1. Northwestern Mutual

IS YOUR RE TIREMENT PROTECTED?

Oftentimes, the effects of long-term care expenses resulting from an accident, a chronic illness or a cognitive impairment

are overlooked. We cannot predict the future, but we could eventually need caregiving services on a long-term basis.

The cost of receiving these services can jeopardize not only our lifestyle but also our family’s lifestyle and the financial

security we’ve spent our lifetime establishing. This can also cause emotional and financial strain on family members.

The following example illustrates a hypothetical retirement scenario for a married couple, both 50 years old, who are

expected to retire at age 65 with a life expectancy to age 90. A long term care event is illustrated for only one individual.

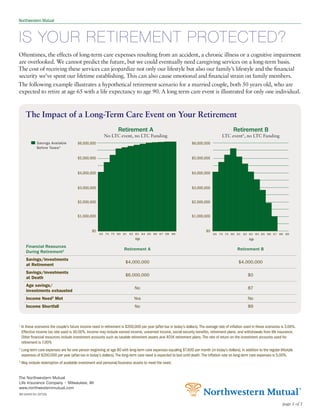

The Impact of a Long-Term Care Event on Your Retirement

$7,000,000

$7,000,000 Retirement A $7,000,000

Retirement B

No LTC event, no LTC Funding LTC event2 , no LTC Funding

Savings Available $6,000,000 $6,000,000

$6,000,000

Before Taxes 3

$5,000,000 $5,000,000

$5,000,000

$4,000,000 $4,000,000

$4,000,000

$3,000,000 $3,000,000

$3,000,000

$2,000,000 $2,000,000

$2,000,000

$1,000,000 $1,000,000

$1,000,000

$0 $0

$0 65 70 75 80 81 82 83 84 85 86 87 88 89 65 70 75 80 81 82 83 84 85 86 87 88 89

65/65

66/66

67/67

68/68

69/69

70/70

71/71

72/72

73/73

74/74

75/75

76/76

77/77

78/78

79/79

80/80

81/81

82/82

83/83

84/84

85/85

86/86

87/87

88/88

89/89

Age Age

Financial Resources

Age

Retirement A Retirement B

During Retirement1

Savings/investments

$4,000,000 $4,000,000

at Retirement

Savings/investments

$6,000,000 $0

at Death

Age savings/

No 87

investments exhausted

Income Need3 Met Yes No

Income Shortfall No 89

1

In these scenarios the couple’s future income need in retirement is $200,000 per year (after-tax in today’s dollars). The average rate of inflation used in these scenarios is 3.00%.

Effective income tax rate used is 30.00%. Income may include earned income, unearned income, social security benefits, retirement plans, and withdrawals from life insurance.

Other financial resources include investment accounts such as taxable retirement assets and 401K retirement plans. The rate of return on the investment accounts used for

retirement is 7.00%

2

Long-term care expenses are for one person beginning at age 80 with long-term care expenses equaling $7,600 per month (in today’s dollars), in addition to the regular lifestyle

expenses of $200,000 per year (after-tax in today’s dollars). The long-term care need is expected to last until death. The inflation rate on long-term care expenses is 5.00%.

3

May include redemption of available investment and personal/business assets to meet the need.

The Northwestern Mutual

Life Insurance Company • Milwaukee, WI

www.northwesternmutual.com

90-2443-01 (0710)

page 1 of 1