More Related Content Similar to JLL Detroit Office Insight & Statistics – Q2 2016 (17) More from Aaron Moore (9) 1. CBD Detroit vacancy rates

Source: JLL Research

CBD absorption and rents

Source: JLL Research

Suburban Class A rents and vacancies

Source: JLL Research

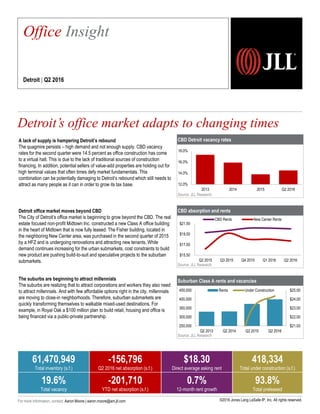

Detroit’s office market adapts to changing times

2,257

Office Insight

Detroit | Q2 2016

61,470,949

Total inventory (s.f.)

-156,796

Q2 2016 net absorption (s.f.)

$18.30

Direct average asking rent

418,334

Total under construction (s.f.)

19.6%

Total vacancy

-201,710

YTD net absorption (s.f.)

0.7%

12-month rent growth

93.8%

Total preleased

A lack of supply is hampering Detroit’s rebound

The quagmire persists – high demand and not enough supply. CBD vacancy

rates for the second quarter were 14.5 percent as office construction has come

to a virtual halt. This is due to the lack of traditional sources of construction

financing. In addition, potential sellers of value-add properties are holding out for

high terminal values that often times defy market fundamentals. This

combination can be potentially damaging to Detroit’s rebound which still needs to

attract as many people as it can in order to grow its tax base.

Detroit office market moves beyond CBD

The City of Detroit’s office market is beginning to grow beyond the CBD. The real

estate focused non-profit Midtown Inc. constructed a new Class A office building

in the heart of Midtown that is now fully leased. The Fisher building, located in

the neighboring New Center area, was purchased in the second quarter of 2015

by a HFZ and is undergoing renovations and attracting new tenants. While

demand continues increasing for the urban submarkets, cost constraints to build

new product are pushing build-to-suit and speculative projects to the suburban

submarkets.

The suburbs are beginning to attract millennials

The suburbs are realizing that to attract corporations and workers they also need

to attract millennials. And with few affordable options right in the city, millennials

are moving to close-in neighborhoods. Therefore, suburban submarkets are

quickly transforming themselves to walkable mixed-used destinations. For

example, in Royal Oak a $100 million plan to build retail, housing and office is

being financed via a public-private partnership.

12.0%

14.0%

16.0%

18.0%

Q2 2016201520142013

$15.50

$17.50

$19.50

$21.50

Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016

CBD Rents New Center Rents

$21.00

$22.00

$23.00

$24.00

$25.00

250,000

300,000

350,000

400,000

450,000

Q2 2013 Q2 2014 Q2 2015 Q2 2016

Rents Under Construction

For more information, contact: Aaron Moore | aaron.moore@am.jll.com ©2016 Jones Lang LaSalle IP, Inc. All rights reserved.

2. Current conditions – submarket Historical leasing activity (s.f.)

Source: JLL Research Source: JLL Research

Total net absorption (s.f.)

Source: JLL Research

Total vacancy rate (%)

Source: JLL Research

Direct average asking rent ($ p.s.f.)

Source: JLL Research

-1,304,860

-476,545

-1,953,820

-1,767,490

1,277,568

1,510,536

176,382

1,288,053

872,323

-201,710

-2,500,000

-1,000,000

500,000

2,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD 2016

$20.75

$19.73

$19.31

$19.10

$18.56

$18.15

$17.76

$17.99

$18.41 $18.32

$17.00

$18.50

$20.00

$21.50

2007 2008 2009 2010 2011 2012 2013 2014 2015 Q2 2016

25.9% 26.7%

30.0%

32.9%

30.8%

28.3% 28.0%

25.3%

19.0% 19.6%

15.0%

25.0%

35.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 Q2 2016

Northern I-275,

Washtenaw

Landlordleverage

Tenantleverage

Peaking

market

Falling

market

Bottoming

market

Rising

market

CBD

Downriver,

Dearborn

5,000,000

5,300,000 5,100,000

3,300,000

989,081

0

2,000,000

4,000,000

6,000,000

2012 2013 2014 2015 YTD 2016

Southfield, Troy, Macomb,

Farmington Hills

©2016 Jones Lang LaSalle IP, Inc. All rights reserved.For more information, contact: Aaron Moore | aaron.moore@am.jll.com

Royal Oak

Southern I-275

North Oakland

Birmingham

New Center

3. Office statistics

Detroit | Q2 2016

Class Inventory (s.f.)

Total net

absorption (s.f.)

YTD total net

absorption (s.f.)

YTD total net

absorption (% of

stock)

Direct vacancy

(%)

Total vacancy

(%)

Average direct

asking rent ($

p.s.f.)

YTD completions

(s.f.)

Under

construction (s.f.)

CBD Totals 12,843,492 -90,382 -10,198 -0.1% 14.4% 14.5% $20.61 0 0

New Center Totals 1,117,100 4,348 4,348 0.4% 20.9% 21.2% $18.20 0 0

Urban Totals 13,960,592 -86,034 -5,850 0.0% 14.9% 15.0% $20.34 0 0

Birmingham/Bloomfield Totals 2,858,942 17,486 24,065 0.8% 7.6% 8.0% $23.43 0 34,354

Dearborn Totals 2,547,516 -5,533 -1,713 -0.1% 43.5% 43.5% $15.16 0 0

Downriver Totals 404,475 547 412 0.1% 41.9% 41.9% $12.65 0 0

Farmington/Farmington Hills Totals 4,178,825 -24,686 -32,807 -0.8% 25.9% 26.0% $18.13 0 0

Macomb Totals 945,140 -3,167 -18,337 -1.9% 11.4% 11.4% $17.21 0 0

Northern I-275 Corridor Totals 3,621,671 -402 -70,431 -1.9% 12.7% 13.2% $19.65 0 383,980

North Oakland Totals 2,375,789 -18,269 -38,522 -1.6% 18.3% 8.7% $17.78 0 0

Royal Oak/Southeast Oakland Totals 638,607 -7,400 -6,567 -1.0% 11.1% 11.1% $15.80 0 0

Southern I-275 Corridor Totals 1,129,017 0 161,168 14.3% 0.0% 0.0% $0.00 0 0

Southfield Totals 12,810,271 -9,902 153,819 1.2% 25.7% 25.9% $17.38 0 0

Troy Totals 10,470,696 -14,296 -17,667 -0.2% 24.4% 24.6% $18.12 0 0

Washtenaw Totals 5,529,408 -5,140 -349,280 -6.3% 9.4% 11.2% $23.85 0 0

Suburbs Totals 47,510,357 -70,762 -195,860 -0.4% 21.1% 21.0% $17.90 0 418,334

Detroit Totals 61,470,949 -156,796 -201,710 -0.3% 19.7% 19.6% $18.32 0 418,334

CBD A 6,194,714 -88,183 -43,001 -0.7% 14.2% 14.4% $22.20 0 0

Urban A 6,194,714 -88,183 -43,001 -0.7% 14.2% 14.4% $22.20 0 0

Birmingham/Bloomfield A 1,413,082 3,041 7,435 0.5% 6.6% 6.6% $27.68 0 34,354

Dearborn A 446,890 0 0 0.0% 11.3% 11.3% $25.00 0 0

Farmington/Farmington Hills A 618,109 0 -18,728 -3.0% 14.1% 14.1% $22.50 0 0

Macomb A 295,494 -3,167 -411 -0.1% 2.3% 2.3% $19.29 0 0

Northern I-275 Corridor A 1,059,039 -7,300 -4,959 -0.5% 4.2% 4.2% $22.80 0 383,980

North Oakland A 433,137 13 -18,577 -4.3% 47.5% 47.5% $20.02 0 0

Southern I-275 Corridor A 950,857 0 161,168 16.9% 0.0% 0.0% NA 0 0

Southfield A 2,789,819 -3,383 154,554 5.5% 16.4% 16.7% $22.89 0 0

Troy A 1,924,131 -1,670 70,189 3.6% 16.5% 17.3% $25.46 0 0

Washtenaw A 3,220,406 -2,071 -247,653 -7.7% 9.7% 12.8% $25.80 0 0

Suburbs A 13,150,964 -14,537 103,018 0.8% 12.0% 12.9% $23.92 0 418,334

Detroit A 19,345,678 -102,720 60,017 0.3% 12.7% 13.4% $23.31 0 418,334

CBD B 6,648,778 -2,199 32,803 0.5% 14.5% 14.6% $19.16 0 0

New Center B 1,117,100 4,348 4,348 0.4% 20.9% 21.2% $18.20 0 0

Urban B 7,765,878 2,149 37,151 0.5% 15.5% 15.5% $18.97 0 0

Birmingham/Bloomfield B 1,445,860 14,445 16,630 1.2% 8.7% 9.3% $20.26 0 0

Dearborn B 2,100,626 -5,533 -1,713 -0.1% 50.3% 50.3% $14.69 0 0

Downriver B 404,475 547 412 0.1% 41.9% 41.9% $12.65 0 0

Farmington/Farmington Hills B 3,560,716 -24,686 -14,079 -0.4% 28.0% 28.1% $17.75 0 0

Macomb B 649,646 0 -17,926 -2.8% 15.5% 15.5% $17.07 0 0

Northern I-275 Corridor B 2,562,632 6,898 -65,472 -2.6% 16.2% 16.9% $19.31 0 0

North Oakland B 1,942,652 -18,282 -19,945 -1.0% 11.8% 11.8% $15.77 0 0

Royal Oak/Southeast Oakland B 638,607 -7,400 -6,567 -1.0% 11.1% 11.1% $15.80 0 0

Southern I-275 Corridor B 178,160 0 0 0.0% 0.0% 0.0% $0.00 0 0

Southfield B 10,020,452 -6,519 -735 0.0% 28.3% 28.5% $16.49 0 0

Troy B 8,546,565 -12,626 -87,856 -1.0% 26.2% 26.3% $17.08 0 0

Washtenaw B 2,309,002 -3,069 -101,627 -4.4% 9.0% 9.0% $20.90 0 0

Suburbs B 34,359,393 -56,225 -298,878 -0.9% 24.6% 24.7% $16.78 0 0

Detroit B 42,125,271 -54,076 -261,727 -0.6% 22.9% 23.0% $17.05 0 0

©2016 Jones Lang LaSalle IP, Inc. All rights reserved.For more information, contact: Aaron Moore | aaron.moore@am.jll.com