Retail, Mobile and OOH Summary

•

2 likes•951 views

This is a summarised version of the full Retail, Mobile and OOH presentation. The original presentation can be found here: http://www.slideshare.net/Posterscope/retail-mobile-and-ooh

Recommended

More Related Content

More from Posterscope

More from Posterscope (20)

Recently uploaded

Recently uploaded (20)

Retail, Mobile and OOH Summary

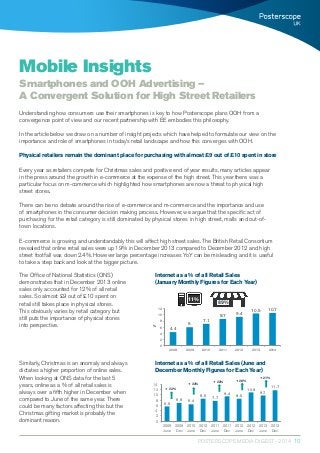

- 1. POSTERSCOPE MEDIA DIGEST - 2014 10 Understanding how consumers use their smartphones is key to how Posterscope plans OOH from a convergence point of view and our recent partnership with EE embodies this philosophy. In the article below we draw on a number of insight projects which have helped to formulate our view on the importance and role of smartphones in today’s retail landscape and how this converges with OOH. Physical retailers remain the dominant place for purchasing with almost £9 out of £10 spent in store Every year as retailers compete for Christmas sales and positive end of year results, many articles appear in the press around the growth in e-commerce at the expense of the high street. This year there was a particular focus on m-commerce which highlighted how smartphones are now a threat to physical high street stores. There can be no debate around the rise of e-commerce and m-commerce and the importance and use of smartphones in the consumer decision making process. However, we argue that the specific act of purchasing for the retail category is still dominated by physical stores in high street, malls and out-of- town locations. E-commerce is growing and understandably this will affect high street sales. The British Retail Consortium revealed that online retail sales were up 19% in December 2013 compared to December 2012 and high street footfall was down 2.4%. However large percentage increases YoY can be misleading and it is useful to take a step back and look at the bigger picture. The Office of National Statistics (ONS) demonstrates that in December 2013 online sales only accounted for 12% of all retail sales. So almost £9 out of £10 spent on retail still takes place in physical stores. This obviously varies by retail category but still puts the importance of physical stores into perspective. Similarly, Christmas is an anomaly and always dictates a higher proportion of online sales. When looking at ONS data for the last 5 years, online as a % of all retail sales is always over a fifth higher in December when compared to June of the same year. There could be many factors affecting this but the Christmas gifting market is probably the dominant reason. Mobile Insights Smartphones and OOH Advertising – A Convergent Solution for High Street Retailers 5.6 6.9 6.4 8.5 7.7 9.4 8.5 10.9 9.7 11.7 0 2 4 6 8 10 12 14 2009 June 2009 Dec 2010 June 2010 Dec 2011 June 2011 Dec 2012 June 2012 Dec 2013 June 2013 Dec + 23% + 33% + 22% + 28% + 21% Internet as a % of all Retail Sales (January Monthly Figures for Each Year) Internet as a % of all Retail Sales (June and December Monthly Figures for Each Year) 4.4 6 7.1 8.7 9.4 10.5 10.7 0 2 4 6 8 10 12 2008 2009 2010 2011 2012 2013 2014 % 11% 89% 4.4 6 7.1 8.7 9.4 10.5 10.7 0 2 4 6 8 10 12 2008 2009 2010 2011 2012 2013 2014 % 11% 89%

- 2. POSTERSCOPE MEDIA DIGEST - 2014 11 Smartphones are predominantly used for browsing not buying and play a major role in Influencing sales in physical stores When it comes to online sales it is laptops/PCs and in fact tablets over smartphones that are the key drivers of this. Data released by Affiliate Window for October 2013 demonstrated that m-commerce is growing rapidly with almost 23% of sales taking place on their affiliate web sites on mobile devices, double the 11% in October 2012. However of this only 7.9% were on smartphones, 14.6% on tablets and 77.5% were still on desktops. Considering the penetration of smartphones is still far higher than tablets, this is more testament to the phenomenal rise in purchasing on tablets. So when it comes to smartphones we believe their current role in retail is predominantly one of researching products and services, comparing prices and reading reviews rather than as a sales platform. Smartphones can be a threat to physical retailers via showrooming, but we believe that they play an even greater role as a key influencer of in-store sales and we have used a variety of research studies to demonstrate this. In November 2013, Google released their Mobile Path to Purchase Research commissioned with Nielsen amongst 950 smartphone users, all of whom had made a purchase in the last 30 days. It corroborated our view that most items that were researched on smartphones were not actually bought on these devices. Across all the different product categories 82% had purchased in-store, 45% bought online (desktop/ tablet) and only 17% purchased via a smartphone. Another great piece of research was commissioned by Deloitte in 2013 called Mobile Influence. In this report Deloitte demonstrated how smartphones should be considered more as a driver of stores sales than as a sales platform. They term this the ‘Mobile Influence Factor’ which is the percentage of store sales where smartphones were used as part of the shopping journey. In 2013 they believe the Mobile Influence Factor stood at almost 7% of store sales which is the equivalent of generating £18bn. As seen in the graphic below, this is almost 4 times the £5bn of m-commerce (mobile/tablets) and really proves the importance that consumers place on using their smartphones to help them make purchase decisions in physical stores Deloitte predicts the Mobile Influence Factor to grow significantly in the coming years and by 2017 smartphones could be influencing up to 15% of all store sales with a value of over £40bn. The Mobile Influence Factor for each retailer category is calculated individually and as expected the importance varies hugely dependent on the category. It appears particularly important for categories where more research is required in the decision making process. So for example Electronics has a Mobile Influence Factor of 13% and Home Furnishings 10%, compared to an average of 7% for all retailer categories. By 2017 Deloitte predicts that the Mobile Influence Factors for these categories may have risen to over 33% (1 in 3 purchases) for Electronics and 22% (1 in 4 purchases) for Home Furnishings. When these figures are considered, media strategies that incorporate an understanding and application of this mobile insight are no longer a nice to have, but a necessity.

- 3. POSTERSCOPE MEDIA DIGEST - 2014 12 Immediacy – What OOH advertising and mobile have in common What both OOH advertising and mobiles have in common is immediacy. Through smartphones consumers now have the ability to act immediately on impulses, desires and triggers using their smartphones as a portable encyclopedia, map, comparison and review guide. Similarly, OOH advertising with its proximity to retailers, can illicit an immediate response in the form of driving consumers in store. Posterscope’s latest OCS survey demonstrates that 11% of consumers have actually made a purchase in a physical shop/supermarket/restaurant or cinema in the last 7 days as a direct result of seeing an OOH advert. But the real advantage for both brands and consumers is when the two mediums converge. We now live in a society where consumers are exposed to more content and communications than ever before and patience is not a virtue as far as consumers are concerned. An immediate response is often vital to drive a consumer from the awareness to the involvement stage in the purchasing journey, maintaining the level of engagement generated by communications. OOH advertising is often the inspiration and trigger for consumers when out and about to drive them onto their smartphones. It is here that they can immediately gather information or access a promotion that encourages them to visit a physical store there and then. Immediate online response Inspiration OOH adverts Immediate store visit response Moment of purchase Active evaluation Information gathering, shopping Post-purchase experience Ongoing exposure Loyalty loop Initial- consideration set Trigger

- 4. POSTERSCOPE MEDIA DIGEST - 2014 13 Moreover the Google Path to Purchase research demonstrated that consumers using a smartphone for shopping related activities have a desire to make a purchase in the immediate future: 55% within the hour and 83% within a day. It also proved that 71% of smartphone owners had used a store locator. Google also conducted another piece of research on “The Role of Click to Call” in September 2013 amongst 3,000 smartphone users who regularly use mobile search. This highlighted the fact that 7 in 10 had used the click to call button for retailer questions such as business hours, making a reservation or inquiring about availability or inventory. So considering all this insight, smartphones could actually be the saviour for physical stores, compared to their online desktop and tablet equivalents. They are often used by consumers to do shopping related research when they are out and about and with a desire to purchase. Smartphones not only encourage them to visit a store in their vicinity but also give them the reassurance and confidence to make a purchase. And OOH advertising with its proximity to stores can be the ideal trigger to drive consumers onto their smartphones. OOH and Mobile Convergent Opportunities Posterscope believes the convergence of OOH advertising and mobile is paramount in the media landscape. It is particularly appropriate for bricks and mortar retailers along with the brands and products they sell and one role for OOH and mobile is to make the consumer shopping journey as easy and seamless as possible. This could be in the form of providing opportunities for consumers to interact with posters in the proximity to retailers and using their smartphones to access local information, directions, download special offers/ vouchers and to compare prices. All of which can encourage consumers to visit local retailers. Another opportunity is to utilise data in planning, such as with EE’s mobile data. This helps to select targeted poster sites in locations that are identified as hotspots for online mobile activity for a particular retail category and are therefore more likely to reach consumers in a responsive frame of mind. Such convergent opportunities are especially important over the next few years, particularly as Deloitte predicts that by 2017 in-store sales will still account for over 80% of all retail sales and smartphones will directly be influencing up to 15% of this with an annual value of £40bn. To access the full presentation please click on the following link: Retail, Mobile and OOH Please click on the following link to access the Deloitte Mobile Influence Report Please click on the following link to access the Google Mobile Path to Purchase Of consumers using mobile to research, want to purchase within the hour55% Want to purchase within a day 83%