Recommandé

Recommandé

Contenu connexe

Similaire à The Case of Tanzanite

Similaire à The Case of Tanzanite (12)

Dernier

Dernier (20)

The Case of Tanzanite

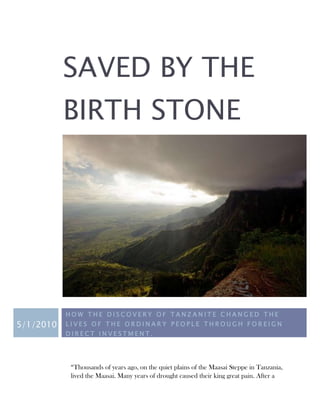

- 1. SAVED BY THE BIRTH STONE HOW THE DISCOVERY OF TANZANITE CHANGED THE 5/1/2010 LIVES OF THE ORDINARY PEOPLE THROUGH FOREIGN DIRECT INVESTMENT. “Thousands of years ago, on the quiet plains of the Maasai Steppe in Tanzania, lived the Maasai. Many years of drought caused their king great pain. After a

- 2. Saved by the birth stone mysterious dream, he announced that he would journey to the misty summit of Mount Kilimanjaro, home of the gods. He told his beloved daughter, Ayanda, to care for the people until his return. Heavy of heart, Ayanda watched her father walk towards the distant slopes. Ayanda cared for her people and they, in turn, adored their beautiful queen. One hot and dry night, Ayanda too was visited by a dream. Her father took her by the hand and guided her to the edge of a vast lake of violet- blue depths. Ayanda understood that her father would never return but that he was showing her the means to save their people. Ayanda set off to find the life-giving waters. For weeks she travelled arid lands. Finally she reached the foothill of Kilimanjaro where nestled in a shallow valley was the promised lake. Ayanda leaned over to drink from the waters: her father’s image shone up at her from the crystal blue- violet depths. She reached to touch his face, but it disappeared amongst a swirl of ripples. On lifting her hand from the water, a small drop fell into her lap. The drop magically transformed into a beautiful, faceted gem the deep violet-blue of the lake. And the heavens broke out with a cool, sweet rain, bringing life to her land. Centuries later, the Maasai people were again struck with poverty. Remembering the legend of Queen Ayanda, the village elders decided to make the journey to Ayanda’s fabled lake. What they found was not the blue-violet waters that legend spoke of, but a deposit of precious blue-violet gem. The gem was named Tanzanite in honor of the Tanzanian people.” Despite the hope that people engrained in the stone, it seems like Tanzanite has failed to save them from the vicious circles of poverty. On a hot airy night in November, Dr. Peter Kafumu, the Minister of Energy and Minerals, was looking out over the endless panoramas of green fields that his country was so rich in, as he remembered the myth that his grandfather told him when he was a little boy - with hopes that he too, some day, could save his people from poverty. Dr. Kafumu was sipping a popular local liquor konyagi, wondering if he should have agreed with President Kikwete three years ago on the question of the mining contracts. President Kikwete proposed to increase tax royalties from the mining companies in order to boost tax revenue. However, Dr. Kafumu believed in trade liberalization and the attraction of foreign dirext investment (FDI), which would be stymieed if the royalties to mining companies were to be increased. Page 1

- 3. Saved by the birth stone Now his ideas were questioned in High Court by a constitutional petition that was filed in November 2009 seeking to have all the mining contracts entered into by the government without Parliament's approval declared null and void. The petitioners believe that the government is giving away their natural resources to mining companies without getting a fair compensation for the people from taxes and royalties. Dr. Kafumu is believed to have sole power in signing these mining contracts which include huge tax concessions. (Ayanda tanzanite) Page 2

- 4. Saved by the birth stone Contents INTRODUCTION ......................................................................................... 4 1. TANZANITE .......................................................................................... 6 2. PORTER’S DIAMOND ............................................................................. 7 2.1. Factor conditions ................................................................................ 9 Human Labor .......................................................................................... 10 Material Resources ................................................................................. 11 2.2 Demand Conditions ............................................................................ 12 2.3. Related industries ............................................................................. 13 2.4. Firm Strategy, Structure and Rivalry .................................................. 16 3. A 3-PARTY RELATIONSHIP BETWEEN THE GOVERNMENT, FOREIGN INVESTORS AND SMALL-SCALE MINERS .............................................................................. 26 3.1. Mining companies and community development ............................... 30 3.2. Tax initiatives .................................................................................... 31 CONCLUSION ........................................................................................... 34 Update as of April 24, 2010 from Reuters ................................................ 34 APPENDICES ............................................................................................. 37 Table 1. World Tanzanite Production ........................................................ 37 Table 2. Production of Tanzanite by Tanzanite One .................................. 37 Table 3. Ease of doing business in Tanzania ............................................ 38 Summary of Indicators .............................................................................. 39 Table 4. Economic contributions by mining companies – general economic indicators ................................................................................................................. 41 REFERENCES ............................................................................................. 42 Page 3

- 5. Saved by the birth stone Saved by the birth stone THE AIM OF THIS CASE IS TO DETERMINE WHO IS BENEFITING FROM THIS CONTROVERSIAL INDUSTRY AND WHAT IMPACT THE MINING OF A RARE TANZANITE HAS ON THE ECONOMY OF TANZANIA. INTRODUCTION The theme of this paper is determine if a country can transform a monopoly on a natural resource into a competitive industry and can effectively implement FDI policies to benefit the growth of the economy as well as the development of the community and infrastructure. The aim of the research was to show that despite the efforts to make a country competitive for foreign investors and attract FDI, it is vital to make a distinction in the impact of the FDI on the economic, social and political factors. It is important to have a stable and reliable political framework that allows the country to distribute the accumulated wealth from foreign sources fairly; otherwise, the benefit of FDI, without a direct impact on the economy and lives of the local people, is reduced to profits shared among the elites of the government and the CEO‟s of major companies. The paper is organized in three chapters that discuss the history of Tanzanite against the backdrop of the Porter‟s diamond and cluster models, showing what factors in the industry fail to support the whole system. In the last chapter the intertwined relationship between the government, the local miners and the foreign investors is shown. Looking at the economical factors, it is possible to say at a first glance that Tanzania has all the resources to transform its unique resource into a “goldmine”. However, looking into the political situation reveals that the situation leaves much improvement to be desired. Page 4

- 6. Saved by the birth stone Before going into the discussion of Tanzania, an insight into a neighboring country is essential to understanding what could have been done differently to achieve a national competitive advantage. It is useful to present the example of Botswana which as a poor country with rich natural resources has achieved great economic growth and stability. It currently ranks as #3 on the African Competitiveness Report in 2009 only after Tunisia and South Africa. At a first glance Botswana could fall into the category of a “resource curse” country. Nevertheless, it has reached a success rate thanks to its management of these precious resources, rather than their exploitation. From 2004 to 2005 the economy of Botswana grew by 8.3% benefiting largely from the mining industry which represents 35% of GDP and 80% of exports. Health facilities, education, clean water and electricity are available to over 90 percent of the population; and literacy rates, which stood at 50 percent in the early 1970s, are over 80 percent today. (SANGA, 2006/2007) The new administration that came in 1995 performed a political miracle – they actually implemented the policies that they promised: low and stable taxes to mining companies, liberalized trade, increased personal freedom, and low marginal income tax rates (to deter tax evasion and corruption). The growth was further encouraged by the properly ran institutions and good governance – two common sense attributes of a successful government. Unfortunately, these melancholic dreams of a better future did not seem to reach the hearts of the Tanzania officials who failed to follow the Botswana experience in a more lucrative situation. After all, Botswana has achieved a De-Beers like success with diamonds, which are found in other parts of the world. Tanzania on the other hand is the only source of tanzanite, revealing how far the “resource curse” can go. Despite all the accusation, they tried to make it happen. After becoming the United Republic of Tanzania in 1964, the government started promoting the inflows of foreign direct investment (FDI) through an attractive tax structure and tariffs, protecting companies from nationalization and expropriation, offering investment opportunities in the public sector. In 1986 the Economic Page 5

- 7. Saved by the birth stone Recovery program focused on macroeconomic stabilization and trade liberalization. By 1999, virtually all export restrictions had been eliminated. The rationalization of import tariff rates in 1998 reduced it from 35% to 23% (A case study of Tanzania: impact of FDI on developing economies, 2003). These measures have undoubtedly attracted foreign investors; however, the price that was paid for their benevolence seems to be too high. Today Tanzania is still one of the poorest countries in the world with per capita income estimated at $US440 in 2008 (World Bank, 2008). 1. TANZANITE Tanzanite is a deep blue-violet gemstone discovered in 1967 in the Merelani Hills near Mount Kilimanjaro and 70km south-east of Arusha. Merelani is the only source of tanzanite in the world with a supply projected to be 15-20 years depending on the methods and pace of extraction. Geologists predict that the chances of finding another deposit are 1: 100,000 (Tanzanite One). The stone saw the light of day when a geologist‟s father Hyman Saul showed the stones in New York to Henry B. Platt, Vice President of Tiffany‟s, who decided to market the stone to the rest of the world. The mineralogical name of the stone, zoisite, sounded much like “suicide,” hence Mr. Platt christened the stone after the country of origin. The largest crystal of gem HTTPS://WWW.CIA.GOV/LIBRARY/PUBLICATIONS/THE- WORLD-FACTBOOK/GEOS/TZ.HTML tanzanite known to survive measures 7 by 8 by 22 cm and weighs more the 3 kg (16,839 carats). It was found in July 2005 in Block C. The Tanzanite One Company has decided to retain the crystal in its uncut state, as an exhibit specimen, though it is currently kept in vault because of its high value (Vincent Pardieu and Richard W. Hughes, 2008). Page 6

- 8. Saved by the birth stone After a growing interest for the rare stone, the government of Tanzania decided to divide the 2 by 8 sq km of deposit into four areas, named blocks – A, B, C, and D. The government attempted to profit from the booming sector by nationalizing the mines in 1972 in a State Mining Corporation until 1983. The nationalized mine was poorly management, had haphazard open-pit mining and led the State to abandon the mines in 1986. In 1990 the government decided to clear the area and license it to foreign investors and local miners. The most suitable area – Block C – was awarded to JABE, a British –Australian company (later Afgem and Tanzanite One). The other Blocks were licensed to local businessmen as well as small-scale miners who are represented by the Arusha Regional Miners Association (AREMA). Signs of enrichment started to emerge: the wealth of the lucky Merelani brokers is invested in local hotels, bars and clubs. Brand new Toyota Land Cruisers and off- road motorcycles maneuver on the treacherous dirt roads that cut through town. Satellite dishes adorn hastily built homes. Cell phone towers can be seen in town and it is even possible to gain internet access through the phone. But most people live desperate lives. This is a town of lawlessness. There is no running water. Those who can‟t afford bottled water take it from shallow wells, contracting diseases like typhoid and cholera. 60% of the people may be HIV infected. A deeper look at the country‟s industry and economy will reveal the reason for such disparity in the distribution of the tanzanite profits. In the following chapter, Michael Porter‟s Diamond and Cluster Frameworks are used, as well as the value chain, to see if discovery of tanzanite could create a competitive advantage given all the factors and conditions. 2. PORTER’S DIAMOND Michael Porter (Porter, 1998) argues that there are inherent factors in each nation that create the foundation for creating a competitive advantage. In this case, the limitation of the framework is that essentially there is no competition since one of Page 7

- 9. Saved by the birth stone the foreign companies dominates the process. It will be explained further how the government could assist in changing this situation. This sector explores competitiveness dynamics that could be adjusted with the help of the government. The national playing field is an important determinant in the competitiveness of the country, as determined by Porter. His diamond framework will be used to show if the government of Tanzania has achieved a competitive advantage in an industry where it inherited a monopoly over the rare gemstone. Each of the factors in the quadrants determines the dynamics of competitiveness. As can be seen from the diagram, the role of the government in this framework should be that of a facilitator and motivator for companies to increase their advantages through fair competition, by enforcing anti-trust laws and promoting small and medium-size. The following sub-chapters will look at the state of these conditions in Tanzania and their impact on the advancement of possible competition. Page 8

- 10. Saved by the birth stone 2.1. Factor conditions Porter argues that inherited factors, such as natural resources and unskilled labor do not contribute to a competitive advantage because any other firm can obtain them. A competitive advantage is obtained when the firm creates a product, service or relationships with suppliers and/or buyers as well as the government and other agencies that is difficult to imitate. In the same manner, the country must possess an attractive infrastructure, skilled human capital, political and economic stability to be attractive to foreign investors. There are factors that are not inherited and can be changed, such as the macroeconomic stability, political situation and socio-cultural factors. Tanzania is free of ideological confrontations, ethnic problems and labor disputes; it is considered a center of economic and political stability in Sub Saharan Africa. As a result of prudent fiscal and monetary policy, the inflation rate has been lowered to sustainable level of 12.5% as of November, 2009 (National Bureau of Statistics, 2009). The government has increased revenue streams and reduced spending, which enables it to grow the current account and increase the level of domestic investment spending and the growth of economy. Institutional support is readily available from the Tanzania Investment Center. Mining and tourism are the main recipients of FDI and are tipped to become growth sectors. Since this industry is labor intensive at the outset, Tanzania has great potential with its low cost of labor and natural resources. However, companies need a developed infrastructure and a reliable economic and political background to perform operations. Besides, after around 200 meters, it is almost impossible to dig by hand, and technology is needed to continue exploration. At this point only the foreign companies have the power to obtain the financing for this type of technology and deliver knowledge and skills for its use. The rarity of tanzanite makes it an attractive investment opportunity, as well as a source of government revenue. If the proper education on the rarity of this stone is Page 9

- 11. Saved by the birth stone performed, the government may stand in a position of power as it possesses a limited desirable resource. However, from the point of view of the multinational companies (MNC‟s), tanzanite may be just a mineral that may be compared to all the other investments in the mining industry. It is in the best interest of the government of Tanzania to present it as a rare opportunity and provide ample resources for foreign investors. Human Labor The labor supply in the mining industry remains a challenge, yet Tanzania is one of the poorest countries in the world, and people travel from other regions to work in the mines. The Merelani area alone provides around 75,000 people with an estimated 15,000 mine workers (MAGNE BRÅTVEIT, 2002). The Maasai people who are the indigenous tribe in the area look down on the work of the miners and prefer not to engage in such business. However, workers from other cities (where there are few other job opportunities) flow into the area in hopes of finding a fortune. 60% of the population lives on less than $2 a day and an average person lives on $280 a year (USAID, 2005). Mining is a tedious process involving manual labor, which often attracts uneducated and unskilled labor. The people also move around a lot in search of better opportunities. Those workers who switch to mining are usually involved in agriculture and cattle farming. If they find no success in the gemstone business, they are likely to go back to their previous livelihoods. Therefore, the level of commitment is low on the side of the workers. Following successful negotiations between the company and the union representatives and government, non-core employees are paid sector rates as opposed to mining sector rates. The average pay for mineworkers in Tanzania is US$128 to US$240 a month. This is a high salary compared to other jobs, in areas where few other jobs are available. However, by contrast, Barrick‟s chief executive, Greg Wilkins, received US$9.4 million in 2006, including basic salary, bonus and stock options. It would take an average Tanzanian miner over 500 years to make this amount of money (Lissu, 2008). Page 10

- 12. Saved by the birth stone The knowledge capital related to this industry is low since it attracts a certain type of people, usually poor and without formal education. However, the labor force is trainable and the government has made a long-term commitment to develop a pool of well-trained and educated specialists. The government recognizes that if they don‟t invest in education now, they will have a gap of knowledge in this generation, putting them further in line for attracting FDI. This issue if not dealt with will affect the future human resource of a nation because they are getting a generation of children who are missing out on education. The outcome will be that they will have a gap or a generation of people who are not educated, who don‟t have any skills to contribute to the human development. Women sell food at the mines, but their income from the business is not enough to support the family. This dire situation forces women to subsidize their income through prostitution. Children are also compelled into sex work in order to survive. Sub-Saharan Africa has the highest proportion of child laborers of any region in the world. Unfortunately, Tanzania is not an exception. Parents encourage their children to work at the mines because there are no schools near the diggings. Children are called “snakes” for their ability to move lithely with dynamite through the narrow mine pits. Every day, 4000 child miners between the ages of 8 and 14 risk their lives in poorly constructed mine shafts for barely a meal a day (TANZANIA Gem Slave, 2006). The government doesn‟t want kids to work in mines. It is the government‟s wish that they go to school, but there are not enough schools for the kids. Material Resources The capital resources are also scarce; it is difficult for an individual to obtain financing if he were to start a business in mining a pit. Most of the men get the proceeds from the sale of their cattle for the initial investment in the mines. Claim titles are cheap ($18 per year), while the investment to start production is extremely high. One needs $91,743 to buy a compressor, water pump, explosives and other equipment. A common share system in small scale mining is that the sponsor gets Page 11

- 13. Saved by the birth stone 40%, the claim holder 30%, the person owning the compressor 20%, and the workers as a group 10%. According to the Zonal Mines office there are 600 claim holders in the northern zone, of which 200 are active at any time. AREMA1 operates with a number of 700 mines in Merelani alone. Each of the active claim holders has 25-60 workers, which means there are 12,500 small scale miners in Merelani (Lange, CMI Report R 2006: 11 54 p. ). Nevertheless, the development of the industry is bringing urbanization features to the locals. The National Micro-Finance Bank (NMB) plans to install an ATM at Merelani Township in Simanjiro district in a bid to bring financial services closer to people. The present NMB decision follows a special request from Merelani residents through a Tanzanite dealer Laizer Kurian. The township has no bank services and instead people are forced to travel long distances to t Arusha or to Boma Ng‟ombe in Hai. 2.2 Demand Conditions According to the World Bank, the population of Tanzania in 2008 is around 42.5 million people with a growth rate of 2.9% per year. A population that can barely afford food and water will hardly bother to get jewelry. The local demand is supposed to drive the innovation and product development; the more educated and demanding the consumers are, the more the local companies will try to please the customer by offering better quality product or service. In the case of tanzanite, the local demand is obviously low. The only buyer‟s market that exists is that of the local dealers and brokers that buy directly from the mine in the village or in town and later resell abroad. The miners are uneducated about the prices that transfer abroad and sell the stone at a fraction of what it is worth to the end consumer. Raw tanzanite represents one twentieth of the final value of the stone after cutting and polishing. In 2008 the prices of raw tanzanite were $9-14 per carat 1 Arusha Regional Miners Association Page 12

- 14. Saved by the birth stone compared to the price of a cut and polished stone selling at $250-500 (Kilimba, 2008). The external market is represented by Jaipur, India, where 80-90% of the stone goes for processing; therefore most of the value accrues overseas. The U.S., South Africa and Thailand are the main trading markets for tanzanite, accounting for about 70% and Europe 5% (Selasini, 2009). 2.3. Related industries Related industries are represented in the cluster model where support one another in an area which has reached a certain level of integration in cluster development. Mining is yet an indigenous industry which is self-sustainable. Before the foreign companies, artisanal miners used only their hands and a few simple tools to dig for the stones. Therefore, it is difficult in this industry to form clusters were the other companies would support the mining. Of course transportation, food, telephone, and hotel industries have grown since the coming of the big multinational companies. Page 13

- 15. Saved by the birth stone The value chain helps to determine if the industry is positioned to become a cluster. The value chain follows the process of creation of a product or service to its final consumption or use. If the value chain participants are closely intertwined, yet independent, they can drive competition. If the buyers and suppliers of the company are separate entities, a process of development is sustained. However, if the company is vertically integrated, it creates a lot of value for the company, but leaves no room for rivals to develop a competitive environment. Page 14

- 16. Saved by the birth stone The value chain of mining consists of exploration, mining, ore crushing and processing, transportation, dealers and brokers, jewelry design, wholesale and retail. Unfortunately most of these value adding activities are outsourced and are unable to form a cluster. Tanzania is left to do the extractive work. However, in June 2003, the government banned the export of unprocessed tanzanite over 1 carat to India. It was to spur the local lapidary work and processing facilities, recouping the value for the local people. Jaipur in India has one third of its exports from tanzanite (Kilimba, 2008). Tanzanite One, the largest mining company of tanzanite, has set up 6 cutting stations in Merelani and has hired both men and women to do this work. The company has trained the cutters themselves, both locally and in South Africa, planning to expand the tanzanite facility to 25 cutting stations and to invest even more in training. There is only one other company which exports stones. The owner, Sailesh Pandit, says employment would be secured for 3000 people if all stones were Page 15

- 17. Saved by the birth stone processed in Tanzania (Lange, CMI Report R 2006: 11 54 p. ). Besides, local processing doesn‟t mean that the quality goes down. The mining sector falls under the jurisdiction of the Ministry of Energy and Mining. There is also a Chamber of Mining that oversees the development of the sector and serves the interests of large, small and artisanal miners in collaboration with Tanzania Miners Development Association (TAMIDA). Mining, research and exploration center located in Dodoma serves as a referral center for all technological studies and related research. Foreign investors partnered with local investors are the most favored for licensing purposes. This should increase the demand for local processing of the gemstone. Because of the fragmented nature of operations every business tries to do all things for themselves: bulk supplies procurement from long distances (mining equipment and food), health services, transportation, technological and social infrastructure development, small scale lapidary work, entrepreneurial development and employee capacity building. The result is uncoordinated growth and development of the mining area. Coordination of existing fragmented service providers and the associations into a solid network that is facilitative to the various suppliers would strengthen the cluster. More investment in lapidary and jewelry manufacture and capacity building is needed for relevant local skills. The whole industry would become more competitive if the following issues would be addressed: artisanal miners don‟t have access to technology, socio-economic development efforts are uncoordinated, the lapidary development is low, small scale miners suffer from dominant buyers of raw and polished tanzanite and have little bargaining capacity, low multiplier/spillover effects of mining to related economic activities. 2.4. Firm Strategy, Structure and Rivalry Page 16

- 18. Saved by the birth stone The main players of the industry can be divided into local miners and foreign companies. The main foreign player is Tanzanite One, which is South-African, previously under the name of Afgem. Tanzanite One occupies Block C, the other blocks are destined to be for the local miners, who are represented by two associations AREMA and MAREMA. Main Players 1. Tanzanite One Company Ltd The following three players are subsidiaries of the main company and represent a full forward integration. 2. Tanzanite Trading Ltd 3. Tanzanite Marketing 4. Tanzanite Foundation 5. Arusha Region Miners Association (B and D) 6. Manyara Region Miners Association (B and D) 7. Tanzanite Africa Ltd (D) The tanzanite resource strikes along a length of seven kilometers and is divided into four blocks. Tanzanite One in Block C undertakes large scale mining; medium scale mining is undertaken by Kilimanjaro Mining in Block A and Tanzanite Africa in Block D. The company‟s neighboring Blocks B and D are mined largely by artisanal and small scale miners. This poses a challenge for Tanzanite One - the artisanal miners continue mining into Tanzanite One‟s designated license area. This continues to be a major challenge to the operation with ongoing illegal mining activities continuing to take place from both Blocks B and D. Constant communication with officials from the Zonal Mines Office and the Ministry of Energy and Minerals yields results from time to time, but the problem continues. The foreign investors are more welcome by the government since they bring new technology, skills, spillover effects (such as employee training, introduction of new techniques, management know-how, which are generally more beneficial in the manufacturing sector) as well as safe working conditions and community Page 17

- 19. Saved by the birth stone development projects. On the other side, the local miners face many challenges, as their production is dispersed and they are disorganized. Due to unsafe mining practices, they have suffered several accidents in the mines. Although they are supposed to dig straight down on the 150 by 150 feet plot that they are assigned, nobody follows the rules (Lovgren, 2001). The mines are in the form of “Swiss cheese”. The government officials seem to close their eyes on the tense relationships between multinational companies and artisanal miners. The controversy around the linkage of tanzanite to Al-Qaeda funding has been groundless. Nevertheless, it seems like the whole aim of the story that was published in the Wall Street Journal by Daniel Pearl and Robert Block on November 16, 2001 was to show that the artisanal miners were involved in the smuggling of the stone and that anything bought from them could be of dubious origin. The story created quite a stir and several articles that appeared shortly after never failed to mention that despite the link of tanzanite to terrorism funding, there is only one company that tracks the stone from the mining pit to the hands of the consumer – Tanzanite One. It has been mentioned that the journalist of the article visited the Tanzanite One shortly before the issue, perhaps going over the story. Even though Tanzanite One would have suffered as the sale price of tanzanite dropped 50%, it is possible to consider that they implemented a long-term strategy, where they would draw the attention to the dark link of tanzanite to terrorism, and then carefully isolate themselves from this picture. Thus, in the eyes of the consumers, Tanzanite One would be the only viable supplier of the rare gemstone. Isn‟t it a perfect recipe for a monopoly? Of course, the artisanal miners were furious with the attempt of Tanzanite One to push them out of the market. The story attracted attention across the world and was a threat to the reputation of the stone, as many jewelers dropped the sale of tanzanite after the article was published. Shortly after the investigation, on February 9, 2002 in Tucson, Arizona, the Government of Tanzania and all trade associations representing the full Page 18

- 20. Saved by the birth stone international scope of tanzanite miners, gemstone dealers, manufacturers, suppliers and the retail jewelry industry in the United States, which accounts for 80% of the world market for tanzanite, met and agreed to eliminate concerns about the tanzanite trade, its alleged connection to funding terrorism, and to restore confidence in tanzanite. The Protocols were to designate the mining area as Merelani Controlled Area and develop plans to tighten security around the mine enclave and strengthen rules governing the exports. A high-level US delegation that same year verified that the government was taking substantive steps to comply with the agreement. The tangible effects are the following: By 2007 a 10 foot fence was built encircling the entire 12km² mining enclave. Police and guard posts were built. Systems of written warranties and secure packaging were in place and observed by legitimate exporters. Smuggling dried up to 10% of its former volume. The use of child labor has decreased dramatically. Thousands of miners and laborers acquired official ID passes (Schroeder, 2010). On balance, many of the leaks, facilitating illegal trading, were plugged. Tanzanite One met the requirements before they were set in place. They possessed a self-contained mining compound with elaborate security measures to guard against theft by their own employees and outsiders, they moved their gems through a vertically integrated system that funneled rough stones directly to processors, wholesalers and jewelers. In 2009 Tanzanite task force was formed to carry out the Tanzanite Protocols. A chain of warranties would accompany each tanzanite shipment from the mine all the way to the retail store, stating that “tanzanite herein invoiced was mined in Tanzania and has been traded through legitimate sources.” COMPANY’S STRATEGY Tanzanite One represents the only large foreign company in the Merelani mines and has developed a strategy that helps it stay that way. Tanzanite One is the largest Page 19

- 21. Saved by the birth stone and most scientifically advanced miner and supplier of rough tanzanite, a unique position that affords it the opportunity to support and influence the entire channel, from mine to market, ensuring that maximum stakeholder value is achieved at each stage of the process. The mine is considered a modern, low-cost operation and boasts an exemplary safety record. It applies international best practice in the design of its employment, social and environmental policies. Processing and sorting take place on site within purpose-built infrastructure and facilities. A conservative estimate of Tanzanite One's resource, and as published at the time of listing on AIM in 2004, would place the figure at 63-83 million carats. At an average price of $ 12 per carat in the rough, this represents an estimated $756 million to $996 million in the ground (Tanzanite One, 2008). It has vertically integrated itself into trading, marketing and building awareness of tanzanite through Tanzanite Trading, Tanzanite Marketing and Tanzanite Foundation. Their strategy is similar to the De-Beers cartel in the diamond industry which controlled the prices and positioned diamonds as the stone for a life-time which should never be sold, thus limiting the supply. They were the ones who came up with the marketing slogan “A diamond is forever” and made it the obligatory engagement ring, pouring in millions of dollars in marketing to strengthen the spell. In the same manner, the Tanzanite Foundation, a subsidiary of Tanzanite One, came up with a similar strategy. The next section tells the story: “Tanzanite, the birthstone, is the gift given on the birth of a child. Fittingly this theme draws on the inspiration that we are all born to something special. The promise of a person begins with the earliest moments of life and every tradition cherishes and celebrates a child being born, the miracle of birth, and the gift of life. From the heart of Africa comes a powerful tradition. Maasai women who have had the Page 20

- 22. Saved by the birth stone honor of giving birth to a baby wear vibrant blue beads and adornments to bestow upon the child a healthy and positive life, whilst setting themselves apart as creators of new life. This custom, protected and preserved by the proud Maasai through the generations, is now celebrated in a modern tradition: the giving of tanzanite on the birth of a baby. Every culture all over the world cherishes and celebrates the miracle of new life. Tanzanite, a precious heirloom to treasure through the generations, is the perfect gift to give on the occasion of birth. It uniquely symbolizes new beginnings, and pays tribute to those who have shown the greatest of loves by becoming a parent.” (Tanzanite One) With the help of this “spell” Tanzanite One controls 35% of tanzanite (Larenaudie, 2007). Naturally, due to the fact that they have the rights to Block C which is considered the most productive part of the mine, as well thanks to the company‟s efforts to be everything from the supplier to the distributor and the certifier. Production for the year 2008 totaled 2.2 million carats, a significant 29% increase over 2007, recovered from 42.3 thousand tonnes. This was also a result of a combination of improved mining methods and increased security presence through the upgrading of security systems. The company‟s ability to increase production to 3 million carats per annum remains unchanged and it will be fully exploited once the markets return to normality. In August 2008, Tanzanite One opened The Tanzanite Experience (TTE), a museum in Arusha that showcases the history of tanzanite through a series of visual and interactive exhibitions whilst affording visitors the unique opportunity to purchase cut and polished tanzanite directly from the world‟s only known source. TTE targets approximately 600,000 tourists who pass through the town annually. Marketing is geared towards safari companies and tour operators in an effort to include a visit to this facility on their itineraries (Tanzanite One, 2008). In a nutshell Tanzanite One is carrying out a massive strategy of dominating the market and letting the whole world know about tanzanite. Page 21

- 23. Saved by the birth stone The following structure of the Tanzanite One Company shows how the company controls the supply, marketing, grading, certification and community projects to further spread the monopolistic influence. Tanzanite One Trading Tanzanite One Trading is a Group subsidiary based in Arusha that purchases rough tanzanite from smaller miners, brokers and dealers; cementing its position as one of if not the strongest tanzanite buying operation in Tanzania. Tanzanite One Trading operates under the guidelines of the Tucson Tanzanite Protocols. Tanzanite One Trading (T1T) Relationships have been developed with all the prominent. Processing and selling is controlled by Tanzanite Trading; it buys from small scale miners, which accounts for 15% of output (Tanzanite One ). In support of more stability in terms of rough prices, Tanzanite One Trading pays a small premium. This strategy has been well received in the local market and as a result, Tanzanite One Trading has become a market leader in procuring high quality material. Tanzanite One Marketing Tanzanite One Marketing is the Group‟s marketing and sales arm for rough tanzanite. The subsidiary consolidates the available mined and traded rough tanzanite and is able to add further value by applying a proprietary rough tanzanite grading system and preparing parcels of material specifically suited to the individual business needs of each of its eight “sightholders”. This is achieved through the Preferred Supply Strategy, which is a world first in the colored gemstone industry, aimed to grow the global market for tanzanite through strategic collaborative relationships with exclusive customers, „Sightholders', selected from the world's leading gemstone houses and jewelry manufacturers. Page 22

- 24. Saved by the birth stone Sightholders have been chosen for their focus on tanzanite, ability to make a long- term commitment, distribution capabilities, understanding of the need for vertical integration and most importantly their operational standards of integrity. Their belief in and commitment to supporting an ethical route of the tanzanite market has also been a prerequisite for their appointment. Tanzanite One has initially appointed eight Sightholders, with plans to increase this number in the medium term. These initial eights are listed below (Tanzanite One ): • AG Color Inc • Colorjewels • Intercolor • Paul Wild • KL Tambi • Rare Multicolor Gems • STS Jewels Inc. • Tanzanite International The Tanzanite Foundation The Tanzanite Foundation is a non-profit, industry-supported organization that strives to develop the tanzanite industry by growing demand and creating value for all stakeholders in the tanzanite value chain. By striving to standardize stakeholder conduct and communication, the Tanzanite Foundation aims to uphold an ethical route to market in accordance with the Tanzanite Tucson Protocols and invests in meaningful and sustainable projects developed in configuration with the local communities situated at tanzanite‟s source. Tanzanite One is a founding member and primary fund provider of the Tanzanite Foundation. In order to contribute positively Page 23

- 25. Saved by the birth stone to the community and area surrounding the tanzanite mines, the Tanzanite Foundation™ is committed to making a meaningful and sustainable difference to the social, economic and environmental uplift in the area. Projects undertaken to date include: • the construction of a 400m² Community Centre for the residents of Nasinyai, the village bordering the tanzanite mining area • the renovation and installation of electricity to the Nasinyai Medical-Clinic • the upgrading and maintenance to the road leading to the tanzanite mining area • active participation in the establishment of the Merelani Controlled Area. In compliance with the Tucson Tanzanite Protocols the Tanzanite Foundation™ provided funding and support for the establishment of a satellite police station in the mining area and donated a police vehicle to local authorities • the provision of water to over 2,000 villagers and 4,500 head of cattle on a daily basis in the severely drought stricken region surrounding the tanzanite mining area • the refurbishment and extensive expansion of the Nasinyai Primary School, which has seen school attendance quadruple to a current figure of 432 enrolled students • in partnership with the Nasinyai community and World Vision (an international aid Christian humanitarian organization), the construction of Nasinyai Secondary School • the development and initiation of SMAP (Small Mines Assistance Program). SMAP provides geological, mining, survey, safety, logistical, operational and other guidance and support to small mines with the aim of building and developing the entire tanzanite mining industry and sound stakeholder relations • mitigation of acid mine drainage by appropriate design of waste rock and tailings disposal systems and monitoring of water quality. Regular water analysis indicates that Tanzanite One is well within the recommended pH levels • the donation of tailings to local communities, which also operates as a Page 24

- 26. Saved by the birth stone community support project. Tailings have a recognized and measured tanzanite content which is uneconomical for Tanzanite One to extract. Local communities extract this tanzanite, which is generally sold back to Tanzanite One Trading. The remaining tailings are used as building material. This system reduces waste and encourages economic activity • rendering old mine workings safe, and continuously monitoring the same; closing numerous old mine workings on Tanzanite One's property and in common areas around the mining license that were deemed safety hazards. (Tanzanite One) Tanzanite One secured a position where it holds the keys to all the steps in the process. By integrating forward and backward, the company is able to control the process in a De-Beers style, managing the supply and directing the price, which has already gone upward in the past decades. Grading and Certification The Tanzanite Foundation‟s Tanzanite Quality Scale™ is the first internationally recognized tanzanite-specific grading system. Developed in collaboration with leading gemological laboratories, the Tanzanite Quality Scale™ is based on 4Cs criteria, grading tanzanite quality based on Color, Clarity, Cut and Carat weight. A fifth “C” stands for Confidence, and is the assurance that tanzanite accompanied with a Tanzanite Quality Scale™ certificate is genuine, rare and precious (Tanzanite One, 2008). Tanzanite One has benefited from the controversy around the Al-Qaeda link, since it promoted the certification that accompanies every stone from their mine as a guarantee against the “illegitimate” stones. As can be seen from this previous analysis and the strategy of the company, the industry does not promote competition, since one giant corporation is trying to push out all the small-scale miners. Besides, the latter don‟t have the technique or resources to drive innovation and be competitive. Tanzanite One had the resources to Page 25

- 27. Saved by the birth stone drive the marketing campaign that created the demand for tanzanite which will have a stronger effect closer to the “extinction” of the stone. The role of the government is an important factor in the facilitation of a country‟s competitiveness, and in the following part, it will become clear why the industry turned out that way. 3. A 3-PARTY RELATIONSHIP BETWEEN THE GOVERNMENT, FOREIGN INVESTORS AND SMALL-SCALE MINERS The government of Tanzania has carried out successful economic policies and structural reforms to attract foreign investors. It seems like the industry is not developing in a way that would benefit the local communities. Taking into consideration that the tanzanite reserves will be depleted within a decade or two, if the local community doesn‟t get the development funds from tax revenues, the country will be left without proper infrastructure, human development or a valuable natural resource. Reform of the mining law in 1997 offered attractive fiscal incentives for investors: substantial tax breaks, and lead to a significant and rapid boom according to EIU. Favorable fiscal and legal measures flowing from the Mining Act have acted as a catalyst for FDI. : Tax incentives such as repatriation of profits Special VAT relief Zero import duties for equipment and machinery used during exploration Depreciation allowance of 100% 15% withholding tax for foreign contractors on technical services and management fees. The mineral‟s sector contribution to GDP has risen from 2.0% in 1998 to 3.7% in 2007, and could reach 10% by 2025 (A brief on the mineral sector of Tanzania, 2009). Page 26

- 28. Saved by the birth stone The question at hand is – why invite FDI if the benefits to the people are miniscule? It goes without saying that large mining companies earn huge revenues; hence they should pay enough taxes for the government to raise the standard of living of the people whose resources are being depleted. The following chapter will look at the impediments that stand in the way of this promising industry. Tanzania exports 80% of tanzanite to US. It is a $500 million a year industry although Tanzania gets barely $20 million annually, with the lion‟s share going to Indian and American dealers (Lyimo, 2009). The discrepancy is not only caused by smuggling through Kenya, but the government failing to collect revenue from royalties and taxes. Royalties are paid by commercial companies to the owners of a mineral in return for the right to extract a non renewable source; they are the main income that governments earn from new mining projects in the first few years of operation. International companies can manipulate their tax base to reduce declared profits. In 2003 an independent auditor contracted by the government to examine the accounts of four major gold companies alleged that the country‟s two largest mining companies both over-declared their losses, which reduced their tax liabilities. Companies can manipulate their accounts where the company made profits, but no tax is due. This tax deferral can continue for years, starving the government of their main source of revenue. A 2008 report by the Business & Human Rights Resource Centre estimated that the combined loss to the country over the previous seven years as a result of low royalty rates, unpaid corporation taxes and tax evasion by major gold mines amounted to US$400million (Research and Markets: Tanzania Mining Report Q1 , 2010). Another way a company can avoid paying taxes is by trade mis-invoicing. Companies either under-declare the value of their exports or overstate the prices of their imports. This enables the company to reduce profits. Most mining authorities don‟t have the requisite skills to audit the complex accounts of large MNC‟s. The Page 27

- 29. Saved by the birth stone auditors allege that they were hindered in their work by persistent reluctance of the mining companies to cooperate. When the investment environment was not conducive in Tanzania, the World Bank prompted the government to give the foreign companies major tax concessions. The government agreed to use all means to attract FDI even of dubious quality, knowing that it would hurt the country‟s long-term industrial development (with no revenues to fund its expenditures). It seems that now is the right time for a world organization to provide auditors who would make it clear who‟s making the money in this industry. In October 2006 President Kikwete directed the Minerals and Energy ministry to review mining policies and laws. President Kikwete and Commissioner for Minerals and Energy Dr. Peter Kafumu didn‟t agree with each other on the mining royalties. President Kikwete argument of raising royalties was based on the experience of South Africa, which charged a 12% royalty; and the desire to raise government revenue. Dr. Kafumu chose the side of foreign companies fearing that the increased royalty will shy away new investors into the country. Besides, South Africa is incomparable with Tanzania in terms of infrastructure, human and capital resources. According to Dr. Kafumu, miners in Tanzania have to cover operational costs that are around 60 percent of the total profit they generate. Out of this 60 percent, 20 percent is spent on taxes and other levies. This means miners are left with 40 percent and they still have to pay a further three percent as royalty. This leaves the miners with 37 percent and out of this, according to Dr. Kafumu investors have to service bank loans at 12 percent and are left with 25 percent after-tax profit from where 30 percent in corporate tax is derived. (Jomo, 2007) However, Tanzania is becoming a more competitive destination due to good government policies (Bekefi, 2006). It would be wise if the royalty was changed for already established companies, since their extensive investment would prevent them from leaving. These exemptions should only apply to new companies; however the ones that are in place and reluctant to leave should be taxed at a higher rate. Page 28

- 30. Saved by the birth stone Companies argue that they need these tax concessions because mining is a high risk industry that requires huge initial outlays of capital in the early years. But high return is accompanied by high risk, and after all – isn‟t this included in the cost of doing business in less developed countries? For some reason companies don‟t take the government as a serious partner, especially in this case when the resource is located only in Tanzania. It would be quite bizarre if a company asked the supplier to give them equipment for free just because exploration sometimes doesn‟t yield any results. Nevertheless, they approach the government of the resource in this manner. Of course it is important to hear both sides and come to a compromise royalty fee. However, in this case it appears that the fee is not the problem, the major leak is in tax revenue collection. African governments are foregoing millions of dollars in revenue, because they failed to collect significant budget revenue from mining, despite higher production and prices, for two main reasons: excessive tax concessions to mining companies, and aggressive tax avoidance by mining companies, primarily by insisting on tax breaks in secret mining contracts. The main beneficiaries of the mining boom are a handful of African political elites, the shareholders of mining companies, the engineering, construction and management consultant firms servicing the global mining industry, and the financial institutions backing these ventures. The question is not whether to increase taxes or royalties but how to collect them and make sure that the money is reaching the people. In March 2009 Reuters reported that a group of five grassroots organizations criticized the way the government dealt with mining corporations. “Breaking the curse” said that governments should publish and review all tax subsidies and concessions given to MNC‟s. Revenues lost by secret deals and backroom transactions could be used for fighting poverty. Only one miner in the country - AngloGold Ashanti - had paid corporate income tax by the end of 2008, 10 years after industrial mining began there. Page 29

- 31. Saved by the birth stone Major reforms to the legislation covering the mining sector are expected in the amended Mining Act that was held in parliament in April 2009 include royalties on gemstones to change from 5 to 7%, for cut and polished stones - rising to 3% from zero. The Parliamentary committee advised the government to stop selling shares in mining companies, stating that no mine should be wholly foreign-owned and recommending that the government own a 10% share in all the mining companies (Tanzania Mining Report Q2, 2009). 3.1. Mining companies and community development Mining companies create little forward or backward linkages into the local or national economy that would stimulate more private sector development and job creation. World Bank believes that if multinational companies can commit to sustainable development as part of its bottom line, then the transfer of skills, technology and capital from mining can revolutionize the impact of mining on economic and social development. As can be seen from the example of the Tanzanite Foundation, a company can do a lot for a community that it is based in. But what are the motives that drive a corporation to do good? And is it good from the perspective of the Maasai tribe people who are often evicted from their villages or are deprived of a water source because the company needed the land? Or is it unfair, from the perspective of Milton Friedman (Friedman, 1970), to expect the companies to provide the people with their livelihoods, replacing the duties of the failing government? Instead of improving electricity and transport network, fundamental to the operation of the mining companies in remote areas, governments give them tax breaks instead, hoping that this would compensate for the additional costs of operations. Therefore, Tanzania is falling down a slippery slope. If they don‟t collect taxes and invest in infrastructure and human development, they will not only deprive their people of the basic needs but also loose their competitiveness. Page 30

- 32. Saved by the birth stone Why not attract FDI by advanced infrastructure that is financed from the tax revenue instead of lowering taxes? This in the long term will provide an enhanced benefit to the local communities and increase the flow of FDI. Government needs to improve infrastructure rather than give tax breaks. MNC‟s are more interested in government support rather than that of the community. Their only incentive for involvement in socially-responsible behavior is the pressure of the outside world. Services to communities may be direct, but they are not constant or something that people should rely on. Unfortunately, the tax money doesn‟t reach the communities, and they are happy with what the foreign companies have to offer. The money that does reach the communities is often sporadic and does not usually present the most economically optimal solution. 3.2. Tax initiatives Most African mineral rich countries, whose economies depend heavily on extractive industries, have lower economic growth and human development than those that are not so dependent on these industries. Many believe that revenues from extractive industries serve to heighten corruption. The “resource curse” can be broken once mining tax laws are transparent and equitable, skilled tax authorities are able to collect taxes, and these are distributed through a participatory and transparent budget process. To ensure that the correct amount is collected from mining activity, and that this is spent equitably according to the country‟s agreed national development strategy, civil society organizations and parliaments need to be able to monitor and oversee the collection, allocation and actual spending of budget revenue. Unless there is a legal framework in place that allows civil society organizations, parliamentarians and citizens access to budget and revenue information, and unless there are laws that allow them to hold the government accountable for its fiscal management and expenditure, there is no guarantee that income earned from mining would contribute to development and poverty reduction. There are some positive changes - in 2008 the Tanzanian government announced their intention to join the Extractive Industries Transparency Initiative Page 31

- 33. Saved by the birth stone (EITI) initiative (Extractive Industries Transparency Initiative). EITI requires companies to report publicly the following: 1. Revenue and profit for each concession or license 2. Taxes and fees paid to the state Once communities have information on the revenue transmitted to the government and other structures meant to service them, they will be able to monitor these funds directly, instead of expecting companies to spend more on community services directly. Of course this initiative will have an effect if the people will have the power to question the actions of the mining companies and their relations with the government. The following problems need immediate attention as they are vital for the attraction of FDI. According to the 2009 African Competitiveness Report, the most problematic factors for doing business in Tanzania are: 1. inadequate infrastructure (more than 70% of the firms listed “electricity” as the most serious constraint). 2. inadequately educated work force 3. corruption 4. access to financing. (World Economic Forum, 2009) It is possible to link the third problem as the reason for the first two. Botswana offers a guideline to follow in fighting with the causes of corruption. As a poor country with vast natural resources, it has succeeded due to the following efforts: • Voice and accountability, measured via political process, and also civil liberties and political rights – which indicate an ability to criticize those in authority when it comes to resource extraction issues. • Government effectiveness measured by the quality of public services and the competence of civil servants. Its use of mineral revenue has kept an eye on an implicit self-disciplining rule – the sustainable budget index – any mineral revenue is supposed to finance investment expenditure and ensure spending on education and health – this is in contrast with Tanzania, where all mineral revenues go into general Page 32

- 34. Saved by the birth stone budget. • Natural resource development must involve a long-term relationship with all private parties, while market-friendly policies like price controlled and excessive regulatory burdens are undesirable. Mining lease are 25 vs. 10 years in Tanzania (SANGA, 2006/2007). The government holds 50% of shares in the largest diamond company; and the Ministry of Minerals and Water Resources has direct responsibility for natural resource regulation and management. • Anti-corruption policies are essential to a fair and transparent distribution of resource benefits. If Tanzania wants to replicate this, it should start with good governance policies. Page 33

- 35. Saved by the birth stone CONCLUSION When we look back and think about why Tanzania has not become as competitive as Botswana, it seems that the problem is not in the amount of royalties, macroeconomic factors or fiscal policies. They all trace back to the way the government operates. The success of the tax reforms and revenue distribution is supported by the guarantees of the natural development law. Any successful development is guaranteed through a dialogue of the opposing parties. Truth is born in an argument. Botswana has secured this through civil liberties and rights of the people to question and challenge the actions of the government. Unfortunately, this is absent in Tanzania, and no reforms will help the economy unless the laws are implemented in tax revenue collection and distribution. The problems mentioned in the Competitiveness Report can be eliminated once strict rules are in place directing the use of the government budget. Basically, Tanzania has a monopoly on the rare gemstone, and it could charge the companies any reasonable amount of royalties. However, new companies may consider that mining tanzanite is the same as mining gold and diamonds. Then, the government does not have the monopolistic power. In the case of Tanzanite One, which already established operations and invested millions of dollars into the mines, it would be reasonable to impose applicable taxes, which were pardoned in the last decade. If the government increased royalties and taxes in the new mining contracts, coupled with a stricter tax revenue distribution, the impact of this FDI could truly bring out of poverty those who still believe in the legend of Ayanda. Update as of April 24, 2010 from Reuters “Tanzania's parliament has passed a new mining law that increases the rate of royalty paid on minerals like gold from 3 percent to 4 percent and requires the government to own a stake in future mining projects. The Mining Act 2010 also requires mining companies to list on the Dar es Salaam Stock Exchange. Page 34

- 36. Saved by the birth stone As part of the new legislation, Tanzania will not issue new gemstone mining licenses to foreign companies. Current agreements with foreign mining companies remain unchanged. "This bill makes comprehensive provision for prospecting for minerals, mining, processing and dealing in minerals, for the granting, renewal and termination of mineral rights, for payment of royalties, fees and other charges and for any other relevant matters," said part of the legislation. "The bill is a response to challenges faced and experience gained during 12 years of the implementation of the Mining Act ... that was enacted in the year 1998." Gemstones identified by the new law include diamonds, tanzanite, emerald, ruby, sapphire, turquoise, topaz, and others. Gemstone producer Tanzanite One (TNZ.L), will not be affected by the new ownership rules. Mining stakeholders said they will issue a joint statement on the new mining law on Monday. "The government will increase revenues a lot thanks to the new mining legislation ... But, it might send a negative signal to investors and might impact foreign direct investment. I'm worried on that," Zitto Kabwe, a member of parliament from the opposition Chadema party told Reuters. "We were supposed to pass a new law that balances benefits of the people and the interests of mining companies. The mood of the day in Tanzania is that foreign investors are stealing from the country and this might not necessarily be the case all the time." Government's stake in future mining projects would be determined by the level of investment in each individual joint venture, Kabwe said. Tanzania earned $57 million from mining royalties in 2009, but is expected to double this amount after the new mining law comes into force, he said. Page 35

- 37. Saved by the birth stone "The main highlight of this new legislation is that it makes gemstone mining the preserve of Tanzanians. It also changes the method of calculating royalties by using the gross value of minerals instead of the net value," said Kabwe.” (Hardy, 2010) Only time will show if this new legislation will make it easier for the local people to extract value from their unique stone or make the issue more controversial. Now that Tanzania will not issue new gemstone mining licenses to foreign companies, Dr. Kafumu will have to find new ways to attract FDI in the Minerals and Energy sector. Page 36

- 38. Saved by the birth stone APPENDICES Table 1. World Tanzanite Production WORLD TANZANITE PRODUCTION (in kilograms) 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 e Tanzania 467 1 094 2 250 1 946 5 228 5 516 5 473 6 461 4 490 3 400 3 400 e Estimated; estimated data are rounded to no more than two significant digits. (Thomas R. Yager, Weight of Production of Emeralds, Rubies, Sapphires, and Tanzanite from 1995 Through 2005, 2008) Table 2. Production of Tanzanite by Tanzanite One Page 37

- 39. Saved by the birth stone (Tanzanite One, 2009) Table 3. Ease of doing business in Tanzania Tanzania is ranked 131 out of 183 economies. Singapore is the top ranked economy in the Ease of Doing Business. Whole Africa receives less FDI that Singapore. Page 38

- 40. Saved by the birth stone Summary of Indicators Page 39

- 41. Saved by the birth stone (Doing Business in Tanzania, 2010) Page 40

- 42. Saved by the birth stone Table 4. Economic contributions by mining companies – general economic indicators (A brief on the mineral sector of Tanzania, 2009) Page 41

- 43. Saved by the birth stone REFERENCES A brief on the mineral sector of Tanzania. (2009). Retrieved 03 25, 2010, from The United Republic of Tanzania National website: http://www.tanzania.go.tz/ministriesf.html A case study of Tanzania: impact of FDI on developing economies. Morgan State University (2003). Ayanda tanzanite. (n.d.). Retrieved 4 20, 2010, from Tanzanite International: http://www.tanzanite-int.com/ayanda.htm Bekefi, T. (2006). Tanzania: Lessons in building linkages for competitive and responsible entrepreneurship. United Nations Industrial Development Organization and Kennedey School of Government, Harvard University. Doing Business in Tanzania. (2010). Retrieved 04 24, 2010, from The International Bank for Reconstruction and Development / The World Ban: http://www.doingbusiness.org/Documents/CountryProfiles/TZA.pdf Extractive Industries Transparency Initiative. (n.d.). Retrieved 2010, from http://www.eiti.org/Tanzania Friedman, M. (1970). The Social Responsibility of Business is to Increase its Profits. New York Times Magazine . Hardy, H. N.-M. (2010, 04 24). UPDATE 2-Tanzania increases royalties in new mining law. Retrieved 04 30, 2010, from http://www.reuters.com/article/idUSLDE63N04720100424 Jomo, F. (2007, 05 09). Tanzania to remove some mining incentives to benefit more from its resources. Retrieved 04 03, 2010, from Mineweb: http://www.mineweb.com/mineweb/view/mineweb/en/page67?oid=20681&sn=Detail&p id=54 Kilimba, J. J. (2008, 05 26). The tanzanite value chain illustration of key issues, challenges and opportunities. Retrieved 01 28, 2010, from Page 42

- 44. Saved by the birth stone http://roundtableafrica.net/media/uploads/File/Jackson%20Jonathan%20Kilimba- Tanzanite%20Value%20Chain%20in%20Tanzania.pdf Lange, S. (CMI Report R 2006: 11 54 p. ). Benefit Streams from Mining in Tanzania: Case Studies from Geita and Mererani. Bergen: Chr. Michelsen Institute . Larenaudie, S. (2007). Romancing a New Stone. Time , 2. Lissu, M. C. (2008, 10 08). A golden opportunity: How Tanzania is failing to benefit from gold mining . Retrieved 03 23, 2010, from Africa Files: http://www.africafiles.org/article.asp?ID=19218 Lovgren, S. (2001, 08 13). All that glitters. U.S. NEWS & WORLD REPORT , pp. 24-28. Lyimo, J. (2009, 11 22). Mererani residents occupied by tanzanite wealth dreams. Retrieved 03 17, 2010, from AllAfrica.com: http://allafrica.com/stories/200911231355.html MAGNE BRÅTVEIT, B. E. (2002). Dust Exposure During Small-scale Mining in Tanzania: A Pilot Study . University of Bergen, Ulriksdal 8c, N-5009 Bergen, Norway: Section for Occupational Medicine, Department of Public Health and Primary Health Care. National Bureau of Statistics. (2009, 12 18). Retrieved 04 20, 2010, from http://www.nbs.go.tz/index.php?option=com_phocadownload&view=category&id=67:inf lation&Itemid=106 Research and Markets: Tanzania Mining Report Q1 . (2010, 03 10). Retrieved 2010, from Business Wire: http://www.allbusiness.com/economy-economic-indicators/economic- indicators/14067337-1.html SANGA, S. P. (2006/2007). The role of poor governance in the T-Al-Qaeda link controversy. CPS International Policy Fellowship Program: C P S I N T E R N A T I O N A L P O L I C Y F E L L O W S H I P P R O G R A M. Schroeder, R. A. (2010). Tanzanite as conflict gem: Certifying a secure commodity chain in Tanzania. Critical Review Forum: Behind Enemy Lines (pp. Volume 41, issue 1, pages 56-65). http://www.sciencedirect.com/science?_ob=ArticleURL&_udi=B6V68-4VY16F8- 1&_user=10&_coverDate=01%2F31%2F2010&_rdoc=1&_fmt=high&_orig=search&_sort=d Page 43

- 45. Saved by the birth stone &_docanchor=&view=c&_searchStrId=1317212420&_rerunOrigin=google&_acct=C00005 0221&_version=1&_urlVersion=0&_us: Geoforum. Selasini, E. (2009, 03 21). Tanzanite Price Hits Rock Bottom. Retrieved 02 16, 2010, from All Africa: http://allafrica.com/stories/200903231136.html Tanzania - Still A Haven For Mining Investors? (2007, 05 07). Retrieved 03 25, 2010, from http://www.fleetstreetinvest.co.uk/commodities/mining/tanzania-still-a-haven-for- mining-investors-00008.html TANZANIA Gem Slave, T. c. (2006, 09 06). IRIN: humanitarian news and analysis. Retrieved 01 20, 2010, from http://www.irinnews.org/Report.aspx?ReportId=61004 Tanzania Mining Report Q2. (2009, 05 07). Retrieved 04 03, 2010, from Business Monitor International: http://www.marketresearch.com/product/display.asp?productid=2267465 Tanzanite One. (n.d.). Retrieved 2010, from The Tanzanite Foundation: http://www.tanzaniteone.com/tanzanite_tanzanite_foundation.htm Tanzanite One. (n.d.). Retrieved 2010, from Corporate Social Responsibility: http://www.tanzaniteone.com/tanzaniteone_social.htm Tanzanite One . (n.d.). Retrieved 2010, from Trading and sightholders: http://www.tanzaniteone.com/tanzanite_sightholders.htm Tanzanite One. (2008). Retrieved 02 22, 2010, from Annual Report 2008: http://www.tanzaniteone.com/financials/2008/TanzaniteOne_AR_2008.pdf Tanzanite One. (2009, 09 17). Retrieved from H1 2009 Financial Results and Marketing Update: http://www.tanzaniteone.com/Presentations/2009_09_17_T1_Presentation.pdf Thomas R. Yager, W. D. (2008, 10 13). Weight of Production of Emeralds, Rubies, Sapphires, and Tanzanite from 1995 Through 2005. Retrieved 04 19, 2010, from http://pubs.usgs.gov/of/2008/1013/ofr2008-1013.pdf Thomas R. Yager, W. D. (2008, 10 13). Weight of Production of Emeralds, Rubies, Sapphires, and Tanzanite from 1995 Through 2005. Retrieved 2010, from U.S. Geological Survey: http://pubs.usgs.gov/of/2008/1013/ofr2008-1013.pdf Page 44

- 46. Saved by the birth stone USAID. (2005, 06 16). USAID/Tanzania Annual Report . Retrieved 04 02, 2010, from http://pdf.usaid.gov/pdf_docs/PDACD882.pdf Vincent Pardieu and Richard W. Hughes, w. G. (2008, july). The merelani tanzanite mines. Retrieved 02 29, 2010, from Ruby-sapphire.com: http://www.ruby- sapphire.com/tanzania-tanzanite-mines.htm World Bank. (2008). GNI per capita, Atlas method . World Bank Statistics. World Economic Forum. (2009, 06 10). Retrieved 04 03, 2010, from The Africa Competitiveness Report : http://www.weforum.org/en/initiatives/gcp/Africa%20Competitiveness%20Report/index. htm Page 45