1. Calculating your income taxes is very easy. All you need to know is which tax slab will be

applicable to you. But, before we get to tax slabs, lets understand in 3 quick steps how to

calculate taxes.

Step 1: Identify and tabulate all sources of income – salary, business income, interest, rental,

capital gains

Step 2: Identify which deductions and tax savings are applicable to you – 80C deductions,

interest repayment

Step 3: Apply the relevant tax slab depending upon your sex and age, after taking the deductions

and savings

In addition to the tax payable on income, you will also have to pay a Surcharge (if your income

exceeds Rs.10 lakhs in case of individuals) and an Education Cess levied by the Government on

all tax payers. If you are a salaried employee, chances are that your employer has already

deducted these in your monthly pay.

The tax slab will help you identify how much of your income will be available to you tax free

and thereafter what tax rate will be charged to the remaining income.

If you are a woman or a senior citizen, you will be entitled to a larger tax-free amount. The

following tables will help you identify which tax slabs are relevant for you:

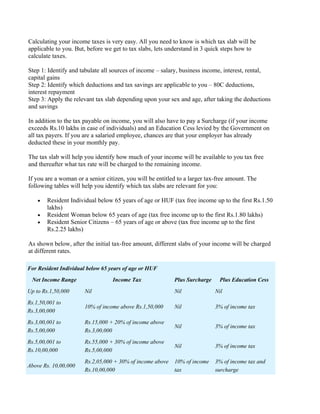

• Resident Individual below 65 years of age or HUF (tax free income up to the first Rs.1.50

lakhs)

• Resident Woman below 65 years of age (tax free income up to the first Rs.1.80 lakhs)

• Resident Senior Citizens – 65 years of age or above (tax free income up to the first

Rs.2.25 lakhs)

As shown below, after the initial tax-free amount, different slabs of your income will be charged

at different rates.

For Resident Individual below 65 years of age or HUF

Net Income Range Income Tax Plus Surcharge Plus Education Cess

Up to Rs.1,50,000 Nil Nil Nil

Rs.1,50,001 to

10% of income above Rs.1,50,000 Nil 3% of income tax

Rs.3,00,000

Rs.3,00,001 to Rs.15,000 + 20% of income above

Nil 3% of income tax

Rs.5,00,000 Rs.3,00,000

Rs.5,00,001 to Rs.55,000 + 30% of income above

Nil 3% of income tax

Rs.10,00,000 Rs.5,00,000

Rs.2,05,000 + 30% of income above 10% of income 3% of income tax and

Above Rs. 10,00,000

Rs.10,00,000 tax surcharge

2. For Resident Women below 65 years of age

Net Income Range Income Tax Plus Surcharge Plus Education Cess

Up to Rs.1,80,000 Nil Nil Nil

Rs.1,80,001 to

10% of the income above Rs.1,80,000 Nil 3% of income tax

Rs.3,00,000

Rs.3,00,001 to Rs.12,000 + 20% of the income above

Nil 3% of income tax

Rs.5,00,000 Rs.3,00,000

Rs.5,00,001 to Rs.52,000 + 30% of the income above

Nil 3% of income tax

Rs.10,00,000 Rs.5,00,000

Rs.2,02,000 + 30% of the income 10% of income 3% of income tax and

Above Rs.10,00,000

above Rs.10,00,000 tax surchargee

For Resident Senior Citizens ( 65 years of age and above, including those who turn 65 at any time

during the Financial Year 2008-09)

Net Income Range Income Tax Plus Surcharge Plus Education Cess

Up to Rs.2,25,000 Nil Nil Nil

Rs.2,25,001 to

10% of the income above Rs.2,25,000 Nil 3% of income tax

Rs.3,00,000

Rs.3,00,001 to Rs.7,500 + 20% of the income above

Nil 3% of income tax

Rs.5,00,000 Rs.3,00,000

Rs.5,00,001 to Rs.47,500 + 30% of the income above

Nil 3% of income tax

Rs.10,00,000 Rs.5,00,000

Rs.2,05,000 + 30% of the income 10% of income 3% of income tax and

Above Rs.10,00,000

above Rs.10,00,000 tax surchargee