Global Central Banks Monetary Policy Review highlights 2013

•Télécharger en tant que DOCX, PDF•

1 j'aime•956 vues

Global Central Banks Monetary Policy Review highlights 2013 Country wise Month wise

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Global Central Banks Monetary Policy Review highlights 2013

Similaire à Global Central Banks Monetary Policy Review highlights 2013 (20)

Plus de Jhunjhunwalas

Plus de Jhunjhunwalas (20)

Dernier

Dernier (20)

Global Central Banks Monetary Policy Review highlights 2013

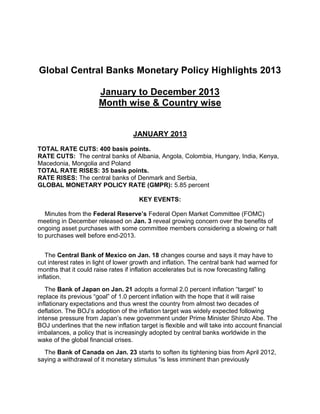

- 1. Global Central Banks Monetary Policy Highlights 2013 January to December 2013 Month wise & Country wise JANUARY 2013 TOTAL RATE CUTS: 400 basis points. RATE CUTS: The central banks of Albania, Angola, Colombia, Hungary, India, Kenya, Macedonia, Mongolia and Poland TOTAL RATE RISES: 35 basis points. RATE RISES: The central banks of Denmark and Serbia, GLOBAL MONETARY POLICY RATE (GMPR): 5.85 percent KEY EVENTS: Minutes from the Federal Reserve’s Federal Open Market Committee (FOMC) meeting in December released on Jan. 3 reveal growing concern over the benefits of ongoing asset purchases with some committee members considering a slowing or halt to purchases well before end-2013. The Central Bank of Mexico on Jan. 18 changes course and says it may have to cut interest rates in light of lower growth and inflation. The central bank had warned for months that it could raise rates if inflation accelerates but is now forecasting falling inflation. The Bank of Japan on Jan. 21 adopts a formal 2.0 percent inflation “target” to replace its previous “goal” of 1.0 percent inflation with the hope that it will raise inflationary expectations and thus wrest the country from almost two decades of deflation. The BOJ’s adoption of the inflation target was widely expected following intense pressure from Japan’s new government under Prime Minister Shinzo Abe. The BOJ underlines that the new inflation target is flexible and will take into account financial imbalances, a policy that is increasingly adopted by central banks worldwide in the wake of the global financial crises. The Bank of Canada on Jan. 23 starts to soften its tightening bias from April 2012, saying a withdrawal of it monetary stimulus “is less imminent than previously

- 2. anticipated” due to a weaker-than-expected global economic outlook, a more muted outlook for inflation and slower growth in household credit. The National Bank of Denmark on Jan. 24 raises its benchmark lending rate by 10 basis points to 0.30 percent and the rate on certificates of deposit to minus 0.10 percent, a sign of the waning appeal of Denmark as a safe haven for jittery euro zone investors. Denmark entered uncharted monetary policy territory in July 2012 when it cut the rate on CDs to negative to weaken the demand for the krone currency after inflows pushed the currency above the central bank’s peg to the euro. Bank of Israel Governor Stanley Fischer announces on Jan. 29 that he will step down on June 30, two years earlier than expected. Fischer, who was appointed in 2005, was widely credited with steering Israel’s economy through the global financial crises relatively unscathed. Previously, Fischer was chief economist at the World Bank, International Monetary Fund first deputy managing director. At the Massachusetts Institute of Technology, Fischer’s students included Federal Reserve Chairman Ben Bernanke and European Central Bank President Mario Draghi. FEBRUARY 2013 TOTAL RATE CUTS: 200 basis points RATE CUTS: The central banks of Azerbaijan, Bulgaria, Colombia, Georgia, Hungary, India and Poland. TOTAL RATE RISES: 25 basis points RATE CUTS: The central bank of Serbia. GLOBAL MONETARY POLICY RATE (GMPR): 5.83 percent KEY EVENTS: Minutes from the Federal Reserve’s Federal Open Market Committee (FOMC) meeting in January released on Feb. 20 reveal intense debate over asset purchases, with some members suggesting that purchases should be varied in response to changes in the economic outlook and others proposing that purchases may be tapered before the outlook for the labor market improves. Another issue is how the Fed should communicate a commitment to a highly accommodative policy, for example by holding securities for a longer period than envisoned in the Fed’s exit principles that were outlined in June 2011 FOMC. The Bank of England (BOE) on Feb. 7 publishes an unusually lengthy statement, saying it would look through the ”temporary, albeit protracted, period of above-target inflation” and maintain, or even provide additional monetary stimulus, if warranted by the outlook. The statement illustrates the widespread commitment by central banks to “flexible inflation targeting.”

- 3. MARCH 2013 TOTAL RATE CUTS: 500 basis points RATE CUTS: The central banks of Belarus, Colombia, Georgia, Hungary, India, Mexico, Poland, Vietnam and West African States. TOTAL RATE RISES: 75 basis points RATE RISES: The central banks of Egypt and Tunisia, GLOBAL MONETARY POLICY RATE (GMPR): 5.78 percent KEY EVENTS: Haruhiko Kuroda, nominated as the next Bank of Japan governor, says on March 3 that it would be “natural for the BOJ to buy longer-dated government bonds in huge amounts.” The Central Bank of Brazil on March 7 omits its guidance from November 2012 that stable monetary conditions for a prolonged period was appropriate, foreshadowing future rate hikes to combat rising inflation. The Bank of Mexico on March 8 cuts its benchmark rate by a larger-than-expected 50 basis points, its first rate cut since July 2009, due to weak economic global growth. The bank says it is not embarking on new cycle of easing. Russian President Vladimir Putin on March 13 picks Elvira Nabiullina, former economy minister and aide to Putin, as new chairman of the Bank of Russia. She becomes the first woman to head at Group of Eight (G8) central bank. Norges Bank, Norway’s central bank, on March 14 further delays any rate rise until the first half of 2014 after it pushed back a planned rate rise by end-2012 to 2013 in October 2012. The central bank decides to impose an extra cushion of capital - known as a countercyclical capital buffer - that banks should build up during good economic times so they can draw on that reserve if the event of losses during an economic downturn. The South African Reserve Bank on March 20 maintains interest rates but points to European policy makers decision to impose an unprecedented tax on bank deposits in Cyprus as having the “potential to reignite the banking and sovereign debt crises and undermine growth prospects further.” The levy on Cyprus bank deposits was part of a rescue package worth 10 billion euros and revived speculation of a breakup of the euro area. The Bank of England on March 20 is given a new remit from the UK government that formalizes the flexible inflation target and includes the ability to “deploy explicit forward guidance.” The 2 percent inflation target was also restated.

- 4. The Central Bank of Egypt on March 21 becomes the first emerging market central bank to raise rates in 2013, increasing the overnight deposit rate by 50 basis points and saying inflationary expectations are more harmful to an economy than the weak outlook for economic growth. APRIL 2013 TOTAL RATE CUTS: 776 basis points RATE CUTS: The central banks of Belarus, Botswana, Hungary, Moldova, Mongolia, Sierra Leone and Turkey. TOTAL RATE RISES: 25 basis points RATE RISES: The central bank of Brazil. GLOBAL MONETARY POLICY RATE (GMPR): 5.75 percent KEY EVENTS: The Bank of Japan (BOJ) on April 4 launches a "new phase of monetary easing" aimed at reaching the 2.0 percent inflation target "at the earliest possible time, with a time horizon of about two years.” The objective is to rid the country of 15 years of deflation. Only two weeks after taking over as governor, Haruhiko Kuroda replaces the BOJ’s asset purchase program with "quantitative and qualitative monetary easing," (known as QQE) under which the BOJ will no longer target the overnight call rate, which has been at effectively zero since December 2008, but the monetary base, or bank reserves at the central bank plus cash in circulation. The BOJ aims to double the monetary base by 60-70 trillion yen annually by end-2014 and push down interest rates across all maturities by buying government bonds at an annual pace of about 50 trillion yen. The BOJ will no longer focus its purchases on shorter maturities but include 40year bonds so the average remaining maturity of its new bond purchases will extend to about seven years from less than three years. The BOJ will also boost its annual purchases of Exchange Traded Funds (ETFs) and real estate investment trusts, so-called J-REITs, by an annual 1.0 trillion and 30 billion yen, respectively. It will also purchase commercial paper and corporate bonds until their outstanding amounts reach 22 trillion and 3.2 trillion yen, respectively. The BOJ is one of the pioneers in using its balance sheet to stimulate economic activity and launched its first attempt at quantitative easing in March 2001 by raising the target for banks’ current account balances (CAB) at the BOJ in excess of their required reserve levels. The BOJ raised the target for CAB nine more times before exiting quantitative easing in March 2006 amid signs the economy was emerging from deflation. In October 2010, following the Global Financial Crises, the BOJ introduced Comprehensive Monetary Easing (CME), mainly purchasing government securities but also private assets. CME, which aimed at purchasing assets worth 101 trillion yen by 2014, was absorbed into QQE.

- 5. The Central Bank of Barbados (CBB) on April 5 starts guiding interest rates by intervening directly in the market for Treasury bills instead of using the minimum deposit rate. The rationale behind the new policy was unveiled in a CBB working paper from March that set out the limitations of using interest rates to control inflation in a country like Barbados where 80 percent of inflation is imported. In a small, open economy like Barbados, the policy of targeting a deposit rate to guide the local availability of credit is weak because banks, firms and households go abroad for funds. Banks will be free to set all rates except for a minimum savings rate, which is set by the CBB, to insulate small savers and non-profit organizations against inflation. The CBB also realizes that interest rates have to be kept in line with international rates to avoid “destabilizing inflows and outflows of capital." The Central Bank of Brazil on April 17 kicks off its widely-expected tightening campaign, raising rates by 25 basis points after inflation exceeds the central bank’s upper tolerance level for the first time since November 2011. The benchmark Selic rate had been frozen at 7.25 percent since November 2012 after 10 consecutive rate reductions from August 2011. Sweden’s Riksbank on April 17 keeps rates steady, but pushes back a planned hike in interest rates by around a year to the second half of 2014 as it will take longer time for inflation to start to rise toward the bank’s target. The Riksbank says inflation is low due to weak demand, the strong value of the Swedish krone and a difficulty of companies in passing on higher costs to consumers. After seven rate cuts totaling 200 basis points, the Central Bank of Colombia on April 26holds rates steady, saying its past easing and proposed fiscal measures should help strengthen economic growth push up inflation toward its target. The Bank of Thailand on April 30 voices its concern over the rapid rise in the value of its baht currency and pledges to take action when needed. There are fears the baht will continue to rise in response to the BOJ’s aggressive easing, with money seeking higher yield in other countries, such as Thailand and South Korea. MAY 2013 TOTAL RATE CUTS: 885 basis points RATE CUTS: The central banks of Australia, Belarus, Denmark, Dominican Republic, Eurosystem, Georgia, Hungary, India, Israel, Kenya, Poland, Serbia, South Korea, Sri Lanka, Thailand, Turkey and Vietnam TOTAL RATE RISES: 350 basis points RATE RISES: The central banks of Brazil, Bulgaria, Gambia and Ghana, GLOBAL MONETARY POLICY RATE (GMPR): 5.72 percent

- 6. KEY EVENTS: The European Central Bank (ECB) on May 2 cuts benchmark refinancing rate by 25 basis points and says it will provide banks with all they money they need for as long as necessary. ECB President Mario Draghi pledges that the “monetary policy stance will remain accommodative for as long as needed.” The Reserve Bank of Australia on May 6 resumes its easing cycle by cutting its benchmark rate by 25 basis points, saying lower-than-expected inflation had given it scope to encourage growth. The RBA, which is striving to counter the dampening effects of lower mining investments, embarked on an easing cycle in October 2011 and last cut rates in November 2012 before pausing to let the impact of the rate cuts take effect. The RBA says the A$ exchange rate is “at a historically high level” and the Aussie dollar falls sharply following the rate cut. The Bank of Korea on May 9 cuts its base rate by 25 basis, citing considerable downside risks to global growth and its latest forecast that “the domestic economy will show a negative output gap for a considerable time, due mostly to the slow recovery of the global economy, to the influence of the Japanese yen weakening, and to the geopolitical risk in Korea." The Bank of Israel on May 13 cuts its policy rate by 25 basis points after an unscheduled meeting of its monetary policy committee and says it will buy some $2.1 billion of foreign exchange in 2013 to hold back the appreciating shekel. The shekel has risen due to external demand for its natural gas, low interest rates in major economies and an expected slowing of global growth. The National Bank of Serbia on May 14 cuts its policy rate by 50 basis points due to “significantly lower inflationary pressure.” The central bank raised rates eight consecutive times from June 2012 to February 2013 in response to accelerating inflation but then paused in March and April before starting its current easing cycle. Federal Reserve Chairman Ben Bernanke on May 22 tells a U.S. Congressional committee that the Fed could “in the next few meetings take a step down in our pace of purchases,” of $85 billion of Treasury bonds and housing-related securities. Bernanke says monetary policy has helped offset “incipient deflationary pressures and kept inflation from falling even further below the 2 percent longer-run objective” and repeats that the Fed is prepared to either increase or decrease the pace of its asset purchases depending on economic conditions. The Bank of Israel on May 27 cuts its policy rate for the second time in May to “to "narrow the gaps between the Bank of Israel's interest rate and the rates in major economies worldwide, in order to weaken the forces for appreciation of the shekel." The Bank of Thailand (BOT) on May 29 cuts rate by 25 basis points, citing growing downside economic risks and says it is “ready to take appropriate action as warranted”

- 7. in light of the risks to financial stability from capital flows. Referring to exchange rate volatility, the BOT says Thai exports could be affected by slower growth in China and Asian economies while Japan’s economy is starting to benefit from stimulus measures. The Bank of Japan’s launch of monetary easing in April has led to a sharp fall in the yen and fears of capital inflows to higher-yielding currencies, such as the Thai baht. The BOT and Thai finance ministry are considering measures to weaken the baht. JUNE 2013 TOTAL RATE CUTS: 926 basis points RATE CUTS: The central banks of Belarus, Botswana, Bulgaria, Georgia, Hungary, Mauritius, Mongolia, Mozambique, Pakistan, Poland, Rwanda, Serbia, Sierra Leone, Uganda and Ukraine. TOTAL RATE RISES: 450 basis points RATE RISES: The central banks of Gambia, Indonesia and Zambia. GLOBAL MONETARY POLICY RATE (GMPR): 5.63 percent KEY EVENTS: Bank Indonesia on June 13 raises benchmark rate by 25 basis points in what it described as a pre-emptive move to "rising inflation expectations and to maintain macroeconomic stability and financial system stability amid increasing uncertainty in global financial markets." The rate hike, under the central bank’s new governor Agus Martowardojo, follows a 25 basis point increase in the overnight deposit rate on June 11, underlining authorities' determination to defend and stabilize the rupiah. The rupiah, along with other emerging market currencies, have come under pressure along as investors start to shift funds toward advanced economies with improving growth prospects and an expected reduction in asset purchases by the U.S. Federal Reserve. Federal Reserve Chairman Ben Bernanke on June 19 firms up his comments from May 22 and says after a meeting of the Federal Open Market Committee (FOMC) that asset purchases would be slowly reduced later this year and then wound up by mid2014, assuming the economy continues to expand. "The Committee currently anticipates that it would be appropriate to moderate the monthly pace of purchases later this year; and if the subsequent data remain broadly aligned with our current expectations for the economy, we would continue to reduce the pace of purchases in measured steps through the first half of next year, ending purchases around midyear," Bernanke says. He adds, however, that the Fed is not fixed on any dates and if "conditions improve faster than expected, the pace of asset purchases could be reduced more quickly." Conversely, if the economic outlook deteriorates, the reductions in purchases could be delayed. Norges Bank on June 20 drops its tightening bias from March and says the policy rate will remain at the current level, or somewhat lower, in the year ahead" as inflation

- 8. will take longer to rise and economic activity is lower than expected. At its previous meeting in March, the Norwegian central bank said it expected to maintain rates until the spring of 2014 and then raise the rate. It omits any mention of rate rises. Jaime Caruana, general manager of the Bank for International Settlements (BIS) on June 23 says major central banks will decide how and when to exit from extraordinary easy monetary policy with much less certainty that they probably will like but they cannot afford to wait for irrefutable evidence. Caruana tells the annual BIS meeting that nobody really knows “how central banks will exit, or what they will exit into” and major central banks will need to draw on all their communication skills to make the exit from such policy as smooth as possible. "And they will have to take decisions with much less certainty than they would probably like - waiting for irrefutable evidence may complicate exit and prove costly," Caruana says, adding:. "The bigger the scale and scope of their interventions, the more difficult it will be to reduce them." The Bank for International Settlements (BIS) warns in its annual report on June 23 that a sharp rise in interest rates from major central banks’ exit from extraordinary accommodative policy could raise the risk of stress in the financial system as banks hold large portfolios of long-dated fixed income assets that will fall in value. While central banks have more tools at their disposal, are more transparent and experienced in managing expectations that in 1994 - when a tightening of U.S. monetary policy lead to turbulence in global bond markets - BIS said the situation now is much more complex with the exit requiring “a sequencing of both interest rate increases and the unwinding of balance sheet policies. Central banks’ will be exiting at a time of very high levels of debt with much issued at record low levels, raising the risk of public and government anger over higher interest payments and losses. A rise in U.S. Treasury yields by 300 basis points, for example, would result in losses to holders of those securities that exceed $1 trillion, or almost 8 percent of U.S. GDP. While yields are not likely to jump that much overnight, BIS noted that yields in 1994 rose some 200 basis points during one year in a number of countries, illustrating that “a big upward move can happen relatively fast.” The Bank for International Settlements (BIS) says in its annual report on June 23that central banks should stop influencing overall financial conditions and return to their traditional role of controlling short-term rates now that the global financial crises is receding. In response to extreme pressure on financial markets during the height of the crises, central banks in advanced economies expanded their operations and influence on markets; accepting a wider range of collateral, engaging in large-scale asset purchases and creating special lending schemes. But the BIS says such tools were most suitable for exceptional circumstances and central banks should now return to influencing short-term policy rates only as a way to affect monetary conditions. Since late 2007, central banks’ total assets have roughly doubled to over $20.5 trillion, up from $18 trillion last year, accounting for just over 30 percent of global Gross Domestic Product (GDP), double the ratio of a decade ago.

- 9. JULY 2013 TOTAL RATE CUTS: 190 basis points RATE CUTS: The central banks of Albania, Hungary, Latvia, Poland, Romania and Tajikistan, TOTAL RATE RISES: 126 basis points RATE RISES: The central banks of Brazil, Bulgaria, Indonesia and Zambia. GLOBAL MONETARY POLICY RATE (GMPR): 5.62 percent KEY EVENTS: The National Bank of Poland (NBP) on July 3 says its latest rate cut ends its cycle of easing. The NBP started cutting rates in November 2012 - a move that was criticized as too late to cushion the economy from the euro area's recession – but then froze rates in April before cutting again in May and June. The Bank of England (BOE) on July 4, in a rare statement accompanying its rate decision, says the rise in market interest rates will have a negative impact on its outlook for economic growth and inflation, and it does consider the implied rise in its policy rate to be warranted by economic developments. The BOE's Monetary Policy Committee, chaired for the first time by Governor Mark Carney after he arrived from the Bank of Canada, says recent data have been consistent with the BOE’s outlook and inflation is expected to slowly fall back towards the bank's 2.0 percent target though it may rise further in the near term. "The significant upward movement in market interest rates would, however, weigh on that outlook; in the Committee's view, the implied rise in the expected future path of Bank Rate was not warranted by the recent developments in the domestic economy," the BOE says. Yields on government bond yields in the U.K. and U.S. have risen in recent weeks following better economic data and the Federal Reserve’s statement on June 19 that the U.S. central bank is considering slowing down its asset purchases later this year. The European Central Bank (ECB) on July 4 broke with tradition and adopted a form of forward guidance to counter a rise in global interest rates, saying it will maintain an easy monetary policy stance for "as long as necessary" and may even cut rates further. The ECB said the risks surrounding its economic outlook remain on the downside and the recent rise in global bond yields "may have the potential to negatively affect economic conditions." "The Governing Council expects the key ECB interest rates to remain at present or lower levels for an extended period of time," ECB President Mario Draghi says. Long-term interest rates rose worldwide following the Federal Reserve's decision on June 19 to start winding up its asset purchase program later this year as long as the economy continues to recover. Bank Indonesia on July 11 raises benchmark BI rate by higher-than-expected 50 basis points to "ensure that inflation will return to its target path after the fuel price hike." Indonesia's government cut fuel subsidies on June 22 to reduce budget deficits and the

- 10. BI had forecast this would trigger higher inflation. The central bank, which cuts its 2013 economic growth forecast, also says it will provide adequate liquidity to the foreign exchange market to maintain a stable exchange rate. The Reserve Bank of India (RBI) on July 15 raises its marginal standing facility (MSF) rate by 200 basis points to 10.25 percent to “restore stability to the foreign exchange market.” The Central Bank of the Republic of Turkey on July 23 raises overnight lending rate by a sharp 75 basis points and says it will tighten monetary policy further if necessary to support financial stability. The central bank says recent developments have an adverse affect on inflation, including a surge in unprocessed food prices and rising oil prices, and the increased exchange rate volatility may continue to adversely impact inflation in the short term. "Although the Committee sees these developments as temporary to a large extent, a measured tightening is deemed necessary in order to contain a deterioration in the pricing behaviour," the central bank says, adding: "Capital flows have weakened since May due to increasing uncertainty regarding the global monetary policies," and tighter policy would help support financial stability. The Central Bank of Nigeria on July 23 warns of the risks from rising government deficits, pressure on the exchange rate from excess liquidity in the banking system and a possible reversal of capital flows. The central bank also raises to 50 percent from 12 percent the Cash Reserve Requirement on banks’ public sector deposits, i.e. deposits that originate from federal, state and local governments and ministries, department and agencies (MDAs). "The Committee observed the build-up in excess liquidity in the banking system, and expressed concern over the rising cost of liquidity management as well as the sluggish growth in private sector credit, which was traced to DMB's (deposit money banks) appetite for government securities," the CBN said, adding: "The situation is made more serious by the perverse incentive structure under which banks source huge amounts of public sector deposits and lend same to the government (through securities) and the CBN (via OMO bills) at high rates of interest." The Reserve Bank of New Zealand on July 24 confirms that it will hold rates steady through the year but warns that will probably have to tighten policy in the future, depending on how much the housing market and construction sector fuels inflation pressures. The introduction of a tightening bias was not expected by economists, though the central bank has often voiced its concern over the strength of the housing market and the effect this may have on inflation. The Reserve Bank of India (RBI) on July 30 maintains its main policy rates but cuts the growth forecast and appeals to politicians to take immediate steps to slash the current account deficit and it says it is "ready to use all available instruments and measures at its command to respond proactively and swiftly to any key adverse development." The RBI says it is "caught in a classic 'impossible trinity' trilemma whereby we are having to forfeit some monetary policy discrection to address external

- 11. sector concerns." The trilemma refers to a concept in international economics that says it is impossible to have a fixed exchange rate, free capital movement and an independent monetary policy at the same time. Under normal circumstances, the RBI would have been able to continue last year's policy of easing to boost growth but downward pressure on the rupee is limiting its options. AUGUST 2013 TOTAL RATE CUTS: 645 basis points RATE CUTS: The central banks of Angola, Australia, Botswana, Egypt, Georgia, Hungary, Jordan, Mozambique, Romania, Sierra Leone and Ukraine. TOTAL RATE RISES: 350 basis points RATE CUTS: The central banks of Armenia, Brazil, Dominican Republic and Indonesia, GLOBAL MONETARY POLICY RATE (GMPR): 5.58 percent KEY EVENTS: The Central Bank of Egypt on Aug. 1 cuts its overnight deposit rate by 50 basis point, saying the downside risks to economic growth outweigh the upside risks to inflation. The central bank raised rates in March to fend off inflationary pressure but now says inflationary risks have moderated as a rebound in international food prices is unlikely in light of slow global growth. The Czech National Bank on Aug. 1 says it is now more likely to use intervention in foreign exchange markets to keep the koruna currency low. The Czech Republic's central bank first raised the issue of using foreign exchange market intervention to lower the koruna currency in September 2012 and in May it said it was ready to use intervention if further policy easing becomes necessary. In its presentation, the bank sharpens its language, saying "the likelihood of launching foreign exchange interventions to ease monetary policy has increased further." The Reserve Bank of Australia (RBA) on Aug. 6 cuts its cash rate by a further 25 basis points, but omits a reference to having scope to adjust policy if required to support demand, a signal that it is approaching the end of its easing cycle. The RBA ,which has cut rates by 225 basis points since October 2011, says the Australian dollar remains at a high level although it has depreciated by around 15 percent since early April. "It is possible that the exchange rate will depreciate further over time, which would help to foster a rebalancing of growth in the economy," the RBA says, repeating last month's statement and acknowledging the benefits of a lower exchange rate on the international competitiveness of its exports.

- 12. The Bank of England (BOE) on Aug. 7 adopts forward guidance to better influence market expectations about the conditions that may lead to a change in monetary policy stance. The BOE says it intends to maintain its Bank Rate at the current level of 0.5 percent and is ready to purchase further assets at least until the U.K. unemployment rate falls to a threshold of 7.0 percent. But the BOE is also introduces two inflation conditions and a financial stability condition that would "knock out" the unemployment threshold. Under the inflation conditions, consumer prices should remain below 2.5 percent in 1-1/2 to 2 years ahead and medium-term inflation expectations should remain anchored. Under the financial stability condition, the BOE's new Financial Policy Committee must not consider the monetary policy stance a "significant threat to financial stability." "The knock-outs would not necessarily trigger an increase in Bank Rate - they would instead be a prompt for the MPC to reconsider the appropriate stance of policy," says BOE Governor Mark Carney. "But until the unemployment threshold is reached the MPC intends not to reduce the stock of asset purchases from the current 375 billion pounds." The two inflation knockouts were included to ensure that the forward guidance - known as a state-contingent guidance - is consistent with the BOE's primary objective of price stability, currently defined as inflation of 2.0 percent. The financial stability knockout was included because the BOE has been given responsibility for ensuring financial stability."It is important to stress that forward guidance does not mean the MPC is promising to keep interest rates low for a particular period of time. The path of Bank Rate and asset purchases will, as always, depend on economic conditions," Carney says, adding: "So 7% is merely a 'way station' at which the MPC will reassess the state of the economy, the progress of the economic recovery, and, in that context, the appropriate stance of monetary policy." The Central Bank of Chile on Aug. 14 again warns it may cut rates in coming months if the economy continues to slow down. The central bank, which last cut its rate in January 2012, said global economic activity in the second quarter was generally lower than expected and surveys show that domestic consumption, which remains dynamic, is expected to ease and investment to moderate. "The consolidation of the trends outlines in the last Monetary Policy Report could call for adjustments to the monetary policy interest rate in the coming months," the central bank said, repeating its statement from July. The Central Bank of the Republic of Turkey on Aug. 20 raises its overnight lending rate by 50 basis points and says "additional monetary tightening will be implemented whenever needed" until the inflation outlook is in line with medium-term targets. Turkey's lira has been hard hit from the change in global risk assessments as investors prepare for a reduction in quantitative easing by the U.S. Federal Reserve, and the central bank said the weakness in capital flows that started in May had continued. Bank Indonesia (BI) on Aug. 29 raises its benchmark BI rate by 50 basis points, strengthens its currency intervention and liquidity management operations and signs a

- 13. $12 billion swap agreement with the Bank of Japan to bolster its defenses in light of the outflow of capital, pressure on the rupiah currency and high inflationary expectations. The central bank says, after an extraordinary meeting of its board, that it "was ready to take further measures to strengthen its monetary policy instruments and the macroprudential policy mix if required." Pressure on the rupiah is also continuing, the BI says, partly from the general pressure on almost all emerging market currencies but also because of the high current account deficit and inflation. "Bank Indonesia assesses that the level of today's exchange rate reflects the fundamentals as well as supports increased exports and decreased imports as part of the process of adjusting the current account deficit," the bank says. BI says the increase in interest rates should help it further control inflation expectations and "mitigate the risk of a possible influence of the rupiah deprecation on inflation and vice versa." It adds the new measures should also reduce the current account deficit to a sustainable level. The Federal Reserve Bank of Kansas City’s 2013 Jackson Hole Economic Policy Symposium on Aug. 23 publishes paper by Robert E. Hall: “The Routes into and out of the Zero Lower Bound.” Paper says pent-up demand for investment on business plants and equipment, homebuilding and consumer durables will strengthen the U.S. economy and the main danger over the next two years is that the Federal Reserve contracts its portfolio of assets or raise rates on reserves before the economy has returned to a normal state. Hall writes that most of the forces that led the U.S. and other advanced economies into the 2007-2009 recession and investment flows are now beginning to return to normal and the labor market has returned to normal in terms of jobs value notwithstanding the continued high unemployment rate. The Federal Reserve Bank of Kansas City’s 2013 Jackson Hole Economic Policy Symposium on Aug. 23 publishes paper byArvind Krishnamurthy and Annette VissingJorgensen: “The Ins and Outs of LSAPs.” The authors write that the Federal Reserve should spell out its conditions for winding down quantitative easing (QE) to avoid further damaging rises in long-term interest rates. So far, the Fed has been deliberately vague about its plans for asset purchases – so-called large scale asset purchases or LSAPs to retain flexibility in its policy given its limited knowledge of how this tool affects the real economy. But the jump in global bond yields and the plunge in stock markets following the Fed’s June 19 statement is evidence of the sensitivity of investors to the future of LSAPs, mainly because QE targets long term bonds whose prices are very sensitive to expectations of future policy. One of the distinguishing features of QE is that it entails the purchase of longer maturity assets, such as mortgage-backed securities (MBS) or Treasury bonds. This compares with traditional monetary policy that typically focuses on short-term rates, and in the case of the Fed, the overnight fed funds rate.“Since the prices of long maturity assets are much more sensitive to expectations about future policy than short maturity assets, controlling those expectations is of central importance in the transmission mechanism of QE. Therefore, how an exit is communicated to investors matter greatly,” they say. “By being imprecise in the state-dependence of LSAP policy, the Fed has left it to investors to form expectations over the future of LSAPs,” they write, adding that “Investors only understand that LSAPs are a tool to be used when the zero-lower-bound is binding. Thus when the Fed communicates that it

- 14. plans on not using LSAPs, investors assume that the zero-lower-bound will not be binding and that rate hikes will follow.” The Federal Reserve Bank of Kansas City’s 2013 Jackson Hole Economic Policy Symposium on Aug. 24 publishes paper by Helene Rey: “Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence.” Rey writes that a global financial cycle, mainly determined by U.S. monetary policy, constrains national monetary policies when capital is freely mobile regardless of the exchange rate regime. Rey shows how global capital flows, asset prices, credit growth and financial leverage tend to move in sync with the VIX, the ticker symbol for the Chicago-traded index that measures uncertainty and risk aversion in financial markets. The VIX thus becomes a proxy for a global financial cycle that is independent of countries’ specific economic conditions. SEPTEMBER 2013 TOTAL RATE CUTS: 220 basis points RATE CUTS: The central banks of Egypt, Hungary, Israel, Latvia, Mexico, Romania and West African States. TOTAL RATE RISES: 201 basis points RATE RISES: The central banks of Bulgaria, India, Indonesia, Pakistan and Uganda, GLOBAL MONETARY POLICY RATE (GMPR): 5.58 percent KEY EVENTS: The Bank of Mexico on Sept. 6 surprises markets by cutting its interbank target rate by 25 basis points, saying economic growth this year and 2014 will be weaker than expected, putting downward pressure on inflation. The central bank says downside risks to the economy had risen and growth this year will be "considerably" less than forecast, just as growth in 2014 will be below the forecast. "With regard to inflation risks in the short term, there is the possibility that the weakening of Mexico's economic activity is greater and more prolonged than expected and that could cause downward pressure," the bank says. The central bank notes the recent volatility and pressure on the currencies of emerging economies, including Mexico's, and higher medium and longterm interest rates due to the expected changes in U.S. monetary policy. "Mexico's sovereign risk, unlike other emerging economies, has remained stable after having increased in May and June, contributing to the strength of Mexico's macroeconomic fundamentals," the central bank says. The Bank of Russia on Sept. 13 takes major step forward in its move toward an inflation-targeting regime on Feb. 1, 2014 and adopts the rate on one-week deposit auctions as its main policy instrument to provide liquidity, replacing the refinancing rate. The one-week rate on deposit auctions is raised to 5.50 percent from 5.0 percent. The bank also adopts a new interest rate corridor comprising one-day liquidity provisions as

- 15. the upper limit and one-day absorption facilities as the lower limit. The rates are set at 6.50 percent and 4.50 percent. The Reserve Bank of New Zealand (RBNZ) on Sept. 11 repeats that it expects to maintain its benchmark Overnight Cash (OCR) steady this year but adds that "OCR increases will likely be required next year" and the "the extent and timing of the rise in policy rates will depend largely on the degree to which the momentum in the housing market and construction sector spills over into broader demand and inflation pressures." The guidance by the RBNZ is slightly more specific than in July when it said a "removal of monetary stimulus will likely be needed in the future," omitting any mention of when it may tighten. The Bank of Russia on Sept. 13 takes major step forward in its move toward an inflation-targeting regime on Feb. 1, 2014 and adopts the rate on one-week deposit auctions as its main policy instrument to provide liquidity, replacing the refinancing rate. The one-week rate on deposit auctions is raised to 5.50 percent from 5.0 percent. The bank also adopts a new interest rate corridor comprising one-day liquidity provisions as the upper limit and one-day absorption facilities as the lower limit. The rates are set at 6.50 percent and 4.50 percent. The U.S. Federal Reserve on Sept. 18 surprises markets by deciding to continue with its monthly purchase of $85 billion worth of mortgage-backed securities and longterm Treasury bonds "until the outlook for the labor market has improved substantially in a context of price stability." The Federal Reserve's policy making body, the Federal Open Market Committee (FOMC) says the economy and labor market has improved over the last year when its began its latest asset purchase program, despite the impact of the cuts in the federal deficit. "However, the Committee decided to await more evidence that progress will be sustained before adjusting the pace of its purchases," the FOMC says, adding that asset purchases were not on preset course and the pace of the purchases will depend on conditions in the labor market. The Fed affirms that it still expects to keep the federal funds rate between zero and 0.25 percent at least as long as the unemployment rate is above 6.5 percent and inflation is below 2.5 percent. The Fed’s surprise decision to continue with its asset purchases, triggers debate over the usefulness of forward guidance given that investors’ expectations were so wrong. By adding more predictability and transparency to central banks’ policy, forward guidance was supposed to reduce market volatility. Most of the criticism of the Fed is directed toward its ability to communicate but the consequence of the Fed’s deliberate policy of vagueness and uncertainty about winding down quantitative easing may have consequences for its policy, as witnessed by Richard Fisher, president of the Dallas Fed, who says the decision calls into question the credibility of the Fed’s communications. The Reserve Bank of India (RBI) on Sept. 20 begins to wind up exceptional measures aimed at shoring up the embattled rupee and raises the policy repo rate by

- 16. 25 basis points to combat inflation while cutting the marginal standing facility (MSF) rate by 75 basis points to ease short-term liquidity conditions. The RBI also cuts the minimum daily maintenance of the cash reserve ratio (CRR) to 95 percent from 99 percent while keeping the overall CRR rate unchanged at 4.0 percent. "We believe that easing the exceptional liquidity measures was warranted given that the external environment has improved and given that the government and the RBI have used the time since the measures were put in place to narrow the current account deficit and ease its financing," the new governor of the RBI, Raghuram Rajan, says. He adds: "Recognizing that inflationary pressures are mounting and determined to establish a nominal anchor which will allow us to preserve the internal value of the rupee, we have raised the repo rate by 25 basis points." The Bank of Israel (BOI) on Sept. 23 cuts its policy rate by 25 basis points as inflation is below the midpoint of the bank's target range, domestic growth is slowerthan-expected, the economies of advanced economies may slow down and the shekel has continued to appreciate. The BOI also cuts its growth forecast for 2013. The Czech National Bank (CNB) on Sept. 26 says it’s "ready to use the exchange rate if further monetary policy easing becomes necessary." "The probability of launching foreign exchange interventions has not changed and remains high," the CNB says, adding that interest rates are first forecast to rise in 2015 and "given the zero lower bound on monetary policy rates, this points to a need for easing monetary policy using other instruments." "The risks to the inflation forecast are slightly on the downside, tilted toward the need for slightly easier monetary conditions," the strongest sign to date that the CNB is ready to intervene in foreign exchange markets to push down the koruna's exchange rate. The Reserve Bank of Australia on Sept. 30 says the full effects of rate cuts since late 2011 "are still coming through, and will be for a while yet." While the RBA repeated that it would "continue to assess the outlook and adjust policy as needed," the bank softened its description of the Australian dollar, saying that it is still about 10 percent below its level in April despite a recent rise. "A lower level of the currency than seen at present would assist in rebalancing growth in the economy," the RBA said, no longer describing the exchange rate of the A$ as high, as it has in recent months. OCTOBER 2013 TOTAL RATE CUTS: 306 basis points RATE CUTS: The central banks of Bulgaria, Chile, Hungary, Jordan, Mexico, Mozambique, Serbia, Sri Lanka and Tajikistan, TOTAL RATE RISES: 75 basis points RATE RISES: The central banks of Brazil and India,

- 17. GLOBAL MONETARY POLICY RATE (GMPR): 5.52 percent KEY EVENTS: The European Central Bank (ECB) on Oct. 2 confirms that it expects to maintain its policy rates "at present or lower levels for an extended period of time," but adds that it is keeping a close eye on the rise in money market rates "which may have implications for the stance of monetary policy and are ready to consider all available instruments." U.S. President Barrack Obama on Oct. 9 nominates Federal Reserve Vice Chair Janet Yellento succeed Ben Bernanke, whose second term as chairman of the world’s most powerful central bank ends on January 31, 2014. If approved, Yellen will become the first woman to head a central bank in a Group of Seven (G7) leading economic nation. The Central Bank of Chile on Oct. 17 cuts its policy rate by 25 basis points, surprising economists although the bank’s board had considering cutting in the previous five meetings and warned it would cut if the economy continues to slow down. The bank said the cut, the first since January 2012, came in response to slower global growth and signs that domestic demand is slowing further and inflation is below forecasts. Norges Bank on Oct. 24 omits its guidance from September that rates would be maintained at the current level until next summer when they would be gradually raised to a more normal level. The Norwegian central bank says growth among its main trading partners was fairly low but in line with its forecasts but the expected increase in key rates abroad had again been pushed somewhat further into the future. In addition, household demand in Norway seems to be slightly weaker than assumed, house prices have leveled off and inflation has slowed. The Bank of Canada (BOC) on Oct. 23 drops its slight tightening bias due to lower-than-expected economic activity from weaker global growth and says the "substantial monetary policy stimulus currently in place remains appropriate." The BOC started to warn financial markets in April 2012 that it would have to raise interest rates at some point to keep inflation at bay but economic growth then slowed in the second half of the year and in January 2013 the BOC conceded that a rate rise was less imminent than expected. Although the BOC still maintained a tightening bias, the arrival of new Governor Stephen Poloz, who took over from Mark Carney, now at the Bank of England, was accompanied by a slight change to the wording of its guidance in July, though the BOC still maintained in September that it would eventually normalize rates as economic conditions return to normal. The Bank of Mexico on Oct. 25 cuts its policy rate by another 25 basis points, its third rate cut this year, but says it is not considering further rate reductions “in the foreseeable future” and wants to ensure that inflation is not affected by changes to taxes and U.S. monetary policy. The Reserve Bank of India (RBI) on Oct. 29 raises its policy rate by another 25 basis points to "curb mounting inflationary pressures and manage inflation expectations

- 18. in a situation of weak growth." The RBI cuts the marginal standing facility (MSF) rate by a further 25 basis points to 8.75 percent to “infuse liquidity into the system” as it finishes unwinding July’s exceptional tightening measures. NOVEMBER 2013 TOTAL RATE CUTS: 545 basis points RATE CUTS: The central banks of Albania, Angola, Armenia, Chile, Congo Dem. Repl., Eurosystem, Hungary, Latvia, Peru, Romania, Serbia and Thailand, TOTAL RATE RISES: 125 basis points RATE RISES: The central banks of Brazil, Indonesia and Pakistan. GLOBAL MONETARY POLICY RATE (GMPR): 5.47 percent KEY EVENTS: The Reserve Bank of Australia (RBA) on Nov. 4 describes the exchange rate of the Australian dollar as "uncomfortably high" and a "lower exchange rate is likely to be needed to achieve balanced growth in the economy." The statement about the Aussie is much stronger than in recent months. In September, for example, the RBA dropped its earlier description of the A$ exchange rate as "high" and merely said that a lower exchange rate level would "assist" in rebalancing growth. The National Bank of Poland (NBP) on Nov. 6 pushes back any rate rise by another six months, saying it would maintain rates "at least until the end of the first half of 2014" as the latest forecast confirms low inflationary pressure and an expected moderate economic recovery. At its previous meeting in September, the NBP said it would maintain its interest rate at "least until the end of 2013." The Central Bank of Peru on Nov. 7 cuts its policy rate by 25 basis points, its first rate change since April 2011, describing the rate cut as "preventative and does not imply a sequence of reductions." The European Central Bank (ECB) on Nov. 7 surprises markets by cutting its refinancing rate by 25 basis points, its second cut this year, following a sharp drop in October inflation to 0.7 percent and says it will give banks all the money they need for as long as necessary, and at least until the second quarter of 2015, to boost economic growth. ECB says the euro area “may experience a prolonged period of low inflation.” The ECB also affirms its guidance that its monetary policy will "remain accommodative for as long as necessary" and it "expects the key ECB interest rates to remain at present or lower levels for an extended period of time."

- 19. The National Bank of Denmark on Nov. 7 maintains key rates, breaking with its tradition of following the European Central Bank’s rate changes, saying commercial banks have "a large need to place funds" at the central bank. The bank entered unchartered territory in July 2012 when it cut its rates, including the deposit rate by 25 basis points to a negative 0.2 percent, in an attempt to weaken the crown which came under upward pressure as investor sought safe haven outside the euro area's sovereign debt crises. In January rates were raised by 10 basis points, leaving the deposit rate at a negative 0.10 percent and the key lending rate at 0.30 percent. The Czech National Bank on Nov. 7 says it will "start using the exchange rate as an additional instrument for easing the monetary conditions" and "will intervene on the foreign exchange market to weaken the koruna so that the exchange rate against the euro is close to CZK 27." The central bank’s board has been debating currency intervention for months and in October it decided that it was "ready to use the exchange rate if further monetary policy easing becomes necessary," citing the risk that inflation may decline further. The Bank of Latvia on Nov. 11 slashes its refinancing rate by 125 basis points to 0.25 percent, mirroring the ECB’s rate, saying "inflation indicators remain low in Latvia and the rate at which the economy develops does not pose risks to price stability in the medium term." Latvia becomes the 18th nation to adopt the single currency, the euro, on January 1, 2014. The Central Bank of the Republic of Turkey (CBRT) on Nov. 19 scraps its onemonth repurchase auctions to limit the impact of exchange rate fluctuations on inflation and the volatility of short term money market rates, saying this would strengthen the bank's "cautious stance," and result in interbank money market rates of around 7.75 percent. The bank also omits the reference to the one-week repo rate as its “policy rate” and on Nov. 20 explains that the one-week repo rate should no longer be considered its reference rate and instead markets should focus on the overnight interbank lending or repo rates . Minutes from the October meeting of the Federal Reserve’s Federal Open Market Committee published on Nov. 20 says some of the committee members “pointed out that, if economic conditions warranted, the Committee could decide to slow the pace of purchases at one of its next few meetings.” The South African Reserve Bank (SARB) on Nov. 21 says that "given the increased upside risks to the outlook, we do not see room for further monetary accommodation." Although the growth outlook remains fragile, upside risks to inflation and a possible further deprecation of the rand from a reduction in the U.S. Federal Reserve's asset purchases outweighs this weak outlook for growth. "The challenge facing the MPC is not only to anticipate the timing and speed of Fed tapering, but also to try to assess the extent to which tapering is already priced into the exchange rate.

- 20. There is a risk that, should there be a stronger or more disorderly response by the markets to actual Fed tapering, the reaction of the exchange rate could be more extreme," said Gill Marcus, SARB governor. The Central Bank of Chile on Nov. 19 cuts its policy rate for the second time in a row, saying third quarter data confirmed its expectations that all components of demand are slowing down. The Bank of Thailand (BOT) surprises markets on Nov. 27 by cutting its rate for the second time this year, saying there is room for monetary policy to mitigate the growing downside risks to the economy "given the benign inflation outlook and moderating household credit growth.” The BOT had been expected to maintain rates due to concern over high household debt and fears that an expected reduction in asset purchases by the U.S. Federal Reserve in coming months could lead to outflow of capital and downward pressure on the Thai baht. The Central Bank of Brazil on Nov. 27 raises its benchmark Selic rate for the sixth time in a row but omits its usual reference to the decision contributing to reducing inflation and ensuring that this trend would persist into next year. This stokes speculation that the central bank will pause in its tightening cycle. Brazil's inflation rate eased slightly to 5.84 percent in October from 5.86 percent in September, continuing its decline since hitting a year-high of 6.7 percent in June. The Bank of England on Nov. 28 rolls back support for the U.K. housing sector, saying “additional stimulus for lending to households is no longer required.” BOE Governor Mark Carney explains the shift toward neutral in the bank’s support of home lending would in fact allow the bank’s key rates to stay low for longer. The move comes two weeks after the BOE’s upgraded its view of the UK economy in its November inflation report with the implication that interest rates may be raised in 2015 rather than 2016. DECEMBER 2013 TOTAL RATE CUTS: 495 basis points RATE CUTS: The central banks of Albania, Armenia, Botswana, Egypt, Hungary, Serbia, Sweden, Uganda and Uzbekistan. TOTAL RATE RISES: 50 basis points RATE RISES: The central bank of Tunisia. GLOBAL MONETARY POLICY RATE (GMPR): 5.42 percent KEY EVENTS:

- 21. The Bank of Canada on Dec. 4 says the "substantial monetary policy stimulus currently in place remains appropriate" but cautions that the downside risks to inflation "appear to be greater." The Central Bank of Egypt on Dec. 5 surprises financial markets by cutting its benchmark rate by 50 basis points, its third cut in a row, despite rising inflation. The central bank has been under pressure to maintain high rates to attract capital and not deplete foreign currency reserves, which have been under pressure since the political uprising in 2011 that toppled President Hosni Mubarak. But the bank says there are limited risks to higher inflation due to “pronounced downside risks to domestic GDP combined with the persistently negative output gap since 2011.” The European Central Bank (ECB) on Dec. 5 says economic activity should slowly recover in 2014 and 2015 but the euro area “may experience a prolonged period of low inflation.” The ECB cuts its inflation forecast for 2013 and 2014 and says the lower forecast confirms the ECB’s decision to cut rates in November. Norway’s central bank, Norges Bank on Dec. 5 pushes back its forecast for a rate rise by one year until the summer of 2015, saying inflation had been lower than expected in the past two months, economic growth will be lower than forecast, house prices have declined and wage growth may be somewhat lower than projected. In September Norges Bank forecast that rates would be maintained at the current level until the summer of 2014 and then gradually raised, but then in October the bank dropped this guidance, saying rate rises by key trading partners had been pushed further into the future. Bank Indonesia on Dec. 12 holds rates steady but says it will remain "watchful of the planned tapering policy by the Federal Reserve and will bolster the ongoing policy response. The bank has raised its rates five times to curb inflation, also said its current stance was "consistent with ongoing efforts to bring inflation back towards the target corridor” as well as to reduce the current account deficit to a more sustainable and sound level." The Reserve Bank of New Zealand on Dec. 11 warns it "will increase the OCR as needed in order to keep future average inflation near the 2 percent target," a more hawkish statement than in October when it said an increase in the Official Cash Rate (OCR) “will likely be required next year.” The central bank raises its forecast for the 90day rate, which has closely tracked the OCR rate ever since it was introduced in March 1999, by about 50 basis points, projecting a rise to 3.8 percent by December 2014 from around 2.5 percent. The Reserve Bank of India on Dec. 18 surprises markets by holding its main interest rates steady and emphasizes that it is not soft on inflation and is poised to act if inflation does not fall in coming months. The RBI describes its decision as a close one and says "there are obvious risks to waiting for more data, including the possibility that tapering of quantitative easing by the US Fed may disrupt external markets and that the Reserve Bank may be perceived to be soft on inflation." But the RBI expects inflation to

- 22. fall in coming months and does not want to tighten policy too much and damage the economy given the long lag before any rate rise takes effect. Sweden’s Riksbank on Dec. 17 cuts its repo rate by 25 basis points and pushes back any rate rise until early 2015 from late 2014 due to lower-than-expected inflation. The Federal Reserve on Dec. 18 decides to trim its purchase of bonds and housingrelated securities assets by a modest $10 billion to $75 billion a month starting in January 2014 due to the improved situation on the labor market and will then probably continue to reduce the pace of asset purchases "in further measured steps" in coming months if the jobless rate continue to fall and inflation rises towards the central bank's 2.0 percent objective. But the Fed adds that its asset purchases were not on a preset course and decisions about the future pace of purchases are contingent on the economic outlook. But to reinforce the message that it rates will remain low, the Fed says it expects to keep its fed funds rate at essentially zero "well past the time that the unemployment rate declines below 6-1/2 percent, especially if projected inflation continues to run below the Committee's 2 percent longer-run goal." Article credit and link : http://www.centralbanknews.info/2014/01/global-monetarypolicy-highlights-2013.html