FEX | Industrie & Energie | 131112 | Conferentie Schaliegas & Olie | Presentatie | Gürcan Gülen

•

0 j'aime•709 vues

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (19)

En vedette

En vedette (16)

Similaire à FEX | Industrie & Energie | 131112 | Conferentie Schaliegas & Olie | Presentatie | Gürcan Gülen

Similaire à FEX | Industrie & Energie | 131112 | Conferentie Schaliegas & Olie | Presentatie | Gürcan Gülen (20)

Plus de Flevum

Plus de Flevum (20)

Dernier

Dernier (20)

FEX | Industrie & Energie | 131112 | Conferentie Schaliegas & Olie | Presentatie | Gürcan Gülen

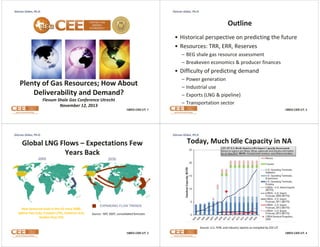

- 1. Gürcan Gülen, Ph.D. Gürcan Gülen, Ph.D. Outline • Historical perspective on predicting the future • Resources: TRR, ERR, Reserves – BEG shale gas resource assessment – Breakeven economics & producer finances • Difficulty of predicting demand Plenty of Gas Resources; How About Deliverability and Demand? Flevum Shale Gas Conference Utrecht November 12, 2013 – – – – Power generation Industrial use Exports (LNG & pipeline) Transportation sector ©BEG-CEE-UT, 1 Gürcan Gülen, Ph.D. Gürcan Gülen, Ph.D. Global LNG Flows – Expectations Few Years Back 2000 New terminals built in the US since 2000: Sabine Pass (LA), Freeport (TX), Cameron (LA), Golden Pass (TX) ©BEG-CEE-UT, 2 Today, Much Idle Capacity in NA 2030 EXPANDING FLOW TRENDS Source: NPC 2007, consolidated forecasts Source: U.S. FERC and industry reports as compiled by CEE‐UT. ©BEG-CEE-UT, 3 ©BEG-CEE-UT, 4

- 2. Gürcan Gülen, Ph.D. Gürcan Gülen, Ph.D. Thanks to Shale Gas Production Source: EIA Annual Energy Outlook 2013 ©BEG-CEE-UT, 5 Gürcan Gülen, Ph.D. ©BEG-CEE-UT, 6 Gürcan Gülen, Ph.D. Technically Recoverable Resource Estimates Shale Gas Mostly Responsible for Increased Estimates but… • Shale gas resource estimates cover a wide range • Some are for TRR; others are for ERR • Assumptions & approach not always transparent Source: Based on a widely used chart produced by Gas Technology Institute (GTI). ©BEG-CEE-UT, 7 Source: McGlade C, Speirs J, Sorrell S (2013). Unconventional gas – A review of regional and global resource estimates. Energy. ©BEG-CEE-UT, 8

- 3. Gürcan Gülen, Ph.D. BEG’s Integrated Approach: Barnett, Fayetteville, Haynesville, Marcellus Log and seismic data Structure, porosity, net pay-zone maps Production history data and directional surveys Decline Analysis: Production rate estimate, EURs Spacing Study: Well Recovery, Drainage Areas, Infill drilling locations (by tier) => Technically Recoverable Resources Attrition rate, Breakeven prices, Representative well profiles (by tier) Production Outlook: Pace of drilling and ultimate recovery w.r.t. Prices, Technology, and Time www.beg.utexas.edu/sloan.php Funded by Alfred P. Sloan Foundation $10 Tcf @ $10 HH Tcf per Year (Base Case Sensitivity to Price) $8 2 Tcf @ $4 HH $7 Tcf @ $3 HH $6 1.5 Henry Hub $2010 $5 $4 1 $3 Base Case @ $4 HH 45 Tcf Cumulative Production 0.5 $2 $1 $- 0 1995 2000 2005 2010 2015 2020 ©BEG-CEE-UT, 9 Gürcan Gülen, Ph.D. $9 Tcf @ $6 HH Well Economics: Econometric Analysis: Validate Decline Curve; Test Geologic and Other parameters; Describe “typical well” 2.5 Tcf per Year Geologic Analysis: Barnett Shale Resources Henry Hub $2010 Gürcan Gülen, Ph.D. 2025 2030 ©BEG-CEE-UT, 10 Gürcan Gülen, Ph.D. At What Price Can the Producers Deliver? Depends on Location $18 $16 $14 Breakeven Economics – 10% IRR Barnett Low Btu $12 $10 Barnett High Btu $8 NGL Uplift: how much, when & where? $4 Henry Hub $6 $4 $2 $0 Tier 1 Tier 2 Tier 3 Tier 4 Tier 5 Tier 6 Tier 7 Tier 8 Tier 9 Tier 10 Monitoring U.S./Global Oil and Gas: Upstream Attainment, Producer Challenges http://www.beg.utexas.edu/energyecon/thinkcorner/Think%20Corner%20‐%20Producers.pdf ©BEG-CEE-UT, 11 BEG analysis. ©BEG-CEE-UT, 12

- 4. Gürcan Gülen, Ph.D. Gürcan Gülen, Ph.D. Price Expectations How Much Demand? At What Price? • • • • Power generation Industrial demand Exports (LNG and pipeline) Transportation (LNG, CNG) Foss et al, “Sharp Cycles Ahead” Oil & Gas Investor, September 2013 ©BEG-CEE-UT, 13 Gürcan Gülen, Ph.D. ©BEG-CEE-UT, 14 Gürcan Gülen, Ph.D. Gas Use in Generation Increased Different Views of the World Net generation by fuel, 1998‐2012 Consumption of Natural Gas (Index, 2010 = 1) 2.5 Avg y‐y growth of 2.5% 2.0 1.5 1.0 0.5 AEO Real GDP IHS Real GDP AEO Industrial IHS Industrial AEO Electricity IHS Electricity 0.0 2010 2015 2025 2030 2035 Based on data from EIA AEO 2013 & IHS Global Insight 2040 ©BEG-CEE-UT, 15 15% 2% 19% 3% 52% 31% 2020 5% 19% 0% 37% 1998 2012 ©BEG-CEE-UT, 16

- 5. Gürcan Gülen, Ph.D. Gürcan Gülen, Ph.D. A Scenario on Gas Use in Power More Risk for Coal & Nuclear – announced about 32 GW (2014‐2020) – 2.6 GW in 2011; 8 GW in 2012; 2 GW in 2013 YTD already retired (mostly older, smaller units) • 4 recent nuclear retirement announcements; more on the way? 9 8 7 Quads • Pending EPA regulations on SO2/NOX, mercury, water, coal ash, GHG • State‐level regulations • Up to 80 GW of coal capacity may retire by 2020 Nuclear shutdowns 6 Change in Gas Price Forecast 5 Coal risks 4 3 2 1 Quad 1 tcf ~2.7 bcfd 1 0 2030 U.S. Gas‐Power Linkages: Building Future Views for details: http://www.beg.utexas.edu/energyecon/thinkcorner/Think%20Corner%20Gas‐ Power%20Linkages.pdf ©BEG-CEE-UT, 17 Gürcan Gülen, Ph.D. ©BEG-CEE-UT, 18 Gürcan Gülen, Ph.D. Dampers on Gas Use in Power • Currently, coal is competitive with gas at $4‐4.5/MMBtu of gas price (even at $3.5 in some locations) • Renewables capacity has been growing Increased Industrial Competitiveness 2005 2012 HH $8.69 $2.75 WTI $56.64 $94.00 Ratio 6.5 34.2 – Better capacity factors for wind – Declining cost of PVs (thanks to Chinese subsidies) – Storage projects seem to be moving forward • Smart grid and demand response • Energy efficiency and conservation (EIA AEO 2013 Reference Case: 0.9% annual demand growth; 0.2% in “best technology available” case) ©BEG-CEE-UT, 19 What happens if the WTI‐HH ratio declines? American Chemistry Council, Shale Gas Study (May 2013) ©BEG-CEE-UT, 20

- 6. Gürcan Gülen, Ph.D. Gürcan Gülen, Ph.D. Volatile Markets 140% Propane % of Oil 120% 12 NGL Composite % of Oil 10 Frac Spread ‐ Propane 100% Risks for Industrial Demand 14 HH % of Oil Frac Spread ‐ NGL Composite • Need to export petrochemical products – Domestic market seems saturated 8 6 80% 4 2 60% 0 40% ‐2 • • • • Tremendous petchem capacity additions globally Ethane‐naphtha cost differential Frac spread (ethane‐natural gas) Infrastructure bottlenecks ‐4 20% ‐6 0% ‐8 – Tens of billions of dollars worth of pipeline & processing projects are planned or already under development ©BEG-CEE-UT, 21 Gürcan Gülen, Ph.D. ©BEG-CEE-UT, 22 Gürcan Gülen, Ph.D. Industrial Gas Demand – A Growth Scenario based on Projects in Progress Increasing Gas Exports • Several terminals received permits to export LNG to non‐FTA countries – Construction started on 2 liquefaction trains of the Sabine Pass terminal in August 2012 – The first exports are not expected until 2016 • EIA AEO: 4.4 bcfd by 2027 (1.6 tcf per year) • Others: 6‐8 bcfd by 2020 and 8‐10 bcfd by 2025 (3.6 tcf) • Pipe exports to Mexico was 0.6 tcf in 2012 – Expected to reach 2.4 tcf by 2040 (EIA AEO) or sooner (much sooner). CEE analysis ©BEG-CEE-UT, 23 ©BEG-CEE-UT, 24

- 7. Gürcan Gülen, Ph.D. Gürcan Gülen, Ph.D. Is there Room for U.S. LNG Exports? Non‐North American LNG Supply 2012 Consumption: 328 bcm 2012 Liquefaction capacity: 388 bcm Source: Howard V. Rogers, Senior Research Fellow, The Oxford Institute for Energy Studies, and David Ledesma, South‐Court, LNG 17, Houston, 2013. ©BEG-CEE-UT, 25 Gürcan Gülen, Ph.D. ©BEG-CEE-UT, 26 Gürcan Gülen, Ph.D. Changing World LNG Trade – Exporters Mix Global LNG Market Risks • Slow economic recovery / growth – Continental European demand fell 6+ million tons (or ~9 bcm) between 2012 and 2013 • Japan re‐opening nuclear plants • Increased pipeline trade • Russia “flooding” the market; non‐Gazprom exports? • Global shale gas production (longer term) • Increased & more effective use of renewables; energy efficiency & conservation ©BEG-CEE-UT, 27 Small group dominated by Asian suppliers (1995) Algeria 19% Libya 2% Indonesia 36% Abu Dhabi 8% United States (export) 2% Brunei 9% Australia 11% Malaysia 15% Much more diversified, emerging Middle East suppliers led by Qatar Source: CEE calculations based on petroleum‐economist.com and BP Statistical Review of World Energy ©BEG-CEE-UT, 28

- 8. Gürcan Gülen, Ph.D. CEE analysis Jan‐2011 CEE analysis ©BEG-CEE-UT, 29 Gürcan Gülen, Ph.D. Mar‐2012 Henry Hub Sep‐2008 Liquefaction Nov‐2009 High Cost Pacific Jul‐2007 High Cost Europe May‐2006 High HH Jan‐2004 Low Cost LNG $/DGE Estimate Mar‐2005 Shipping U.S. No 2 Diesel Retail Prices (Dollars per Gallon) Nov‐2002 Regasification Henry Hub Gulf Coast Natural Gas Spot Price ($/DGE) Jul‐2000 $11/MMBtu Japan 2010 $10/MMBtu NBP $9/MMBtu European floor Diesel and Natural Gas Spot Prices (1997‐2013) $5.00 $4.50 $4.00 $3.50 $3.00 $2.50 $2.00 $1.50 $1.00 $0.50 $‐ Sep‐2001 $15‐16/MMBtu Asia spot May‐1999 16 15 14 13 12 11 10 9 8 7 6 5 4 3 2 1 0 NG Use in Transportation Encouraged by Diesel‐NG Price Differential Jan‐1997 $/MMBtu Is U.S. LNG Competitive? Mar‐1998 Gürcan Gülen, Ph.D. LNG trucks are ~30% more expensive than diesel trucks with emission systems ©BEG-CEE-UT, 30 Gürcan Gülen, Ph.D. Expectations Infrastructure Challenge • Only 32 public LNG fueling stations in operation, with about a third of them located in California; 41 private LNG filling stations; and 72 planned stations. • 587 CNG stations available to the public; 639 private filling stations; and 87 planned stations. • In comparison, there are 4,000 truck stops that sell diesel fuel. ©BEG-CEE-UT, 31 • The most aggressive scenarios: 1‐3 bcfd of incremental use by 2020 (1 tcf per year). • EIA: less than 0.3 bcfd by 2020. • Current use is about 0.1‐0.2 bcfd. American Clean Skies Foundation (2013) ©BEG-CEE-UT, 32

- 9. Gürcan Gülen, Ph.D. Gürcan Gülen, Ph.D. Putting All Together CEE “What If” Scenario 45 45 40 40 Transportation EIA ref 35 35 LNG exports EIA ref LNG exports CEE Pipeline exports EIA ref 30 30 Power generation EIA ref 25 Dry gas prod EIA ref Imports EIA ref 15 Total supply EIA ref 10 Total demand CEE High 25 TCF TCF Other EIA ref 20 Power generation CEE 20 Industrial CEE 15 Other CEE (EIA ref Other & Transportation) 10 Total supply EIA High OGR 5 0 2012 Pipeline exports CEE Industrial EIA ref 5 2015 2018 2021 2024 2027 0 2012 2030 2015 2018 2021 2024 2027 2030 ©BEG-CEE-UT, 33 Gürcan Gülen, Ph.D. ©BEG-CEE-UT, 34 Gürcan Gülen, Ph.D. What to Remember We Welcome Participation & Feedback • Shale gas resources are significant but – Costs for many locations are higher than $3‐3.5 – Infrastructure bottlenecks and environmental regulations can delay development – Conventional production has been declining – NGL revenues help • Demand side puzzles – Export markets are needed, at least for liquids & petrochemical products – The largest growth potential for gas use remains power generation, which depends on many uncertain factors ©BEG-CEE-UT, 35 Gürcan Gülen, Ph.D. Senior Energy Economist Center for Energy Economics Bureau of Economic Geology Jackson School of Geosciences The University of Texas at Austin 713‐654‐5404 (o) gurcan.gulen@beg.utexas.edu www.beg.utexas.edu/energyecon ©BEG-CEE-UT, 36