Ecosystem Environment for Starting a Semiconductor Company

•

3 j'aime•2,286 vues

Management presentation on the complex ecosystem necessary for a successful semiconductor startup. Covers key issues: marketing, finacial, legal, PR, funding, and technology.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (19)

En vedette

En vedette (6)

Similaire à Ecosystem Environment for Starting a Semiconductor Company

Similaire à Ecosystem Environment for Starting a Semiconductor Company (20)

Ecosystem Environment for Starting a Semiconductor Company

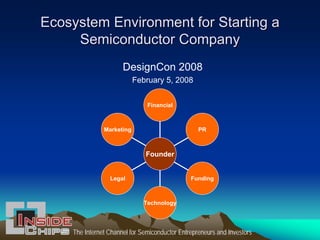

- 1. Ecosystem Environment for Starting a Semiconductor Company DesignCon 2008 February 5, 2008 Financial Marketing PR Founder Legal Funding Technology The Internet Channel for Semiconductor Entrepreneurs and Investors

- 2. Startup Ecosystem Panel Steve Szirom Steve Bengston Senior Analyst, InsideChips Director, Emerging Ventures Practice, President, HTE Research PriceWaterhouseCoopers Lucio Lanza Glen Balzer Managing Director, President, Lanza techVentures New Era Consulting Dave Guzeman James Prenton President, Partner, Mindpik K&L Gates 2

- 3. 2007 World Electronics Markets 2007 World Electronics Markets Worldwide Markets WW GDP $48,000B Total Electronics 100.0% $1,765B Semiconductors 14.3% $252B Consumer Electronics 8.2% $145B Semi Equipment 2.4% $42B Semi Materials 2.3% $41B EDA 0.3% $5.6B Source: InsideChips.com 3

- 4. Ecosystem: Legal • Pre-incorporation: employer issues, NDA/confidentiality/IP issues, founders agreements • Incorporation package, form of equity • Added value – May have synergistic relationships/network – Adds credibility for potential investors 4

- 5. Ecosystem: Technology • EDA tools and IP core partners • Design team strategy and formation – Architecture, circuit design, software, algorithm, compiler – WW design teams • China, Taiwan (multimedia, consumer) • India (software, tools) • Central Europe (software, algorithm) • Israel (DSP) • Russia (algorithm, mathematical) • Reference design customer partner • Wafer fab, test, assembly partners 5

- 6. Ecosystem: Marketing • Marketing objectives, strategies and tactics • How big/where is the market today and in five years – Key customers – Product definition, segmentation – Price trends • Key reference/development customer relationships • Sales and market forecasts • Competitive landscape, unique differentiators • International strategy 6

- 7. Ecosystem: Financial • CPA consultant or part-time CFO (semiconductor experience helpful) • Accounting firm relationship – Pre-sales burn rate, sales ramp, break-even, profitability => P&L, Balance sheet, cash-flow – May have synergistic relationships/network – Adds credibility for potential investors 7

- 8. Ecosystem: Public Relations • Sets the stage for company’s external image/visibility – Investors, customers, partners, distributors/reps, others • Company name, logo and brand – Memorable, what does it mean, domain available, lasting, original, craft a unique and visionary story for the new venture • Web site design and content – Drives the company image worldwide (big bang for the buck) • Create and increase the “buzz” level as appropriate for stage of company 8

- 9. Ecosystem: Public Relations • Use “guerrilla” tactics to stretch limited $$$ • Use combination of external and internal resources • Combine various elements, have an integrated marcom plan for various stages of growth • Think globally, act locally • Do it right the first time! 9

- 10. Craft A+ Communications Financial Marketing PR Founder 50 pages Legal Funding Business Plan 5 pages Design Exec Summary 15 minutes Short Pitch 2 minutes Elevator Pitch Credibility + Potential 10

- 11. Ecosystem: Investors Funding source Stage • “Kitchen table” • Founder(s) • Seed • FFF, Angels, Incubation • “A” round • VCs, Corporate 11

- 12. Key Success Factor: Founder/CEO • Organize founding team, expectations, share agreements, vision • Experience (ideal) in development, operations, marketing, and finance, such as business unit director of mid-large chip maker • Ethics/integrity, creativity, adaptability, persistence, intelligence, experienced, moderate ego • Wisdom to turn reigns over to seasoned management • Openness in internal and external matters • Energy and drive to thrive in resource constrained environment • Act as coach and therapist in early tough going “Startups fold or perform poorly as a result of CEO failure more often than any other single cause” NEXT 12

- 13. Top 5 Legal Issues for Semiconductor Startups James Prenton james.prenton@klgates.com

- 14. #5 – Effect of Employment Agreements ASSUMPTION: I possess all ownership rights to an idea I conceive or develop. ASSUMPTION: I own all inventions that I develop entirely on my own time without using my employer’s equipment, supplies, facilities or trade secret information. ASSUMPTION: My employer wasn’t interested in my idea so I can pursue development. FACT: Potential investors will carefully examine IP ownership to avoid buying into a lawsuit. Certain market segments are notorious for litigation against former employees. When in doubt, seek guidance!

- 15. #4 - Timing and Form of Entity Timing: Dictated by need to memorialize ownership of the business by the founders, sign contracts with third parties, secure IP ownership in the Newco, adopt and use incentive stock plans and set the stage for investments. Delay may result in: (a) dispute among founders (“forgotten founder”), (b) uncertainty over IP ownership and (c) adverse tax consequences when founders try to acquire shares at a nominal price (“cheap stock”). Form of Entity: Corporations over LLC LLCs – Ease in legal maintenance and can be taxed as partnership (losses and gains of business flow through the members’ individual 1040 returns). However, (a) VCs will not invest in an LLC, (b) stock options are not available as incentives, and (c) cannot be acquired tax-free in a stock acquisition exit. Corporations – Sophisticated investors will prefer corporate form. Employees, consultants and advisors will appreciate familiar stock-based incentive plans. More alternatives for successful exit.

- 16. #3 - Ensure Company Owns IP EMPLOYERS. Ensure former and current employers of founders, consultants and advisors will not have a claim against the company’s IP. FOUNDER(S). Individual ownership of idea is not the same as ownership by the company. Each founder must assign their rights to the idea to the company. CONSULTANTS/EMPLOYEES. Ensure agreements with third party developers and employees expressly requires assignment of intellectual property to the company. FACT: Company ownership of IP is one of the key areas investors will focus on when conducting investment due diligence.

- 17. #2 - Manage Equity Carefully Founder Allocation – Difficult to discuss as friends or colleagues. Consider contributions by each and agree in writing. Assumptions and delays re: contributions and equity percentage problematic. Repurchase Right – Ensure shares subject to company’s repurchase right which lapses over time (vesting schedule). Provides incentive for founders to remain with the company. Right of First Refusal – Give company and other shareholders right to acquire shares in the event of a proposed share transfer. Helps avoid unwanted “partner” from joining. Securities Law Compliance – Offering and selling securities highly regulated. Failure to comply can create liabilities and limit ability to raise capital in the future. Avoid Promise to Issue Percentage of Shares. Promises to give certain percentage of shares to consultants and employees can be problematic. Best to document and agree in terms of number of shares. Any cloud over stock ownership will jeopardize the success of a potential fundraising.

- 18. #1 - Seek Help from Experienced Advisors Early! Experienced entrepreneurs, lawyers, accountants, consultants and investors can offer valuable advice to assist in the development of your new startup. Many investors rate judgment of entrepreneurs by their choice of the advisors. Certain advisors will offer promising startups special arrangements which may include a combination of reduced rates, fee deferral or equity ownership. Silicon Valley: a unique concentration of the key components necessary for a startup to succeed. Take full advantage of what the environment has to offer! Dave Guzeman, President, Minkpik

- 19. Marketing Chip Startups Dave Guzeman, CEO - Mindpik guzeman@mindpik.com

- 20. Starting Up… What to do on Day One Marketing & Sales Strategies and initial roadmap set by founders and thrashed out in business plan Critical to have all six Big-M Marketing functions explicitly assigned to people One of the founders should be VP Marketing / Sales Identify six target customers… call them and share that with them Have a plan for achieving financial credibility… why should customers feel safe betting their companies on you?

- 21. Big-M Marketing Executing the Complete Marketing Function Driving the Products – Product Marketing Making the Market – Tactical Marketing Entering Orders – Order Entry / Customer Service Creating a Buzz – Promotional Marketing Working the Technical Community – Technical Marketing Developing Strategies – Strategic Marketing Intel at $50M had Product Marketing, Tactical Marketing, Promotional Marketing, and Order Entry Intel at $100M had added Strategic Marketing and Technical Marketing

- 22. The Intel Startup Model Sell memory chips to IBM and the Seven Dwarfs Limited direct sales force – total 12 direct sales people at $100M – leverage reps and distributors When you know someone’s home phone number… don’t advertise to them… call them! Top company salesman was Bob Noyce Use Noyce, Moore, and Art Rock (VC) to gain credibility Marketing & Engineering driven Extensive publicity campaign Even at $100M, marketing headcount was still 3 times sales headcount

- 23. The Pitfalls The more earthshattering and revolutionary your product is, the more important it is to have financial credibility Don’t skimp on promotional marketing in the early days – outsource it and buy great stuff The more complex your product, the more important product marketing becomes It takes as long to develop a sales channel as to do your chip… and costs about the same Sales channels are driven by relationships… even though your company is young you need to hire a sales manager with 20 years of relationships Customers and contract manufacturers are working to prevent you from selling proprietary products

- 24. Build it and they will come… hahahaha I don’t know who you are. I don’t know your organization. I don’t know your service or product. I don’t know what you stand for. I don’t know your customers. I don’t know your track record. I don’t know your reputation. Now, what was it you wanted to sell me?

- 25. What has changed? WWW – the world’s largest flea market Killed most printed tech publications Zero printing costs for web-based tech literature Still have layout costs plus web programming costs Works well when people know who you are and search by company name Disappearance of printed publications has made it harder – not easier – to get attention Sales reps are harder to find and much more expensive to sign Distributors are disappearing – replaced by CM’s… contract manufacturers and you need a “Fast Eddy” to deal with them NEXT

- 26. Creating a Sales Presence Glen Balzer, President, New Era Consulting glenbalzer@msn.com

- 27. Creating a Sales Presence • Avoid Exclusive Arrangements in your sales channel

- 28. Creating a Sales Presence • Avoid Exclusive Arrangements in your sales channel • Build Direct Sales only when necessary

- 29. Creating a Sales Presence • Avoid Exclusive Arrangements in your sales channel • Build Direct Sales only when necessary • Cause and Convenience – Always reserve the opportunity to terminate a channel partner for cause and convenience

- 30. Creating a Sales Presence • Avoid Exclusive Arrangements in your sales channel • Build Direct Sales only when necessary • Cause and Convenience – Always reserve the opportunity to terminate a channel partner for cause and convenience • Due Diligence – must be performed seriously

- 31. Creating a Sales Presence • Avoid Exclusive Arrangements in your sales channel • Build Direct Sales only when necessary • Cause and Convenience – Always reserve the opportunity to terminate a channel partner for cause and convenience • Due Diligence – must be performed seriously • English Language Skill in a foreign market is not very important Steve Bengston, Director, PwC

- 32. DesignCon 2008 Steve Bengston steve.bengston@us.pwc.com 650 281 9843 © 2007 PricewaterhouseCoopers LLP. All rights reserved. quot;PricewaterhouseCoopersquot; refers to PricewaterhouseCoopers LLP (a Delaware limited liability partnership) or, as the context requires, other member firms of PricewaterhouseCoopers International Ltd., each of which is a separate and independent legal entity. *connectedthinking is a trademark of PricewaterhouseCoopers LLP. SJ_07_0080

- 33. MoneyTree Total Investments: Q1 1999 – Q3 2007 ($ in billions) $32.0 $28.4 $28.2 $26.4 $24.0 $23.3 $22.2 $16.0 $13.2 $12.8 $11.4 $11.0 $8.0 $8.3 $8.1 $7.5 $7.2 $7.1 $6.9 $6.9 $6.8 $6.6 $6.4 $6.3 $6.3 $6.3 $6.0 $5.9 $5.9 $5.8 $5.6 $5.3 $5.0 $5.0 $5.0 $4.9 $4.6 $4.5 $4.3 $0.0 1999 2000 2001 2002 2003 2004 2005 2006 2007 1999 2000 2001 2002 2003 2004 2005 2006 2007 # of Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Deals 918 1304 1421 1865 2128 2107 1931 1743 1283 1217 1001 974 837 849 687 719 692 735 711 782 709 850 682 832 724 819 783 805 864 935 897 912 850 1000 887 November 2007 PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report Slide 2 based on data from Thomson Financial

- 34. MoneyTree Total Investments: 1980 – YTD Q3 2007 Annual Venture Capital Investments ($ in billions) 1980 to YTD Q3 2007 $105.1 $120 $100 $80 $54.1 $60 $40.6 $40 $26.4 $23.0 $22.4 $21.9 $21.8 $21.1 $19.7 $14.9 $11.3 $20 $8.0 $4.1 $3.7 $3.3 $3.3 $3.3 $3.5 $3.0 $3.0 $2.8 $3.0 $2.8 $2.2 $1.6 $1.2 $0.6 $0 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 D6 07 Y T 200 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 20 20 20 20 20 20 20 November 2007 PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report Slide 3 based on data from Thomson Financial

- 35. Investments by Region: Q3 2007 Upstate NY New England $31.5 Northwest $998-14% 12 Deals $290.6 119 Deals 47 Deals Sacramento/N. CA NY Metro $14.5 North Central $385-5% 2 Deals $111.0 57 Deals 17 Deals Philadelphia Metro Silicon Valley $238.3 $2,485-35% Midwest Colorado 26 Deals 287 Deals $343-5% $196.6 45 Deals 24 Deals LA/Orange County DC/Metroplex $425-6% $331-5% Southwest South Central 56 Deals 34 Deals $134.2 $19.2 23 Deals San Diego 7 Deals Southeast $359-5% $353-5% 37 Deals Texas 52 Deals $386-5% 39 Deals KAU AI AK/HI/PR NIIHA U O AHU $4.1 MOLOKAI MA UI LANAI 3 Deals KAHOOLA WE HA W AII Q3 2007 Total Investments - $7,104 in 887 Deals November 2007 PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report Slide 4 based on data from Thomson Financial

- 36. Investments by Industry: Q3 2007 ($ in millions) $1,108.1 Software $1,091.2 Biotechnology $920.6 Industrial/Energy # of % Change $ $825.5 Medical Devices and Equipment Industry Deals from Q2 ’07 $585.1 Telecommunications Software 187 -27.18% Biotechnology 99 -10.04% $513.2 Semiconductors Media and Entertainment 96 9.68% $508.5 Media and Entertainment Industrial/Energy 83 69.42% Medical Devices and Equipment 76 -19.86% $353.9 IT Services Telecommunications 74 13.56% $289.1 Networking and Equipment Semiconductors 55 12.19% IT Services 51 44.7% $280.2 Financial Services Financial Services 31 420.22% $194.7 Business Products and Services Networking and Equipment 29 -22.16% Business Products and Services 23 -2.59% $152.8 Electronics/Instrumentation Electronics/Instrumentation 21 -1.95% $96.3 Healthcare Services Consumer Products and Services 20 -65.91% Healthcare Services 15 251.14% $87.7 Computers and Peripherals Computers and Peripherals 13 -41.07% $57.3 Consumer Products and Services Retailing/Distribution 13 -56.89% Undisclosed/Other 1 -100.00% $40.0 Retailing/Distribution TOTAL 887 -1.43% $0.0 Other NM = Not Meaningful $0 $900 $1,800 Q3 2007 Total: $7,104 in 887 Deals Visit www.pwcmoneytree.com for Industry definitions November 2007 PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report Slide 5 based on data from Thomson Financial

- 37. Investments by Stage of Development: Q3 2007 ($ in millions) Later Stage $2,976.4 Expansion $2,718.5 % Change in # of Stage of Development $ Amount Deals from Q2 2007 Early Stage $1,185.3 Expansion Stage 294 16.00% Later Stage 288 -7.07% Early Stage 213 -17.54% Startup/Seed 92 0.29% Startup/Seed $224.0 Total 887 -1.43% $0 $1,000 $2,000 $3,000 Q3 2007 Totals: $7,104 in 887 Deals Last November 2007 PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report Slide 6 based on data from Thomson Financial

- 38. Questions and Discussion? • Steve Szirom, InsideChips (www.insidechips.com) – Marketing, PR, business, international, strategy • Lucio Lanza, Lanza techVentures – Incubation, venture capital, VC trends, other • Dave Guzeman, Mindpik (www.mindpik.com) – Marketing, other • Glen Balzer, New Era Consulting (www.neweraconsulting) – Sales, distribution, international, other • Steve Bengston, PriceWaterhouseCoopers (www.pwc.com) – Financial and accounting issues • James Prenton, K&L Gates (www.klgates.com) – Legal issues, founders’ agreements, incorporation, employment issues The Internet Channel for Semiconductor Entrepreneurs and Investors