Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à 8 c 2

Similaire à 8 c 2 (20)

8 c 2

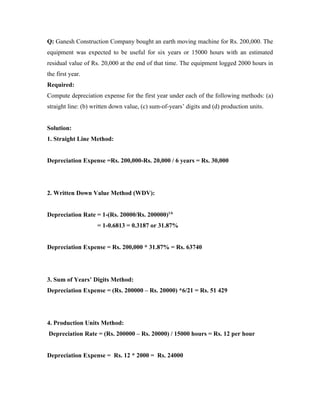

- 1. Q: Ganesh Construction Company bought an earth moving machine for Rs. 200,000. The equipment was expected to be useful for six years or 15000 hours with an estimated residual value of Rs. 20,000 at the end of that time. The equipment logged 2000 hours in the first year. Required: Compute depreciation expense for the first year under each of the following methods: (a) straight line: (b) written down value, (c) sum-of-years’ digits and (d) production units. Solution: 1. Straight Line Method: Depreciation Expense =Rs. 200,000-Rs. 20,000 / 6 years = Rs. 30,000 2. Written Down Value Method (WDV): Depreciation Rate = 1-(Rs. 20000/Rs. 200000)1/6 = 1-0.6813 = 0.3187 or 31.87% Depreciation Expense = Rs. 200,000 * 31.87% = Rs. 63740 3. Sum of Years’ Digits Method: Depreciation Expense = (Rs. 200000 – Rs. 20000) *6/21 = Rs. 51 429 4. Production Units Method: Depreciation Rate = (Rs. 200000 – Rs. 20000) / 15000 hours = Rs. 12 per hour Depreciation Expense = Rs. 12 * 2000 = Rs. 24000

- 2. Q: Bond Company bought for Rs. 600,000 a piece of equipment for detecting defective bottles. The equipment has an estimated useful life of six years and an estimated residual value of Rs. 60,000. It is expected to last 50,000 hours. The machine worked 10,000 hours in a year 1: 18000 hours in year 2: 2000 hours in year 3: 11000 hours in year 4: 6000 hours in year 5 and 3000 hours in year 6. Required: 1. Compute yearly depreciation expense for each year under each of the following methods: (a) straight line: (b) written down value, (c) sum-of-years’ digits and (d) production units. 2. Comment on the trend of yearly depreciation expense and book value.