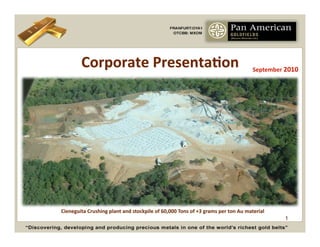

Pan American Power Point Sept 2010

•

1 like•490 views

Gold producer in Mexico MXOM - OTCBB

Recommended

Recommended

More Related Content

What's hot

What's hot (16)

Similar to Pan American Power Point Sept 2010

Similar to Pan American Power Point Sept 2010 (20)

More from Christopher R Anderson

More from Christopher R Anderson (20)

Recently uploaded

Recently uploaded (20)

Pan American Power Point Sept 2010

- 1. 1

- 2. The Quiet Gold Rush – Sierra Madre Gold belt Mexico Gold has been geHng harder to find and produce nearly everywhere in the world. Mexico's Sierra Madres have been experiencing a boom in gold discoveries and producCon. And yet not even half of the area has been explored. The last 10 years -‐ new mines of the Sierra Madre: Dolores -‐Minefinders, Mulatos -‐Alamos Gold, Pinos Altos -‐ Agnico Eagle, Ocampo-‐Gamon Lake, Palmarejo -‐Cour d'Alene, Monterde -‐ Kimber Resources, El Sauzal -‐ Goldcorp, and now Pan American Goldfields 2

- 3. Pan American Core Project Sierra Madre Occidental Gold-‐ LocaCon Silver Belt: • Over 40 million ounces of gold and more than 2 billion ounces of silver has been produced • More than 20 million ounces of gold have been Dropped --- _ discovered since 1992 Sold for $3.7 • The largest epithermal precious metal province Exploration --- million) inventory in the world and host a majority of Mexico’s In production gold and silver deposits AcquisiCons targeted in South and LaCn America 3

- 4. ExecuCve: experCse and a history of success • Director, Chairman Former President of the NaConal Mining AssociaCon of Mexico, he is a Mario Ayub metallurgist, with an extensive track record in mine exploraCon & development, his family has operated mines and other businesses in the region for generaCons and he has discovered and placed into producCon eight mines (including the Cieneguita) in Mexico. • President, Director, A Corporate lawyer and metallurgical engineer he co-‐founded MAG Silver George Young Corp. and InternaConal Royalty Corp. He was also the president of gold junior, Oro Belle Resources, and was responsible for acquiring and iniCaCng development of the now 11 million ounce Au Guacamayo project which Viceroy Resources acquired by taking over Oro Belle. Yamana Gold recently bought Viceroy principally to acquire the Guacamayo project. IRC was recently taken over by Royal Gold. Penoles abempted a hosCle take over of Mag Silver. • Director, A business administraCon and finance expert. Mr. Buchamer was the Randy Buchamer, Managing Director, OperaCons for The $5 billion revenues, 25,000 employee, Jim Paberson Group. Prior to this Mr. Buchamer was first the CIO and later the COO of Mohawk Oil Company Ltd. during its restructuring, corporate turnaround and lisCng on the Toronto Stock Exchange. At the Cme Mohawk was one of Canada's largest independent petroleum and convenience store retailers. 4

- 5. ExecuCve: experCse and a history of success • Independent An accomplished geologist and project manager with diverse experCse Director, Gary regarding the exploraCon and development of base and precious metals, Parkison industrial minerals, and uranium projects. Mr. Parkison was former Vice President-‐ExploraCon and Development for ConstellaCon Copper CorporaCon and Chief Geologist for Cambior USA, Inc. Managed various mine feasibility studies and development projects most recently the PEA for Chesapeake Gold’s Metates deposit, one of the largest undeveloped, disseminated gold deposits in the world. He is also credited with the Terrazas discovery – now Mexico’s largest silver-‐zinc deposit, and he idenCfied and outlined the Cerro de Marcado the largest iron oxide copper gold deposit ever found in Mexico. • Director, Mr. Neil Maedel is a SE Asia -‐based financier specializing in internaConal Neil Maedel, resource projects. Formerly the Director, Business Development of Manas Petroleum. Mr. Maedel is the editor of Switzerland based fincial leber Maedel’s. Mr. Maedel worked as a professional stock trader and researcher in Canada during the 1980s and has assisted in financing resource companies such as (Ultra Petroleum, Velvet ExploraCon, Manas Petroleum) for the past two decades. 5

- 6. Unique Opportunity • Completely carried to producCon with immediate cash flow at its flagship gold property – Cieneguita • Limited ProducCon commenced April 2010 ramped up to 950 OPM exit Dec 2010 1460 OPM (Au Eq.) • ExploraCon upside from 2 projects in Mexico's Sierra Madre gold trend • Current market capitalizaCon < US $20 MM • A classic “mine discovery-‐producCon cycle” opportunity • ExcepConal seven fold upside from upgrade of Cieneguita’s drill indicated to proven-‐ probable reserves ($30 per ounce to $210 per ounce P&P industry average) from 43-‐101 Drilled Resources 1.1 million ounces Au eq. • AcquisiCons targeted (producing gold mines with excellent exploraCon potenCal) in South and LaCn America. 6

- 7. Our Growth Strategy • Increase cash flow and producCon to 100,000 Au annually at Cieneguita • Upgrade drill indicated resources to proven probable thus increase reserve value from current $30 per ounce to current PP industry average of $210 per ounce. • AcquisiCon of producing properCes with significant growth potenCal in the Americas Strategic Mine Development Joint Venture – Mexico • Fully funded $8 million JV agreement in place for the future development of Cieneguita • First stage build mill develop pit and begin producCon at Cieneguita -‐ completed • Four million dollar second stage carried feasibility study to expand producCon 100% funded underway • Partner Minera Rio Tinto (MRT) – Local advantage and experCse 7

- 8. Corporate Developments New Chairman Board of Directors • Pan American was taken over by a new investor and group and execuCve beginning late 2009 • Its Corporate reorganizaCon and the filing of a disclosure document (S1) outlining the changes was executed under the direcCon of John Clair a private Investment Banker, and former Goldman Sachs ExecuCve and Law firm DLA Piper. • Restructured balance sheet eliminated 80% of of outstanding debt and liabiliCes • Commenced processing, shipping and selling gold copper silver concentrate from Cieneguita project. • CNQ lisCng TSX .V applicaCon under way 8

- 9. Share Structure Cash On Hand : $ 0.5 Million Burn rate (monthly): $120,000 Cash flow (MRT monthly: start Sept 2010 exit December 2010) $100,000 $194,000 Capital Structure: • Trading Symbol: OTCBB: MXOM & FRANKFURT: 0YA1 • Issued and Outstanding: 54,378,826 • Fully Diluted 89,378,826 • Warrants to expire December 31, 2010 1.454,000 • Warrants and options @ $0.50 or greater 11,113,000 • Corporate • CUSIP#: 6978 44 108 • State of Incorporation: Delaware , USA • Auditors: Myler & Company LLC • Transfer Agent: Corporate Stock Transfer • Legal Counsel DLA Piper (USA). • Management & Executive ownership of shares +14.4% including warrants/options 22.8% 9

- 10. Flagship Project -‐ Cieneguita Cieneguita, a new Au and polymetallic discovery in the Sierra Madre Occidental • Cieneguita Deposit In Situ Resource estimate within optimized Pit Shell @ 0.8 g/t AuEq Cut- off Measured Au eq.186,690 and Indicated 920,900 Total M&I 1,107,500 oz Au eq. • Hole CI-30 intersected 94.0 m of 1.21 g/t Au, 79.81 g/t Ag, 0.0.78% Pb and 1.19% Zn • Fully funded $9 million JV agreement with Minera Rio Tinto (MRT) • Production commenced Q2, 2010 by partner MRT 10

- 11. Cieneguita Gold-‐Silver Project Key Project CharacterisCcs: • Located ~20 km from Gold Corp’s El Sauzal mine (2.1 Moz Au) • MineralizaCon extends 900 meters along strike, is up to 300 meters wide and sCll remains open to the southwest and to depth • 100 holes completed for a total of 20,215.01 meters of drilling • Analysis results completed and received for 54 holes (CI-‐01 to CI-‐54) • Broad mineralizaCon intercepts including: CI-‐21: 111.5m with 1.2 g/t Au, 99.6 g/t Ag, 0.45% Pb & 0.73% Zn CI-‐30: 94m with 1.21 g/t Au, 79.81 g/t Ag, 0.7% Pb & 1.19% Zn CI-‐34: 55m with 3.99 g/t Au, 75.36 g/t Ag CI-‐35: 31m with 1.72 g/t Au, 67.36 g/t Ag, 0.56% Pb & 0.72% Zn CI-‐46: 23m with 8.93 g/t Au & 63.39 g/t Ag CI-‐47: 48.8m with 0.86 g/t Au, 166.9 g/t Ag, 0.52% Pb & 1.1% Zn CI-‐67*: 24.0m with 1.53 g/t Au and 107.36 g/t Ag CI-‐69*: 15.0m with 0.95 g/t Au and 510.2 g/t Ag, including: 4.5m @ 1.41 g/t Au and 1,072 g/t Ag • ExploraCon ongoing; infill drilling program has been designed to expand inferred resources 11

- 12. Cieneguita Gold-‐Silver Project Resource and PotenCal: • Large, outcropping and near-‐surface open pit gold-‐silver resource with upside laterally and with depth • Infill drilling displays excellent conCnuity of mineralizaCon and overall grades • Excellent infrastructure: highway and power, located close to a town site in a mining-‐friendly state • PotenCal porphyry system and for addiConal discoveries: Piedras Blancas 12

- 13. Cieneguita Project – Mexoro & MRT • Mexoro-‐MRT JV Agreement • 20:75 partnership to mine first 15 meters • $2,600,000 placement by new control group/execuCve • $4,000,000 investment to put Cieneguita into ProducCon (done) • $4,000,000 investment to take Cieneguita through the Feasibility stage • 60:40 Partnership to mine the complete Cieneguita deposit ayer bankable feasibility study completed • Exit 2010 at $190,000 monthly cash flow to Pan American 13

- 14. Cieneguita Gold-‐Silver Project ExploraCon and Future PotenCal Piedra Blanca Target: • New idenCfied area 500 meters to the south of the Cieneguita deposit • It is exhibiCng intense alteraCon characterized by quartz-‐ sericite-‐pyrite assemblages. Areas with intense fracturing and stockworks where limonites dominated by goethite and hemaCte are common • Assay results from surface sampling have returned values ranging from 0.30 to 4.04 g/t Au and 100 to 8900 ppm Cu • MineralizaCon extends at least 700 x 300 meters and is located in the intersecCon of main structures 14

- 15. Lab facilities at Cieneguita Gold-‐Silver Project 15

- 16. Encino Gordo Project Main Features: • Geology shows porphyries intruding volcanic rocks (dacite and andesite) • AlteraCon zones exhibit potassic alteraCon assemblages grading outward to quartz-‐sericite and propyliCc alteraCon • MulCple events of veining including: quarzt+chalcopyrite, quartz+pyrite, quartz+chalcopyrite+pyrite veins • Coincident copper and gold geochemical anomalies spaCally associated to a potassic alteraCon core • Geology, mineralizaCon and alteraCon assemblages suggest the presence of a porphyry-‐style mineralizaCon system 16

- 17. Encino Gordo Project ExploraCon: No exploraCon planned • Geological mapping and geochemical sampling has idenCfied: Anomaly N (similar environment to Coeur d’Alene’s Palmarejo which has +3 million ounces of gold equivalent and is only 4-‐ 5 km away) Elyka Structure (mineralized over 2 km long) 17

- 18. Acquisition Target #1 • Produced 37,000 oz/au 2009 • High grade (7 grams per ton) Au/equ. • Approximately 200,000 oz reserves (6 years production) in area currently being mined. • Property covers approximately 200 square Km. • Significant potential to expand reserves and production 18

- 19. Pan American Goldfields Summary • has just made the leap from explorer to gold producer – mine cycle opportunity • upgrade from indicated to proven probable reserves = potential 7 fold upside • bankable feasibility study for Cieneguita Mine expansion fully funded • accelerate growth through acquisition of producing gold mines • executive has proven track record of acquiring and developing major projects in North and South America 19

- 20. www.panamericangoldfields.org OTCBB: MXOM DISCLAIMER This presentaCon contains projecCons and forward looking informaCon that involve risks and uncertainCes regarding future events. Such forward-‐looking informaCon can include without limitaCon statements based on current expectaCons involving a number of risks and uncertainCes and are not guarantees of future performance of the CorporaCon. These risks and uncertainCes could cause actual results and the CorporaCon’s plans and objecCves to differ materially from those expressed in the forward-‐looking informaCon. Actual results and future events could differ materially from anCcipated in such informaCon. These and all subsequent wriben and oral forward-‐looking informaCon are based on esCmates and opinions of management on the dates they are made and expressly qualified in their enCrety by this noCce. The CorporaCon assumes no obligaCon to update forward-‐looking informaCon should circumstances or management’s esCmates or opinions change. 20