Business Principles, Tools, and Techniques in Participating in Various Types...

12 November Daily Market Report

1. QE Intra-Day Movement

Market Indicators

10,080

10,060

10,040

10,020

9:30

12 Nov 13

11 Nov 13

%Chg.

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

343.2

543,161.1

10.4

5,298

38

22:14

472.7

541,481.6

14.7

4,998

39

26:9

(27.4)

0.3

(28.9)

6.0

(2.6)

–

Market Indices

10:00

10:30

11:00

11:30

12:00

12:30

13:00

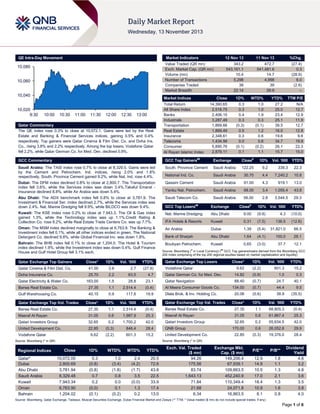

Qatar Commentary

The QE index rose 0.3% to close at 10,072.1. Gains were led by the Real

Estate and Banking & Financial Services indices, gaining 0.5% and 0.4%

respectively. Top gainers were Qatar Cinema & Film Dist. Co. and Doha Ins.

Co., rising 3.8% and 2.2% respectively. Among the top losers, Vodafone Qatar

fell 2.2%, while Qatar German Co. for Med. Dev. declined 0.9%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,390.65

2,518.75

2,406.15

3,287.49

1,869.66

1,869.49

2,348.61

1,434.99

5,890.76

2,879.11

0.3

0.3

0.4

0.3

(0.3)

0.5

0.3

0.0

(0.1)

0.1

1.0

1.0

1.9

0.3

(0.1)

1.2

0.6

0.6

(0.2)

1.1

27.2

25.0

23.4

25.1

39.5

16.0

19.6

34.7

26.1

15.7

N/A

12.7

12.9

11.9

12.7

12.8

9.6

19.8

22.3

15.0

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Vol. „000

Saudi Arabia: The TASI index rose 0.7% to close at 8,329.5. Gains were led

by the Cement and Petrochem. Ind. indices, rising 2.0% and 1.8%

respectively. South. Province Cement gained 9.2%, while Nat. Ind. rose 4.4%.

South. Province Cement

Saudi Arabia

122.25

9.2

338.3

22.3

National Ind. Co.

Saudi Arabia

30.70

4.4

7,240.2

10.8

Dubai: The DFM index declined 0.8% to close at 2,800.7. The Transportation

index fell 3.6%, while the Services index was down 3.4%.Takaful Emarat Insurance declined 8.8%, while Air Arabia was down 5.4%.

Qassim Cement

Saudi Arabia

91.00

4.3

919.1

13.0

Yanbu Nat. Petrochem.

Saudi Arabia

68.00

3.4

1,055.4

43.8

Abu Dhabi: The ADX benchmark index fell 0.8% to close at 3,781.9. The

Investment & Financial Ser. index declined 2.7%, while the Services index was

down 2.4%. Nat. Marine Dredging fell 9.9%, while BILDCO was down 9.4%.

Saudi Telecom Co.

Saudi Arabia

56.00

2.8

3,544.5

29.3

GCC Top Losers

Exchange

1D% Vol. „000

YTD%

Kuwait: The KSE index rose 0.2% to close at 7,943.3. The Oil & Gas index

gained 1.3%, while the Technology index was up 1.1%.Credit Rating &

Collection Co. rose 8.2%, while Real Estate Trade Centers Co. was up 7.7%.

Nat. Marine Dredging

Abu Dhabi

9.00

(9.9)

4.3

(10.0)

IFA Hotels & Resorts

Kuwait

0.31

(7.5)

136.5

(12.6)

Oman: The MSM index declined marginally to close at 6,763.9. The Banking &

Investment index fell 0.1%, while all other indices ended in green. The National

Detergent Co. declined 9.8%, while Global Financial Inv. was down 1.8%.

Air Arabia

Dubai

1.39

(5.4)

31,821.0

66.5

Bank of Sharjah

Abu Dhabi

1.64

(4.1)

100.0

28.1

Boubyan Petrochem.

Kuwait

0.65

(3.0)

37.7

12.1

Bahrain: The BHB index fell 0.1% to close at 1,204.0. The Hotel & Tourism

index declined 1.9%, while the Investment index was down 0.4%. Gulf Finance

House and Gulf Hotel Group fell 3.1% each.

##

1D%

Vol. „000

YTD%

Qatar Exchange Top Losers

41.00

3.8

2.7

(27.9)

Vodafone Qatar

2.2

63.5

4.7

Qatar German Co. for Med. Dev.

163.00

1.5

28.8

23.1

Qatar Navigation

Barwa Real Estate Co.

27.35

1.1

2,514.4

(0.4)

Al Meera Consumer Goods Co.

Gulf Warehousing Co.

40.15

0.9

117.8

19.9

Dlala Brok. & Inv. Holding Co.

Qatar Electricity & Water Co.

Close*

1D%

Vol. „000

YTD%

9.62

Close*

Qatar Cinema & Film Dist. Co.

25.70

Close

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Gainers

Doha Insurance Co.

#

YTD%

(2.2)

601.3

15.2

14.82

(0.9)

1.0

0.3

40.1

88.40

(0.7)

24.7

134.00

(0.7)

44.4

9.5

20.06

(0.6)

38.9

(35.5)

Close*

1D%

Vol. „000

YTD%

Close*

1D%

Val. „000

YTD%

Barwa Real Estate Co.

27.35

1.1

2,514.4

(0.4)

Barwa Real Estate Co.

27.35

1.1

68,805.3

(0.4)

Masraf Al Rayan

31.05

0.6

1,987.9

25.3

Masraf Al Rayan

31.05

0.6

61,867.4

25.3

Qatari Investors Group

32.65

0.2

1,700.2

42.0

Qatari Investors Group

32.65

0.2

55,634.5

42.0

United Development Co.

22.85

(0.3)

846.4

28.4

QNB Group

170.00

0.6

26,052.8

29.9

9.62

(2.2)

601.3

15.2

United Development Co.

22.85

(0.3)

19,376.0

28.4

Qatar Exchange Top Vol. Trades

Vodafone Qatar

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Qatar Exchange Top Val. Trades

Close

1D%

WTD%

MTD%

YTD%

10,072.05

2,800.69

3,781.94

8,329.48

7,943.34

6,763.90

1,204.02

0.3

(0.8)

(0.8)

0.7

0.2

(0.0)

(0.1)

1.0

(3.4)

(1.8)

0.8

0.0

0.1

(0.2)

2.4

(4.2)

(1.7)

3.5

(0.0)

1.3

0.2

20.5

72.6

43.8

22.5

33.9

17.4

13.0

Exch. Val. Traded

($ mn)

94.26

175.56

83.74

1,643.13

71.84

21.68

6.34

Exchange Mkt.

Cap. ($ mn)

149,206.4

67,939.1

109,663.5

452,240.9

110,349.4

24,071.8

16,863.5

P/E**

P/B**

12.9

14.9

10.5

17.0

18.4

10.9

8.1

1.8

1.1

1.3

2.1

1.3

1.6

0.8

Dividend

Yield

4.6

3.2

4.8

3.6

3.5

3.8

4.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index rose 0.3% to close at 10,072.1. The Real Estate

and Banking & Financial Services indices led the gains. The

index rose on the back of buying support from non-Qatari

shareholders despite selling pressure from Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

75.50%

80.98%

(18,806,643.63)

Non-Qatari

Qatar Cinema & Film Dist. Co. and Doha Insurance Co. were the

top gainers, rising 3.8% and 2.2% respectively. Among the top

losers, Vodafone Qatar fell 2.2%, while Qatar German Co. for

Med. Dev. declined 0.9%.

Buy %*

24.50%

19.01%

18,806,643.63

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Tuesday declined by 28.9% to

10.4mn from 14.7mn on Monday. However, as compared to the

30-day moving average of 6.9mn, volume for the day was 51.8%

higher. Barwa Real Estate Co. and Masraf Al Rayan were the

most active stocks, contributing 24.1% and 19.0% to the total

volume respectively.

Earnings and Global Economic Data

Earnings Releases

Company

Revenue

(mn) 3Q2013

% Change

YoY

Operating Profit

(mn) 3Q2013

% Change

YoY

AED

26.5

75.2%

–

–

1.2

N/A

AED

1,895.7

42.3%

–

–

307.1

97.3%

Dubai

AED

375.0

42.2%

–

–

44.8

-42.9%

Dubai

AED

56.1

4.2%

–

–

7.8

N/A

Abu Dhabi

AED

166.1

36.8%

–

–

14.5

50.3%

Abu Dhabi

AED

31.8

6.5%

–

–

2.2

-63.8%

Abu Dhabi

AED

230.1

13.1%

–

–

-31.1

43.0%

Abu Dhabi

AED

342.6

-3.1%

–

–

54.5

7.7%

Abu Dhabi

AED

19.3

6.8%

–

–

0.03

N/A

Oman

OMR

112.3

3.6%

–

–

29.1

3.9%

Oman

OMR

208.7

10.3%

35.1

6.4%

17.2

112.3%

Oman

OMR

1.8

-61.4%

–

–

1.4

-66.9%

Bahrain

BHD

2.6

-5.6%

–

–

0.02

-90.5%

Bahrain

USD

–

–

–

–

-3.2

N/A

Bahrain

BHD

3.5

0.4%

–

–

0.4

-14.3%

Market

Currency

Dar Al Takaful

Dubai

Union Properties (UP)*

Dubai

Oman Insurance Co. (OIC)

Al Sagr National Insurance

Co. (ASNIC)

National Corporation for

Tourism & Hotels (NCT&H)

Al Dhafra Insurance Co.

Abu Dhabi National Hotels

(ADNH)

Abu Dhabi National

Insurance Co. (ADNIC)

Green Crescent Insurance

Co. (GCIC)

Oman Telecommunications

Co. (Omantel)

Renaissance Services*

Global Financial Investments

Holding (GFIH)*

United Paper Industries

(UPI)

Inovest

Bahrain National Holding

Co. (BNH)

Net Profit (mn)

3Q2013

% Change

YoY

Source: Company data, DFM, ADX, MSM (*9M2013)

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

11/12

France

Bank of France

Bank of France Bus. Sentiment

11/12

Germany

Destasis

Wholesale Price Index MoM

11/12

Germany

Destasis

11/12

Germany

Destasis

11/12

Germany

11/12

Previous

October

99

97

97

October

-1.00%

–

0.70%

Wholesale Price Index YoY

October

-2.70%

–

-2.20%

CPI MoM

October

-0.20%

-0.20%

0.00%

Destasis

CPI YoY

October

1.20%

1.20%

1.10%

Germany

Destasis

CPI EU Harmonized MoM

October

-0.30%

-0.20%

0.00%

11/12

Germany

Destasis

CPI EU Harmonized YoY

October

1.20%

1.30%

1.60%

11/12

UK

RICS

RICS House Price Balance

October

57%

58%

53%

11/12

UK

ONS

PPI Input NSA MoM

October

-0.60%

-0.70%

-1.00%

11/12

UK

ONS

PPI Input NSA YoY

October

-0.30%

0.10%

0.90%

11/12

UK

ONS

PPI Output NSA MoM

October

-0.30%

0.00%

0.00%

11/12

UK

ONS

PPI Output NSA YoY

October

0.80%

1.00%

1.20%

11/12

UK

ONS

PPI Output Core NSA MoM

October

0.10%

0.10%

0.00%

11/12

UK

ONS

PPI Output Core NSA YoY

October

0.90%

0.70%

0.80%

11/12

UK

ONS

ONS House Price YoY

September

3.80%

–

3.70%

11/12

UK

ONS

CPI MoM

October

0.10%

0.30%

0.40%

11/12

UK

ONS

CPI YoY

October

2.20%

2.50%

2.70%

Page 2 of 6

3. 11/12

UK

ONS

CPI Core YoY

October

1.70%

2.00%

11/12

UK

ONS

Retail Price Index

October

251.9

252.8

2.20%

251.9

11/12

UK

ONS

RPI MoM

October

0.00%

0.40%

0.40%

11/12

UK

ONS

RPI YoY

October

2.60%

2.90%

3.20%

11/12

Japan

ESRI

Consumer Confidence Index

October

41.2

45.5

45.4

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Qatar‟s PPI in 2Q2013 declines 6.1% QoQ – According to the

data released by the Ministry of Development Planning &

Statistics (MDPS), the Producer Price Indices (PPIs) for the

industrial sector for 2Q2013 stood at 166.2, showing a decline of

6.1% QoQ. In the mining group, the PPI declined by 6.1% QoQ

primarily due to the price fall in the crude oil & natural gas group.

The PPI for the manufacturing group fell by 6.7% QoQ due to

declining prices of refined petroleum products by 9.9% QoQ,

dairy products 3.9% QoQ and basic chemicals by 3.3% QoQ.

On the other hand, the prices in basic metals rose by 2.7% QoQ

and glass products by 0.6% QoQ. The data showed that the PPI

for the electricity & water group increased 1.2% QoQ. (QSA)

QE welcomes S&P Dow Jones‟ upgrade of Qatar to

emerging market – The Qatar Exchange (QE) has welcomed

the decision of S&P Dow Jones to upgrade the Qatari market

from a frontier market to an emerging market, describing this

decision as a positive step that will attract further foreign

investments to the Qatari stock market. QE’s CEO Rashid Bin

Ali Al Mansoori expressed his satisfaction about the upgrade of

the Qatari market, which clearly indicates the recognition for the

positive steps taken by the Qatar Exchange over the past years.

(QE)

IMF: Qatar world leader in gross national savings –

According to the latest data released by the IMF, Qatar is the

world’s top-saving country, leading a list dominated by

petroleum powers in the Middle East and emerging nations in

the Far East. Qatar’s gross national savings, a measure that

accounts for both private and public savings, stood at 59% of its

GDP. Two other countries, Kuwait and China, also save over

half of their GDP. Of the top 15 countries, 11 have economies

based on oil. (Peninsula Qatar)

QA fleet will move to HIA next year – Qatar Airways’ CEO

Akbar al-Baker said its entire fleet will move to the new Hamad

International Airport (HIA) in 2014. HIA will open with a capacity

of 24mn passengers a year, rising to around 50mn, when it

reaches full operational capacity in 2015. This represents an

increase in HIA’s aircraft movement from 137,000 to 360,000

each year. HIA’s annual cargo capacity is also set to double,

from 0.8mn tons to 1.4mn tons. (Gulf-Times.com)

CBQK to hold EGM on November 27 – The Commercial Bank

of Qatar (CBQK) will hold its shareholders’ extraordinary general

meeting (EGM) on November 27, 2013. (QE)

International

OECD indicator finds improvement in developed economies

– The Organization for Economic Cooperation & Development

(OECD) said the growth outlook among developed economies

has improved further in September 2013, with a fledgling

recovery gaining momentum in the Eurozone. The OECD’s

leading indicator (CLI) covering its 33-member countries pointed

to a growth in line with its long-term trend. The CLI rose to 100.7

in September from 100.6 in August, moving further above the

long-term average of 100. The reading for the US dipped

slightly, to 100.8 in September from 100.9 in the two preceding

months. Likewise, activity remained above trend in Japan with a

figure of 101.1 in September after staying two months at 101.0.

The Eurozone saw its growth gaining momentum with a reading

of 100.7, up from 100.6 in August. Among the other major

emerging economies, India's reading eased to 96.7 from 96.9,

while China's reading rose to 99.4 from 99.2, which the OECD

described as a tentative positive change in momentum.

(Reuters)

IEA: US set to become world‟s biggest oil producer in 2015

– The International Energy Agency (IEA) said the US will stride

past both Saudi Arabia and Russia to become the world’s

leading oil producer by 2015. However, the IEA also said the

oilfields of Texas and North Dakota will be past their prime by

2020, and the Middle East will regain its dominance —

especially as a supplier to Asia. The IEA said oil prices would

continue to rise and spur development of unconventional

resources such as the light, tight oil that has fuelled the US

shale oil boom, oil sands in Canada, deepwater production in

Brazil and natural gas liquids. (Gulf-Times.com)

Bank of France sees 4Q2013 French growth at 0.4% –

According to the Bank of France, the country’s economy is set to

gain momentum towards the end of 2013 and will post a

marginal growth of 0.4% in 4Q2013. Both the French central

bank and economists polled by Reuters expect a first official

reading for 3Q2013 to show that growth slowed to 0.1% from

0.5% in the previous quarter. The Bank of France based its

4Q2013 estimate on the results of its monthly business

sentiment survey, which showed the industrial sector’s index

rising to 99 in October from 97 in September, just below the

long-term average of 100. (Reuters)

China vows decisive role for markets and results by 2020 –

China’s ruling party pledged to let markets play a decisive role in

allocating resources as it unveiled a reform agenda for the next

decade, in an effort to overhaul the world’s second-largest

economy. After the conclave of its 205-member Central

Committee, the ruling Communist Party stated that China aims

to achieve decisive results in its reform push by 2020, with

economic changes as a central focus of its overall reforms.

(Reuters)

Regional

IMF: GCC‟s energy exporting countries will face fiscal

deficit in 2016 – The IMF has warned that the Arab world's

energy exporting states are not saving enough of their oil

revenues and they may run into a fiscal deficit by 2016 if their

current policies do not change. The IMF said together with

substantial oil revenue risks, this prospect underscores the need

for countries to strengthen their fiscal and external buffers. The

total state spending among GCC members rose 9.7% in 2012,

which is much less than 17.7% in 2011. The IMF expects growth

in the GCC region’s state spending to slow further in coming

years, forecasting an annual average rise of 4% during 20132018. The fund said this spending restraint will not be enough to

prevent state budgets in many countries from going into the red.

Currently, Bahrain is the only GCC country in red, which is

expected to be followed by Oman by 2015 and Saudi Arabia in

2018. Meanwhile, the IMF said that 1mn GCC nationals may

remain jobless or seek careers in the bloated public sector by

Page 3 of 6

4. 2018, unless measures are taken to create more private sector

jobs. Private companies in the GCC region are expected to

generate 600,000 jobs, which is 1mn less than needed.

(Reuters, Bloomberg)

Al Waseen agrees to sell 75% stake to IDB – Al Waseen

Trading Company has reached an agreement to sell its 75%

shareholding to the Irish Dairy Board Cooperative Ltd (IDB).

This deal involves an investment of more than SR100mn in the

Kingdom, which includes the development of a new state-of-theart fresh white cheese manufacturing plant at Al Wazeen’s

facility in Riyadh. This new investment will further strengthen Al

Wazeen’s position in the Saudi market, where it markets a range

of dairy products to retailers and wholesaler customers.

(GulfBase.com)

SPCC signs SR713mn plant construction contract – The

Southern Province Cement Company (SPCC) has signed

SR713mn contract to construct a second production line with a

capacity to produce 5,000 tons of clinker per day at its Bisha

Cement plant. Experimental production will begin after 20

months, while commercial production will begin after 23 months.

The Bisha project and the proposed third production line at

Tihama plant will raise SPCC’s production capacity to 33,000

tons of clinker per day or 35,000 tons of cement by the end of

2014. (GulfBase.com)

HGISC completes procedures to transfer EMS‟ 20% shares

– The Al Hassan Ghazi Ibrahim Shaker Company (HGISC) has

completed the required procedures to transfer 20% shares of

the Energy Management Services (EMS) to HGISC. The capital

of EMS has also been increased from AED1.5mn to

AED3.375mn, which is divided into 225 shares. Out of these

shares, 45 shares worth AED0.68mn have been allocated to

HGISC. The balance amount of AED1.8mn will be paid by EMS’

partners based on each partners’ share interest and will be

recorded as part of company’s equity. (Tadawul)

IMF: Fundamentals must drive Dubai‟s property market not

speculation – The IMF’s Director for the Middle East & North

Africa (MENA) Masood Ahmed said the Dubai government has

to ensure that its property market is driven by fundamental

factors, not speculation and be ready to act if it sees rapid

increases in asset prices. House prices in the Emirate have

increased over 20% in 2013, which had prompted the IMF to

warn of the risk of another bubble forming in July foreseeing

another crash similar to Dubai's inflated property market in

2008-2010, which nearly caused state-linked companies to

default. (Reuters)

Moody‟s revised UAE bank system outlook to Stable from

Negative – Moody's Investors Service has revised the outlook

for the UAE's banking system to Stable from Negative. The

outlook change reflects the continued improvements in the

operating environment, as well as the ongoing recovery of the

local real-estate market, which Moody's believes will lead to a

decline in problem loan levels and an increase in profitability

over the next 12 to 18 months. In addition, the rating agency

expects that banks will continue to maintain high liquidity and

capital buffers that were built up since the onset of the global

financial crisis. Moody's expects real GDP to grow by 3.6% in

2013 and 3.7% in 2014, supported by continued public sector

spending, particularly in Abu Dhabi; and strong signs of recovery

in Dubai's more diversified private sector. This economic growth,

combined with increasing confidence and the ongoing real

estate market recovery, will support credit growth of 7-10% in

2014. (Bloomberg)

High fuel costs, currency swings curb Emirates first-half

profits – The Emirates Airline reported a near-flat net profit of

AED1.75bn for the six months ended September 30 compared

with AED1.7bn in the prior-year period, despite a 15% rise in

passengers to 21.5mn. High fuel costs and weak currencies in

some key markets flattened first-half profit growth. Meanwhile,

the Emirates Airline and French carrier Corsair International

have signed an interline agreement that will connect travelers

from Senegal to Paris. Under this agreement, customers will be

able to purchase joint Emirates-Corsair itineraries and

conveniently connect between Paris and West Africa.

(GulfBase.com, Bloomberg)

Al Ain Dairy to invest AED400mn in new farm & factory – Al

Ain Dairy is set to boost its production with AED400mn

investment on a new farm and factory in Al Ain. This new facility

will be operational by 2016, but the dairy producer does not

expect profits from it until 2017. (Bloomberg)

DFM accredits Mashreq Securities to provide DMA for

global brokers – The Dubai Financial Market (DFM) has

accredited Mashreq Securities to provide direct market access

(DMA) for global brokers, lifting the number of DMA service

providers to five. DMA allows brokerage companies to mandate

a global broker to use its access point to place buy and sell

orders on DFM through electronic trading. (DFM)

GEMS sets initial price on hybrid sukuk – Dubai-based

Global Education Management Systems (GEMS) has set the

initial pricing thought of 11.75-12% profit rate for its debut sale of

hybrid Islamic bond. GEMS has appointed Morgan Stanley,

Credit Suisse and Abu Dhabi Islamic Bank to arrange for this

sukuk sale, which will use a mudaraba structure and will be

callable after five years. (Reuters)

Abu Dhabi introduces new crude blend “Das” to improve

shipping flexibility – The Abu Dhabi Marine Operating

Company’s (ADMA-OPCO) CEO Ali R. Al Jarwan said that the

Emirate has introduced a new crude blend named ―Das‖ to

improve shipping flexibility. The Das crude will go on sale in July

2014 and replace Abu Dhabi’s Umm Shaif and Lower Zakum

grades. Meanwhile, the Abu Dhabi National Oil Company’s

(ADNOC) Marketing & Refining Director Sultan Al Mehairi said

that this new crude will sell at about the same price as Lower

Zakum. (Bloomberg)

NDC signs AED1bn deal with CPTDC to obtain 9 land rigs –

The National Drilling Company (NDC) has recently entered into

an agreement worth AED1bn with the China Petroleum

Technology & Development Corporation (CPTDC) to obtain nine

new land rigs. These new rigs will join NDC’s fleet by 2015 and

are in addition to the 11 land rigs that were manufactured by

CPTDC. (GulfBase.com)

ADNOC plans to sell Murban crude to western oil majors in

2014 – According to sources, ADNOC is planning to sell its

year's supply of Murban crude without a pre-determined

destination to a group of western oil majors in 2014. This move

ensures that the Murban crude will remain available for trade in

the spot market and could help ADNOC earn more revenue by

selling its cargoes at a premium. (Reuters)

ADCB sets initial price for dollar denominated floating rate

note – The Abu Dhabi Commercial Bank (ADCB) has set an

initial price talk of 135 basis points over the three-month LIBOR

for the January 2017 issue of a dollar-denominated floating rate

note. ADCB has appointed Deutsche Bank, JP Morgan and

Standard Chartered as joint book runners for this issue, which is

expected to have a benchmark size. (Reuters)

OCHL to set up chlorine-alkali JV plant in Abu Dhabi –

Oman Chlorine (OCHL) will set up a joint venture chlorine-alkali

plant worth $70mn in Abu Dhabi to cater to the oil & gas sector

Page 4 of 6

5. in the Gulf region. Union Chlorine, a JV between OCHL and Abu

Dhabi-based Horizon Energy will produce 70 tons per day of

caustic soda, hydrochloric acid and sodium hypochlorite. The

plant will begin commercial production by 3Q2015. (Reuters)

Salah Nooruddin acquires 5.71% stake in GFH – Gulf

Finance House (GFH) has announced that Nooruddin’s family

consortium led by Salah Nooruddin has acquired a 5.71% stake

in GFH. (Bahrain Bourse)

Bahrain Bourse to be closed on November 13-14 – Bahrain

Bourse will be officially closed on November 13 and 14, 2013 on

the occasion of Ashoura for the Hijri year 1435. The bourse will

resume trading on November 17, 2013. (Bahrain Bourse)

Page 5 of 6

6. Rebased Performance

Daily Index Performance

150.0

1.2%

0.7%

144.7

140.0

0.6%

130.0

0.3%

130.1

120.0

118.3

110.0

0.2%

0.0%

(0.1%) (0.0%)

(0.6%)

90.0

QE Index

S&P Pan Arab

S&P GCC

Source: Bloomberg

Asset/Currency Performance

1D%

WTD%

YTD%

Global Indices Performance

1,268.00

(1.2)

(1.6)

(24.3)

DJ Industrial

20.73

(3.0)

(3.6)

(31.7)

105.81

(0.6)

0.7

(4.8)

3.69

2.0

4.3

7.8

118.13

(0.3)

0.0

32.0

140.75

(0.8)

0.3

(18.6)

Euro

1.34

0.2

0.5

1.8

Yen

99.64

0.5

0.6

14.9

Nikkei

GBP

1.59

(0.5)

(0.7)

(2.2)

MSCI EM

CHF

1.09

0.2

0.5

(0.2)

SHANGHAI SE Composite

AUD

0.93

(0.6)

(0.9)

(10.5)

USD Index

81.19

0.1

(0.1)

RUB

32.90

0.2

0.8

BRL

0.43

(0.0)

(0.7)

(12.1)

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Dubai

Source: Bloomberg

Close ($)

Gold/Ounce

Oman

Jul-13

Bahrain

May-12 Dec-12

Kuwait

Oct-11

Qatar

Jan-10 Aug-10 Mar-11

(0.8%) (0.8%)

Saudi Arabia

(1.2%)

80.0

Abu Dhabi

100.0

Close

1D%

WTD%

YTD%

15,750.67

(0.2)

(0.1)

20.2

S&P 500

1,767.69

(0.2)

(0.2)

23.9

NASDAQ 100

3,919.92

0.0

0.0

29.8

321.68

(0.6)

(0.3)

15.0

DAX

9,076.48

(0.3)

(0.0)

19.2

FTSE 100

6,726.79

(0.0)

0.3

14.1

STOXX 600

CAC 40

4,263.78

(0.6)

0.1

17.1

14,588.68

2.2

3.6

40.3

991.45

(0.2)

(0.4)

(6.0)

2,126.77

0.8

1.0

(6.3)

HANG SENG

22,901.41

(0.7)

0.7

1.1

1.8

BSE SENSEX

20,281.91

(1.0)

(1.9)

4.4

7.8

Bovespa

51,804.33

(1.6)

(0.9)

(15.0)

1,437.37

0.7

0.2

(5.9)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (―QNBFS‖) a wholly-owned subsidiary of Qatar National Bank (―QNB‖). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6