Public and Private Real Estate Returns by Leverage

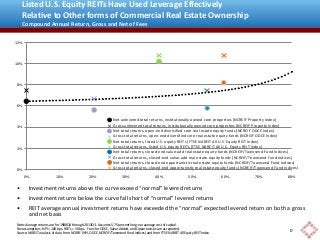

This chart shows reported long-term average annual returns, gross and net of fees, for different forms of real estate ownership. The line starts from the average net unlevered return of institutionally owned commercial properties (6.44%) and shows what the return would be if you simply applied leverage at a long-term average cost of 5.75%. Any NET return above the line suggests better performance at the property level. Private equity real estate funds following core (lavender) and value-add (blue) strategies have under-performed. Private equity funds following opportunistic strategies have over-performed, but not by much, with average net returns of 8.20% compared to implied net returns of 7.48% for institutionally owned private real estate with comparable leverage. Listed U.S. equity REITs have performed much, much better, with long-term average net returns of 10.19% compared to the implied net return of 6.90% for institutionally owned core properties using comparable leverage (40%, the approximate long-term average for listed equity REITs). There is abundant data showing that private real estate has tended to perform worse than listed real estate in the U.S.; this also suggests that private real estate funds have tended to perform worse than institutionally owned private real estate that is held directly rather than through funds. Questions? Contact me at bcase@nareit.com.

Recommandé

Recommandé

Contenu connexe

Dernier

Dernier (20)

En vedette

En vedette (20)

Public and Private Real Estate Returns by Leverage

- 1. Listed U.S. Equity REITs Have Used Leverage Effectively Relative to Other forms of Commercial Real Estate Ownership Compound Annual Return, Gross and Net of Fees 12% 10% 8% 6% Net unlevered total returns, institutionally owned core properties (NCREIF Property Index) ╳ Gross unlevered total returns, institutionally owned core properties (NCREIF Property Index) 4% ╳ ╳ 2% ╳ ╳ 0% 0% 10% 20% Net total returns, open-end diversified core real estate equity funds (NCREIF ODCE Index) Gross total returns, open-end diversified core real estate equity funds (NCREIF ODCE Index) Net total returns, listed U.S. equity REITs (FTSE NAREIT All U.S. Equity REIT Index) Gross total returns, listed U.S. equity REITs (FTSE NAREIT All U.S. Equity REIT Index) Net total returns, closed-end value-add real estate equity funds (NCREIF/Townsend Fund Indices) Gross total returns, closed-end value-add real estate equity funds (NCREIF/Townsend Fund Indices) Net total returns, closed-end opportunistic real estate equity funds (NCREIF/Townsend Fund Indices) Gross total returns, closed-end opportunistic real estate equity funds (NCREIF/Townsend Fund Indices) 30% 40% 50% 60% 70% 80% • Investment returns above the curve exceed “normal” levered returns • Investment returns below the curve fall short of “normal” levered returns • REIT average annual investment returns have exceeded the “normal” expected levered return on both a gross and net basis Note: Average returns are for 1988Q4 through 2013Q3. Assumes 5.75 percent long-run average cost of capital. Fee assumptions: NPI = 100 bps, REITs = 50 bps. Fees for ODCE, Value-Added, and Opportunistic are as reported. Source: NAREIT analysis of data from NCREIF (NPI, ODCE, NCREIF/Townsend Fund Indices) and from FTSE NAREIT All Equity REIT Index. 0