1. Macroeconomic Environment of craftsmen and artists’ world:

PESTEL ANALISYS

01/10/2015

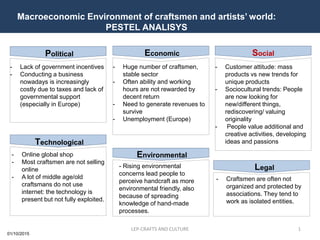

- Lack of government incentives

- Conducting a business

nowadays is increasingly

costly due to taxes and lack of

governmental support

(especially in Europe)

- Huge number of craftsmen,

stable sector

- Often ability and working

hours are not rewarded by

decent return

- Need to generate revenues to

survive

- Unemployment (Europe)

Political Economic

- Online global shop

- Most craftsmen are not selling

online

- A lot of middle age/old

craftsmans do not use

internet: the technology is

present but not fully exploited.

- Customer attitude: mass

products vs new trends for

unique products

- Sociocultural trends: People

are now looking for

new/different things,

rediscovering/ valuing

originality

- People value additional and

creative activities, developing

ideas and passionsTechnological

Environmental

Social

Legal- Rising environmental

concerns lead people to

perceive handcraft as more

environmental friendly, also

because of spreading

knowledge of hand-made

processes.

- Craftsmen are often not

organized and protected by

associations. They tend to

work as isolated entities.

1LEP-CRAFTS AND CULTURE

2. Analysis about the intermediary industry between craftsmen and

customers :THE 5 FORCES MODEL

Five Forces Impact and Rating

Score from Score* to Implied rating

0,0 1,0Very Weak

1,1 2,0Weak

2,1 2,4Low medium

2,5 2,5Medium

2,6 3,0High medium

3,1 4,0Strong

4,1 5,0Very strong

Our aim is to use this rating to try to assess the relative importance of the five forces in

this industry. In particolar these forces are:

•COMPETITIVE RIVALRY

•THREAT OF SUBSTITUTE PRODUCTS

•THREAT OF NEW ENTRANTS

•BARGAINING POWER OF SUPPLIERS

•BARGAINING POWER OF BUYERS

2LEP-CRAFTS AND CULTURE

*The higher the score, the stronger the force: ceteris paribus, the industry will be less attractive.

3. LEP-CRAFTS AND CULTURE 3

•COMPETITIVE RIVALRY: Our major competitors will be online retailers for

handmade goods and other online platforms. These sites sell everything and sometimes

they are more similar to bazaars than to quality-assuring services. However they are

numerous, heterogeneous and they are not concentrated. The industry faces medium

fixed costs, low exit barriers and there are not switching costs for customers. On the

other hand we think the market for hand-made and art products is growing, opening new

spaces for competition. It is clear that our goal is to differentiate our service in order to

assure quality and to offer products whose provenience is guaranteed to lower this

competition and target a more specific segment.

Industry growth

Concentration

Differentiation

Switching costsFixed-Variable costs

Excess capacity

Exit barriers

Rivalry among existing firm

Industry growth 1,5

Concentration 4,0

Differentiation 3,0

Switching costs 4,5

Fixed-Variable costs 3,0

Excess capacity 2,5

Exit barriers 4,0

Avg 3,2

FF impact Strong

4. LEP-CRAFTS AND CULTURE 4

•THREAT OF SUBSTITUTE PRODUCTS: Evaluating this force, we thought that the

alternative to our business is directly purchasing at craftsmen’s laboratories or at art fairs.

This traditional way of buying is costly and time consuming. Our alternative is new, cheap

and the customer can save time and efforts. Most imporantly, the quality is assured by our

close relationships with the artists.

Relative price and

performance

Buyers' willingness

to switch

Cheap alternative

products

Threat of substitute products

Relative price and performance 2,0

Buyers' willingness to switch 2,0

Cheap alternative products 1,5

Avg 1,8

FF impact Weak

5. LEP-CRAFTS AND CULTURE 5

•THREAT OF NEW ENTRANTS: In the chosen industry reputation and relationships

are crucial and it is necessary to invest time and money to develop them in a proper way.

The key is being a first-mover (or almost), in order to develop the biggest network possible

(we are talking about a two-sided market) : if we do this, it is likely that first mover

advantage and learning curve will protect us. On the other hand it is true that we do not

possess legal barriers (excluding trademark) to prevent entrance and that the capital

requirement is low.

First mover

advantage

Learning curve

Relationship with

customer

Legal barriers

Capital

requirements

Threat of new entrants

First mover advantage 2,0

Learning curve 2,0

Relationship with customer 1,5

Legal barriers 4,0

Capital requirements 4,0

Avg 2,7

FF impact

High

medium

6. LEP-CRAFTS AND CULTURE 6

•BARGAINING POWER OF SUPPLIERS: For networking purposes it is

important to involve a high number of suppliers, in our case artists and craftsmen.

This will provide us with a double advantage: the network effect as well as a lower

bargaining power of suppliers in the end. In fact, if we network with high numbers of

individuals, we will have more power attracting them.

In conclusion, we have also to remember that for this type of service the quality of

goods is crucial, and this will surely increase suppliers’ bargaining power.

The final outcome lies on the middle.

Switching costs

Backward

integration threath

Importance of

product for quality

Numbers of

suppliers

Volume per

suplliers

Bargaining power of suppliers

Switching costs 4,0

Backward integration threath 1,5

Importance of product for quality 4,5

Numbers of suppliers 2,0

Volume per suplliers 1,5

Avg 2,7

FF impact

High

medium

7. LEP-CRAFTS AND CULTURE 7

•BARGAINING POWER OF BUYERS: We expect customers to be numerous and

fragmented. As a consequence their bargaining power will be very low. Even if we start

selling to hotels, it is unlikely that there will not be a big buyer that tries to influence the

price or the services offered. For this reason this should be the weakest force in our

analysis. The only drawback is the lack of switching costs they face.

Switching costs

Backward

integtration threath

Numbers of buyers

Volume per buyer

Bargaining power of buyers

Switching costs 4,0

Backward integtration threath 1,0

Numbers of buyers 1,0

Volume per buyer 2,0

Avg 2,0

FF impact Weak

8. LEP-CRAFTS AND CULTURE 8

FINAL ASSESMENT

Five forces

Degree of rivalry 3,2

New entrants 2,7

Substitutes 1,8

Buyer power 1,9

Supplier power 2,6

Avg 2,4

FF impact Low medium

The result of this study underlines how the forces on this industry are low-medium,

meaning that it could be attractive to exploit the actual circumstances with an

original idea. The real challenge is finding something different from the actual

rivals, that represent the most fierce force.

Editor's Notes

voice control system, internet connectivity, emergency assistance