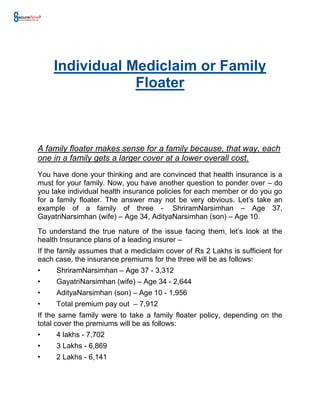

Individual mediclaim or family floater

A family floater makes sense for a family because, that way, each one in a family gets a larger cover at a lower overall cost. You have done your thinking and are convinced that health insurance is a must for your family. Now, you have another question to ponder over – do you take individual health insurance policies for each member or do you go for a family floater. The answer may not be very obvious. Let’s take an example of a family of three - Shriram Narsimhan – Age 37, Gayatri Narsimhan (wife) – Age 34, Aditya Narsimhan (son) – Age 10. To understand the true nature of the issue facing them, let’s look at the health Insurance plans of a leading insurer – If the family assumes that a mediclaim cover of Rs 2 Lakhs is sufficient for each case, the insurance premiums for the three will be as follows: • Shriram Narsimhan – Age 37 - 3,312 • Gayatri Narsimhan (wife) – Age 34 - 2,644 • Aditya Narsimhan (son) – Age 10 - 1,956 • Total premium pay out – 7,912 If the same family were to take a family floater policy, depending on the total cover the premiums will be as follows: • 4 lakhs - 7,702 • 3 Lakhs - 6,869 • 2 Lakhs - 6,141 Before we draw any conclusions, let us first try and understand a family floater policy. The sum insured value floats among the family members. Most of the policies will cover husband, wife and a couple of children; some may cover parents too. The coverage for the entire family is limited to the sum insured. Now, in our example, the Narsimhan family can take a 3L or 4L policy at a lower cost than a 2L policy for each. When they take a floater policy, they do not need to take a cover that is 3 times the felt need for each. This is because the likelihood of all three getting hospitalized during the same year is considerably lower than the likelihood of only one of the three getting hospitalized during a given year. Therefore a family floater makes sense for a family because, that way, each one in a family gets a larger cover at a lower overall cost. The possibility of more than one family member getting hospitalized in the same year is incredibly low, unless there are exceptional families where the whole family is travelling together most of the times in a year or has a history of medical problems that can happen concurrently. These are really remote possibilities.

Recommandé

Contenu connexe

Dernier

Dernier (20)

En vedette

En vedette (20)

Individual mediclaim or family floater

- 1. Individual Mediclaim or Family Floater A family floater makes sense for a family because, that way, each one in a family gets a larger cover at a lower overall cost. You have done your thinking and are convinced that health insurance is a must for your family. Now, you have another question to ponder over – do you take individual health insurance policies for each member or do you go for a family floater. The answer may not be very obvious. Let’s take an example of a family of three - ShriramNarsimhan – Age 37, GayatriNarsimhan (wife) – Age 34, AdityaNarsimhan (son) – Age 10. To understand the true nature of the issue facing them, let’s look at the health Insurance plans of a leading insurer – If the family assumes that a mediclaim cover of Rs 2 Lakhs is sufficient for each case, the insurance premiums for the three will be as follows: • ShriramNarsimhan – Age 37 - 3,312 • GayatriNarsimhan (wife) – Age 34 - 2,644 • AdityaNarsimhan (son) – Age 10 - 1,956 • Total premium pay out – 7,912 If the same family were to take a family floater policy, depending on the total cover the premiums will be as follows: • 4 lakhs - 7,702 • 3 Lakhs - 6,869 • 2 Lakhs - 6,141

- 2. Before we draw any conclusions, let us first try and understand a family floater policy. The sum insured value floats among the family members. Most of the policies will cover husband, wife and a couple of children; some may cover parents too. The coverage for the entire family is limited to the sum insured. Now, in our example, the Narsimhan family can take a 3L or 4L policy at a lower cost than a 2L policy for each. When they take a floater policy, they do not need to take a cover that is 3 times the felt need for each. This is because the likelihood of all three getting hospitalized during the same year is considerably lower than the likelihood of only one of the three getting hospitalized during a given year. Therefore a family floater makes sense for a family because, that way, each one in a family gets a larger cover at a lower overall cost. The possibility of more than one family member getting hospitalized in the same year is incredibly low, unless there are exceptional families where the whole family is travelling together most of the times in a year or has a history of medical problems that can happen concurrently. These are really remote possibilities. In our example, the Narsimhan family can go for the Rs 4 lakh family floater for two reasons – a) it is cheaper than buying 2 Lakhs cover for each and b) a higher cover provisions for medical care cost escalations over the next

- 3. few years (it is usually difficult to increase the cover without impacting the premium adversely, when you renew premiums during later years). The clear advantage of family floaters are: • Less expensive than an individual mediclaim policy. • You can add your immediate family members like your spouse and kids, without any hassles. Instead of individual mediclaim of Rs 2 lakh, if the Narsimhan family opts for a floater of Rs 4 lakh, they will benefit if there is a big claim in a year of, say, Rs 2.5 lakh. However, there are situations where the floater may not be a good idea. This is especially true if there is an elderly person in the family and the other members are considerably younger. The elderly person will pull up the premium of the floater adversely. In such cases, a better solution will be to have an individual mediclaim for the elderly member and a family floater for the rest. Also, in some cases, such as an elderly family, which is likely to have higher medical needs, may benefit from individual mediclaim policies for each member.

- 4. For Inquiries Visit http://securenow.in/ Fill in our inquiry form