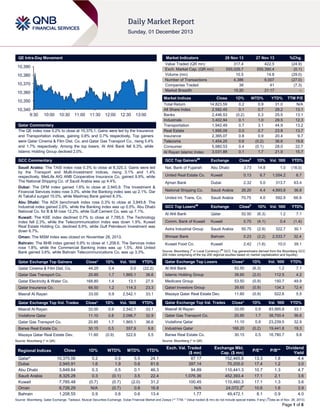

QE Intra-Day Movement and Qatar Market Commentary (38

1. QE Intra-Day Movement

Market Indicators

10,390

10,380

10,370

10,360

27 Nov 13

%Chg.

317.4

555,026.7

10.5

4,386

38

15:20

422.5

555,390.4

14.8

6,007

41

21:17

(24.9)

(0.1)

(29.0)

(27.0)

(7.3)

–

Market Indices

10,350

10,340

9:30

28 Nov 13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.2% to close at 10,375.1. Gains were led by the Insurance

and Transportation indices, gaining 0.8% and 0.7% respectively. Top gainers

were Qatar Cinema & Film Dist. Co. and Qatar Gas Transport Co., rising 5.4%

and 1.7% respectively. Among the top losers, Al Ahli Bank fell 6.3%, while

Islamic Holding Group declined 2.0%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,823.59

2,582.45

2,446.53

3,402.94

1,942.49

1,995.09

2,365.07

1,454.25

5,980.53

3,031.88

0.2

0.1

(0.2)

0.1

0.7

0.0

0.8

0.6

0.4

0.1

0.9

0.7

0.3

1.0

3.1

0.7

0.9

(0.2)

(0.1)

1.7

31.0

28.2

25.5

29.5

44.9

23.8

20.4

36.6

28.0

21.9

N/A

13.1

13.1

12.3

13.2

13.7

9.7

19.8

22.7

15.7

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Vol. ‘000

Saudi Arabia: The TASI index rose 0.3% to close at 8,325.3. Gains were led

by the Transport and Multi-Investment indices, rising 3.1% and 1.4%

respectively. MetLife AIG ANB Cooperative Insurance Co. gained 9.9%, while

The National Shipping Co. of Saudi Arabia was up 4.4%.

Nat. Bank of Fujairah

Abu Dhabi

3.73

14.8

1.0

(18.0)

United Real Estate Co.

Kuwait

0.13

6.7

1,054.2

6.7

Ajman Bank

Dubai

2.32

5.0

313.7

63.4

National Shipping Co.

Saudi Arabia

26.20

4.4

4,893.8

36.8

United Int. Trans. Co.

Saudi Arabia

70.75

4.0

592.9

66.9

Dubai: The DFM index gained 1.6% to close at 2,945.9. The Investment &

Financial Services index rose 3.3%, while the Banking index was up 2.1%. Dar

Al Takaful surged 15.0%, while Mashreq Bank gained 8.3%.

Abu Dhabi: The ADX benchmark index rose 0.3% to close at 3,849.8. The

Industrial index gained 2.6%, while the Banking index was up 0.5%. Abu Dhabi

National Co. for B & M rose 12.2%, while Gulf Cement Co. was up 7.1%.

##

#

1D% Vol. ‘000

Oman: The MSM index was closed on November 28, 2013.

Bahrain: The BHB index gained 0.9% to close at 1,208.6. The Services index

rose 1.8%, while the Commercial Banking index was up 1.5%. Ahli United

Bank gained 3.6%, while Bahrain Telecommunications Co. was up 3.3%.

GCC Top Losers

Exchange

Al Ahli Bank

Qatar

52.50

(6.3)

1.2

7.1

Comm. Bank of Kuwait

Kuwait

0.70

(4.1)

0.4

(1.4)

Astra Industrial Group

Saudi Arabia

50.75

(2.9)

322.7

30.1

Ithmaar Bank

Kuwait: The KSE index declined 0.7% to close at 7,785.5. The Technology

index fell 2.3%, while the Telecommunication index was down 1.9%. Kuwait

Real Estate Holding Co. declined 6.9%, while Gulf Petroleum Investment was

down 6.7%.

Close

YTD%

YTD%

Bahrain

0.23

(2.2)

2,533.7

32.4

Kuwait Food Co.

Kuwait

2.42

(1.6)

10.0

39.1

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Gainers

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Losers

Close*

1D%

Vol. ‘000

YTD%

Qatar Cinema & Film Dist. Co.

44.25

5.4

0.0

(22.2)

Al Ahli Bank

52.50

(6.3)

1.2

7.1

39.60

(2.0)

112.5

4.2

Qatar Gas Transport Co.

20.85

1,865.1

1.7

36.6

Islamic Holding Group

168.80

1.4

13.1

27.5

Medicare Group

53.50

(0.9)

150.7

49.9

Qatar Insurance Co.

66.50

1.2

114.3

23.3

Qatari Investors Group

39.65

(0.9)

134.3

72.4

Masraf Al Rayan

33.00

0.9

2,542.1

33.1

Mazaya Qatar Real Estate Dev.

11.60

(0.9)

522.6

5.5

Qatar Electricity & Water Co.

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Val. ‘000

YTD%

Masraf Al Rayan

33.00

0.9

2,542.1

33.1

Masraf Al Rayan

33.00

0.9

83,995.8

33.1

Vodafone Qatar

11.10

0.8

2,096.7

32.9

Qatar Gas Transport Co.

20.85

1.7

38,700.4

36.6

Qatar Gas Transport Co.

20.85

1.7

1,865.1

36.6

Vodafone Qatar

11.10

0.8

23,239.5

32.9

Barwa Real Estate Co.

30.15

0.5

557.9

9.8

Industries Qatar

168.20

(0.2)

19,441.8

19.3

Mazaya Qatar Real Estate Dev.

11.60

(0.9)

522.6

5.5

Barwa Real Estate Co.

30.15

0.5

16,780.7

9.8

Qatar Exchange Top Vol. Trades

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Qatar Exchange Top Val. Trades

Close

1D%

WTD%

MTD%

YTD%

10,375.06

2,945.91

3,849.84

8,325.28

7,785.48

6,726.29

1,208.55

0.2

1.6

0.3

0.3

(0.7)

N/A

0.9

0.9

1.9

0.5

(0.1)

(0.7)

(0.7)

0.6

5.5

0.8

0.1

3.5

(2.0)

0.8

0.6

24.1

81.6

46.3

22.4

31.2

16.8

13.4

Exch. Val. Traded

($ mn)

87.17

397.14

94.89

1,076.36

100.45

N/A

1.77

Exchange Mkt.

Cap. ($ mn)

152,465.8

70,205.0

110,441.3

452,393.4

110,460.3

24,072.2#

49,472.1

P/E**

P/B**

13.3

17.4

10.7

17.1

17.1

10.6

8.1

1.8

1.2

1.3

2.1

1.3

1.6

0.9

Dividend

Yield

4.4

3.0

4.7

3.6

3.6

3.9

4.0

#

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) ( Data as of Nov. 26, 2013)

Page 1 of 6

2. Qatar Market Commentary

The QE index rose 0.2% to close at 10,375.1. The Insurance and

Transportation indices led the gains. The index rose on the back

of buying support from Qatari shareholders despite selling

pressure from non-Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

76.39%

71.80%

14,572,735.46

Non-Qatari

Qatar Cinema & Film Dist. Co. and Qatar Gas Transport Co.

were the top gainers, rising 5.4% and 1.7% respectively. Among

the top losers, Al Ahli Bank fell 6.3%, while Islamic Holding

Group declined 2.0%.

Buy %*

23.62%

28.20%

(14,572,735.46)

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Thursday declined by 29.0% to

10.5mn from 14.8mn on Wednesday. Further, as compared to

the 30-day moving average of 11.2mn, volume for the day was

6.0% lower. Masraf Al Rayan and Vodafone Qatar were the most

active stocks, contributing 24.2% and 20.0% to the total volume

respectively.

Earnings and Global Economic Data

Earnings Releases

Company

Market

Sudatel Telecom Group

(STG)

Currency

Abu Dhabi

Revenue

(mn) 3Q2013

% Change

YoY

Operating Profit

(mn) 3Q2013

% Change

YoY

Net Profit (mn)

3Q2013

% Change

YoY

123.7

17.3%

–

–

-5.8

-69.4%

USD

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

11/28

EU

Eurostat

Business Climate Indicator

11/28

EU

Eurostat

Economic Confidence

November

0.18

0.05

-0.08

November

98.5

98.0

11/28

EU

Eurostat

97.7

Industrial Confidence

November

-3.9

-4.4

11/28

EU

-5.0

Eurostat

Consumer Confidence

November

-15.4

-15.4

-14.5

11/28

11/29

EU

Eurostat

Services Confidence

November

-0.8

-3.5

-3.7

EU

Eurostat

CPI Estimate YoY

November

0.90%

0.80%

0.70%

11/29

EU

Eurostat

CPI Core YoY

November

1.00%

0.90%

0.80%

11/29

France

Insee

PPI MoM

October

-0.20%

–

0.30%

11/29

France

Insee

PPI YoY

October

-1.40%

-0.80%

-0.70%

11/29

France

Insee

Consumer Spending MoM

October

-0.20%

0.20%

-0.10%

11/29

France

Insee

Consumer Spending YoY

October

-0.10%

0.20%

-0.10%

11/28

Germany

Destasis

Import Price Index MoM

October

-0.70%

-0.30%

0.00%

11/28

Germany

Destasis

Import Price Index YoY

October

-3.00%

-2.60%

-2.80%

11/28

Germany

Destasis

CPI Saxony YoY

November

1.40%

–

1.10%

11/28

Germany

Destasis

CPI MoM

November

0.20%

0.10%

-0.20%

11/28

Germany

Destasis

CPI YoY

November

1.30%

1.20%

1.20%

11/29

Germany

Destasis

Retail Sales MoM

October

-0.80%

0.50%

-0.20%

11/29

Germany

Destasis

Retail Sales YoY

October

-0.20%

1.40%

0.30%

11/28

UK

Lloyds Bank

Lloyds Business Barometer

November

50

–

63

11/29

UK

GfK

GfK Consumer Confidence

November

-12

-10

-11

11/29

UK

Nat'wide

Nationwide House PX MoM

November

0.60%

0.60%

1.00%

11/29

UK

Nat'wide

Nationwide House Px NSA YoY

November

6.50%

6.20%

5.80%

11/28

Spain

INE

GDP YoY

3Q2013

-1.10%

-1.20%

-1.60%

11/28

Spain

INE

GDP QoQ

3Q2013

0.10%

0.10%

-0.10%

11/28

Spain

INE

CPI YoY

November

0.20%

0.20%

-0.10%

11/28

Spain

INS

House Price Index QoQ

3Q2013

-0.40%

–

-2.40%

11/28

Spain

INS

House Price Index YoY

3Q2013

-4.50%

–

-7.60%

11/29

Japan

Markit

Markit/JMMA Manufacturing PMI

November

55.1

–

54.2

11/29

Japan

METI

Industrial Production MoM

October

0.50%

2.00%

1.30%

11/29

Japan

METI

Industrial Production YoY

October

4.70%

6.30%

5.10%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Page 2 of 6

3. News

Qatar

Qatar to maintain LNG lead despite US shale gas revolution

– The development of US shale gas extraction to tap previously

inaccessible reserves, the so called US shale gas revolution, is

not proving to be a game changer for Qatar, according to QNB

Group. Fracking techniques, namely the process of forcing

water, chemicals and sand at high pressure into shale rock

deposits to extract high volumes of gas have been refined only

over the last decade to make US shale gas commercially viable.

This has virtually eliminated the need for the US to import

liquefied natural gas (LNG), including from Qatar. The drop in

demand from the US, however, has been replaced by strong

demand from Asia, particularly from Japan after the Fukushima

nuclear accident in March 2011. As a result, QNB Group

expects global LNG demand to remain strong over the next

decade. Qatar is therefore unlikely to lose its leading role in the

global energy market for years to come. (QNB, Gulf-Times.com)

MARK inches closer to acquire IBB – Masraf Al Rayan

(MARK) and Islamic Bank of Britain (IBB) have announced that

they have reached an agreement on the terms of a

recommended cash offer by Al Rayan (UK) Limited, a wholly

owned subsidiary of MARK for the entire issued and to be

issued share capital of IBB. Earlier on September 30, 2013,

MARK had offered £24.1mn for the acquisition, with each IBB

shareholder entitled to receive 0.53 pence in cash for every IBB

share. (Peninsula Qatar)

QCB to issue QR4bn T-bills on December 3 – The Qatar

Central Bank (QCB) will issue treasury bills with a maturity of 91

days, 182 days and 273 days on December 3, 2013. The total

amount of this issuance is QR4bn. (QCB)

Qatar’s Producer Price Index rises by 1.4% – Qatar’s

Producer Price Index (PPI) of the Industrial Sector for 3Q2013

stood at 168.6, showing 1.4% increase over the PPI in 2Q2013.

Released by the Ministry of Development Planning & Statistics

(MDPS), the PPI showed that the “mining” group increased by

1.4%, primarily due to 1.4% price rise seen in the crude oil &

natural gas group. The 2.4% rise in the PPI for the

“manufacturing” group is mainly due to increasing prices in basic

chemicals (3.6%), refined petroleum products (2.4%), and basic

metals (1%). On the other hand, price declines were recorded in

the dairy products and glass & glass products, which went down

by 1% and 0.6% respectively. Similarly, the PPI for “electricity &

water” showed a decrease of 0.7%. The year-on-year

comparison of PPI for 3Q2013 over PPI for 3Q2012 showed a

rise of 1.6%. (Peninsula Qatar)

QNB launches Al Safwa services – The Qatar National Bank

(QNB) has launched “Al Safwa” services that provide an

innovative gateway and a one-stop solution for both Egyptian

expatriates as well as QNB First Qatari citizens. The service

also builds on the successful acquisition of a controlling stake of

97.12% in its QNB Al Ahli operations in Egypt (formerly NSGB).

(Peninsula Qatar)

India to increase airline seats for Qatar under bilateral pact

– India is set to increase Qatar's entitlement of airline seats

under their bilateral air traffic rights. This move can help in

developing Doha as a major regional hub for westbound traffic

from India. Under the pact, Qatar seeks to enhance its weekly

quota to 72,600 seats from the current 24,800, which was nearly

exhausted. Qatar Airways, is the fifth largest carrier of India's

international traffic, with nearly 4% share of the 45 million

passengers travelling to and from India in 2012-13. (Bloomberg)

QIBK opens Dar Al Salam Mall branch – Qatar Islamic Bank

(QIBK) has opened a branch at Dar Al Salam Mall in Abu

Hamour as part of its expansion strategy. (Peninsula Qatar)

Hotel occupancy rises to 57% in 3Q2013 – According to the

data released by Qatar's Tourism Authority, the hotel occupancy

rate in Qatar averaged at 57% in 3Q2013, up from 50% in

3Q2012. This is despite an addition of 600 rooms and a 4.73%

increase in inventory. The total revenue among four and five star

hotels stood at $193mn, indicating an increase of 13.8% YoY.

(Bloomberg)

Kahramaa’s $3bn project to boost water security – The

Qatar General Electricity & Water Corporation (Kahramaa) is

undertaking a $3bn project designed to provide seven days of

strategic water storage in its network. Kahramaa’s Technical

Director Ahmed al-Naser said the Water Security Mega

Reservoirs project will increase the capacity of water storage in

Qatar by 10 times to about 3,500mn gallons. Kahramaa has also

planned an independent water & power plant (IWPP) with a

power generation capacity of 2,400MW and a desalination

capacity of 130mn gallons per day to meet the growing demand

for water and electricity. The IWPP known as “Facility D” will be

located at the Qatar Economic Zone near Doha. (GulfTimes.com)

QA, JAL enter into code share agreement – Qatar Airways

(QA) and Japan Airlines (JAL) have entered into a code share

agreement for the first time. The airlines will commence their

code share flights from December 3, 2013 on QA operated

flights between Tokyo and Doha as well as Osaka and Doha.

Meanwhile, QA will place its flight indicator on JAL operated

flights. (Bloomberg)

International

S&P removes Dutch from triple-A club, lifts outlook for

Spain – S&P’s has cut the Netherlands' credit rating, reducing

the Eurozone club of full triple-A nations to just three, while

rewarding Spain for efforts to reform its public finances. S&P

lowered the Netherlands, which is suffering from an anemic

economy, slumping house prices and falling consumer

confidence, to "AA+" from "AAA". This left Germany,

Luxembourg and Finland as the only members of the 17-nation

euro zone with the top rating from all three leading credit

agencies. However, it raised the outlook for Spanish debt to

Stable from Negative and upgraded bailed-out Cyprus,

highlighting diverging fortunes within the common currency bloc.

(Reuters)

Moody’s raises Greece to Caa3 on fiscal progress – Moody’s

has raised Greece’s government bond rating to Caa3 from C

with a Stable outlook. Moody’s said it expects Greece to achieve

(and possibly outperform) its target of a primary balance in

2013, and record a surplus in 2014. It also said that a cyclical

recovery in the economy is another reason for the credit grade

increase. Moody’s said the Greek economy is bottoming out

after nearly six years of recession. The ratings company said it

expects the government’s budget focus to remain on savings

generated from structural reform measures as opposed to

further spending cuts. (Bloomberg)

China’s manufacturing index beats estimates as output

rises – A Chinese manufacturing gauge exceeded analysts’

estimates in November, indicating the nation’s economic

recovery is sustaining momentum amid government efforts to

rein in credit growth. Chinese National Bureau of Statistics and

China Federation of Logistics & Purchasing said the Purchasing

Managers’ Index was 51.4. That’s the same reading as October

Page 3 of 6

4. and was higher than 24 out of 26 estimates in a Bloomberg

News survey that had a median forecast of 51.1. (Bloomberg)

China sets IPO reform plan signaling end of freeze on

listings – The China Securities Regulatory Commission has

issued a reform plan for IPOs, as the government prepares to lift

a more than one-year freeze on new listings in the country. The

regulator said about 50 companies are expected to complete the

IPO approval preparations and list or be ready to do so by the

end of January. The regulator said there are more than 760

companies in the queue for approval and it will take about a year

to complete an audit of all the applications. (Bloomberg)

India growth quickens from four-year low as rate increases

loom – Indian economic growth quickened last quarter from a

four-year low on higher factory output, a revival threatened by

looming interest-rate increases to fight rising prices in the nation

of 1.2bn people. The Indian Statistics Ministry said GDP rose

4.8% in the three months ended September from a year earlier,

compared with 4.4 in the previous quarter. The median of 44

estimates in a Bloomberg News Survey was for a 4.6% gain.

(Bloomberg)

S&P sees Islamic finance flourishing next year – According

to a report by S&P, growth of the global Islamic finance market

has continued unabated this year, despite the uncertain

recovery elsewhere in the world’s financial markets. S&P’s

Regional Head of Eastern Europe, Middle East & Africa Zeynep

Holmes said S&P believes that global Shari’ah-compliant

assets, which are estimated at around $1.4tn, are likely to

sustain double-digit growth in the coming 2-3 years. Islamic

finance remains a demand-driven market with scarce supply,

which is still hampered by a limited range of financial centers

and their various regulatory frameworks. The S&P report said it

is only a matter of time before Islamic finance achieves critical

mass, as the pool of assets broadens, enhancing liquidity. The

report said starting from 2014, the regulatory efforts needed to

accommodate Islamic finance and the establishment of

additional industry bodies at national levels will take centre

stage. (Peninsula Qatar)

Regional

Reuters: Mideast fund managers more cautious on equities

– According to a survey conducted by Reuters, fund managers

in the Middle East are showing signs of becoming more cautious

toward some equity markets as change looms in the global

economic environment. The Reuters monthly survey showed

that 47% out of 15 managers expect raising their overall equity

allocation to the region in the next three months, while the rest

expect maintaining it steady. The survey also showed a rise in

the proportion of managers who expect to decrease their

allocations to fixed income in the Middle East over the next three

months from 19% in October to 33% in November. (Reuters)

GCC countries plan a navigation maintenance hub for

shipments – Countries in the GCC region are planning to set up

a common navigation maintenance hub for the better integration

of cargo movements within the GCC waters. Ports across the

region will work in tandem to handle the huge pressure expected

from the heavy volume of shipments during the next few years.

GCC countries are set to witness a huge volume of cargo

movements with $3tn worth of development works projected in

the Middle East over the coming years. The contract for this

project is expected to be signed in the coming months.

(GulfBase.com)

Saudi investments on aquaculture projects to reach

SR60bn – The Saudi Ministry of Agriculture’s Undersecretary for

Fishery Affairs Jabir Al Shihri said that investments on

aquaculture projects will be increased from SR20bn to SR60bn

in order to produce 1mn tons of fish products over the next 16

years. (GulfBase.com)

SCC’s Turkish unit signs deal to supply SR132mn power

equipment – The Saudi Cable Company’s (SCC) Turkish

subsidiary, Demirer Kablo has signed a contract to supply

132kV power cables and related materials worth SR132mn.

These materials will be delivered over a period of 12 months

from the date of receipt of the letter of credit. The financial

impact of this contract will appear in 3Q2014. (Tadawul)

Sumitomo Chemical expects approval for Rabigh II project

expansion in 1H2014 – Japan-based Sumitomo Chemical

Company’s President Masakazu Tokura said the company

expects to win project finance approval for the expansion of

Rabigh II project in Saudi Arabia in 1H2014. This $7bn project

will be operational in 2016. (GulfBase.com)

Invensys signs deal to set up R&D center in DTV – UKbased Invensys has signed an agreement to set up a R&D

center in automation & control systems for oil & gas, energy and

construction sectors in Dhahran Techno Valley (DTV) located at

King Fahd University of Petroleum & Minerals. (GulfBase.com)

ADC signs credit facilities deal with Saudi Fransi Capital –

Al Ahsa Development Company (ADC) has entered into an

agreement for credit facilities (on draft) for guarantee with Saudi

Fransi Capital to ensure the portfolio securities owned by ADC

and the limited facilities at the company to participate in the

IPOs. ADC has announced that the purpose of this agreement is

to increase the sources of income for the company and its

financial impact is expected in 1Q2014. (Tadawul)

Mobily extend talks with EATC shareholders until January

30, 2014 – The Etihad Etisalat Company (Mobily) has extended

talks

with

four

shareholders

in

Etihad

Atheeb

Telecommunication Company (EATC) until January 30, 2014. If

concluded, this deal will give Mobily a majority control in EATC

and enable it to provide fixed-line services directly and attract

customers with bundled packages of internet, television and

phone calls. (GulfBase.com)

JMC’s BoD recommends 50% capital increase through

bonus shares – Jarir Marketing Company’s (JMC) board of

directors has recommended increasing the company’s capital by

50% to SR900mn through the issue of bonus shares. JMC will

issue 30mn additional shares and offer one bonus share for

every two shares owned. (Tadawul)

LG Electronics appoints Shaker Co as distributor – LG

Electronics has appointed the Shaker Company as a nonexclusive distributor for its LED lighting products in Saudi Arabia

for a period of two years. The financial impact of this agreement

is expected to be visible in 1Q2014. (Tadawul)

SABIC opens technical center in Bangalore – Saudi Basic

Industries Corporation’s (SABIC) Chairman of the Board of

Directors Prince Saud Bin Abdullah Bin Thunayan opened

$100mn worth SABIC Technical Center in Bangalore. The newly

opened center is the latest of SABIC technical centers in Asia,

which will have around 300 scientists, engineers and technicians

working for it in India. (GulfBase.com)

ANB Insurance receives approval from Saudi CMA – The

MetLife-AIG ANB Cooperative Insurance Company (ANB

Insurance) has received approval from Saudi Capital Market

Authority (CMA) to be exempt from the requirements of

disclosing its interim financial results for 2013. However, the

company shall disclose its annual audited financial statements

for 2013 according to the listing rules requirements. (Tadawul)

Page 4 of 6

5. SACO obtains SAMA’s approval for insurance products –

The Saudi Arabian Cooperative Insurance Company (SAICO)

has obtained a temporary approval from the Saudi Arabian

Monetary Agency (SAMA) to use its insurance products for six

months. (Tadawul)

UAE to participate in WTO conference – The UAE will

participate in the 9th Ministerial Conference of the World Trade

Organization (WTO), which will take place on December 3 in

Bali, Indonesi. (GulfBase.com)

Kingston Holdings signs JV deal with Glen Dimplex –

Sharjah-based Kingston Holdings and Ireland’s Glen Dimplex

entered into JV named “Xpelair Middle East” to provide

customers with access to full range of Glen Dimplex products.

The total investment for this production unit is estimated to be

$33mn. Apart from the Middle East and Africa region, this JV will

cover India, Sri Lanka, Nepal, Bangladesh, and Maldives as

well. (GulfBase.com)

DEL signs MoU with Nord Stream AG – Dolphin Energy Ltd

(DEL) has entered into a five-year MoU with Nord Stream AG to

exchange operational & maintenance knowledge, and expertise

regarding high pressure gas networks and subsea pipeline

systems. This MoU will also explore opportunities where both

the companies can lend support to each other’s Emergency

Pipeline Repair System, which is essential to ensure minimum

disruption to gas throughput in the event of pipeline repairs.

(GulfBase.com)

IPIC seeks $2bn refinancing loan – According to sources, the

International Petroleum Investment Company (IPIC) is arranging

for a $2bn refinancing loan. This loan will be split between a

three-year facility worth $1bn paying a margin of 40 basis points

(bps) over LIBOR and a five-year facility worth $1bn paying a

margin of 50 bps over LIBOR, with both tranches paying

utilization fees on top. This facility, which is expected to be

completed as a club loan, will be provided by around 12 banks.

(Reuters)

Etihad adds more seats on Abu Dhabi-Melbourne route –

Etihad Airways has added more seats between Abu Dhabi and

Melbourne in Australia by introducing a Boeing 777-300ER on

this route. Operating from December 1, this larger aircraft will

offer 328 seats in a three-class configuration, offering 36 more

than the Airbus A340-600. (GulfBase.com)

MOIC, EDB, GIA sign MoU to develop GPTLB – Bahrain’s

Ministry of Industry & Commerce (MOIC), the Bahrain Economic

Development Board (EDB) and the Gemological Institute of

America (GIA) have entered into a MoU to develop Gemstone &

Pearl Testing Laboratory (GPTLB) in Bahrain for research into

the production of natural pearls. Under this MoU, all three

parties will work together to enhance Bahrain’s pearling industry,

with the aim of developing capacity, research, expertise and

technological know-how at GPTLB, and identify further

opportunities for the sector to grow in Bahrain. (GulfBase.com)

Fitch: Dubai should generate activity; boost confidence

over next few years – According to Fitch Ratings, Dubai's

successful bid for the 2020 World Expo should generate activity

and boost confidence across the Emirate's infrastructure, real

estate and hospitality sectors over the next few years. However,

the ambitious plan of Dubai could throw off the balance of

supply and demand after this expo. Dubai expects 25mn visitors

to visit this expo, which will drive major new construction

projects across a 438-hectare site and significant infrastructure

upgrades. Fitch said that this activity should support rents and

real estate prices up to the event and boost the demand in

construction and hospitality sectors in the Emirate. Fitch expects

government entities to be responsible for infrastructure

improvements, while major developers will handle other projects

such as hotel facilities for visitors. Meanwhile, a well-managed

expo could attract more businesses to the Emirate's free zones

and raise its standing as a travel destination. (GulfBase.com)

(GulfBase.com)

Dubai proposes UAE to create Shari’ah-compliant

retirement packages for foreign workers – Dubai has

proposed to the UAE Federal Government to create a Shari’ahcompliant retirement savings scheme for foreign workers. This

scheme could help in developing the Islamic funds industry in

the Emirates. (GulfBase.com)

MEED Projects: Major investment seen in Dubai after 2020

World Expo win – According to MEED Projects, major

investments are expected to be seen in various infrastructure

projects in Dubai after the successful bid of Dubai World Expo

2020. MEED expects the total value of contracts awarded such

as the metro, new airport and construction of the Expo center to

be around $30bn in 2013. (GulfBase.com)

Emaar Properties bans agents from reselling off-plan

properties – Dubai property developer Emaar Properties has

banned real estate agents from reselling off-plan properties. Any

off-plan property purchase will not be subject to transfer until

handover. (GulfBase.com)

Page 5 of 6

6. Rebased Performance

Daily Index Performance

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

2.1%

149.1

1.4%

130.8

0.7%

1.6%

118.7

0.9%

0.3%

0.2%

0.0%

0.3%

0.0%

(0.7%)

S&P Pan Arab

S&P GCC

Source: Bloomberg

Asset/Currency Performance

1D%

WTD%

YTD%

Global Indices Performance

1,253.49

0.8

0.8

(25.2)

DJ Industrial

19.99

1.4

0.6

(34.1)

109.69

(1.1)

(1.2)

3.79

0.0

LPG Propane (Arab Gulf)/Ton

116.00

LPG Butane (Arab Gulf)/Ton

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

Euro

Yen

Dubai

Oman*

Source: Bloomberg (*Market closed on November 28, 2013)

Close ($)

Gold/Ounce

Bahrain

Jul-13

Kuwait

May-12 Dec-12

Abu Dhabi

QE Index

Oct-11

Qatar

Jan-10 Aug-10 Mar-11

Saudi Arabia

(0.7%)

(1.4%)

Close

1D%

WTD%

YTD%

16,086.41

(0.1)

0.1

22.8

S&P 500

1,805.81

(0.1)

0.1

26.6

(1.3)

NASDAQ 100

4,059.89

0.4

1.7

34.5

0.5

10.6

STOXX 600

325.16

(0.0)

0.7

16.3

0.0

(3.1)

28.9

DAX

9,405.30

0.2

2.0

23.6

138.75

0.0

(3.0)

(21.4)

FTSE 100

6,650.57

(0.1)

(0.4)

12.8

1.36

(0.1)

0.2

3.0

CAC 40

4,295.21

(0.2)

0.4

18.0

102.44

0.1

1.2

18.1

15,661.87

(0.4)

1.8

50.7

GBP

1.64

0.2

0.9

0.7

MSCI EM

1,018.28

0.6

0.9

(3.5)

CHF

1.10

(0.1)

0.1

1.0

SHANGHAI SE Composite

2,220.50

0.1

1.1

(2.1)

AUD

Nikkei

0.91

0.1

(0.8)

(12.4)

HANG SENG

23,881.29

0.4

0.8

5.4

USD Index

80.68

0.1

(0.0)

1.1

BSE SENSEX

20,791.93

1.3

2.8

7.0

RUB

33.12

(0.1)

1.1

8.5

Bovespa

52,482.49

1.2

(0.6)

(13.9)

BRL

0.43

(0.7)

(2.3)

(12.2)

1,402.93

(0.3)

(2.9)

(8.1)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6