Recommended

More Related Content

Similar to European fund distribution 2014

Similar to European fund distribution 2014 (20)

Recently uploaded

Recently uploaded (20)

European fund distribution 2014

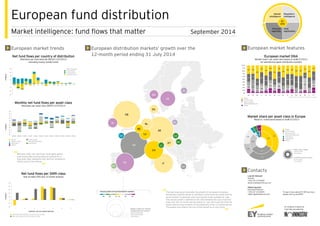

- 1. European fund distribution Market intelligence: fund flows that matter September 2014 Contacts Laurent Denayer Partner +352 42 124 8340 laurent.denayer@lu.ey.com Rafael Aguilera Executive Director +352 42 124 8365 rafael.aguilera@lu.ey.com To learn more about EY GFD services, please visit ey.com/GFD EY analysis is based on fund data provided by Regulatory intelligence Fund registration Market intelligence Fund tax reporting EY GFD European market trends European distribution markets’ growth over the 12-month period ending 31 July 2014 European market features The heat map above illustrates the growth of the largest European distribution markets based on variations of the total net assets held by local investors in domestic and cross-border funds available for sale. The annual growth is defined by the ratio between the sum of all fund flows over the 12-month period ending 31 July 2014 and the total net assets held by local investors at the beginning of the 12-month period. The bubble size reflects the size of the market as at July 2014. “ ” Annual growth of local distribution markets -9% -5% -1% 1% 5% 9% Bubble scaling for market insight (total net assets) About €500 billion About €250 billion <€50 billion -30 -20 -10 0 10 20 30 40 DE FR GB IT CH ES SE LU NL IE AT NO DK BE FI PT -50 -40 -30 -20 -10 0 10 20 30 40 50 08/2013 09/2013 10/2013 11/2013 12/2013 01/2014 02/2014 03/2014 04/2014 05/2014 06/2014 07/2014 -20 -10 0 10 20 30 40 50 1 2 3 4 5 6 7 15% 7% 5% 6% 9% 17% 8% 15% 6% 9% 13% 2% 5% 9% 4% 20% 14% 9% 9% 20% 11% 19% 14% 20% 9% 9% 10% 4% 7% 43% 6% 15% 12% 32% 14% 8% 8% 11% 9% 3% 12% 11% 6% 13% 3% 1% 10% 13% 27% 21% 23% 40% 35% 31% 19% 39% 29% 39% 39% 41% 47% 19% 36% 31% 31% 31% 48% 25% 37% 22% 49% 23% 44% 32% 32% 39% 39% 27% 44% 22% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% DE FR GB IT CH ES SE LU NL IE AT NO DK BE FI PT 33% 33% 23% 4% 4% 3% 35% 27% 12% 16% 3% 3% 4% DE FR GB IT CH ES SE LU NLIE AT NO DK BE FI PT GR PL CZ LI GG HU Net fund flows per country of distribution Allocation per fund domicile 08/2013-07/2014 excluding money market funds European market DNA Market share* per asset class based on AuM 07/2014 for selected European distribution markets Market share per asset class in Europe Retail vs. institutional based on AuM 07/2014 Monthly net fund flows per asset class Allocation per asset class 08/2013-07/2014 Net fund flows per SRRI class Year-to-date (YtD) and 12-month analysis €billions€billions Synthetic risk and reward indicators €billions Equity Money market Alternative Others Fixed income Allocation/balanced Guaranteed Net fund flows 08/2013-07/2014 (12 months) Net fund flows 01/2014-07/2014 (YtD) Other domiciles IE domiciled LU domiciled Domestic funds Equity Fixed income Money market Allocation/balanced Alternative Guaranteed Others Equity Fixed income Money market Allocation/balanced Others * Market shares may not sum to 100% due to rounding Retail share classes (outer circle) €4.8 billion Institutional share classes (inner circle) €1.3 billion Recently (YtD), low-risk funds could again attract new money after having suffered outflows for a long time. Risk categories four and five continue to attract most of the inflows. “ ”