QNBFS Daily Technical Trader Qatar - September 07, 2023 التحليل الفني اليومي ...

The Global Economy Continues to Stumble Along

1. Page 1 of 2

Economic Commentary

QNB Economics

economics@qnb.com.qa

August 10, 2014

The Global Economy Continues to Stumble Along

The global economy continues to stumble

along. According to the latest IMF World

Economic Outlook (WEO) published on July 24,

global economic growth slowed to an annual

rate of 2.7% in Q1 2014, well below the 3.6%

registered in the previous quarter. Part of the

slowdown was due to a temporary contraction

in the US and slower growth in the Eurozone,

China and Emerging Markets (EMs) in Q1.

However, both the US and China rebounded in

the second quarter. Notwithstanding these

temporary factors, the ongoing global

investment slowdown reflects increased

uncertainty about the impact of an eventual

rise in US interest rates and rising geopolitical

risks. Looking ahead, the global economy is

likely to continue to stumble along unless

these clouds are lifted from the investment

horizon.

Global economic growth in Q1 2014 was

weaker than expected for a number of factors.

First, the US registered the largest contraction

(-2.1%) since Q2 2009, reflecting an inventory

overhang and unusually cold weather. While

this contraction was reversed in Q2 2014

(4.0%), US growth for the first half of the year

as a whole was still relatively weak (0.9%) on

weak investment spending. Looking ahead, we

expect US growth of only 1.0%-1.5% for 2014

as a whole as expectations of an eventual rise

in US short-term rates weighs negatively on

investor sentiments.

Second, growth in the Eurozone was barely

positive (0.2%), reflecting stronger economic

activity in Germany and Spain offset by

virtually no growth in France and Italy (see

QNB Group’s Economic Commentary dated

May 25, 2014). The Ukraine crisis has added

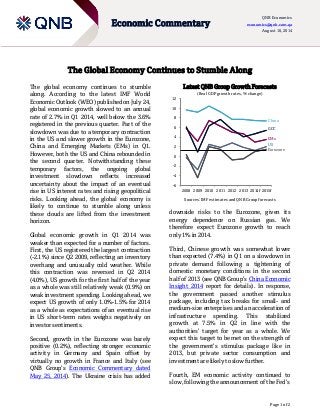

Latest QNB Group Growth Forecasts

(Real GDP growth rates, % change)

Sources: IMF estimates and QNB Group forecasts

downside risks to the Eurozone, given its

energy dependence on Russian gas. We

therefore expect Eurozone growth to reach

only 1% in 2014.

Third, Chinese growth was somewhat lower

than expected (7.4%) in Q1 on a slowdown in

private demand following a tightening of

domestic monetary conditions in the second

half of 2013 (see QNB Group’s China Economic

Insight 2014 report for details). In response,

the government passed another stimulus

package, including tax breaks for small- and

medium-size enterprises and an acceleration of

infrastructure spending. This stabilized

growth at 7.5% in Q2 in line with the

authorities’ target for year as a whole. We

expect this target to be met on the strength of

the government’s stimulus package like in

2013, but private sector consumption and

investment are likely to slow further.

Fourth, EM economic activity continued to

slow, following the announcement of the Fed’s

-6

-4

-2

0

2

4

6

8

10

12

2008 2009 2010 2011 2012 2013 2014f 2015f

China

GCC

EMs

US

Eurozone

2. Page 2 of 2

Economic Commentary

QNB Economics

economics@qnb.com.qa

August 10, 2014

intention to taper Quantitative Easing in May

2013 and the consequent tightening of

financial conditions. Growth in Brazil virtually

stalled (0.2%) in Q1 on tight monetary policy

and political uncertainty. India’s growth rate

was temporarily boosted by election spending

in Q1, but the new Modi administration faces

significant structural challenges to reignite

India’s growth momentum. The same can be

said for the new Jokowi administration in

Indonesia (see QNB Group’s Economic

Commentary dated July 26, 2014). Russia and

South Africa’s economies contracted in Q1 on

the Ukraine crisis for the former and labor

disputes for the latter. Overall, we expect EM

growth to be weak in 2014 (3.0%) on

continued economic and geopolitical

uncertainty weighing on investment

decisions.

Looking ahead, uncertainty about the timing

of higher US interest rates and geopolitical

risks are likely to continue to weigh heavily on

the prospects for the global economy. The

global investment slowdown is partly due to

the end of Quantitative Easing, where super-

cheap money led to large flows of capital to

EMs and risky assets. The eventual increase in

US interest rate will inevitably lead to a

reassessment of investment decisions and the

price of certain asset classes.

The conflicts in Iraq, Libya, Palestine and

Ukraine add significant geopolitical risks to

this already weak outlook. Large disruptions to

gas supplies in Eastern Europe or oil supplies in

Libya and Iraq could put upward pressure on

gas and oil prices and further dampen global

economic growth.

Overall, the outlook for the global economy

remains uneven and risks are tilted heavily on

the downside. The eventual rise in US interest

rates and geopolitical risks emanating from the

conflicts in Eastern Europe and the Middle East

are only likely to add to the global investment

slowdown. As a result, the global economy is

only likely to continue to stumble along until

these clouds are lifted from the investment

horizon.

Contacts

Joannes Mongardini

Head of Economics

Tel. (+974) 4453-4412

Rory Fyfe

Senior Economist

Tel. (+974) 4453-4643

Ehsan Khoman

Economist

Tel. (+974) 4453-4423

Hamda Al-Thani

Economist

Tel. (+974) 4453-4646

Ziad Daoud

Economist

Tel. (+974) 4453-4642

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend

on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a

complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.