2. 6/27/2013

2

AgendaAgendaAgendaAgenda

• History of Health Insurance and Costs

• Individual Mandated Health Insurance

• Tax Credits and Subsidy Programs

• The Exchange: Covered California

• Pay or Play for Large Employers

• ACA Compliance Checklist

• Strategies for Containing Costs

• Resources & Tools Available

3333

3. 6/27/2013

3

A Brief History of HealthA Brief History of HealthA Brief History of HealthA Brief History of Health InsuranceInsuranceInsuranceInsurance

• EmployerEmployerEmployerEmployer sponsored health insurance was born during World Warsponsored health insurance was born during World Warsponsored health insurance was born during World Warsponsored health insurance was born during World War IIIIIIII

• Medicare and Medicaid passed inMedicare and Medicaid passed inMedicare and Medicaid passed inMedicare and Medicaid passed in 1965196519651965

• ACA signed into law on March 23,ACA signed into law on March 23,ACA signed into law on March 23,ACA signed into law on March 23, 2010201020102010

• Supreme Court upheld the ACA on June 28,Supreme Court upheld the ACA on June 28,Supreme Court upheld the ACA on June 28,Supreme Court upheld the ACA on June 28, 2012201220122012

WorldWar IIWorldWar II 19651965 20102010 20122012

5555

Cumulative Premium Increases Compared to InflationCumulative Premium Increases Compared to InflationCumulative Premium Increases Compared to InflationCumulative Premium Increases Compared to Inflation

Family Coverage, California, 2002 toFamily Coverage, California, 2002 toFamily Coverage, California, 2002 toFamily Coverage, California, 2002 to 2012201220122012

• California Employer Hearth

Benefits Cost of Health

Insurance

• Since 2002, health insurance

premiums in California have

increased by 169%, more than

five times the 31.5% increase

in the state's overall inflation

rate.

6666

4. 6/27/2013

4

How Much Will Premiums Increase?How Much Will Premiums Increase?How Much Will Premiums Increase?How Much Will Premiums Increase?

• One state report shows that premiums will go

up 30% in 2014

• Age banded rates cannot vary more than 3:1

for adults for individual and small group

• Eliminates “Risk Adjustment Factor” for small

groups (2 50 ees)

• Essential Benefits

• New health insurance taxes

7777

Essential BenefitsEssential BenefitsEssential BenefitsEssential Benefits8888

6. 6/27/2013

6

Other Employer Cost ConsiderationsOther Employer Cost ConsiderationsOther Employer Cost ConsiderationsOther Employer Cost Considerations

• Must offer benefits to those working 30 hours or more per week

• Maximum waiting period 60 days in CA

• Adjusting contributions to avoid penalties

• Individual mandate may cause employees to join the plan

• Automatic enrollment for companies with 200 plus employees

• More administration for reporting and eligibility mandates

11111111

Individual MandateIndividual MandateIndividual MandateIndividual Mandate

• Jan. 1, 2014 all individuals are required to have health insurance

• Exceptions:

o Family income is below threshold of having to file a tax return

o Currently enrolled in Medicare or Medicaid

o Enrolled in a plan offered by an employer

12121212

7. 6/27/2013

7

Individual/Family Penalties for Not HavingIndividual/Family Penalties for Not HavingIndividual/Family Penalties for Not HavingIndividual/Family Penalties for Not Having

HealthHealthHealthHealth InsuranceInsuranceInsuranceInsurance13131313

YearYearYearYear Percentage ofPercentage ofPercentage ofPercentage of

IncomeIncomeIncomeIncome

Set Dollar Amount perSet Dollar Amount perSet Dollar Amount perSet Dollar Amount per

AdultAdultAdultAdult

Set Dollar Amount perSet Dollar Amount perSet Dollar Amount perSet Dollar Amount per

ChildChildChildChild

YearYearYearYear

2014201420142014 1%1%1%1% $95$95$95$95 $47.50$47.50$47.50$47.50 2014201420142014

2015201520152015 2%2%2%2% $325$325$325$325 $162.50$162.50$162.50$162.50 2015201520152015

2016201620162016 2.5%2.5%2.5%2.5% $695$695$695$695 $347.50$347.50$347.50$347.50 2016201620162016

Health Insurance Penalty PhaseHealth Insurance Penalty PhaseHealth Insurance Penalty PhaseHealth Insurance Penalty Phase In ScheduleIn ScheduleIn ScheduleIn Schedule

Pay the greater of the two amountsPay the greater of the two amountsPay the greater of the two amountsPay the greater of the two amounts

Covered CaliforniaCovered CaliforniaCovered CaliforniaCovered California

• Public, state run Exchange

• Guaranteed Issue for ALL Individuals/Families

• Provides online “apples to apples” comparison

• Begins open enrollment 10/1/13 for coverage effective 1/1/14

• Must have coverage before 3/1/14 or wait until next open enrollment

• 13 carriers state wide with 7 carriers in LA County

• Rates based on age and 19 territories

14141414

8. 6/27/2013

8

Levels of CoverageLevels of CoverageLevels of CoverageLevels of Coverage15151515

CategoryCategoryCategoryCategory

Percentage of expensesPercentage of expensesPercentage of expensesPercentage of expenses

paid by health planpaid by health planpaid by health planpaid by health plan

Percentage of expenses paidPercentage of expenses paidPercentage of expenses paidPercentage of expenses paid

by individualby individualby individualby individual

PlatinumPlatinumPlatinumPlatinum 90% 10%

GoldGoldGoldGold 80% 20%

SilverSilverSilverSilver 70% 30%

BronzeBronzeBronzeBronze 60% 40%

HigherHigherHigherHigher

percentage ofpercentage ofpercentage ofpercentage of

expensesexpensesexpensesexpenses paidpaidpaidpaid

bybybyby planplanplanplan

Lower monthlyLower monthlyLower monthlyLower monthly

premiumpremiumpremiumpremium

paymentpaymentpaymentpayment

Individual PlanIndividual PlanIndividual PlanIndividual Plan RatesRatesRatesRates16161616

PlanPlanPlanPlan BronzeBronzeBronzeBronze SilverSilverSilverSilver GoldGoldGoldGold PlatinumPlatinumPlatinumPlatinum

Health NetHealth NetHealth NetHealth Net

HMO

__ $242 $276 $311$311$311$311

AnthemAnthemAnthemAnthem

HMO

__ $259 $327 $374

Molina HealthcareMolina HealthcareMolina HealthcareMolina Healthcare

HMO

$204 $259 $285 $342

L.A. CareL.A. CareL.A. CareL.A. Care

HMO

$196$196$196$196 $265 $301 $332

Blue ShieldBlue ShieldBlue ShieldBlue Shield

PPO

$240 $287 $342 $392

AnthemAnthemAnthemAnthem

EPO

$225 $299 $363 $420

KaiserKaiserKaiserKaiser

HMO

$245 $325 $399 $429

Health NetHealth NetHealth NetHealth Net

PPO

$301 __ __ __

South Los Angeles CountySouth Los Angeles CountySouth Los Angeles CountySouth Los Angeles County –––– 40 Year Old40 Year Old40 Year Old40 Year Old

9. 6/27/2013

9

2014 Individual Plan Rates to Comparable Small Group2014 Individual Plan Rates to Comparable Small Group2014 Individual Plan Rates to Comparable Small Group2014 Individual Plan Rates to Comparable Small Group

RatesRatesRatesRates

17171717

AreaAreaAreaArea Avg. Cost of Silver PlanAvg. Cost of Silver PlanAvg. Cost of Silver PlanAvg. Cost of Silver Plan

Average cost of 2013 Comparable SmallAverage cost of 2013 Comparable SmallAverage cost of 2013 Comparable SmallAverage cost of 2013 Comparable Small

Group PlansGroup PlansGroup PlansGroup Plans

DifferenceDifferenceDifferenceDifference

Los Angeles (North)Los Angeles (North)Los Angeles (North)Los Angeles (North)

$242$242$242$242 $311$311$311$311 22%22%22%22%

Los Angeles (South)Los Angeles (South)Los Angeles (South)Los Angeles (South) $253$253$253$253 $362$362$362$362 29%29%29%29%

FINANCIALFINANCIALFINANCIALFINANCIAL ASSISTANCE PROGRAMSASSISTANCE PROGRAMSASSISTANCE PROGRAMSASSISTANCE PROGRAMS

AVAILABLE ONLY INAVAILABLE ONLY INAVAILABLE ONLY INAVAILABLE ONLY IN

COVEREDCOVEREDCOVEREDCOVERED CALIFORNIA EXCHANGECALIFORNIA EXCHANGECALIFORNIA EXCHANGECALIFORNIA EXCHANGE

18181818

10. 6/27/2013

10

Federal Poverty Level (FPLFederal Poverty Level (FPLFederal Poverty Level (FPLFederal Poverty Level (FPL))))19191919

Persons in HouseholdPersons in HouseholdPersons in HouseholdPersons in Household FPLFPLFPLFPL 138%138%138%138% FPLFPLFPLFPL 200% FPL200% FPL200% FPL200% FPL 250% FPL250% FPL250% FPL250% FPL 400% FPL400% FPL400% FPL400% FPL

1111 $11,490 $15,856 $22,980 $28,725 $45,960

2222 $15,510 $21,404 $31,020 $38,774 $62,400

3333 $19,530 $26,951 $39,060 $48,825 $78,120

4444 $23,550 $32,499 $47,100 $58,875 $94,200

Medi Cal

Cost Sharing

Subsidies

Premium Subsidies

MediMediMediMedi CalCalCalCal

• Free coverage for qualified individuals and children

• In 2014, Medi Cal eligibility increases from 100% FPL to 138% FPL for

adults and includes adults without children

• Eligibility for children is up to 250% FPL, however differs in other

states

• Estimates range from 1.7 million to more than 3 million Californians

will become eligible

20202020

11. 6/27/2013

11

1111) Cost) Cost) Cost) Cost SharingSharingSharingSharing SubsidiesSubsidiesSubsidiesSubsidies

• Eligibility: 138% to 250% FPL

• Sliding scale based on FPL

• 138% 150% FPL covers 94% of costs

• 150% 200% FPL covers 87% of costs

• 200 250% of FPL covers 73% of costs

21212121

WhatWhatWhatWhat is the benefit?is the benefit?is the benefit?is the benefit?

Allows the purchase of a Silver Plan (which covers the cost of medical

services at 70%) to a HIGHER percentage of coverage (which means

lower deductibles and copayments)

1111) Cost) Cost) Cost) Cost SharingSharingSharingSharing SubsidiesSubsidiesSubsidiesSubsidies22222222

Coverage CategoryCoverage CategoryCoverage CategoryCoverage Category

94% Silver94% Silver94% Silver94% Silver

Covers 94% avg.Covers 94% avg.Covers 94% avg.Covers 94% avg.

annual costannual costannual costannual cost

87% Silver87% Silver87% Silver87% Silver

Covers 87% avg. annual costCovers 87% avg. annual costCovers 87% avg. annual costCovers 87% avg. annual cost

73% Silver73% Silver73% Silver73% Silver

Covers 73% avg. annual costCovers 73% avg. annual costCovers 73% avg. annual costCovers 73% avg. annual cost

70% Silver70% Silver70% Silver70% Silver

Covers 70% avg.Covers 70% avg.Covers 70% avg.Covers 70% avg.

annual costannual costannual costannual cost

Income RangesIncome RangesIncome RangesIncome Ranges 138% 150% FPL 150% 200% FPL 200% 250% FPL 250% 400% FPL

Office VisitOffice VisitOffice VisitOffice Visit $3 $15 $40 $45

LabLabLabLab

DiagnosticsDiagnosticsDiagnosticsDiagnostics

$3

$5

$15

$20

$40

$50

$45

$65

Generic DrugsGeneric DrugsGeneric DrugsGeneric Drugs $3 $5 $20 $25

Annual Out of PocketAnnual Out of PocketAnnual Out of PocketAnnual Out of Pocket

Max. Individual/Max. Individual/Max. Individual/Max. Individual/

FamilyFamilyFamilyFamily

$2,250

$4,500

$2,500

$4,500

$5,200

$4,500

$6,350

$12,700

Examples based on FPLExamples based on FPLExamples based on FPLExamples based on FPL

12. 6/27/2013

12

2222) Premium) Premium) Premium) Premium SubsidiesSubsidiesSubsidiesSubsidies (aka Tax(aka Tax(aka Tax(aka Tax CreditsCreditsCreditsCredits))))

• Eligibility 138% to 400% FPL

• Amount of subsidy is based on a sliding scale

• Applied to the monthly premium

• Individual can earn up to $45,960

• Family of four can earn up to $94,200

• Available only in the Exchange

• Must be Silver plan or higher

23232323

2222) Premium) Premium) Premium) Premium Subsidy ExamplesSubsidy ExamplesSubsidy ExamplesSubsidy Examples24242424

PlanPlanPlanPlan 150 FPL150 FPL150 FPL150 FPL 200 FPL200 FPL200 FPL200 FPL 250 FPL250 FPL250 FPL250 FPL 400 FPL400 FPL400 FPL400 FPL

Health NetHealth NetHealth NetHealth Net

HMOHMOHMOHMO

$40$40$40$40 $103$103$103$103 $175$175$175$175 $242$242$242$242

$202$202$202$202 $138$138$138$138 $66$66$66$66 $0$0$0$0

AnthemAnthemAnthemAnthem

HMOHMOHMOHMO

$57$57$57$57 $121$121$121$121 $193$193$193$193 $259$259$259$259

$202$202$202$202 $138$138$138$138 $66$66$66$66 $0$0$0$0

Molina HealthcareMolina HealthcareMolina HealthcareMolina Healthcare

HMOHMOHMOHMO

$58$58$58$58 $121$121$121$121 $193$193$193$193 $259$259$259$259

$202$202$202$202 $138$138$138$138 $66$66$66$66 $0$0$0$0

L.A. CareL.A. CareL.A. CareL.A. Care

HMOHMOHMOHMO

$64$64$64$64 $127$127$127$127 $199$199$199$199 $265$265$265$265

$202$202$202$202 $138$138$138$138 $66$66$66$66 $0$0$0$0

Blue ShieldBlue ShieldBlue ShieldBlue Shield

PPOPPOPPOPPO

$86$86$86$86 $149$149$149$149 $221$221$221$221 $287$287$287$287

$202$202$202$202 $138$138$138$138 $66$66$66$66 $0$0$0$0

AnthemAnthemAnthemAnthem

EPOEPOEPOEPO

$97$97$97$97 $160$160$160$160 $232$232$232$232 $299$299$299$299

$202$202$202$202 $138$138$138$138 $66$66$66$66 $0$0$0$0

Kaiser PermanenteKaiser PermanenteKaiser PermanenteKaiser Permanente

HMOHMOHMOHMO

$123$123$123$123 $186$186$186$186 $258$258$258$258 $325$325$325$325

$202$202$202$202 $138$138$138$138 $66$66$66$66 $0$0$0$0

40 Year Old Single/ South LA County/Silver Plan40 Year Old Single/ South LA County/Silver Plan40 Year Old Single/ South LA County/Silver Plan40 Year Old Single/ South LA County/Silver Plan

Subsidies shown in

green premium

after subsidy and

monthly premium

after subsidy is

shown in black

13. 6/27/2013

13

CoveredCoveredCoveredCovered California :California :California :California : Cost Estimate Calculator25252525

Groups ofGroups ofGroups ofGroups of EmployeesEmployeesEmployeesEmployees26262626

MediMediMediMedi CalCalCalCal EligibleEligibleEligibleEligible

IndividualIndividualIndividualIndividual with income lower

than $15,856

Or

Family of 2Family of 2Family of 2Family of 2 with income lower

than $21,404

Or

Family of 3Family of 3Family of 3Family of 3 with income lower

than $26,951

Or

Family of 4Family of 4Family of 4Family of 4 with income lower

than $32,499

Group 1Group 1Group 1Group 1

Less than 138% FPLLess than 138% FPLLess than 138% FPLLess than 138% FPL

Group 2Group 2Group 2Group 2

138 to 250% FPL138 to 250% FPL138 to 250% FPL138 to 250% FPL

CostCostCostCost Sharing & PremiumSharing & PremiumSharing & PremiumSharing & Premium

Subsidy EligibleSubsidy EligibleSubsidy EligibleSubsidy Eligible

IndividualIndividualIndividualIndividual with income

between $15,856 $28,725

Or

Family of 2Family of 2Family of 2Family of 2 with income

between $21,404 $38,774

Or

Family of 3Family of 3Family of 3Family of 3 with income

between $26,951 $48,825

Or

Family of 4Family of 4Family of 4Family of 4 with income

between $32,499 $58,876

Must purchase on

the Exchange to

receive subsidies

14. 6/27/2013

14

Groups ofGroups ofGroups ofGroups of EmployeesEmployeesEmployeesEmployees27272727

Premium SubsidyPremium SubsidyPremium SubsidyPremium Subsidy EligibleEligibleEligibleEligible

Individual with income of

$22,980 $45,960

Or

Family of 2 with income of

$31,020 $62,400

Or

Family of 3 with income of

$39,060 $78,120

Or

Family of 4 with income of

$47,100 $94,200

Group 3Group 3Group 3Group 3

138% to 400% FPL

Group 4Group 4Group 4Group 4

Higher than 400% FPL

NoNoNoNo SubsidiesSubsidiesSubsidiesSubsidies

Individual with income

higher than $45,960

Or

Family of 2 with income

higher than $62,400

Or

Family of 3 with income

higher than $78,120

Or

Family of 4 with income

higher than $94,200

Must purchase on

the Exchange to

receive subsidies

Groups ofGroups ofGroups ofGroups of EmployeesEmployeesEmployeesEmployees28282828

GroupGroupGroupGroup 5555

Waives Coverage and Opts to Pay Penalty

YearYearYearYear % of Income% of Income% of Income% of Income AdultAdultAdultAdult ChildChildChildChild

2014 1% $95 $47.50

2015 2% $325 $162.50

2016 2.5% $695 $347.50

15. 6/27/2013

15

Group Health Benefit ChangesGroup Health Benefit ChangesGroup Health Benefit ChangesGroup Health Benefit Changes

Effective Already:Effective Already:Effective Already:Effective Already:

1. Dependents covered until age 26

2. No cost for preventative care

3. No cost for contraceptives

4. No lifetime or annual benefit limits

Effective Jan. 1, 2014:Effective Jan. 1, 2014:Effective Jan. 1, 2014:Effective Jan. 1, 2014:

1. No pre existing exclusions

2. Maximum OOP $6,350 / $12,700

29292929

Small EmployersSmall EmployersSmall EmployersSmall Employers

• No mandate to provide group health insurance

• Defined as 1 – 50 full time employees

• Small employer expands to 100 employees in 2017 but penalty

still applies over 50 FTEs

• Community rating

• Max. plan deductible of $2,000/$4,000

• In the Exchange: min. participation and contribution

requirements may no longer apply (must enroll during special

open enrollment period Nov. 15 – December 15)

30303030

16. 6/27/2013

16

Small Business Health Options Program (SHOP)Small Business Health Options Program (SHOP)Small Business Health Options Program (SHOP)Small Business Health Options Program (SHOP)

• Public Exchange run by Covered California

• Side by side comparison of plans

• Choice of health plans, dental and carriers

• Can provide defined contribution amount towards Bronze,

Silver, Gold or Platinum plans

• One consolidated bill for all plans

• Tax credits are available for 2 years from 2014 to 2020

• On a sliding scale up to a maximum of 50%:

o 25 or fewer FTEs with average payroll less than $50,000 per year and contribute

50% are eligible for minimal tax credit

o 10 or fewer FTEs with average payroll less than $25,000 are eligible for

maximum tax credit

31313131

Large EmployersLarge EmployersLarge EmployersLarge Employers

• Pay or Play!

• 50 or more full time equivalent (FTE) employees in the prior

year.

• Employees working 30 hours per week are deemed full

time.

• Part time employees: add up hours worked for the month and

divide by 120

• 10 employees @ 15 hours per week = 600 hours divided by

120 = 5 FTEs

32323232

17. 6/27/2013

17

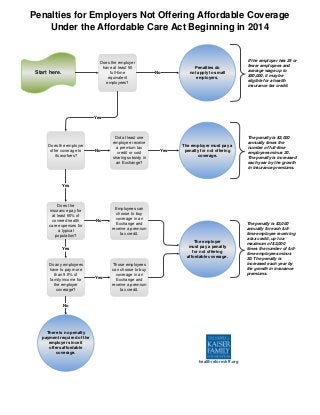

Large Employer PenaltiesLarge Employer PenaltiesLarge Employer PenaltiesLarge Employer Penalties

• No health insurance = $2,000 per year/per employeeNo health insurance = $2,000 per year/per employeeNo health insurance = $2,000 per year/per employeeNo health insurance = $2,000 per year/per employee

o The first 30 employees are not counted:

o Example: 60 employees – 30 = 30 x $2,000 = $60,000 annual penalty

• Unaffordable Coverage = $3,000 per year/per employee that purchases healthUnaffordable Coverage = $3,000 per year/per employee that purchases healthUnaffordable Coverage = $3,000 per year/per employee that purchases healthUnaffordable Coverage = $3,000 per year/per employee that purchases health

insurance through the Exchange and receives a subsidy.insurance through the Exchange and receives a subsidy.insurance through the Exchange and receives a subsidy.insurance through the Exchange and receives a subsidy.

33333333

Minimum Value andMinimum Value andMinimum Value andMinimum Value and AffordabilityAffordabilityAffordabilityAffordability TestTestTestTest

1)1)1)1) Minimum ValueMinimum ValueMinimum ValueMinimum Value TestTestTestTest: health plan must pay a minimum of 60% of

expenses

2)2)2)2) Affordability TestAffordability TestAffordability TestAffordability Test: employees’ contribution cannot exceed 9.5% of

their W 2 wages

• Penalty does not apply:

• If employee has coverage through spouse

• Employee buys health insurance through the Exchange but does not qualify for

a subsidy

• Employee is enrolled in Medicaid/Medicare

34343434

18. 6/27/2013

18

Penalties for Employers Not Offering Affordable CoveragePenalties for Employers Not Offering Affordable CoveragePenalties for Employers Not Offering Affordable CoveragePenalties for Employers Not Offering Affordable Coverage

Under the Affordable Care Act Beginning in 2014Under the Affordable Care Act Beginning in 2014Under the Affordable Care Act Beginning in 2014Under the Affordable Care Act Beginning in 2014

35353535

Penalties for Employers Not Offering Affordable CoveragePenalties for Employers Not Offering Affordable CoveragePenalties for Employers Not Offering Affordable CoveragePenalties for Employers Not Offering Affordable Coverage

Under the Affordable Care Act Beginning in 2014Under the Affordable Care Act Beginning in 2014Under the Affordable Care Act Beginning in 2014Under the Affordable Care Act Beginning in 2014

36363636

19. 6/27/2013

19

Employer Survey on Health ReformEmployer Survey on Health ReformEmployer Survey on Health ReformEmployer Survey on Health Reform

McKinsey & Company, a leading global management consulting firm,

conducted a survey of 1,329 employers to measure their attitudes about

healthcare reform:

• 30% of employers will “definitely or probably” stop providing employer sponsored

insurance in the years following 2014

• Among employers with a “high awareness of reform, this proportion increases to

more than 50%”

• 45 to 50% of employers will “pursue some alternative to traditional” group health

coverage

37373737

Research and Consumer SurveysResearch and Consumer SurveysResearch and Consumer SurveysResearch and Consumer Surveys

• At least 30% of employers would gain economically from dropping

coverage even if they make employees 100% whole

• Contrary to what other employers assume, more than 85% of

employees would remain at their jobs even if their employer stopped

offering employer sponsored insurance

“Most employers, however will find value“Most employers, however will find value“Most employers, however will find value“Most employers, however will find value creating options between thecreating options between thecreating options between thecreating options between the

extremes of completely dropping coverage and making no changes toextremes of completely dropping coverage and making no changes toextremes of completely dropping coverage and making no changes toextremes of completely dropping coverage and making no changes to

the current offering”the current offering”the current offering”the current offering”

Source: McKinsey & Company

38383838

20. 6/27/2013

20

Key Concepts and Plan Design StrategiesKey Concepts and Plan Design StrategiesKey Concepts and Plan Design StrategiesKey Concepts and Plan Design Strategies

39393939

Defined ContributionDefined ContributionDefined ContributionDefined Contribution

Employer provides fixed dollarEmployer provides fixed dollarEmployer provides fixed dollarEmployer provides fixed dollar amountamountamountamount and theand theand theand the

employee canemployee canemployee canemployee can choosechoosechoosechoose how to allocate it amonghow to allocate it amonghow to allocate it amonghow to allocate it among aaaa

variety of benefit options.variety of benefit options.variety of benefit options.variety of benefit options.

40404040

21. 6/27/2013

21

Defined Contribution &Defined Contribution &Defined Contribution &Defined Contribution & PrivatePrivatePrivatePrivate ExchangesExchangesExchangesExchanges

A benefits exchange is an online store where employees purchase

benefit to suit their individual and family needs.

41414141

What is a private exchange?What is a private exchange?What is a private exchange?What is a private exchange?

A benefits model that:

• Allows employees to select health

plans and other benefits from a

menu of products and services

• Employees shop for the products

that best fit them personally using

defined contribution dollars from

their employer, and their own money

if they choose

Health Reimbursement Arrangements (HRAs)Health Reimbursement Arrangements (HRAs)Health Reimbursement Arrangements (HRAs)Health Reimbursement Arrangements (HRAs)42424242

What is an HRA?What is an HRA?What is an HRA?What is an HRA?

• Created under Section 105 of the IRS Code and further

clarified by the IRS in 2002

• HRAs are an employer funded plan to reimburse

employees for medical expenses including individual

and family premiums

• HRAs are notional arrangements; no funds are

expensed until reimbursements are paid

• HRAs are tax deductible for the employer and tax free

to the employee

• HRAs can be restricted for the purchase of individual

and family health and other specified benefit plans

and medical expenses

22. 6/27/2013

22

Healthcare Reform &Healthcare Reform &Healthcare Reform &Healthcare Reform & Defined Contribution HRADefined Contribution HRADefined Contribution HRADefined Contribution HRA43434343

• Medical Underwriting

• No Federal Subsidies for

Individual Policies

• No Standardized System

for Comparing Plans

• Employer Driven

• No Medical Underwriting

• Federal Subsidies for

Individual Policies

• Easy comparison of plans

• Individual/Family DrivenVs.Vs.Vs.Vs.

AfterAfterAfterAfter 2014201420142014BeforeBeforeBeforeBefore 2014201420142014

Advantages to HRAsAdvantages to HRAsAdvantages to HRAsAdvantages to HRAs & Defined& Defined& Defined& Defined ContributionContributionContributionContribution44444444

• Control & predict costs

• No min. contribution or

participation

• Establish own rules

• No admin. hassle

• Allows you to focus on your

business

• Portable & permanent

• Total choice & flexibility

• Up to 29% less cost

• Allows for premium &

cost sharing subsidies

• Better educated consumers

EmployeeEmployeeEmployeeEmployeeEmployerEmployerEmployerEmployer

23. 6/27/2013

23

Pay or Play Spectrum of StrategiesPay or Play Spectrum of StrategiesPay or Play Spectrum of StrategiesPay or Play Spectrum of Strategies45454545

Continue as plan

sponsor for all

employees

(plan provides

minimum value is

affordable)

Restructure

contributions

to qualify

lower paid

employees and

their dependents

for federal

subsidies in

the Exchange

Limit eligibility to plan

and direct ineligibles

to the Exchange

Exclude classes

of full time

employees

Reduce weekly hours

to 29 or less

Discontinue plan

and provide tax free

defined contribution

for employees to

purchase individual

plans in the

Exchange

Discontinue plan

with no employee

contributions

Play and RedirectPlay and RedirectPlay and RedirectPlay and Redirect

• Calculate potential penalties

• Establish defined contribution plan and HRA

• Restructure contributions so that employee contributions are

greater than 9.5% of income for employees earning less than

400% FPL

• Redirect eligible employees to receive cost sharing and premium

subsidies through the Exchange

• Allow non eligible employees to continue group health insurance

or receive tax free defined contribution allowance to purchase

policies through the Exchange

• Provide eligible employees with a tax free defined contribution

HRA allowance to purchase policies through the Exchange

46464646

24. 6/27/2013

24

PayPayPayPay and Redeploy Strategiesand Redeploy Strategiesand Redeploy Strategiesand Redeploy Strategies

• Employer discontinues group coverage and completely subsidizes employee participation

in the Exchange (make employees whole)

• Employer discontinues group coverage and keep employee contributions in the exchange at

the same level of what continued group coverage would have cost (employer cost neutral

Defined Contribution HRA)

• Employer discontinues group coverage and provides contributions for individual exchange

at a level to achieve a savings target i.e. 20% (employer cost savings defined contribution

HRA)

• Employer discontinues coverage and eliminates entire cost of coverage by not subsidizing

any employee exchange participation and pays penalties (pay and exit )

By implementing an HRA, employers avoid using pay increases and paying increased payroll

taxes to compensate employees. Employees still maintain tax free benefits and avoid paying

increased income taxes.

47474747

ACAACAACAACA ComplianceComplianceComplianceCompliance ChecklistChecklistChecklistChecklist

2013:2013:2013:2013:

Summary of Benefits Coverage (SBC)

Include in Open Enrollment Packets

Include in New Hire Packets

W 2 Reporting Requirements (over 250 ees)

Employee Notice of Exchange Distributed by 10/1

Include in New Hire Packets

2014:2014:2014:2014:

Maximum Waiting Period of 60 days in CA

Automatic Enrollment (200 or more ees)

Pending:Pending:Pending:Pending:

Eligibility and Benefits Non Discrimination Testing

48484848

25. 6/27/2013

25

What Are You Doing with Your Plan?What Are You Doing with Your Plan?What Are You Doing with Your Plan?What Are You Doing with Your Plan?

• 90% of employers have moved beyond a “wait and see”

approach

• Only 10% of companies are still in the “wait and see” mode

• More than 50% of companies are developing tactics to deal

with the implications of health reform

• About one third of companies have modeled the financial

impact of reform on their organization

49494949

Which category do you fall into today?Which category do you fall into today?Which category do you fall into today?Which category do you fall into today?

Source: International Foundation of Employee Benefit Plans Survey Results: “2013 Employer

Sponsored Health Care: ACA’s Impact”

Action StepsAction StepsAction StepsAction Steps

Talk to other companies in your industry. What are they doing?

Take advantage of our free whitepapers, reports, tools and resources

Register for our next monthly webinar: “Beyond the Basics: Advanced

Healthcare Reform Strategies” on Thursday, July 18

Evaluate your broker: How well informed are you on the ACA? What

strategies have been discussed and developed specifically for your company?

Take advantage of your complimentary one hour, no obligation consultation

and we’ll develop specific strategies for your company (or to discuss any

topic you desire)

Expect my call tomorrow to answer any questions you might have

50505050

26. 6/27/2013

26

Employer Tools and ResourcesEmployer Tools and ResourcesEmployer Tools and ResourcesEmployer Tools and Resources

Free White Papers and EBooksFree White Papers and EBooksFree White Papers and EBooksFree White Papers and EBooks

51515151

End.End.End.End.

Thank you !