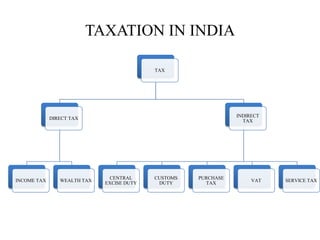

1. TAXATION IN INDIA

TAX

INDIRECT

DIRECT TAX

TAX

CENTRAL CUSTOMS PURCHASE

INCOME TAX WEALTH TAX VAT SERVICE TAX

EXCISE DUTY DUTY TAX

2. NORMAL RATES OF INCOME-TAX

FOR ASSESSMENT YEAR 2012-13

I. In the case of every Individual or Hindu undivided family or AOP/BOI

(other than a co-operative society) whether incorporated or not, or every

artificial judicial person

INCOME %

0-180,000 NIL

180,001-500,000 10

500,001-800,000 20

800,001-ABOVE 30

Note : No surcharge is payable by the above assessees.

‗Education Cess‘ @ 2%, and ‗Secondary and Higher Education Cess (SHEC)‘ @

1% on income tax shall be chargeable.

3. II. In the case of every individual, being a woman resident in India, and

below the age of sixty years at any time during the previous year.

INCOME %

0-190,000 NIL

190,001-500,000 10

500,001-800,000 20

800,001-ABOVE 30

Note : No surcharge is payable by the above assessees.

‗Education Cess‘ @ 2%, and ‗Secondary and Higher Education Cess (SHEC)‘ @ 1% on

income tax shall be chargeable.

4. III. In the case of every individual, being a resident in India, who is of the

age of 60 years or more at any time during the previous year. [Senior citizen]

INCOME %

0-250,000 NIL

250,001-500,000 10

500,001-800,000 20

800,001-ABOVE 30

Note : No surcharge is payable by the above assessees.

‗Education Cess‘ @ 2%, and ‗Secondary and Higher Education Cess (SHEC)‘ @ 1% on

income tax shall be chargeable.

5. IV. In the case of every individual, being a resident in India, who is of the age

of 80 years or more at any time during the previous year. [Very senior citizen]

INCOME %

0-500,000 NIL

500,001-800,000 20

800,001-ABOVE 30

Note : No surcharge is payable by the above assessees.

‗Education Cess‘ @ 2%, and ‗Secondary and Higher Education Cess (SHEC)‘ @ 1% on

income tax shall be chargeable.

6. • WHO IS AN ASSESSEE ?: [Section 2(7)]

-Any person who is liable to pay any tax or any other sum under the

Income Tax Act, 1961

• -Assessee includes

• (a) Every person in respect of whom any proceedings has been taken for

the assessment.

• (b) Every person who is deemed to be an assessee under the Act.

(c) Every person who is deemed to be an assessee in default under the

Act.

7. WHAT IS ASSESSMENT YEAR? [Section 2 (9)]

• 1. Assessment Year means the period of twelve

months commencing on the 1st day of April every

year.

• 2. The year for which tax is paid is called Assessment

Year.

• The present Assessment Year is 2012-13 relating to

previous year 2011-12.

8. SO WHAT IS PREVIOUS YEAR? [Section 3]

• 1. Previous Year is the year in which income is

earned.

• The present previous year 2011-12 and its

Assessment Year is 2012-13.

• Note: Previous Year for Newly established business From the date of

setting up of the business to the end of the Financial year in which

business was set up.

9. • Example : X Ltd. Started business on 1.11.11. So for

X Ltd. Previous year will be considered as

1.11.11 to 31.3.12.

10. INCOME TAX

INCOME FROM SALARIES

INCOME FROM HOUSE PROPERTY

PROFITS AND GAINS OF BUSINESS OR

PROFESSION

CAPITAL GAINS

INCOME FROM OTHER SOURCES

11. INCOME FROM SALARIES

• The term ‗salary‘ for the purposes of Income-Tax Act will include both

monetary payments & non-monetary(e.g.

• MONETARY PAYMENTS include basic salary, bonus, commission,

allowances etc.)

• NON-MONETARY FACILITIES (e.g. housing accommodation, medical

facility, interest free loans etc).

12. INCOME FROM HOUSE PROPERTY

• 1. The basis of chargeability under the head income from house property is

Annual Value.

• 2. The property must consist of Building or Lands Appurtenant thereto.

• 3. The assessee must be the owner of such property.

• 4. The property may be used for any purpose other than the assessee‘s

business or profession.

• Owner

• Deemed Owner:

13.

14. PROFITS AND GAINS OF BUSINESS

OR PROFESSION

• BUSINESS [Sec. 2(13)]

Definition of ―Business‖ includes any trade, commerce or manufacture or

any adventure or concern in the nature of trade, commerce or manufacture.

• PROFESSION [Sec. 2(36)]

Profession involves an exercise of intellect and skill based on learning and

experience.

15.

16. CAPITAL GAINS

• 1. Capital Asset: [Section 2(14)]

• Includes :

• Property of any kind, whether or not connected with business or profession

• Excludes :

• (a) Stock in trade

• (b) Personal Effects

• (c) Rural Agricultural Lands in India

• (d) 6 ½ % Gold Bonds 1977; 7% Gold Bonds 1980 & National Defence

Gold Bonds, 1980.

• (e) Special Bearer Bonds, 1991

• (f) Gold Deposit Bonds issued under Gold Deposlt Scheme 1999

17. INCOME FROM OTHER SOURCES

• (i) Dividend [Sec. 56 (2) (i)]

• (ii) Any winnings from lotteries, crossword puzzles, races including horse races, card games

and other games of any sort or form, gambling or betting of any form or nature whatsoever-

[Sec. 56(2)

• (iv) Income by way of interest on securities, if it is not chargeable as Profits and gains of

business i.e. where securities are held as investments- Sec. 56(2)(id).

• (v) Income from machinery, plant or furniture belonging to the assessee let on hire, if the

income is not chargeable to income-tax under the head, Profits and gains of Business or

Profession - Sec. 56(2)(ii).

• (vi) Income from letting of machinery, plant or furniture, if such income is not chargeable

under the head ―Profits and gains of Business or Profession‖- Sec. 56(iii)

• (viii) Gifts aggregating to more than ` 50,000 in a year on or after 1st Day of April, 2006 -

Sec. 56(vi)

• (ix) Taxation of property acquired without consideration or for an inadequate

consideration as ‘income

18. QUIZ

IS THESE ITEMS TAXABLE?

• GIFT FROM FRIEND 8000 IN THE YEAR 2007

• GIFT FROM CLIENT1 15000 IN THE YEAR 2007

• GIFT FROM CLIENT1 27000 IN THE YEAR 2007

• ANS: IT IS NOT TAXABLE BECAUSE GIFTS DON`T AGGREGATE

MORE THAN ` 50,000 IN A YEAR

19. Wealth Tax

– Wealth tax is chargeable only on the following assets:

Wealth tax is not levied on productive assets, hence investments in shares,

debentures, UTI, mutual funds, etc are exempt from it.

– Any guest house, residential house, commercial property, urban farm house.

– Motor car for personal use.

– Jewellery, bullion, furniture, utensils or any other article made wholly or partly of

gold, silver, platinum or any other precious metal or any alloy containing one or more

of such precious metals.

– Yachts, boats, and air-crafts used for non-business purposes.

– Urban land, subject within the jurisdiction of municipality or cantonment board with a

population of no less than 10,000 according to the preceding census or within 8

kilometers or such local limits.

– Cash in hand exceeding Rs. 50000 of individuals and HUFs and in other cases,

amount not recorded in he book of accounts.

– The value of all the taxable assets on the valuation date is clubbed together and is

reduced by the amount of debt owed by the assessee. The net wealth so arrived at is

charged to tax at the rates specified. The present rate of tax is 1% of the amount by

which the net wealth exceeds Rs. 1500000. The rate is same for individuals, HUF's

and companies.

– Special rules have been laid down in the Act regarding valuation of various assets like

immovable properties, shares, jewellery etc.

20. CORPORATE TAX

ACCORDING TO COMPANIES ACT 1956

DOMESTIC COMPANIES:

• Domestic Corporations / Private Limited Companies 33.99%

• Domestic Corporations / Public Limited Companies 33.99%

• Limited Liability Partnership (LLP's) 30.9%

• NOTE: THE ABOVE TAX RATES INCLUDES SURCHARGE

FOREIGN COMPANIES

• Dividends20%

• Interest Income 20%

• Royalties 30%

• Technical Services30%

• Other income 55%

NOTE: THE ABOVE TAX RATES INCLUDES SURCHARGE

21. DEDUCTION U/S 80

• Any assessee can have a deductions of

MAXIMUM 100,000

22. 12.1 INCOMES NOT INCLUDED IN TOTAL

INCOME [Sec. 10]

• In computing the total income of a previous year of any person, any income

falling within any of the following clauses shall not be included—

• agricultural income;

• any sum received by an individual as a member of a Hindu undivided

family, where such sum has been paid

• out of the income of the family, or, in the case of any impartible estate,

where such sum has been paid out of the income of the estate belonging to

the family ;

• Case Laws:

• Vijayananda Galapati, Maharaj Kumar of Vizianagaram v. CIT

• Kedar Narain Singh v. CIT

:

23. MINIMUM ALTERNATE TAX (MAT)

• Rate of Minimum Alternate Tax increased to 18.5% [Section 115JB(1)]

[W.e.f. A.Y.2012-13]

• BOOK PROFIT:

• First 3,00,000 of book profit — 90%

• Balance of book profit -60%

24. RETURN OF INCOME

• COMPULSORY FILING OF RETURN OF INCOME [SECTION 139(1)]

• When is the ‘Due date’ to file returns -

• (a) 30th September of the assessment year, where the assessee is -

• (i) a company; or

• (ii) a person (other than a company) whose accounts are required to be

audited under the Income-tax Act, 1961 or any other law in force; or

• (iii) a working partner of a firm whose accounts are required to be audited

under the Income-tax Act, 1961 or any other law for the time being in

force.

• (b) 31st July of the assessment year, in the case of any assessee other

than those covered in (a) above.

26. DEFAULT TO FILE A RETURN

INTEREST FOR DEFAULT IN FURNISHING

RETURN OF INCOME [SECTION 234A]

• (1) Interest under section 234A is attracted where

an assessee furnishes the return of income after

the due date or does not furnish the return of

income.

• (2) The interest is payable for the period

commencing from the date immediately following

the due date and ending on the following dates

27. • Every assesse should have PERMANENT ACCOUNT NUMBER (PAN)

to file the return

• It is 10 alphanumeric digits

29. • QUESTIONS & ANSWERS ON RETURN OF INCOME

• Question 1. What is the due date of filling of return of income in case of

a non-working partner of a firm whose accounts are not liable to be

audited?

• Answer : Due date of furnishing return of income in case of non-working

partner shall be 31st July of the assessment year whether the accounts of

the firm are required to be audited or not.

30. Q&A

Can a revised return be further revised?

• Answer : If the assessee discovers any omission or any wrong statement in

a revised return, it is possible to revise such a revised return provided it is

revised within the same prescribed time

[ Niranjan Lal Ram Chandra Vs.CIT (1982)

31. CASE: Joseph engaged in profession filed his return of income for

assessment year 2011-12 on 15th November, 2011. He disclosed an income

of `4,00,000 in the return. In February, 2012 he discovered that he did

not claim certain expenses and filed a revised return on 3rd February,

2012 showing an income of `1,80,000 and claiming those expenses. Is the

revised return filed by Joseph acceptable?

• Answer: Joseph is engaged in profession. The due date for filing income tax

return for assessment year 2011-12 as per section 139(1) of the Income-tax

Act is 30th September, 2011 if his accounts are required to be audited under

any law. The due date is 31st July, 2011 if the accounts are not required to be

audited under any law.

• CASE: Chandra Sinha v. CIT

32. INDIA INDIRECT TAXES N TAX

LEVIES ON IMPORTS / EXPORTS VALUE ADDED TAX

• Customs duty leviable on goods imported • VAT introduced in most Indian states from

into India April 1, 2005

• R&D cess imposed on payment made for • VAT implementation expected to

import of technology streamline multi point levies

• Certain tariff concessions on imports from • Tax credit mechanism for VAT paid on

Singapore, Sri-Lanka, etc as a result of inputs against tax due on outputs

free trade agreements

• Octroi / entry tax also levied in certain

states on purchases from other states

EXCISE DUTY Indirect taxes SERVICE TAX

• Excise duty levied on manufacture • Payment of services tax at 12.24 % on

• Packing/re-packing, labeling / re- labeling certain services availed

of certain products amount to manufacture • Service Tax paid on input service is

• Excise duty is payable on transaction available as credit to discharge either

value i.e. usually sale price. service tax or excise duty liability of output

service and finished product respectively.

33. LAWS RELATING TO CENTRAL

EXCISE

• Central Excise Act, 1944(CEA) : The basic Act which provides the

constitutional power for charging of duty, valuation , powers of officers,

provisions of arrests, penalty, etc.

• Central Excise Tariff Act, 1985 (CETA): This classifies the goods under

96 chapters with specific codes assigned.

• Central Excise Rules, 2002: The procedural aspects are laid herein. The

rules are implemented after issue of notification.

• Central Excise Valuation(Determination of Price of Excisable Goods)

Rules,2000: The provisions regarding the valuation of excisable goods are

laid down in this rule.

• Cenvat Credit Rules, 2004: The provisions relating to Cenvat Credit

available and its utilisation is mentioned.

34. Who is liable to pay duty?

• Rule 4(1) of the Central Excise Rules, 2002 provides that every

person who produces or manufactures any excisable goods, or who

stores such goods in a warehouse, shall pay the duty leviable on such

goods in the manner provided in Rule 8 or under any other law, and no

excisable goods, on which any duty is payable, shall be removed without

payment of duty from any place, where they are produced or manufactured

or from a warehouse, unless otherwise provided.

35. CASE:

• Hindustan General Industries v. CCE 2003-

Ownership of raw material is not relevant for duty liability

36. CENTRAL SALES TAX ACT-1956

CONDITIONS

1. There Should Be A Dealer

2. he Should Be A Registered Dealer

3. he Must Carry On Any Business

4. sale Should Take Place

5. sale May Be To A Registered Or Unregistered Buyer

6. The Sale Should Be Of Goods.

7. The Sale Can Be Of Also Declared Goods (Goods Of Specific

Importance)

8. The Sale Should Take Place In Course Of Inter State

9. The Sales Should Not Be Within The Same State.

11. The Sale Should Not Be Outside India

37.

38. CUSTOMS DUTY:

• Customs duty on imports and exports

• Customs duty is on imports into India and export out of India. Section 12 of

Customs Act, often called charging section, provides that duties of customs

shall be levied at such rates as may be specified under ‘The Customs Tariff

Act, 1975', or any other law for the time being in force, on goods imported

into, or exported from, India.

39. CUSTOMS DUTY:

• Similarity between excise and customs

• There are many common provisions and/or similarities in provisions Central Excise and customs Law.

Administration, Settlement Commission and Tribunal are common. Provisions of Tariff, principles of valuation,

refund, demands, exemptions, appeals, search, confiscation and appeals are similar.

CASE: Kiran Spinning Mills v. CC

• Taxable event in imports

• In case of imports, taxable event occurs when goods mix with landmass of India

CASE :UOI v. Apar P Ltd

• In case of warehoused goods, the goods continue to be in customs bond. Hence, 'import' takes place only when

goods are cleared from the warehouse - confirmed in

CASE: UOI v. Rajindra Dyeing and Printing Mills (2005)

• Taxable event in exports

• In case of exports, taxable event occurs when goods cross territorial waters of India –

• Territorial waters and exclusive economic zone

• Territorial waters of India extend upto 12 nautical miles inside sea from baseline on coast of India and include

any bay, gulf, harbour, creek or tidal river. (1 nautical mile = 1.1515 miles = 1.853 Kms). Sovereignty of India

extends to the territorial waters and to the seabed and subsoil underlying and the air space over the waters.

• ‗Exclusive economic zone' extends to 200 nautical miles from the base-line. Area beyond that is ‗high seas‘.

• Indian Customs Waters ,Indian Customs waters extend upto 12 nautical miles beyond territorial waters. Powers

of customs officers extend upto 12 nautical miles beyond territorial waters.

40. SERVICE TAX

• • Service tax is imposed under Finance Act, 1994 as amended from time to time. There is no

Service Tax Act.

• • Service Tax @ 5% was introduced from 1-7-1994.

• Service tax rate has been reduced to 10.30% w.e.f. 24-2-2009.

• Service tax is payable on taxable services as defined in various clauses of section 65(105) of

Finance Act, 1994. Presently, about 117 services are taxable.

• Service tax is payable on gross amount charged for taxable service provided or to be

provided [Section 67]. If consideration is partly not in money, valuation is required to be

done as per Valuation Rules. Tax is payable when advance is received.

• Small service providers upto ten lakhs are exempt. Export of service is exempt from service

tax under Notification No. 6/2005-ST dated 1-3-2005. Services provided in J&K are not

taxable [section 64(1)]

• Cenvat credit is available of inputs, input services and capital goods used for providing taxable

output Services.

41. OCTROI

• The state government levies the octroi charges when the product enters the

state. This charge is applicable to certain states and fluctuates as per the

Government regulations and we are unable to confirm the amount.

• The octroi charge is payable by the recipient at the time of delivery.

• Octroi/entry tax amount paid by Clearing & Forwarding Agent, CHA or

Transporter on behalf of owner of goods/Principal.

• Customs duty, dock dues, transport charges etc. paid by Customs House

Agent on behalf of client.

• Advertisement charges paid by Advertising Agency to newspaper on

behalf of clients.

• Ticket charges paid by Travel Agent and recovered from his customer.

• Reimbursement of goodown, salary and loading/unloading expenses by

Principal to C & F Agent.

42. OCTROI

CASE :In Bhatat Sanchar Nigam Ltd. v. UOI (2006)

• It has been clearly held that price of goods cannot be included in value of

services.

• As an obvious corollary, service tax cannot be imposed on value of

material.

43. VAT

• VAT- Value Added Tax

•

VAT is a sales tax collected by the government (of the state in which the final consumer is

located) – which is the government of destination state on consumer expenditure.

The mechanism of VAT is such that, for goods that are imported and consumed in a particular

state, the first seller pays the first point tax, and the next seller pays tax only on the value-addition

done – leading to a total tax burden exactly equal to the last point tax.

CENVAT - Central Value Added Tax

• CENVAT is related to central excise.

• CENVAT means, Tax on Value Addition on the goods manufactured according to Central Excise

& Customs Act

• Definition. Here the value addition means the Additional Services/Activities etc. which converts

the Input in to Output, and the output is newly recognised as per the this act as Exciseble goods..