5 Ways Mobile Technology Will Revolutionize ATMs

•

1 like•1,449 views

Despite the proliferation of e-commerce and mobile banking, cash remains a significant factor for consumers. Given the growth of cash-accepting ATMs, the industry is poised at the center of channel convergence in the mobile era. The channel strategies are developing to take full advantage of interactivity between consumer-owned devices and ATMs, the leading selfservice channel. This white paper, from "The Future of Payments: ATM & Mobile Executive Summit" explains the following five ways that mobile technology will change ATMs: - Prestaging transactions - Contactless transactions - Serving the unbanked - Expanded ATM services - Expanded ATM/mobile capabilities

Recommended

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

5 Ways Mobile Technology Will Revolutionize ATMs

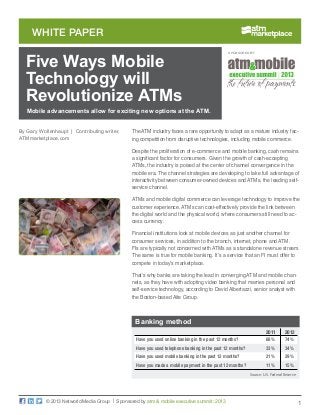

- 1. 1 white paper © 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 The ATM industry faces a rare opportunity to adapt as a mature industry fac- ing competition from disruptive technologies, including mobile commerce. Despite the proliferation of e-commerce and mobile banking, cash remains a significant factor for consumers. Given the growth of cash-accepting ATMs, the industry is poised at the center of channel convergence in the mobile era. The channel strategies are developing to take full advantage of interactivity between consumer-owned devices and ATMs, the leading self- service channel. ATMs and mobile digital commerce can leverage technology to improve the customer experience. ATMs can cost-effectively provide the link between the digital world and the physical world, where consumers still need to ac- cess currency. Financial institutions look at mobile devices as just another channel for consumer services, in addition to the branch, internet, phone and ATM. FIs are typically not concerned with ATMs as a standalone revenue stream. The same is true for mobile banking. It’s a service that an FI must offer to compete in today’s marketplace. That’s why banks are taking the lead in converging ATM and mobile chan- nels, as they have with adopting video banking that marries personal and self-service technology, according to David Albertazzi, senior analyst with the Boston-based Aite Group. Mobile advancements allow for exciting new options at the ATM. By Gary Wollenhaupt | Contributing writer, ATMmarketplace.com SPONSORED BY: Five Ways Mobile Technology will Revolutionize ATMs 2011 2012 Have you used online banking in the past 12 months? 68% 74% Have you used telephone banking in the past 12 months? 33% 34% Have you used mobile banking in the past 12 months? 21% 29% Have you made a mobile payment in the past 12 months? 11% 15% Source: U.S. Federal Reserve Banking method

- 2. The Impact of Market Turbulence on ATMs 2© 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 “Ultimately banks are looking to combine channels to make it easier for the customers,” Albertazzi said. But those in the independent ATM deployer space may face a tougher road in a mobile-dominant future. “With IAD ATMs, the transactions that can be performed are more narrow; they don’t have the bells and whistles like the banks do to offer custom- ers,” Albertazzi said. “The challenges for IADs will be greater. They need to come up with better ways to integrate mobile within their offerings.” The explosion of mobile device usage and the burgeoning mobile payments scene may leave some wondering if there’s a need for a simple cash-dis- pensing device when more transactions are shifting to the digital form. For financial institutions, shifting delivery of some services to mobile de- vices could cut operational costs, according to Alan Goode, an analyst with Basingstoke, England-based Juniper Research. In a report “Mobile — The ATM in your pocket,” Goode wrote, “Data from the U.S. is already pointing to the fact that there is a slow down in the physical ATM market and it won’t be changed by the deployment of intelli- gent mobile ATM solutions that allow mobile users to get statements, make payments and even top-up mobile prepaid via their mobile phones.” For IADs, it’s easier to take a wait-and-see approach to new technology. It’s not enough to simply have the latest cool thing. “Once there’s a way you can make money by turning a mobile application or a mobile transaction into a revenue stream, they’re all for it,” said James Phillips, vice president of sales and marketing for Triton Inc., a Long Beach, Miss.-based ATM manufacturer. Although it might seem obvious that the growth of mobile payments would result in a drop in cash usage, the opposite is true, according to Tom Harper, president of the ATM Industry Association and publisher of ATM- marketplace.com and MobilePaymentsToday.com. “In our research we’ve found that cash use is actually growing in the United States and around the world,” Harper said. “And it’s not just growing, but growing at an increasing rate. Just a few years ago it was increasing at 3 to 4 percent. Last year it increased 6 percent. And with mobile payments exploding, it’s almost counterintuitive.” In fact, the Consumer Payments Research Center’s “Survey of Consumer Payment Choice” shows that cash is still the most familiar and frequently “Ultimately banks are looking to combine channels to make it easier for the customers” — David Albertazzi, senior analyst with the Boston-based Aite Group.

- 3. The Impact of Market Turbulence on ATMs 3© 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 used payment type. Although cash transaction amounts have gotten smaller over time, the frequency of cash usage and the average amount of cash in use are rising in the U.S. population overall. Research from the Federal Reserve Bank found that cash makes up nearly 29 percent of consumer transactions. Overall, U.S. consumers use $1.2 trillion in cash each year. This mini-guide, distributed without cost by ATMmarketplace.com and MobilePaymentsToday.com, media properties of Networld Media Group, outlines five ways that the ATM industry can respond to mobile technology. Prestaging and the mobile device Major ATM manufacturers have already announced technology that inte- grates mobile devices with ATM functionality. In effect, the mobile device re- produces an ATM’s keypad and monitor and its ability to authenticate users. Prestaging an ATM transaction on a mobile device leverages that fact. But is it a real way to make ATMs safer or faster, or is it a technology solution ahead of the marketplace? Manufacturers are taking different approaches. For instance, the device may incorporate GPS technology to ensure the physical location of the mobile device. Also, systems may trigger a transaction with a bar code or a number sequence. The goal is the same: to provide a cardless, simple-to-use way to get cash at the ATM. ATM industry giant NCR Inc. has developed software that lets bank custom- ers conduct cash withdrawals using their mobile devices without the need for an ATM card. The customer uses an app on his mobile device that’s linked to his bank account. The customer enters a password on the mobile device to initiate the transaction and elects the account and amount of cash to be withdrawn. A QR code appears on the screen of the ATM. The cus- tomer scans the code with the phone and the ATM dispenses the cash. Consumers don’t have to use a card or enter their ATM PIN, and they receive cash within 10 seconds. An e-receipt for the transaction is sent automatically to the customer’s email address. This process would allow customers access to cash from their accounts without the need for a payments card. If a person fully adopts a mobile wallet, then he could leave his cards at home and still have access to cash with the mobile device.

- 4. The Impact of Market Turbulence on ATMs 4© 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 Wincor Nixdorf has developed its own mobile application, which allows a bank customer to prestage a cash withdrawal on a smartphone. The app also uses a QR code as a token to confirm the transaction. Also, the app can show the way to the nearest ATM that supports the mobile cash app. In contrast to NCR’s solution, Wincor Nixdorf’s app displays the QR code on the smartphone, and the ATM must be equipped to read the code. A transaction PIN can be entered as an additional security feature. The QR code can be stored in the Passbook app in an Apple iOS device, or in Wincor Nixdorf’s PC/E Mobile Cash app. Also, Android devices can support near-field communication interaction instead of the QR code. The app replaces the function of the ATM keyboard, which could allow for faster service at ATMs with long queues. At an airport or amusement park, a user could prepare the transaction while waiting in line and then complete the withdrawal simply by scanning the QR code. Diebold has debuted its solution for cardless withdrawals. The preregis- tered user integrates the mobile device by scanning a QR code on the ATM screen. This step connects the ATM with the mobile device and authenti- cates the user via the QR code without the use of an ATM card. When the devices sync, a transaction screen appears on the mobile device, where the customer selects the withdrawal amount. The ATM then sends a one-time numerical code to the customer’s device, which the customer enters on the ATM screen to authenticate the transaction and receive cash. The cardless transactions reduce consumer security risks related to lost or stolen cards, as well as the opportunity for skimming. Privacy is enhanced when users input transaction details on the smartphone screen rather than 2011 2012 Checked an account balance or recent transactions 90% 87% Transferred money between two accounts 42% 53% Downloaded your bank's mobile banking app 48% 49% Received a text message alert from your bank 33% 29% Made a bill payment using banking website or app 26% 27% Located the closest in-network ATM for your bank 21% 24% Deposited a check using mobile phone camera 11% 21% Source: U.S. Federal Reserve Mobile transaction Using your mobile phone, have you done any of the following in the past 12 months? The goal is the same to provide a cardless, simple-to-use way to get cash at the ATM.

- 5. The Impact of Market Turbulence on ATMs 5© 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 the ATM screen. In addition, the one-time authentication code expires im- mediately after completion of a transaction. Banks are getting in on the action directly. Royal Bank of Scotland has rolled out a mobile device app that allows customers to withdraw money at its ATMs without a card. To request cash, the user opens the password-protected app and taps the screen to reveal a six-digit, single-use password to be entered at the ATM. The code is valid for a limited period of time at any one of 8,000 RBS-, NatWest- or Tesco-branded ATMs in the U.K. At the moment, the customer service benefits for FIs seem obvious, but the question remains whether IADs will adopt the prestaging technology anytime soon. “We don’t see the IADs coming to the manufacturers asking us to support this because there’s not a big revenue stream in it for them,” Triton’s Phillips said. Contactless transactions and ATMs The migration to the EMV standard will also entail migration to near-field communication at the POS and at the ATM. Ubiquity of NFC in the North American market is still many years down the road, but ATM deployers are preparing for that change. NFC could be ready for prime time soon. Emerging technology forecasting and analysis firm ABI Research expects shipments of NFC-enabled devices to skyrocket from 102 million in 2012 to 1.95 billion in 2017. The future of NFC in Apple iOS devices is uncertain at this point, but the debut of an iPhone with NFC capability should speed up consumer acceptance. “Thinking further ahead, this kind of contactless technology at both ATMs and point-of-sale terminals may mean the end of plastic cards in a decade or two,” Mike Lee, CEO of ATMIA, wrote BankNews.com. NFC could be another link between mobile devices and ATMs. NFC could supplant the QR code or the one-time-use PIN in ATM authentication protocols. That would eliminate the step of reading a code with a phone or entering digits for identification. Atlanta-based SunTrust Banks ($178 billion) has upgraded its fleet of NCR ATMs to units that can communicate with near-field-communication- enabled smartphones and accommodate international chip-and-PIN security protocols. “Thinking further ahead, this kind of contactless technology at both ATMs and point-of-sale terminals may mean the end of plastic cards in a decade or two” — Mike Lee, CEO of ATMIA, BankNews.com

- 6. The Impact of Market Turbulence on ATMs 6© 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 The upgraded ATMs will allow SunTrust customers to use smartphones as an authentication device. Mobile authentication, in which people wave a mobile phone near the NFC-enabled ATM to identify themselves, has proven a popular method to access ATMs in Asia. SunTrust managers said they will retrofit existing ATMs to accept mobile authentication as an option. ATMs and the unbanked The unbanked and underbanked sectors, representing nearly 60 million U.S. residents, have traditionally been served by a variety of alternative financial services providers, including check-cashing stores, money-transfer services and alternative credit sources. With a smartphone, consumers carry a virtual bank in their pockets. The re- sult is that the unbanked (whether by choice or by necessity) have options for many financial services without the need for a bank. However, they may still need ATMs. Prepaid card providers could offer mobile-enabled ATM transactions — although they’re not on the market just yet — to give users of the prepaid cards the same access to cash enjoyed by customers with traditional bank- ing relationships. ATMs provide the unbanked access to the cash stored on the network- branded prepaid cards that are as common as bank-branded debit or credit cards. Prepaid cards such as Green Dot, widely available in convenience and discount stores, give the unbanked customer access to the financial system via ATMs and point-of-sale transactions. Technology now exists for ATMs to dispense prepaid cards from a multicas- sette ATM, loaded with the desired value. In concert with a cash-accepting ATM, an operator dispensing network-branded prepaid cards could offer an end-to-end transaction via the ATM rather than at a retailer’s cash wrap. Unbanked/underbanked Unbanked Underbanked U.S. consumers 9.50% 9.90% Have access to a mobile phone? 59% 90% If yes, is mobile phone a smartphone? 50% 56% Source: U.S. Federal Reserve The unbanked have options for many financial services without the need for a bank, but they may still need ATMs.

- 7. The Impact of Market Turbulence on ATMs 7© 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 For instance, a family could load a balance at the ATM on prepaid cards for their children, who can then withdraw smaller amounts of cash as the need arises or use the prepaid card for POS payments. If the prepaid card provider offered the service, they could then use mobile devices to interact with ATMs the same way a bank customer would. As a reflection of the still-evolving nature of the ATM/mobile convergence, Houston, Texas-based PreCash is testing FlipMoney, a digital wallet app linked to a prepaid debit card designed for people without bank accounts. The app allows users to deposit checks and pay bills on the mobile device and use the prepaid debit card to interact with ATMs and POS terminals. Expanded ATM services There’s more to consider than a direct relationship between ATMs and mo- bile devices. Mobile is changing the entire banking landscape, meaning that more transactions are being done by mobile devices. That hits deployers’ margins. The answer may be in moving beyond cash dispensing to offer new services and sources of revenue such as ticketing, loading prepaid cards, content downloads, device-charging services and a host of other possibilities such as buying prepaid phone minutes or money orders. For instance, international travelers could order foreign currency online and then use the mobile device to authenticate a transaction at an airport ATM to pick up the cash. In many markets outside the United States, ATMs offer an array of expand- ed services that provide a revenue stream in addition to interchange and surcharge fees. In South Africa, Standard Bank offers purchase of prepaid airtime for cell phones via its ATM fleet. Tickets for entertainment venues and transportation have been offered by ATMs in some locations, as an expanded transaction and additional rev- enue stream for IADs. In the U.S., a number of entities have tested general-purpose reloadable card purchases at the ATM. “The deployers are mainly trying to find out how to increase ATM usage,” Albertazzi said. “The card sales have been very small, but the opportunity for prepaid is growing.” Triton has beta-tested a nondenominated gift card that allows the user to set the amount of the gift card available from an ATM. That’s a way for IADs to avoid prepurchasing gift-card stock in specific denominations.

- 8. The Impact of Market Turbulence on ATMs 8© 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 Technology is making direct personal payments easier. Diebold has demoed a process for person-to-person payments using mobile and ATM interactivity. A customer can set up a prestaged transaction that authorizes access to cash to a third party. The customer inputs the payment amount and recipient’s contact information, which can be selected directly from his or her contact list. The recipient then receives a one-time code he can use at an ATM or branch to receive money. This functionality could bridge the last gap for electronic payments, the need for cash for small transactions between regular people. Paying a baby sitter, buying Girl Scout cookies, or sending cash to a child who decided to go to the movies could become much easier with the third-party transaction via the ATM. In April 2012 Burlingame, Calif.-based Nexxo Financial Corporation de- moed its K3000 “Bank-in-a-Box,” an ATM hybrid that allows consumers to cash checks, buy money orders, load prepaid cards, pay bills, send money, top up phone minutes and withdraw cash all at one machine — and all without a bank account. Nexxo offers users a Mobile MoneyStation app to access their accounts. A user can deposit a check using the check reader on the machine and then access the money via the mobile app to pay bills or transfer money. Expanded ATM/mobile capabilities Mobile devices have radically altered consumers’ expectations of what technology can deliver to them. They expect services well beyond simply dispensing cash. FIs could lead the way in providing mobile technology that offers advanced services as well as ATMs that can do everything from dispensing cash to processing loans. Many FIs, some large IADs such as Cardtronics and surcharge-free net- works such as MoneyPass from Elan Financial Services, offer mobile apps that locate ATMs in the network. But that’s simply a wayfinding utility, not a channel integration. With the right strategies and technologies, consumers could come to see their mobile phones as ATMs in their pockets or purses. But there are limits to how much the majority of consumers will risk in adopting technologies connected to their wallets. Consumers will want to be able to conduct an ATM transaction regardless of device or app. “If a transaction is going to be successful, it has to be ubiquitous across all platforms,” Phillips said. “The first time a user goes to a machine expecting A customer can set up a prestaged transaction that authorizes access to cash to a third party. The recipient receives a one- time code he can use at an ATM or branch to receive money.

- 9. The Impact of Market Turbulence on ATMs 9© 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 to do a transaction and this machine doesn’t support it, they start to lose faith in being able to do that transaction at an ATM.” Standard Bank in South Africa launched a “Pay Your Way” service for person-to-person mobile payments. This solution is almost as flexible as cash from an ATM because it does not require preloading the payee into the system. A payment can be handled in an impromptu fashion, like with- drawing cash from an ATM. In the U.S., many true peer-to-peer payments are still handled with cash, such as splitting a check in a restaurant or buying castoffs at a garage sale. The truly impromptu payment may be the last great frontier for cash, until the mobile payments infrastructure supports widely accepted secure pay- ments standards. “The ability to simply pay a person without having all their bank information and just an email account is going to be one of the solutions that affect the use of cash the greatest,” Albertazzi said. One question in the market is how strongly will U.S. consumers use ad- vanced ATMs. Will customers use ATMs to download music or ring tones, or charge their mobile devices? And what would that mean for the core cash-withdrawal function of the standard retail ATM? “People expect ATMs to dispense cash, and you don’t want to do other things at a machine that will inhibit somebody from getting cash, certainly in the IAD world where they make money off every transaction,” Phillips said. ATM manufacturers, especially in the retail space, are reluctant to get too far ahead of the marketplace. They’d rather let the FIs invest in creating the technology and consumer demand first, and then adapt ATMs to serve the customer base. “Nobody wants to spend money on research and development and have to scrap it and start over,” Phillips said. In the future, the ATM could become the hub linking the bank and the branch to the consumer, using existing payment rails. The gamut of devic- es, from smartphones and tablets to desktop terminals to automated stand- alone kiosks, could use the ATM to deliver cash and other transactions. The distinction between an in-person and online consumer is blurring, so the bank of the future will be a multichannel, multifunction and multidevice environment, with self-service channels simply a part of the entire range of transaction types. “If a transaction is going to be successful, it has to be ubiquitous across all platforms”

- 10. The Impact of Market Turbulence on ATMs 10© 2013 Networld Media Group | Sponsored by atm & mobile executive summit: 2013 Is your bank ready for mobile/ ATM convergence? At this event, you will learn what mobile + ATM technologies and business models are working now and in the near future, how customers are reacting, how to protect from cyber threats, where payments regulation is heading, and more. What’s hot in mobile right now (and what’s coming) How to prepare for and protect from cyber threats How banks are integrating their atm & mobile channels Major regulatory issues coming our way What’s a bank to do with the cashless society? • • • • • SAVE $800 WITH CODE: AMCWP OFFER EXPIRES 7/31