1. www.colliers.com/houston

Q4 2012 | OFFICE MARKET

RESEARCH & FORECAST REPORT

HOUSTON OFFICE MARKET

HOUSTON’S HOT ECONOMY BOOSTS OFFICE LEASING,

SALES, AND DEVELOPMENT ACTIVITY

Houston’s strong job growth boosted office leasing in 2012. Fourth quarter

leasing activity reached 2.4 million SF, pushing the year-end total to over 12.2

million SF. The Houston metropolitan area added 85,300 jobs between

November 2011 and November 2012, an annual increase of 3.2% over the prior

year’s job growth. Further, Houston’s unemployment fell to 5.8% from 7.3%

one year ago, which bolstered annual Houston area home sales by 27.9%.

Expansion in the energy industry has driven demand for new office

development as tenants find it harder to locate blocks of quality office space.

Currently, over 4.2 million SF of office space is under construction and

approximately 50.0% of it is pre-leased. A complete list of properties under

construction can be found on page 7 of this report.

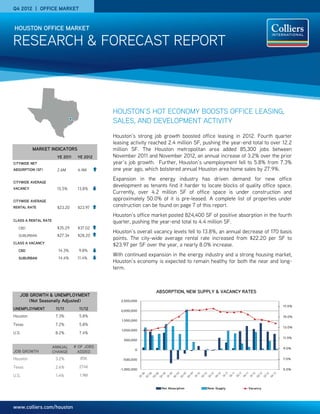

Houston’s office market posted 824,400 SF of positive absorption in the fourth

quarter, pushing the year-end total to 4.4 million SF.

Houston’s overall vacancy levels fell to 13.8%, an annual decrease of 170 basis

points. The city-wide average rental rate increased from $22.20 per SF to

$23.97 per SF over the year, a nearly 8.0% increase.

With continued expansion in the energy industry and a strong housing market,

Houston’s economy is expected to remain healthy for both the near and long-

term.

MARKET INDICATORS

YE 2011 YE 2012

CITYWIDE NET

ABSORPTION (SF) 2.6M 4.4M

)

CITYWIDE AVERAGE

VACANCY 15.5% 13.8%

CITYWIDE AVERAGE

RENTAL RATE $23.20 $23.97

CLASS A RENTAL RATE

CBD $35.29 $37.02

SUBURBAN $27.34 $28.20

CLASS A VACANCY

CBD 14.3% 9.8%

SUBURBAN 14.4% 11.4%

ABSORPTION, NEW SUPPLY & VACANCY RATES

UNEMPLOYMENT 11/11 11/12

Houston 7.3% 5.8%

Texas 7.2% 5.8%

U.S. 8.2% 7.4%

JOB GROWTH

ANNUAL

CHANGE

# OF JOBS

ADDED

Houston 3.2% 85K

Texas 2.6% 274K

U.S. 1.4% 1.9M

JOB GROWTH & UNEMPLOYMENT

(Not Seasonally Adjusted)

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Net Absorption New Supply Vacancy

2. RESEARCH & FORECAST REPORT | Q4 2012 | HOUSTON OFFICE MARKET

$26.00

$28.00

$30.00

$32.00

$34.00

$36.00

$38.00

$40.00

CLASS A OFFICE RENTS

CBD RENTS SUBURBAN RENTS

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

CBD VS. SUBURBAN

CLASS A OFFICE VACANCY

CBD VACANCY SUBURBAN VACANCY

QUOTED GROSS RENTAL RATES FOR TOP PERFORMING OFFICE BUILDINGS

BUILDING NAME ADDRESS SUBMARKET RBA (SF)

YEAR

BUILT

LEASED

AVAIL.

SF

RENT

($/SF)

OWNER

717 Texas 717 Texas CBD 696,228 2003 100% 67,509 $43.79 Hines

5 Houston Center 1401 McKinney St CBD 600,000 2002 97.4% 28,500 $43.66 Wells Real Estate Funds

1000 Main 1000 Main St CBD 837,161 2003 98.3% 22,420 $42.00 INVESCO Realty Advisers, Inc.

Heritage Plaza 1111 Bagby CBD 1,089,266 1986 99.3% 360,917 $41.94 Brookfield Office Properties

BG Group Place 811 Main CBD 972,474 2011 77.2% 221,440 $41.87 CalPERS/Hines

Wells Fargo Bank Tower 1300 Post Oak Blvd.

West Loop/

Galleria

491,254 1983 98.4% 8,071 $40.15 TIAA-CREF

Williams Tower 2800 Post Oak Blvd

West Loop/

Galleria

1,476,973 1983 98.9% 16,926 $40.66 Hines REIT

9 Greenway Plaza 9 Greenway Greenway 746,824 1978 95.7% 37,455 $32.90 Crescent Real Estate Equities

Two Eldridge Place 757 N Eldridge Pky Katy Freeway 280,322 1986 98.3% 11,882 $34.45 Behringer Harvard REIT I, Inc.

San Felipe Plaza 5847 San Felipe St

San

Felipe/Voss

980,472 1984 89.0% 136,891 $37.92 Thomas Properties Group, L.P.

One BriarLake Plaza

2000 W Sam

Houston Parkway

Westchase 502,410 2000 100.0% 26,910 $44.55 Behringer Harvard Holdings

Waterway Plaza II

10001 Woodloch

Forest Dr

The Woodlands 142560 2001 100.0% 56,826 $38.58 The Lionstone Group

Note: Avail. SF includes direct and sublet space.

Source: CoStar Property

2COLLIERS INTERNATIONAL | P.

VACANCY & AVAILABILITY

Houston’s average vacancy rate and the

average suburban vacancy rate both

decreased by 40 basis points to 13.8% from

14.2% on a quarterly basis. The average

CBD vacancy rate decreased by 20 basis

points to 13.7% from 13.9% between

quarters. On a year-over-year basis, the

city-wide vacancy rate decreased by 170

basis points to 13.8% from 15.5%. The

average suburban vacancy rate decreased

by 150 basis points to 13.8% from 15.3%, and

the average CBD vacancy rate decreased by

290 basis points to 13.7% from 16.6%.

The CBD Class A vacancy rate decreased by

80 basis points to 9.8% from 10.6% between

quarters, while the CBD Class B vacancy rate

increased 220 basis points to 20.2% from

18.0%. The suburban Class A and B vacancy

rates both decreased by 60 basis points

between quarters to 11.4% from 12.0% and to

16.1% from 16.5%, respectively.

Of the 1,707 buildings in the Houston office

market, only 43 have 100,000 SF of

contiguous space available for lease or

sublease. Further, only 13 have 200,000 SF

of contiguous space available.

Available sublease space citywide totals 3.2

million SF or 1.7% of total inventory, of which

1.1 million SF is currently vacant.

ABSORPTION & DEMAND

Houston recorded positive net absorption of

824,400 SF in the fourth quarter, pushing the

year-end absorption total to 4,426,000 SF.

Contributing to the fourth quarter’s positive

gain was suburban Class A space with

positive net absorption of 403,000 SF,

followed by CBD Class A space with positive

net absorption of 244,800 SF. Some of the

larger tenants that moved into their space or

expanded into additional space during the

third quarter include Seadrill relocating to

64,400 SF in Two Westway from 23,600 SF

in Westway One, and several expansions

including: Wells Fargo (35,000 SF in Wells

Fargo Plaza), Wood Mackenzie, Inc. (expanded

to 51,919 SF from 28,986 in San Felipe

Plaza), Superior Energy Services (15,165 SF

in 13333 Northwest Freeway), and Gregg &

Valby, LLP (14,000 SF in 1700 West Loop S).

RENTAL RATES

The average citywide rental rate increased

slightly between quarters increasing to

$23.97 from $23.61 per square foot. The

CBD Class A average quoted rental rate

increased to $37.02 from $36.85 per square

foot, while the suburban Class A average

quoted rental rate increased to $28.20 from

$27.31 per square foot.

The CBD Class B average quoted rental rate

increased to $25.00 from $24.00 per square

foot, while the suburban Class B average

quoted rental rate increased to $18.75 from

$18.74 per square foot between quarters.

3. RESEARCH & FORECAST REPORT | Q4 2012 | HOUSTON OFFICE MARKET

Q4 2012 SIGNIFICANT SALES TRANSACTIONS – (100,000 SF or greater)

BUILDING NAME

SUB-

MARKET

RBA (SF)

YEAR

BUILT

BUYER SELLER

SALE

PRICE

$/SF

CAP

RATE

CLOSED

KBR Tower CBD 1,047,748 1973

Corporate Property

Associates 17 Global, Inc.

Brookfield Office

Properties & KBR, Inc.

$175M $167 6.80% 11/2012

1800 West Loop S.

West Loop/

Galleria

406,634 1982

KBS Strategic

Opportunity REIT

Pearlmark Real Estate

Partners

$69M $168 7.00% 12/2012

West Loop I & II Bellaire 313,873 1980

KBS Strategic

Opportunity REIT

Chase Merritt $36M $117 N/A 12/2012

Reserve at Park

Ten

Katy Fwy 145,000 2009 CapLease, Inc.

Principal Global

Investors

$35.5M $245 8.20% 12/2012

Woodway Tower

West Loop/

Galleria

119,127 1979 Donerail Corporation Fidelis Realty Partners $13M $146 8.00% 10/2012

3COLLIERS INTERNATIONAL | P.

SALES ACTIVITY

Houston’s office investment sales activity increased between quarters with 33 properties changing hands, compared to 21 in the

previous quarter. According to CoStar Comps, Houston office total transaction sales volume was approximately $908 million, averaging

$200 per SF. Some of the more significant transactions that closed during the fourth quarter are listed below.

LEASING ACTIVITY

Houston’s office leasing activity reached 2.4 million SF in the fourth quarter, pushing the year-end total to over 12.2 million SF.

Below is a list of Q4 2012 top lease transactions.

1

Renewal

2

Expansion

3

Sublease

4

Pre-lease/under construction

Building name/address Submarket SF Tenant Lease date

Energy Crossing II Katy Freeway 127,000 Modec International4

Oct-12

8 West Centre Katy Freeway 119,000 Helix Energy Solutions Group4

Nov-12

3555 Timmons Ln Greenway 65,000 Houston-Galveston Area Council 1 Nov-12

One Hughes Landing The Woodlands 51,152 Layne Christensen4 Nov-12

Memorial 6 Center Katy Freeway 34,013 Expro Americas1 Nov-12

8584 Katy Freeway Katy Freeway 33,922 IHS Global, Inc.1 Oct-12

Pennzoil Place North CBD 31,879 Seyfarth Shaw Nov-12

San Felipe Plaza West Loop/Galleria 51,919 Wood Mackenzie, Inc.1,2 Nov-12

One Riverway West Loop/Galleria 20,000 Harper & Pearson1 Nov-12

1800 West Loop West Loop/Galleria 20,000 Quanex Building Nov-12

1442 Lake Front Circle The Woodlands 18,819 Shrieve Chemical Company Oct-12

Memorial 6 Center Katy Freeway 18,275 Deep Gulf Energy, LP1 Oct-12

11111 Wilcrest Green Dr Westchase 18,065 Othon, Inc., Consulting Engineers1 Oct-12

7141 Office City Dr Gulf Freeway/Pasadena 17,852 General Services Administration Oct-12

Decorative Center of Houston West Loop/Galleria 17,356 PreCash, Inc. Oct-12

Dairy Ashford Plaza Katy Freeway 17,287 Resurgent Capital Services, LP Oct-12

13333 Northwest Freeway Northwest 15,165 Superior Energy Services2 Nov-12

BBVA Compass Plaza West Loop/Galleria 15,000 Worldwide Machinery4 Nov-12

1700 West Loop S West Loop/Galleria 13,732 Gregg & Valby, LLP2 Oct-12

Q4 2012 Top Office Leases

7. RESEARCH & FORECAST REPORT | Q4 2012 | HOUSTON OFFICE MARKET

OFFICE DEVELOPMENT PIPELINE

Houston’s construction pipeline continues to expand with 4.4 million SF currently under construction. The table below includes buildings

80,000 SF or larger.

HOUSTON SUBURBAN OFFICE MARKET SUMMARY - CONTINUED

Building Name Address Submarket SF Pre-Leased Developer Est. Delivery

Anadarko Tower 2 1201 Lake Robbins Dr The Woodlands 550,000 100.00% Patrinely Group Inc Apr-14

Energy Tower III 11740 Katy Freeway Katy Freeway 428,831 0.00% Mac Haik Realty LLC Jan-14

Energy Crossing II 15011 Katy Freeway Katy Freeway 321,508 64.90% Opus Corporation Aug-13

Murphy Exploration 9805 Katy Freeway Katy Freeway 320,000 100.00% MetroNational Corp Nov-13

BBVA Compass 2200 Post Oak Blvd Galleria/Uptown 306,012 65.40% Redstone and Stream Apr-13

3009 Post Oak Blvd. 3009 Post Oak Blvd Galleria/Uptown 302,536 0.00% Skanska Commercial

Development

Jul-13

Research Forest Lakeside 4 2445 Technology Forest Blvd The Woodlands 300,000 50.00% Warmack Investments Apr-13

Granite Briarpark Green 3151 Briarpark Dr Westchase 299,664 2.10% Granite Properties Jul-13

3 Waterway Square Place 3 Waterway Ave The Woodlands 232,693 90.30% The Woodlands Development

Company, L.P.

Jun-13

8 West Centre 3505 W Sam Houston Pky N Katy Freeway 228,000 52.60% CORE Parkway Central, Ltd Jul-13

One Hughes Landing Grogan's Mill Rd The Woodlands 197,841 28.20% The Woodlands Development

Company, L.P.

Sep-13

17320 Katy Freeway 17320 Katy Freeway Katy Freeway 182,000 1.10% Transwestern Dec-13

Sam Houston Crossing II 10344 Sam Houston Pky N Northwest Far 159,056 0.00% Duke Realty May-13

Mason Creek Office Center 21420 Merchants Way Katy Freeway 135,716 0.00% Myers, Crow & Saviers Apr-13

Blvd Place 1 1 Blvd Place Galleria/Uptown 130,916 56.60% Wulfe & Co. Oct-13

CityCentre Four 840 W Sam Houston Pky N Katy Freeway 120,052 52.80% Midway Companies Jun-13

Haliburton North Campus Bldg Milner Rd & N Sam Houston Pky North Belt/Greenspoint 100,000 100.00% Haliburton Jan-13

Blvd Place 2 2 Blvd Place Galleria/Uptown 80,002 0.00% Wulfe & Co. Jun-14

Vacancy Rental Rate

Class # of Bldgs. Total (SF) (SF) Rate (%) (SF) Rate (%) Total (SF) Q4-2012 Q3-2012 Q4-2012 YTD-2012

AVG

($/SF)

West Loop/Galleria

A 33 14,173,964 1,349,066 9.5% 39,369 0.3% 1,388,435 9.8% 10.0% 24,684 170,832 $31.39

B 58 7,298,163 1,200,590 16.5% 12,617 0.2% 1,213,207 16.6% 16.9% 12,155 99,861 $23.49

C 3 147,042 1562 1.1% 0 0.0% 1,562 1.1% 0.3% -1,129 -1,562 $18.79

Total 94 21,619,169 2,551,218 11.8% 51,986 0.2% 2,603,204 12.0% 12.2% 35,710 269,131 $27.93

Westchase

A 22 6,798,460 399,509 5.9% 9,620 0.1% 409,129 6.0% 7.8% 123,216 506,669 $34.20

B 59 6,218,685 782,040 12.6% 10,468 0.2% 792,508 12.7% 13.8% 17,000 135,450 $18.52

C 6 281,047 77,228 27.5% 0 0.0% 77,228 27.5% 26.5% -2,613 -32,840 $18.32

Total 87 13,298,192 1,258,777 9.5% 20,088 0.2% 1,278,865 9.6% 11.0% 137,603 609,279 $26.81

The Woodlands

A 16 3,198,900 28,606 0.9% 0 0.0% 28,606 0.9% 2.1% 36,167 97,842 $35.51

B 67 3,478,778 318,034 9.1% 17,238 0.5% 335,272 9.6% 10.7% 37,680 254,378 $21.48

C 5 341,192 0 0.0% 0 0.0% 0 0.0% 0.0% 0 918 -

Total 88 7,018,870 346,640 4.9% 17,238 0.2% 363,878 5.2% 6.3% 73,847 353,138 $24.54

Inventory Direct Vacancy Sublease Vacancy Vacancy Rate (%) Net Absorption (SF)

8. RESEARCH & FORECAST REPORT | Q4 2012 | HOUSTON OFFICE MARKET

Accelerating success.

COLLIERS INTERNATIONAL | HOUSTON

1300 Post Oak Boulevard

Suite 200

Houston, Texas 77056

Main +1 713 222 2111

8COLLIERS INTERNATIONAL | P.

LISA R. BRIDGES

Director of Market Research Houston

Direct +1 713 830 2125

Fax +1 713 830 2118

lisa.bridges@colliers.com