FEX | Industrie & Energie | 131112 | Conferentie Schaliegas & Olie | Presentatie | Lucia van Geuns

•

1 j'aime•452 vues

This document discusses the potential for shale gas and tight oil production to expand globally based on the success of these unconventional resources in the United States. It notes that non-OECD economies are driving increased energy consumption and outlines US policies supporting its energy independence. Technological advances like horizontal drilling and hydraulic fracturing enabled large-scale shale gas production in the US, lowering domestic natural gas prices. The US is projected to become a net exporter of natural gas by 2020. Significant shale oil and gas resources exist globally but face challenges in other regions due to infrastructure, policy, environmental and economic issues.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

En vedette (7)

Similaire à FEX | Industrie & Energie | 131112 | Conferentie Schaliegas & Olie | Presentatie | Lucia van Geuns

Similaire à FEX | Industrie & Energie | 131112 | Conferentie Schaliegas & Olie | Presentatie | Lucia van Geuns (20)

Plus de Flevum

Plus de Flevum (20)

Dernier

Dernier (20)

FEX | Industrie & Energie | 131112 | Conferentie Schaliegas & Olie | Presentatie | Lucia van Geuns

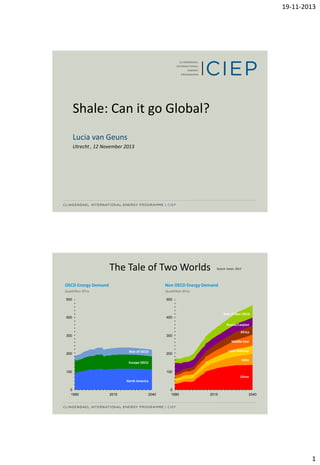

- 1. 19-11-2013 Shale: Can it go Global? Lucia van Geuns Utrecht , 12 November 2013 The Tale of Two Worlds Source: Exxon, 2012 OECD Energy Demand Non OECD Energy Demand Quadrillion BTUs Quadrillion BTUs 500 500 400 400 Rest of Non OECD Russia/Caspian Africa 300 300 Middle East Rest of OECD 200 Latin America 200 India Europe OECD 100 100 China North America 0 1990 2015 2040 0 1990 2015 2040 1

- 2. 19-11-2013 Non-OECD economies drive energy consumption growth… Source: BP energy Outlook 2030, 2012 Foundations of global energy system shifting (EIA WEO 2012) 1. All-time high oil prices acting as brake on global economy 2. Divergence in natural gas prices affecting Europe and Asia 3. Policy makers face critical choices in reconciling energy, environmental & economic objectives 4. US petroleum renaissance is a remarkable achievement of technology and innovation 2

- 3. 19-11-2013 US Energy Policy Direction 2005 “During the next four years, we will continue to enhance our economic security and our national security through sound energy policy. We will pursue more energy close to home, in our own country and in our own hemisphere, so that we're less dependent on energy from unstable parts of the world. And we will continue to work closely with Congress to produce comprehensive legislation that moves America toward greater energy independence.” President Bush - On the nomination of Secretary Bodman - Dec., 10, 2004 Types of unconventional gas Unconventional gas requires extensive use of horizontal drilling and hydraulic fracturing Source: E-on, 2010 3

- 4. 19-11-2013 The Barnett Story – Technology Makes the Difference 3000 Vertical Wells Deviated Wells Horizontal Wells Million Cubic Feet 2500 2000 1500 1000 500 0 85 90 *IHS Database 95 00 05 Date of First Production 10 Source: Schlumberger, 2013 Shale gas production leads growth in production through 2040 U.S. dry natural gas production trillion cubic feet History Projections 2011 Shale gas Non-associated offshore Tight gas Alaska Coalbed methane Associated with oil Non-associated onshore Source: EIA, Annual Energy Outlook 2013 Early Release 4

- 5. 19-11-2013 Natural gas consumption is quite dispersed with electric power, industrial, and transportation use driving future demand growth U.S. dry gas consumption trillion cubic feet History Projections *Includes combined heat-and-power and lease and plant fuel. **Includes pipeline fuel. Electric 32% power 31% 33% Industrial* 33% 2% 6% Gas to liquids Transportation** 3% 13% 12% Commercial 19% 14% Residential Source: EIA, Annual Energy Outlook 2013 Early Release Domestic natural gas production grows faster than consumption and the U.S. becomes a net exporter of natural gas around 2020 U.S. dry gas trillion cubic feet History Projections 2011 Consumption Domestic supply Net imports Source: EIA, Annual Energy Outlook 2013 Early Release 5

- 6. 19-11-2013 The success of shale gas in the US • In 2001, 1% of natural gas production came from shale compared to >20 today • Prices plummeted with positive effects on manufacturing (steel, petrochemical industry) by reducing costs of operations • The rapid expension of shale gas production occured because it was largely free of highly restrictive government policies • Expansion took place almost entirely on private land and was not subject of extensive access restriction and other federal regulations Percentage change in selected indicators in the United States, 2006-2011 Source: IEA. WEO, 2012 GDP (MER) Total primary energy demand CO2 emissions Gas demand Gas-fired power output Coal demand Coal-fired power output Renewables -15% -10% -5% 0% 5% 10% 15% 20% 25% From 2006-2011, United States CO2 emissions went down by 7% due to coal-to-gas fuel switching, power generation efficiency gains & increased renewables output 6

- 7. 19-11-2013 US lower 48 oil and gas shale plays Source: EIA, 2012 US oil production and rig counts Source: Argus 7

- 8. 19-11-2013 U.S. tight oil production leads a growth in domestic production of 2.6 mb/d between 2008 and 2019 U.S. crude oil production million barrels per day History 2011 Projections 8 STEO April 2013 U.S. crude oil projection 6 Tight oil 4 Other lower 48 states onshore 2 Lower 48 states offshore Alaska 0 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 Source: EIA, Annual Energy Outlook 2013 Early Release and Short-Term Energy Outlook, April 2013 Gas flares from Bakken fracking are visible from space Image: NASA Earth Observatory image/Suomi NPP 8

- 9. 19-11-2013 Shale oil and gas have the potential to dramatically alter world energy markets map of basins with assessed shale oil and gas formations, as of May 2013 Source: United States: EIA and USGS; Other basins: ARI Top ten countries with technically recoverable shale resources Shale oil Shale gas Rank Country Billion barrels Rank Country Trillion cubic feet 1 Russia 75 1 China 1,115 2 United States 58 2 Argentina 802 3 China 32 3 Algeria 707 4 Argentina 27 4 United States 665 5 Libya 26 5 Canada 573 6 Venezuela 13 6 Mexico 545 7 Mexico 13 7 Australia 437 8 Pakistan 9 8 South Africa 390 9 Canada 9 9 Russia 285 10 Indonesia 8 10 Brazil 245 World total 345 World total 7,299 Source: United States: EIA and USGS; Other basins: ARI. Note: ARI estimates U.S. shale oil resources at 48 billion barrels and U.S. shale gas resources at 1,161 trillion cubic feet. 9

- 10. 19-11-2013 Shale gas and tight oil resources and production Source: BP energy Outlook 2030, 2012 US shale gas and tight oil production success • • • Globally 240 Bbbs tight oil; 200 Tcm shale gas (technical recoverable resources) In 2012: 2.1 Mb/d (24%) of US oil production from tight oil; 24 Bcf (37%) of natural gas from shale gas US will continue to dominate in 2030 because of the importance of ‘above ground’ factors: – competitive environment – rig availability – robust service sector – land access facilitated by private ownership – deep financial markets – favourable fiscal and regulatory terms A competitive industry spurs continued technological innovation Source: BP energy Outlook 2030, 2012 10

- 11. 19-11-2013 Current European positions on shale gas drilling Source: The Economist, Febr 2013 Economics of unconventional gas in Europe The development of shale gas will only be successful in Europe if the environmental and economic boundary conditions can be fulfilled • Increase drilling efficiency; rig automation technology; zero harmful emissions; lowest possible environmental footprint • Reduce drilling and fracture cost by 50% • Development of clean fracturing technology • Investment in R&D to establish and build the required technology • Build human resource capacity to support large-scale field development • Develop and build required infrastructure Break-even costs for shale gas production in Europe: $5-12/MBtu Source: JRC, 2012 11