How fico scoring system is essentially linked to your lifestyle

•

0 j'aime•222 vues

Being frugal, vigilant and consistent can help you to have a shiny credit score. The scores that we have on our credit reports can be improved if we make it a goal to raise it, and bring our lifestyle in sync with this goal. The perfect credit utilization, proper discriminate between instalment loan and recursive loan etc have to take into consideration for shiny credit score.

Recommandé

Contenu connexe

Dernier

Dernier (20)

En vedette

En vedette (20)

How fico scoring system is essentially linked to your lifestyle

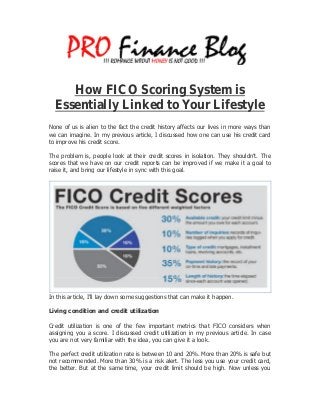

- 1. How FICO Scoring System is Essentially Linked to Your Lifestyle None of us is alien to the fact the credit history affects our lives in more ways than we can imagine. In my previous article, I discussed how one can use his credit card to improve his credit score. The problem is, people look at their credit scores in isolation. They shouldn’t. The scores that we have on our credit reports can be improved if we make it a goal to raise it, and bring our lifestyle in sync with this goal. In this article, I’ll lay down some suggestions that can make it happen. Living condition and credit utilization Credit utilization is one of the few important metrics that FICO considers when assigning you a score. I discussed credit utilization in my previous article. In case you are not very familiar with the idea, you can give it a look. The perfect credit utilization rate is between 10 and 20%. More than 20% is safe but not recommended. More than 30% is a risk alert. The less you use your credit card, the better. But at the same time, your credit limit should be high. Now unless you

- 2. bring changes in your lifestyle, the credit limit-lower usage combo is difficult to maintain. That’s because a high credit limit is tempting. Preventing yourself from spending freely, when you are at a shopping mall, or in a restaurant is not easy at all. But as I said, lifestyle changes are necessary for a better credit score. Student loan We have the best schools in the world, but the course fees of undergraduate and graduate programs are often quite high, and getting a scholarship is incredibly difficult. The question is if you take a loan, would that affect your FICO score. There’s no definitive answer because the graph below shows it’s perfectly possible that someone has a student loan of over $50000, and at the same time, getting a score of 800 on his credit report. FICO may not treat a student loan any different than it treats a mortgage loan, but the delinquency rate of student loan has been increasing at a rapid pace. So, live a frugal life and look for additional earning opportunities, so you pay off the loan as quickly as you could. Understand the difference It’s less of a lifestyle change and more of a perspective change. Most people make a mistake. They don’t discriminate between instalment loan and recursive loan.

- 3. Remember, FICO considers your payment history when it assigns you a score. In fact, your payment history makes up 35% of the overall FICO score. When FICO checks payment history, it considers both instalment loans as well as revolving loans such as the credit card debt. However, it takes instalment loans more seriously. If you don’t promptly pay down the revolving loan, then that’d affect your credit history, but being a defaulter on an instalment loan such as a mortgage loan or a student loan might damage your credit score severely. Hence, if you have a mortgage or student loan to pay, make it your immediate priority, and shift the focus from your credit card outstanding balances, even though the latter is important too. Equal importance What I am going to advise in this paragraph, might appear to be in contrast with what I’ve advised in the previous paragraph. My advice is give equal importance to installment loan and revolving loan. It’s true that an installment debt is different from a revolving debt. It’s also true that not paying an installment debt can damage your score seriously. Nevertheless, if you ignore the revolving debt, you’d score low in the credit mix category. A person with impressive credit mix is one, who pay down all sorts of debts, without discriminating. So, acknowledge the difference, but don’t delay paying off any of these two types of debts. Account maintenance duration You need to show FICO that you are consistent. One of the factors, considered by FICO is the duration of your account. The rule of the thumb is, the longer the better. This simply means if you are new to credit, in other words, if your account doesn’t have a long history, then FICO is likely to give you a low score. Don’t close an account if you have been maintaining it for long. For the same reason, make sure you don’t have a dormant account. If you do, then activate that account asap. Change yourself if you are an impulsive and forgetful person. Otherwise, your credit score will decline. Author Bio- Get to Know Me Better. Hi, I'm TINA! I am a financial planner, blogger, and freelance writer and digital marketing consultant at http://profinanceblog.com. The idea of starting a finance blog has been hitting me for long; I took it seriously after falling into a spiral of finance debacles and recovering from it.