Revenue tax collection , Interim budget 2014 15

•Télécharger en tant que PPTX, PDF•

2 j'aime•3,056 vues

Tax revenue Projection under each head iin percentage for financial year 2014-15, Interim Budget

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

En vedette (20)

Plus de Dr. Sanjay Sawant Dessai

Plus de Dr. Sanjay Sawant Dessai (17)

Dernier

Dernier (20)

Revenue tax collection , Interim budget 2014 15

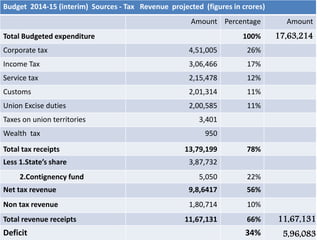

- 1. Budget 2014-15 (interim) Sources - Tax Revenue projected (figures in crores) Amount Percentage Amount Total Budgeted expenditure 100% 17,63,214 Corporate tax 4,51,005 26% Income Tax 3,06,466 17% Service tax 2,15,478 12% Customs 2,01,314 11% Union Excise duties 2,00,585 11% Taxes on union territories 3,401 Wealth tax 950 Total tax receipts 13,79,199 78% Less 1.State’s share 3,87,732 2.Contignency fund 5,050 22% Net tax revenue 9,8,6417 56% Non tax revenue 1,80,714 10% Total revenue receipts 11,67,131 66% 11,67,131 Deficit 34% 5,96,083