-6

months)

LowLIKELIHOODVeryHigh

5

5

.

1

5

.

2

5

.

3

5

.

4

5

.

5

VERY PROBABLE (every 6-

12 Months)

4

4

.

1

4

.

2

4

.

3

4

.

4

4

.

5

PROBABLE (Every 1-3

years

3

3

.

1

3

.

2

3

.

3

3

.

4

3

.

5

UNLIKELY (Every 4-10

years

2

2

.

1

2

.

2

2

.

3

2

.

4

2

.

5

RARE (Every more than 10

Years)

1

1

.

1

1

.

2

1

.

3

1

.

4

1

.

5

OVERALL COMPANY:

HEAT MAP

<RM1000/

INSIGNIFICANT)

RM1000-9,999

(MINOR)

RM10,000-

49,999

(MODERATE)

RM50,000-

199,999

(MAJOR)

>RM200,000

(Catastrophic)

Ke

y Catastrophic/High

Low IMPACT

Very High

Medium

1 2 3 4 5

Low

ALMOST CERTAIN (1-6

months)

LowLIKELIHOODVeryHigh

5

5

.

1

5

.

2

5

.

3

5

.

4

5

.

5

VERY PROBABLE (every 6-

12 Months)

4

4

.

1

4

.

2

4

.

3

4

.

4

4

.

5

PROBABLE (Every 1-3

years

3

3

.

1

3

.

2

3

.

3

3

.

4

3

.

5

UNLIKELY (Every 4-10

years

2

2

.

1

2

.

2

2

.

3

2

.

4

2

.

5

RARE (Every more than 10

Years)

1

1

.

1

1

.

2

1

.

3

1

.

4

1

.

5

OVERALL COMPANY:

HEAT MAP

<RM1000/

INSIGNIFICANT)

RM1000-9,999

(MINOR)

RM10,000-

49,999

(MODERATE)

RM50,000-

199,999

(MAJOR)

>RM200,000

(Catastrophic)

Ke

y Catastrophic/High

Low IMPACT

Very High

Medium

1 2 3 4 5

Low

ALMOST CERTAIN (1-6

months)

LowLIKELIHOODVeryHigh

5

5

.

1

5

.

2

5

.

3

5

.

4

5

.

5

VERY PROBABLE (every 6-

12 Months)

4

4

.

1

4

.

2

4

.

3

4

.

4

4

.

5

PROBABLE (Every 1-3

years

3

3

.

1

3

.

2

3

.

3

3

.

4

3

.

5

UNLIKELY (Every 4-10

years

2

2

.

1

2

.

2

2

.

3

2

.

4

2

.

5

RARE (Every more than 10

Years)

1

1

.

1

1

.

2

1

.

3

1

.

4

1

.

5

OVERALL COMPANY:

HEAT MAP

<RM1000/

INSIGNIFICANT)

RM10,000-

49,999

(MODERATE)

RM50,000-

199,999

(MAJOR)

>RM200,000

(Catastrophic)

Ke

y Catastrophic/High

Low IMPACT

Very High

Medium

1 2 3 4 5

Low

ALMOST CERTAIN (1-6

months)

LowLIKELIHOODVeryHigh

5

5

.

1

5

.

2

5

.

3

5

.

4

5

.

5

VERY PROBABLE (every 6-

12 Months)

4

4

.

1

4

.

2

4

.

3

4

.

4

4

.

5

PROBABLE (Every 1-3

years

3

3

.

1

3

.

2

3

.

3

3

.

4

3

.

5

UNLIKELY (Every 4-10

years

2

2

.

1

2

.

2

2

.

3

2

.

4

2

.

5

RARE (Every more than 10

Years)

1

1

.

1

1

.

2

1

.

3

1

.

4

1

.

5

OVERALL COMPANY:

HEAT MAP

<RM1000/

INSIGNIFICANT)

RM1000-9,999

(MINOR)

RM10,000-

49,999

(MODERATE)

RM50,000-

199,999

(MAJOR)

>RM200,000

(Catastrophic)

Ke

y Catastrophic/High

Low IMPACT

Very High

Medium

1 2 3 4 5

Low

ALMOST CERTAIN (1-6

months)

LowLIKELIHOODVeryHigh

5

5

.

1

5

.

2

5

.

3

5

.

4

5

.

5

VERY PROBABLE (every 6-

12 Months)

4

4

.

1

4

.

2

4

.

3

4

.

4

4

.

5

PROBABLE (Every 1-3

years

3

3

.

1

3

.

2

3

.

3

3

.

4

3

.

5

UNLIKELY (Every 4-10

years

2

2

.

1

2

.

2

2

.

3

2

.

4

2

.

5

RARE (Every more than 10

Years)

1

1

.

1

1

.

2

1

.

3

1

.

4

1

.

5

Finance

Mill Operations

Marketing

Plantations

Compliance

Human Resources

7. See One Picture of the

Aggregated Risks of Your

Company

You can see one picture or drill down into

component areas, even specific issues, because

of consistency of risk methodology.

Overall Enterprise-Wide HEAT MAP

Based on COSO ERM & IIA’s IPPF

22. PART 2.

COSO – Enterprise-wide Risk

Management.

IIAM ERM & IA - DSK Leong

2016

22

23. IIAM ERM & IA - DSK Leong

2016

23

5. Where Do We Start?

Before we even implement anything,

We have to understand the methodologies used –ERM and IIA’s IPPF.

Risk Evaluation Objectives according to IPPF Standard 2130-A1.

24. 24

It Started in 1992 with the First Internal Control COSO Cube.

26. 26

COSO/COSO ERM in 7 Different Languages!

The World’s Best Known and Only Established ERM Framework for Integrated

Control.

27. IIAM ERM & IA - DSK Leong 2016 Page 27

COSO (1) Evolved into COSO-ERM (2004)

28. ERM Re-defined / Improved:

“… a process, effected by an entity's board of directors, management

and other personnel, applied in strategy setting and across the

enterprise, designed to identify potential events that may affect the

entity, and manage risks to be within its risk appetite, to provide

reasonable assurance regarding the achievement of entity objectives.”

Source: “COSO Enterprise Risk Management – Integrated Framework” 2004. COSO.

IIAM ERM & IA - DSK Leong

2016

28

So why Enterprise-wide Risk Management?

29. IIAM ERM & IA - DSK Leong 2016 Page 29

1992

2004

May 2013

The Development of the Three COSO Frameworks.

The 2013 COSO Framework (17 Principles) is the Best yet.

1992 COSO

has been

replaced

NEW!

30. IIAM ERM & IA - DSK Leong

2016

Page 30

A Quick View of the Overall

Framework that should be achieved.

33. Internal control is defined as follows:

“Internal control is a process, effected by an entity’s board of

directors, management, and other personnel, designed to

provide reasonable assurance regarding the achievement of

objectives relating to operations, reporting, and compliance”

“Internal Control—Integrated Framework.”

COSO Publication May 2013

IIAM ERM & IA - DSK Leong 2016 Page 33

The Requirement is Integrated Internal Control.

Board must

lead and

sponsor!

34. “The combination of processes and structures implemented by

the Board to inform, direct, manage and monitor the activities

of the organization towards achievement of its objectives.”

IPPF Glossary

IIAM ERM & IA - DSK Leong 2016 Page 34

Definition of Governance – What the

Board is now expected to do.

35. Specimens of Internal Audit Report

based on COSO (2013) Format.

IIAM ERM & IA - DSK Leong

2016

35

36. IIAM ERM & IA - DSK Leong

2016

36

CA02 Control Activities

No review performed on audit trail report for MYSTICS

system

Criteria

The BNM Audit in 2013 has highlighted on the absence of

Policy and Procedures on the requirement to review audit

trail in MYSTIC System (Issue No. 15). FIN has since

revised the Policy and Procedures effective 19MAR14 to

incorporate periodic revision of audit trail by officer.

Section 1.1 of Audit Trail Review for MYSTIC is to guide

FIN in the preparation of Audit Trail Report where the

system administrator is responsible for the review of audit

trail every month for at least two (2) modules.

Condition

However, Audit's observation was that the review of audit

trail for MYSTIC system was not implemented / carried out

as now required under Section 1.1.

Cause

a) Guideline was not strictly followed and enforced

accordingly.

b) Unawareness of staff in-charge on the

usefulness/benefits of audit trail in monitoring activities

of MYSTIC users and preventing fraud risks.

Risk (High)

a) Non-compliance with Section 1.1 of Audit Trail Review

for MYSTICS Manual.

b) System control lapses may go undetected.

FIN must ensure that the Audit Trail

Review for MYSTICS Manual are

adhered accordingly and to report to

Risk Management Department

(RMD) on any unusual activities

under incident reporting (if any).

Management’s Response:

We have reviewed the audit trail for

the month of March 2014, April

2014, May 2014, Jun 2014 and

July 2014 and have been

concurred by FC accordingly on 2

September 2014.

Target Date:

Implemented

Person Responsible:

Zahid Muhammad, Head of

Section

Detailed Audit Finding as per Implementation Guide 2410-1

37. IIAM ERM & IA - DSK Leong

2016

37

TABLE 1: COSO 5 COMPONENTS & 17 PRINCIPLES MATRIX

CONTROL ENVIRONMENT

1. The organization demonstrates a commitment to integrity and ethical values.

Answer: Yes. Board of Directors is committed to ethical and integrity values.

2. The board of directors demonstrates independence from management and exercises

oversight of the development and performance of internal control.

Answer: Yes. Board of Directors is independent and exercises oversight. New Board

members in 2014.

3. Management establishes, with board oversight, structures, reporting lines, and

appropriate authorities and responsibilities in the pursuit of objectives.

Answer: Yes. Board has established reporting lines and structures. In 2013, Board has

changed the external auditors to PwC.

4. The organization demonstrates a commitment to attract, develop, and retain

competent individuals in alignment with objectives.

Answer: FIN lost 6 experienced staff in 2013 and 2014 (including the Head of Department)

5. The organization holds individuals accountable for their internal control

responsibilities in the pursuit of objectives.

Finding IMP01: Absence of internal/manual attendance record for staff working during

public holidays

Opinion: Tightening of controls and discipline seems obvious given the nine control lapses in

this report.

RISK ASSESSMENT

6. The organization specifies objectives with sufficient clarity to enable the identification

and assessment of risks relating to objectives.

Opinion: This should be improved as staff do not seem to implement controls as they should.

7. Organization identifies risks to the achievement of its objectives across the entity and

analyzes risks as a basis for determining how the risks should be managed.

Opinion: The Identification of Risk is not adequate or systematic enough. Probably

coupled it with lack of responsibility, the control lapses occur.

8. The organization considers the potential for fraud in assessing risks to the

achievement of objectives.

Finding RA01: User ID (MYSTICS) logged in during staff's absence. (Medium Risk)

9. The organization identifies and assesses changes that could significantly impact the

system of internal control.

Answer: Yes. GST was highlighted to management.

CONTROL ACTIVITIES

10. The organization selects and develops control activities that contribute to the

mitigation of risks to the achievement of objectives to acceptable levels.

Yes: Controls are in manuals but not implemented. Hence, see findings in Principle No.12,

11. The organization selects and develops general control activities over technology to

support the achievement of objectives.

Finding CA05: No adjustments made for TPUB-i profit charged due to limitation in

Contract Financing Module (CFM-BOS) (Medium)

Finding CA08: Six (6) IDs of resigned staffs were not deactivated (Medium Risk)

12. The organization deploys control activities through policies that establish what is

expected and procedures that put policies into action.

Finding CA01: Inappropriate month end closing (High Risk)

Finding CA02: No review performed on audit trail report for Mystics System (High Risk)

Finding CA03: Non-compliance with Accounting Policy -Checklist not used (High Risk)

Finding CA04: Incomprehensive updates in Manual (Medium Risk)

Finding CA06: Wrong Preparation of Accounts: Written off asset was treated as loss on

disposal of asset. (Medium Risk)

Finding CA07: Security Cabinet containing cheque book was not locked. (Medium Risk)

INFORMATION & COMMUNICATION

13. The organization obtains or generates and uses relevant, quality information to

support the functioning of internal control.

See related comments in Principle No. 16.

14. The organization internally communicates information, including objectives and

responsibilities for internal control, necessary to support the functioning of internal

control.

Answer: Meetings are held with other internal parties.

15. The organization communicates with external parties regarding matters affecting the

functioning of internal control.

Answer: Yes. This is done with PwC, the external auditors.

MONITORING

16. The organization selects, develops and performs ongoing and / or separate

evaluations to ascertain whether the components of internal control are present and

functioning.

Answer: FIN will ensure the figures and information related to FIN are correct .

17. The organization evaluates and communicates internal control deficiencies in a

timely manner to those parties responsible for taking corrective action, including

senior management and the board of directors, as appropriate.

Answer: Yes, CGC as a whole communicate deficiencies but implementation is hampered

by staff quality and IT issues. See CA 03, 04, 05 and Finding Other 01 (Un-reconciled

receipts).

38. IIAM ERM & IA - DSK Leong

2016

38

Risk Rating and

Type

Reported this

Audit

Maximum for

Satisfactory

Maximum for

"Needs

Improvement"

High Risk 3 2 4

Medium Risk 6 6 6

Other Department

Risk

1 NA NA

Improvement 1 NA NA

TOTAL 11

Rating the Internal Audit Consistently/No Surprise Approach..

39. IIAM ERM & IA - DSK Leong

2016

39

“The former JP Morgan Chase trader known as the “London

Whale” has broken cover to say he was not responsible for the

scandal that lost the bank $6.2bn. In a letter sent late on Monday

night to news outlets including Financial News and Bloomberg,

Bruno Iksil said he was “instructed repeatedly” by his superiors to

carry out the trading strategy that led to the losses.”

Bruno Iksil (The “London Whale”)

The Independent

Does Senior Management (and Board) really know their Risk

Appetite?

(Mr Iksil is helping the US authorities bring a case against key figures at JP Morgan, but he is

not among those being prosecuted. JP Morgan lost USD 6.2 Billion and was fined USD 1

Billion by regulators.)

Jamie Dimon, JP Morgan’s

CEO.

40. Appeals court rules company

directors liable for offences

committed during their tenure

Published: 28 September 2015

IIAM ERM & IA - DSK Leong

2016

40

The Court of Appeal today ruled that Section 122(1) of the Securities

Industry Act 1983 (SIA) – which states that when an offence has been

committed under the act by a corporate body, a director or chief

executive officer (CEO) or one purporting to act in such a capacity for

the organisation is deemed liable – does not violate the Federal

Constitution.

The decision overturned the High Court’s ruling that the section was

unconstitutional when Transmile Group Bhd’s founder and former

CEO Gan Boon Aun and its former executive director Khiuddin

Mohd challenged the validity of a charge brought against them.

–

Is your

Board

aware of

this Risk?

41. IIAM ERM & IA - DSK Leong 2016 Page 41

Implication: Making COSO-ERM Thinking the Way of

Life for Achievement of Company Objectives.

5 Components 8 Components !

Is your Board &

Management

aware of COSO?

42. Implication: Changes Required for Internal

Audit

IA is prime mover and player in ERM

IIAM ERM & IA - DSK Leong

2016

42

Professional & Proactive Internal

Audit. (IIA qualified)

Risk-Based Internal Audit (Uses

COSO 2013).

Implement International

Professional Practices Framework

(IPPF) which require IA to give

assurance on effectiveness of the

governance, risk management and

internal control systems.

43. Will IA’s Participation in ERM compromise IA’s

Independence? ANSWER – NO.

IIAM ERM & IA - DSK Leong

2016

Page 43

44. Starting ERM Risk Assessment - How to Identify Risks in

Your Division?

IIAM ERM & IA - DSK Leong

2016

Page 44

•Brainstorming (Participation by implementers)

•Delphi System (Asking Experts)

•Monte Carlo Simulation (IT Program)

46. IIAM ERM & IA - DSK Leong

2016

46

• Identification of Risk

Universe.

• Organize Brainstorming

sessions in risk areas.

• Identify risks and identify

the controls.

• Document the high &

medium risks.

• Prepare each area’s top risks

and controls.

• Institute monitoring to

ensure identified controls

are implemented /working.

• Institute regular reporting to

ERM centre.

• Review controls and update

risk registers.

• Institute annual review

by Internal Audit.

• Internal Audit to test

ERM system in internal

audits of each area.

• Aggregate and update

quarterly reporting to

Risk Committee.

• Continuous training and

annual updating of Risk

Universe.

• Integrate into Strategic

review and annual

budgeting.

• Add stress testing to

ERM.

• Establish Scope and

Objectives of ERM

Project

• Establish ERM Project

Roles and Project

Structure.

• Identify key executives.

• Conduct training for key

individuals.

• Appoint CIA and Head of

ERM/CRO.

• Establish Risk Committee.

• Identify resources for

ERM.

47. In Summary:

Benefits of Coordinating the Company with an Integrated ERM

Program and IA

IIAM ERM & IA - DSK Leong

2016

Page 47

Risk Management becomes easy to apply. We will have substance instead of

form. Collaborative Risk Management achieved.

Internal audit recommendations become understandable and implemented.

ERM gives the Board better real assurance over internal controls.

All departments work on the same internationally recognized methodology.

Risk registers are easily available online to all users. Related risks are

identified. Redundant controls are eradicated.

We have less work and less stress (no duplicated controls).

Each entity will know their main risks and controls. This leads to more

focused work and efficiency. Logical and fair internal audits.

Entities will pass internal audits. More value-add from internal audits.

Company will suffer less losses make higher profits and be competitive.

Company has more time for strategy and be more focused.

Company will have compliance with Law, regulations and policies.

For manufacturers, better safety in the operations area.

Less staff turnover – Better staff Morale.

48. Final Take Away Pointers

IIAM ERM & IA - DSK Leong

2016

48

Look at Risks using COSO/COSO ERM Frameworks

Establish with AC the Risk Appetite and COSO ((2013)/COSOERM.

Do Risk Universe Analysis using Brainstorming

Emphasize the Biggest Risks and review every three months.

Do Internal Audit Planning using the COSO (2013) Framework.

Discuss with Auditees the use of COSO (2013) Framework.

Determine/Measure Risk using risk appetite set and risk registers.

Report risks based on Criteria, Condition Impact and Cause into High

and Medium Risks,.

Establish Real Cause with Auditees to recommend action.

Hold the person/entity with responsibility/authority accountable.

Be consistent with standards of evidence (No evidence, it’s an opinion)

Write report based on COSO (2013) format.

Be consistent with ratings across the board (No exception.)

If you have any serious opinion (e.g. corruption) to share, write a

management memorandum separately to Management or Board.