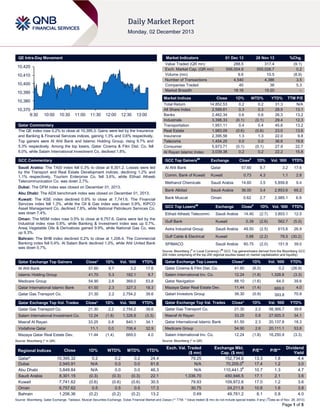

1. QE Intra-Day Movement

Market Indicators

10,420

10,410

10,400

10,390

28 Nov 13

%Chg.

288.5

556,004.9

9.6

4,540

40

18:16

317.4

555,026.7

10.5

4,386

38

15:20

(9.1)

0.2

(8.9)

3.5

5.3

–

Market Indices

10,380

10,370

9:30

01 Dec 13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.2% to close at 10,395.3. Gains were led by the Insurance

and Banking & Financial Services indices, gaining 1.3% and 0.6% respectively.

Top gainers were Al Ahli Bank and Islamic Holding Group, rising 9.7% and

5.3% respectively. Among the top losers, Qatar Cinema & Film Dist. Co. fell

6.0%, while Salam International Investment Co. declined 1.8%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,852.53

2,589.61

2,462.34

3,398.33

1,951.11

1,983.09

2,395.56

1,454.25

5,973.71

3,039.38

0.2

0.3

0.6

(0.1)

0.4

(0.6)

1.3

0.0

(0.1)

0.2

0.2

0.3

0.6

(0.1)

0.4

(0.6)

1.3

0.0

(0.1)

0.2

31.3

28.5

26.3

29.4

45.6

23.0

22.0

36.6

27.9

22.2

N/A

13.1

13.2

12.3

13.2

13.6

9.8

19.8

22.7

15.8

GCC Commentary

GCC Top Gainers##

Exchange

Saudi Arabia: The TASI index fell 0.3% to close at 8,301.2. Losses were led

by the Transport and Real Estate Development indices, declining 1.2% and

1.1% respectively. Tourism Enterprise Co. fell 3.6%, while Etihad Atheeb

Telecommunication Co. was down 2.7%.

Al Ahli Bank

Abu Dhabi: The ADX benchmark index was closed on December 01, 2013.

Kuwait: The KSE index declined 0.6% to close at 7,741.6. The Financial

Services index fell 1.3%, while the Oil & Gas index was down 0.9%. KIPCO

Asset Management Co. declined 7.8%, while National Petroleum Services Co.

was down 7.4%.

Oman: The MSM index rose 0.5% to close at 6,757.6. Gains were led by the

Industrial index rose 0.8%, while Banking & Investment index was up 0.7%.

Areej Vegetable Oils & Derivatives gained 9.9%, while National Gas Co. was

up 9.3%.

Bahrain: The BHB index declined 0.2% to close at 1,206.4. The Commercial

Banking index fell 0.4%. Al Salam Bank declined 1.0%, while Ahli United Bank

was down 0.7%.

1D%

Qatar

57.60

9.7

3.2

17.6

Comm. Bank of Kuwait

Kuwait

0.73

4.3

1.1

2.8

Methanol Chemicals

Saudi Arabia

14.60

3.5

5,859.8

9.4

Bank Albilad

Dubai: The DFM index was closed on December 01, 2013.

Close#

Saudi Arabia

36.00

3.4

2,853.6

69.2

2.7

2,985.1

6.9

Bank Muscat

Oman

##

0.62

#

GCC Top Losers

Exchange

Etihad Atheeb Telecomm.

Saudi Arabia

Close

Gulf Bank

Kuwait

Astra Industrial Group

Saudi Arabia

Gulf Cable & Electrical

Kuwait

SPIMACO

Saudi Arabia

Vol. ‘000

1D% Vol. ‘000

YTD%

YTD%

14.40

(2.7)

3,803.1

12.5

0.39

(2.6)

562.7

(5.0)

49.50

(2.5)

615.6

26.9

0.88

(2.2)

60.75

(2.0)

78.5 (30.2)

151.9

39.0

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Al Ahli Bank

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Losers

Close*

1D%

Vol. ‘000

YTD%

57.60

Qatar Exchange Top Gainers

9.7

3.2

17.6

Qatar Cinema & Film Dist. Co.

41.60

(6.0)

0.2

(26.9)

Salam International Inv. Co.

12.24

(1.8)

1,328.8

(3.3)

39.6

Islamic Holding Group

41.70

5.3

182.1

9.7

Medicare Group

54.90

2.6

369.0

53.8

Qatar Navigation

88.10

(1.6)

64.0

Qatar International Islamic Bank

61.50

2.3

327.3

18.3

Mazaya Qatar Real Estate Dev.

11.44

(1.4)

669.0

4.0

Qatar Gas Transport Co.

21.30

2.2

2,754.2

39.6

Qatari Investors Group

39.30

(0.9)

393.8

70.9

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Val. ‘000

YTD%

Qatar Gas Transport Co.

21.30

2.2

2,754.2

39.6

Qatar Gas Transport Co.

21.30

2.2

58,366.7

39.6

Salam International Investment Co.

12.24

(1.8)

1,328.8

(3.3)

Masraf Al Rayan

33.25

0.8

27,925.3

34.1

Masraf Al Rayan

33.25

0.8

840.1

34.1

Qatar International Islamic Bank

61.50

2.3

20,137.8

18.3

Vodafone Qatar

11.1

0.0

706.4

32.9

Medicare Group

54.90

2.6

20,111.1

53.8

11.44

(1.4)

669.0

4.0

Salam International Inv. Co.

12.24

(1.8)

16,250.9

(3.3)

Qatar Exchange Top Vol. Trades

Mazaya Qatar Real Estate Dev.

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Qatar Exchange Top Val. Trades

Close

1D%

WTD%

MTD%

YTD%

10,395.32

2,945.91

3,849.84

8,301.15

7,741.62

6,757.62

1,206.36

0.2

N/A

N/A

(0.3)

(0.6)

0.5

(0.2)

0.2

0.0

0.0

(0.3)

(0.6)

0.5

(0.2)

0.2

0.0

0.0

(0.3)

(0.6)

0.5

(0.2)

24.4

81.6

46.3

22.1

30.5

17.3

13.2

Exch. Val. Traded

($ mn)

79.25

N/A

N/A

1,036.70

79.93

30.75

0.49

Exchange Mkt.

Cap. ($ mn)

152,734.6

70,205.0#

110,441.3#

450,946.5

109,972.6

24,211.8

49,761.2

P/E**

P/B**

13.3

17.4

10.7

17.1

17.0

10.6

8.1

1.8

1.2

1.3

2.1

1.2

1.6

0.8

Dividend

Yield

4.4

3.0

4.7

3.6

3.6

3.8

4.0

#

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) ( Data as of Nov. 28, 2013)

Page 1 of 5

2. Qatar Market Commentary

The QE index rose 0.2% to close at 10,395.3. The Insurance and

Banking & Financial Services indices led the gains. The index

rose on the back of buying support from non-Qatari shareholders

despite selling pressure from Qatari shareholders.

Al Ahli Bank and Islamic Holding Group were the top gainers,

rising 9.7% and 5.3% respectively. Among the top losers, Qatar

Cinema & Film Dist. Co. fell 6.0%, while Salam International

Investment Co. declined 1.8%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

72.16%

77.60%

(15,682,482.04)

Non-Qatari

27.84%

22.40%

15,682,482.04

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Sunday declined by 8.9% to 9.6mn

from 10.5mn on Thursday. Further, as compared to the 30-day

moving average of 10.8mn, volume for the day was 11.8% lower.

Qatar Gas Transport Co. and Salam International Investment

Co. were the most active stocks, contributing 28.8% and 13.9%

to the total volume respectively.

News

Qatar

QNCD to expand capacity by 7,500 tons per day – As

expected, Qatar National Cement Company (QNCD) has

decided to expand its capacity. The company will add another

7,500 tons per day taking its total clinker capacity to ~18,500

tons per day after the expansion. QNCD plans to sign a contract

with global company FLSmidth in this regard. QNCD has

already signed a letter of intent (LoI) with FLSmidth and the

contract is expected to be signed next month. The company

expects to invest QR1.2bn for completing this facility. The new

facility will be operational in 24 months after the signing of the

contract (and the start of construction). The expansion is in line

with our estimates and we expect EPS to jump from QR8.45 in

2012 to QR12.81 in 2016e. We also expect the firm to announce

a cash dividend of QR6.00 per share with FY2013 results

(dividend yield of 5.74%). In our view, QNCD’s focus on Qatar

makes it one of the pure infrastructure/construction plays on the

Qatar growth story; we recommend an Accumulate rating with a

target price of QR116.25. (QNBFS Research, Peninsula Qatar)

CBQK’s shareholders approve 25% non-Qatari ownership –

The Commercial Bank of Qatar’s (CBQK) shareholders have

approved a 25% ownership for non-Qatari investors in the

bank’s share capital. The shareholders have also approved the

issue of QR2bn as additional Tier 1 capital. (Bloomberg)

MDPS: Qatar population surges to 2.068mn in November –

According to the Ministry of Development Planning & Statistics

(MDPS), Qatar’s population has continued to surge and reach

2.068mn by the end of November, due to heavy influx of foreign

workers for mega development projects. The population stood at

2.024mn by the end of October and it was slightly higher at

2.035mn in September. This figure shows total people in country

rather than residents. (Peninsula Qatar)

Foreign workers remit QR49.3bn in 2012 – According to data

released by the Qatar Central Bank (QCB), remittances by

foreign workers totaled QR49.3bn in 2012, up 3.8% over 2011.

Remittance volumes were QR47.5bn in 2011. QCB said the

economically active non-Qatari population that made much of

this money transfer grew to 1.3mn in 2012. (Peninsula Qatar)

Ezdan Holding, Sharp Corp sign MoU – Ezdan Holding Group

has signed a MoU with Sharp Corporation Global to source all

the electrical devices and smart systems for the real estate

group’s units. (Peninsula Qatar)

Vodafone, NetComm to bolster M2M in Qatar – Vodafone

Qatar and NetComm Wireless Ltd announced a strategic

partnership to extend Vodafone Qatar’s fixed and mobile

networks for devices and machines that enable Smart City

applications. These applications include security systems,

intelligent transport systems, smart metering and smart medical

devices. (Peninsula Qatar)

International

HSBC: China manufacturing activity eases in November –

HSBC said Chinese manufacturing activity expanded at a

slightly slower rate in November, supported mainly by domestic

demand. HSBC's purchasing managers' index (PMI) stood at

50.8 in November, the second-highest reading in eight months

despite easing marginally from October's 50.9. However, it is

well up from the preliminary estimate of 50.4 HSBC gave on

November 21. (ET)

Osborne pledges reduction in UK Consumers’ energy bills

– Chancellor of the Exchequer George Osborne has pledged

that domestic power customers will benefit from a reduction in

government levies for energy companies. The proposal, outlined

by Prime Minister David Cameron and Deputy Prime Minister

Nick Clegg, will cut the average energy bill by about £50 per

year. The government will fund some of the costs currently

included in consumer energy bills. (Bloomberg)

UK to pledge extra £250mn for Business Bank – The

Department for Business said UK government will announce

that it will provide an extra £250mn to increase lending to small

businesses through its so-called business bank. The

Department added that Deputy Prime Minister Nick Clegg and

Business Secretary Vince Cable will announce the additional

funding for the bank, which will be based in Sheffield, northern

England. The money will support initiatives including capital

support for new market entrants, later stage venture capital and

asset-based finance. (Bloomberg)

NDRC: China 2014 inflation seen at lower end of 3-5% range

– The National Development and Reform Commission (NDRC)

said China's consumer price inflation is likely to be at the lower

end of a 3-5% range next year. NDRC researchers Xu

Lianzhong and He Xiaoying said that it will be higher than the

2.7% forecast for 2013. They added prices will face relatively

heavy pressure to rise next year, prices of agricultural products,

especially pork, will rise faster next year than this year. (ET)

Japan 3Q2013 capex rises, BOJ Kuroda warns of overseas

risks – Japanese companies raised spending on factories and

equipment in the July-September quarter, but the slow pace of

increase casts some doubt on the strength of capital spending

Page 2 of 5

3. that is needed to help sustain economic growth. Japan’s Ministry

of Finance data showed the 1.5% YoY rise in capital spending

followed a flat reading in the prior quarter and marked the first

gain in four quarters, but the result disappointed some

economists who were expecting stronger gains. Bank of Japan

Governor Haruhiko Kuroda said capital expenditure will likely

increase as a trend, though he warned that overseas

uncertainties were among key risks in meeting the central

bank's goal of accelerating inflation to 2% in roughly two years.

(Reuters)

Regional

SAMA: Saudi banks’ liquidity ratio eases to 11.79% –

According to the Saudi Arabian Monetary Agency (SAMA), the

aggregate liquidity ratio of Saudi commercial banks fell to

11.79% in October 2013 from 12.35% in previous month. The

liquidity ratio, which accounts for bank reserves over total

deposits, declined due to a 5% MoM drop in bank reserves held

in the form of cash in the vault or as deposits with SAMA to

SR158bn outpacing 0.2% MoM contraction in total deposits held

by commercial banks to SR1.342tn in October. Meanwhile, the

rising propensity of Saudi households and corporate clients to

borrow for consumption and investment purposes (claims on

private sector) pushed aggregate bank credit extended by Saudi

banks up by 0.6% MoM to SR1.112tn in October. Total deposits

held by commercial banks contracted by 0.2% MoM to

SR1.342tn. As a result, the ratio of bank claims on the private

sector to total deposits at commercial banks moved higher to

82.89% in October from 82.14% in September. (Bloomberg)

S&P: Gulf seeks sukuk for refinancing; mega infrastructure

investments – According to S&P, Islamic bonds (sukuk) are

being increasingly sought in the Gulf region due to low yields, as

well as increased demand for refinancing and funding for

mammoth infrastructure sector spending. The renewed investor

interest comes in the wake of the US Federal Reserve’s delay in

tapering of its quantitative easing. Infrastructure plans include

investments in power and water projects, expansion related to

events like the FIFA World Cup in Qatar in 2022, along with

corporate companies aiming to diversify their funding sources.

S&P said, in a tougher regulatory environment, issuers are likely

to turn to alternative sources of funding in the capital markets,

with corporate and infrastructure entities in the Gulf favoring

sukuk. (Gulf-Times.com)

SAMA: Saudi M3 money supply slows to 10.4% in October –

According to the data released by the Saudi Arabian Monetary

Agency (SAMA), Saudi Arabia's M3 money supply growth has

slowed to a 14-month low of 10.4% YoY in October 2013 from

13.4% in September 2013. Growth in bank lending to the private

sector slowed to 13.5% from 14.6% – the lowest level since May

2012. Meanwhile, SAMA data also showed that its net foreign

assets reached a record high of SR2.66tn in October.

(GulfBase.com)

SRO signs $67.2mn contract to import 500 wagons – The

Saudi Railways Organization’s (SRO) President General Eng.

Mohammed bin Khalid Al Suwaiket signed a contract worth

$67.2mn with American Freight Car Inc. to import 500 wagons.

This step aims to modernize SRO's fleet of freight wagons,

which transport cement, grains, lime and rocks. (Bloomberg)

ACWA Power led consortium signs PPA with SEC – A

consortium led by ACWA Power International has entered into a

power purchase agreement (PPA) with the Saudi Electricity

Company (SEC) to finance, build and operate the SR5.1bn

Rabigh II power project. This consortium, which also includes

Samsung C&T, will set up a split venture with SEC to establish

Al Mourjan for Electricity Production Company. ACWA said that

74% of this project will be financed through senior debt, while

the rest will be in the form of equity bridge loans. This project will

deliver 2,060MW of electricity to SEC under a 20-year

agreement, beginning from the scheduled commercial

operational date of June 2017. (GulfBase.com)

Saud Consult partners to acquire 40% stake in PGESCo –

The Saudi Consulting Services (Saud Consult) has partnered

with BPE Power and BPE Investments to acquire a 40% stake in

Egypt-based Power Generation Engineering & Services

Company (PGESCo). Under this agreement, Saud Consult will

acquire 20% shares in PGESCo, while BPE Power and BPE

Investments together will acquire the remaining 20% stake.

(GulfBase.com)

Al Khodari Sons gets SR170mn Islamic credit facilities from

SAIB; renews SR824.3mn Islamic facilities with Riyadh

Bank – Abdullah A M Al Khodari Sons Company has obtained

Islamic credit facilities worth SR170mn from Saudi Investment

Bank (SAIB). Al Khodari Sons will utilize 47% of these facilities

under Murabaha and 53% will be utilized for multi-bonds,

documentary credit and foreign exchange hedging. These

facilities are secured by promissory notes and assignment of

contract proceeds of the financed projects. This agreement is

renewable when it expires on April 30, 2014. Meanwhile, Al

Khodari Sons has renewed its existing Islamic facilities

agreement worth SR824.3mn with Riyadh Bank. Al Khodari

Sons will utilize these facilities under Tawarroq, progress

payment, multi-bonds, documentary credit and Murabaha

financing. These facilities consist of 45% of Tawarroq,

Murabaha and 55% of multi-bonds, documentary credit, and are

secured by promissory notes and assignment of the contract

proceeds of the financed projects. This credit facilities

agreement is renewable when it expires on September 17,

2016. (Tadawul)

BDB receives its first dry bulk vessel – Bahri Dry Bulk (BDB)

has received its first dry bulk vessel “Bahri Arasco”. This is the

first vessel delivered among the five vessels that were

contracted in 2012. The financial impact of this vessel will be

visible in 4Q2013. The remaining four vessels are expected to

be delivered in 1H2014. (Tadawul)

PAL resume flights to Riyadh, Dammam – Philippine Airlines

(PAL) has resumed its flights to Riyadh from December 1, 2013

and Dammam from December 3, 2013. The airline had

suspended flights to Riyadh in March 2011, while flights to

Dammam were suspended in August 2001. (GulfBase.com)

AIG appoints new Group CEO – Astra Industrial Group (AIG)

has appointed Mohammad Abdullah Al Hagbani as the new

CEO of the group. Al Hagbani has 10 years of extensive

experience and has held the post of General Manager for

Investment Research at the General Organization for Social

Insurance. He was also a senior member in the investment

group at Al Rajhi Bank. (Tadawul)

UAE approves extra AED20bn spending on development

projects – The UAE President Sheikh Khalifa bin Zayed al

Nahayan has announced an additional spending of AED20bn on

approved development projects. Sheikh Khalifa added that

10,000 new homes will be built for Emiratis across the UAE and

the housing funds allocated to citizens under the Sheikh Zayed

program has been increased to AED800,000 from AED500,000

currently. The latest spending allocations are AED7.4bn for

developing roads that link Abu Dhabi with Saudi Arabia and

Dubai. Another AED4.3bn will go towards building a hospital in

the city of Al Ain. (GulfBase.com)

Page 3 of 5

4. Kuwait's inflation eases to 2.7% in October – Kuwait's

inflation has eased down to 2.7% in October 2013 from 2.9% in

September 2013, despite a spurt in the prices of food &

beverages. The prices of food & beverages – accounting for

18% of the basket – have risen by 3.5% YoY (+0.2% MoM) in

October. In September, analysts polled by Reuters had

forecasted an average inflation of 3.4% in 2013 and 4% in 2014.

(GulfBase.com)

Zain wants to retain control of Zain Bahrain after IPO – The

Mobile Telecommunications Company’s (Zain) CEO Scott

Gegenheimer said the company wants to retain majority control

of its Bahraini subsidiary, Zain Bahrain after the unit's IPO.

However, Zain is yet to agree the exact terms of the share sale.

Zain currently holds a 56.3% stake in Zain Bahrain and would no

longer be a majority owner after the IPO. (Reuters)

Wataniya appoints new COO – The National Mobile

Telecommunications Company (Wataniya) has appointed Peter

Kaliaropoulos as the company’s new COO. (Reuters)

Khaleeji Commercial, Al Khair starts due diligence for

merger – Bahrain-based Khaleeji Commercial Bank said it has

appointed service providers which have started to conduct due

diligence process for possible merger with Bank Al Khair.

Meanwhile, Khaleeji Commercial Bank has appointed Khalil Al

Meer as its new CEO. (Bloomberg)

Page 4 of 5

5. Rebased Performance

Daily Index Performance

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

0.8%

0.5%

149.4

0.4%

S&P Pan Arab

S&P GCC

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Oman

Source: Bloomberg (*Market closed on December 01, 2013)

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,253.49

0.0

0.0

(25.2)

DJ Industrial

16,086.41

0.0

0.0

22.8

19.99

0.0

0.0

(34.1)

S&P 500

1,805.81

0.0

0.0

26.6

109.69

0.0

0.0

(1.3)

NASDAQ 100

4,059.89

0.0

0.0

34.5

3.79

0.0

0.0

10.6

STOXX 600

325.16

0.0

0.0

16.3

116.00

0.0

0.0

28.9

DAX

9,405.30

0.0

0.0

23.6

138.75

0.0

0.0

(21.4)

FTSE 100

6,650.57

0.0

0.0

12.8

1.36

0.0

0.0

3.0

102.44

0.0

0.0

18.1

GBP

1.64

0.0

0.0

0.7

CHF

1.10

0.0

0.0

1.0

AUD

0.91

0.0

0.0

(12.4)

USD Index

80.68

0.0

0.0

RUB

33.12

0.0

0.0

BRL

0.43

0.0

0.0

(12.2)

Yen

Bahrain

Jul-13

Source: Bloomberg

Dubai*

QE Index

May-12 Dec-12

(0.6%)

Kuwait

(0.8%)

Oct-11

(0.2%)

(0.3%)

Qatar

(0.4%)

Jan-10 Aug-10 Mar-11

0.0%

0.0%

Saudi Arabia

118.6

0.0%

Abu Dhabi*

0.2%

130.6

4,295.21

0.0

0.0

18.0

15,661.87

0.0

0.0

50.7

MSCI EM

1,018.28

0.0

0.0

(3.5)

SHANGHAI SE Composite

2,220.50

0.0

0.0

(2.1)

HANG SENG

23,881.29

0.0

0.0

5.4

1.1

BSE SENSEX

20,791.93

0.0

0.0

7.0

8.5

Bovespa

52,482.49

0.0

0.0

(13.9)

1,402.93

0.0

0.0

(8.1)

Source: Bloomberg

CAC 40

Nikkei

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5