1. Economic Commentary

QNB Economics

economics@qnb.com

March 8, 2014

The Risk of Deflation is Likely to Keep Short-Term

Interest Rates Low

In the Eurozone and the US, inflation

remains dangerously low and well below

the 2% central bank targets. Inflation is

not expected to pick up in the short term

as weak global demand holds back global

energy and food prices. With weak

growth expected in Europe and recent

disappointing economic data in the US,

the risk of deflation remains high. As

such, European and US central banks are

likely to keep monetary policy loose for

an extended period. Therefore, QNB

Group expects short-term interest rates

in the Eurozone and the US to stay low

for longer than prevailing market

expectations.

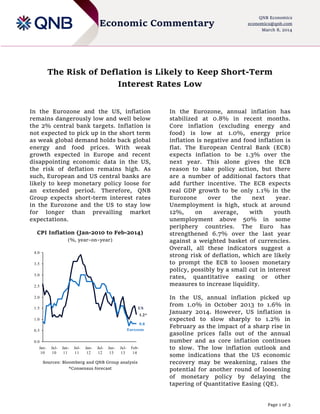

CPI Inflation (Jan-2010 to Feb-2014)

(%, year–on–year)

4.0

3.5

3.0

2.5

2.0

1.5

US

1.2*

1.0

0.8

Eurozone

0.5

0.0

Jan10

Jul10

Jan11

Jul11

Jan12

Jul12

Jan13

Jul13

Feb14

Sources: Bloomberg and QNB Group analysis

*Consensus forecast

In the Eurozone, annual inflation has

stabilized at 0.8% in recent months.

Core inflation (excluding energy and

food) is low at 1.0%, energy price

inflation is negative and food inflation is

flat. The European Central Bank (ECB)

expects inflation to be 1.3% over the

next year. This alone gives the ECB

reason to take policy action, but there

are a number of additional factors that

add further incentive. The ECB expects

real GDP growth to be only 1.1% in the

Eurozone

over

the

next

year.

Unemployment is high, stuck at around

12%,

on

average,

with

youth

unemployment above 50% in some

periphery countries. The Euro has

strengthened 6.7% over the last year

against a weighted basket of currencies.

Overall, all these indicators suggest a

strong risk of deflation, which are likely

to prompt the ECB to loosen monetary

policy, possibly by a small cut in interest

rates, quantitative easing or other

measures to increase liquidity.

In the US, annual inflation picked up

from 1.0% in October 2013 to 1.6% in

January 2014. However, US inflation is

expected to slow sharply to 1.2% in

February as the impact of a sharp rise in

gasoline prices falls out of the annual

number and as core inflation continues

to slow. The low inflation outlook and

some indications that the US economic

recovery may be weakening, raises the

potential for another round of loosening

of monetary policy by delaying the

tapering of Quantitative Easing (QE).

Page 1 of 3

2. Economic Commentary

The Federal Reserve (Fed) has shown

firm commitment to QE tapering during

early 2014, despite a soft patch in

economic data, which has widely been

put down to bad weather. However, this

resolve may be easing as recent

comments from the Fed Chair, Janet

Yellen, have indicated that QE tapering

could be adjusted if the US economy

weakens. Upcoming economic data

releases in March and April should give a

clearer picture on how much of the

recent weak economic data can be put

down to bad weather. We do not expect

the picture to be clear enough for the

Fed to postpone QE tapering at its next

meeting on March 19, but by the time the

Fed meets on April 30, there is some risk

that the economic outlook could have

deteriorated enough to warrant a

slowdown in the pace of QE tapering

(the first reading of GDP growth in Q1

2014 is also released on April 30) to

offset the risk of deflation.

The potential for falling inflation in the

Eurozone and US will make central

banks wary of falling into a deflationary

trap. According to economic theory,

deflation fuels expectations that prices

will continue to fall, encouraging delays

to purchases, thus holding back growth

(Japan’s experience in the last two

decades is a good example). It also

increases the real value of outstanding

domestic debt, thus making it more

QNB Economics

economics@qnb.com

March 8, 2014

difficult

for

borrowers

to

make

repayments. Deflation also tends to lead

to

a

stronger

exchange

rate,

undermining

competitiveness

and

growth. On the other hand, a moderately

inflationary

environment

reinforces

expectations that prices will continue to

rise

and

encourages

spending,

borrowing,

growth

and

a

more

competitive exchange rate. For these

reasons, central banks tend to use

monetary policy to target moderate

annual inflation of around 2%, thus

avoiding the perils of a deflationary trap.

Looking ahead, the risk of deflation and

weak economies in the US and Eurozone,

present a strong case for the Fed and

ECB to loosen or refrain from tightening

monetary policy. This implies that any

increase in short-term interest rates in

the Eurozone or in the US is still some

way off. Qatar’s policy rates tend to

track rates in the US owing to the pegged

exchange rate. Therefore, interest rates

are also likely to remain low in Qatar. A

pause in tightening monetary policy in

the US would have the added benefit of

bringing greater stability to global

financial markets. The implementation

of QE tapering has led to capital

outflows from a number of emerging

markets, weakening their currencies and

driving down asset prices. Delayed QE

tapering could help bring greater

stability.

Contacts

Joannes Mongardini

Head of Economics

Tel. (+974) 4453-4412

joannes.mongardini@qnb.co

m.qa

Rory Fyfe

Senior Economist

Tel. (+974) 4453-4643

rory.fyfe@qnb.com.qa

Ehsan Khoman

Economist

Tel. (+974) 4453-4423

ehsan.khoman@qnb.com.qa

Hamda Al-Thani

Economist

Tel. (+974) 4453-4646

hamda.althani@qnb.com.qa

Page 2 of 3

3. Economic Commentary

QNB Economics

economics@qnb.com

March 8, 2014

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising

from use of this report. Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only.

Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. The report is distributed on a complimentary basis. It may not be reproduced in whole or in

part without permission from QNB Group.

Page 3 of 3