1. Roland George Investments Program

Bond Swap Recommendation

Adam Frocione

3/16/2015

Buy Candidate Overview

CHC Helicopter is one of the largest commercial operators of helicopters in the world based on revenue

and fleet size. The company operates 234 heavy and medium sized helicopters spanning six continents.

They have 70 bases which operate in roughly 30 countries. Revenue is reported in two segments:

helicopter services and heli-one. Helicopter services involve the transportation of employees to offshore

oil and gas customers, search and rescue, and emergency medical services. Oil and gas customers make

up roughly 88% of this segment, while the latter two primarily consist of government agency contracts.

Helicopter services account for 79.2% of total revenue. The second reporting segment is heli-one. It

accounts for 20.8% of revenue and consists of helicopter maintenance, repair and overhaul services.

These facilities are located in Norway, Poland, Canada, and the United States. The company has

experienced a significant decline in sales largely attributable to a high correlation with oil. They recently

retired five older models of helicopters and purchased an additional 22 to be outfitted with new

technology. CHC Helicopter is and has maintained a B+ credit rating. On October 1, 2014, Moody’s

upgraded the company’s outlook from stable to positive. Clayton, Dubilier, and Rice (CDR), a private

equity firm, invested roughly $600 million in the company. If they can demonstrate more sustainable cash

flow growth while decreasing their financial leverage below 5.5x, HELI could experience a ratings

upgrade.

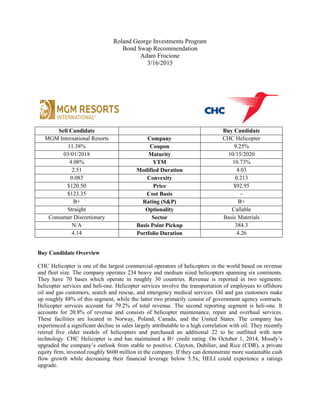

Sell Candidate Buy Candidate

MGM International Resorts Company CHC Helicopter

11.38% Coupon 9.25%

03/01/2018 Maturity 10/15/2020

4.08% YTM 10.73%

2.51 Modified Duration 4.03

0.083 Convexity 0.213

$120.50 Price $92.95

$123.35 Cost Basis -

B+ Rating (S&P) B+

Straight Optionality Callable

Consumer Discretionary Sector Basic Materials

N/A Basis Point Pickup 384.3

4.14 Portfolio Duration 4.26

2. CHC Helicopter is driven by two main factors: the price of oil and the general level of offshore

production and drilling activity. Volatility in the price of oil can cause companies to reconsider and

sometimes cut back on their capital expenditures due to decreases in their margins. The price of oil

largely sets production schedules for these companies which in turn determine how many employees and

crew changes they will need over a given period of time. HELI has experienced slowed revenue growth

over the last several quarters for three main reasons. The first being that oil prices recently plummeted

and resulted in companies scaling back their production schedules. The second reason is the company

recently purchased a 65,000 square foot hangar in Poland which will be used to do the majority of repairs

and maintenance in-house which will streamline margins and promote efficiency. Finally, HELI decided

to retire five different models ahead of schedule in order to keep up with new technology. They recently

entered into purchase agreements to add 22 new technologically advanced helicopters to their fleet. The

company has seen an increased debt to equity ratio largely in order to finance the purchases just

discussed. By upgrading their fleet of helicopters, CHC Helicopter has expanded their market share and

well positioned themselves for stability in the energy market.

Interest Rate Forecast

As evidenced by figure I below, the credit spread between US Treasury bonds and US corporate bonds

has been narrowing since 2010, indicative of improving conditions in the United States’ economy. US

gross domestic product grew at a rate of 2.4% in 2014. This figure is projected to continue growing at a

rate of 3.3% for 2015. Economic data has largely been improving with the unemployment rate in

February coming in at 5.5%, beating its forecast of 5.6%. Nonfarm payroll data from March shows that

295,000 jobs were added to the US economy. On June 19, 2013, Federal Reserve ex-chairman Ben

Bernanke suggested that if inflation followed a 2% target and the unemployment rate decreased to 6.5%

then the Federal Reserve would likely start raising interest rates. His successor, Janet Yellen, has said that

she will follow the same ideology.

The main economic indicator currently preventing a rate hike is inflation. The most recent inflation data

pegs the rate at 1.6%, inferior of the 2% target rate the Federal Reserve has hinted it will raise rates at.

The Consumer Price Index (CPI) has been marginally declining since October, experiencing -0.7%

growth in January. The CPI has recently been weighed down by falling oil prices. Projected stability to oil

prices should result in minimal change to the CPI which will keep inflation hovering around its current

level and postpone a rate hike. Since inflation has remained stable and even slightly depreciated, there is

no pressing reason to justify a rate hike. I predict that inflation will slightly rise over the course of the

year due to the eventual stability of oil prices which will result in less deflationary pressure to the CPI and

allow other sectors to bring inflation up. Interest rates will fluctuate roughly 25 basis points over the

course of the year and a rate hike will be postponed.

Figure I. Projected Yield Curve

3. On January 22, 2015, Mario Draghi, the president of the European Central Bank announced that they

would be launching an expanded asset purchasing program where €60 billion would be purchased per

month. This stimulus is planned to last through September 2016 and end with at least €1.1 trillion euros

on its books. The United States recently ended their quantitative easing program on October 29, 2014,

ending with $4.5 trillion in assets. The euro has seen its value depreciate against the dollar by 32.5% over

the last year. The dollar has seen significant upward momentum against the euro since August largely due

to a quickly growing US economy paired with a state of economic recovery in Europe. Further, Greece

recently began pulling themselves out of a massive hole. They recently came to an agreement with the

European Union partners to keep the country’s government solvent for the foreseeable future.

Analyzing what is going on in the Asian markets is very necessary to gauge a more complete

macroeconomic picture. China’s economy slowed down from 7.7% in 2013 to 7.4% in 2014. Gross

domestic product growth is estimated to be a slowing 6.8% for 2015. China has said before that 7%

growth is necessary to create enough jobs for China’s population. Japan is currently in the midst of a

quantitative easing program that consists of buying $80 trillion worth of bonds per year. The dollar has

largely separated itself from the yen in their currency pairing, appreciating 19.8% over the last year.

The United States’ economy is experiencing quick sustainable growth while several major economies in

the world are undergoing quantitative easing programs. The Eurozone is poised for minimal growth and

recently instituted its own program. China is seeing its growth slow down to unsustainable levels. Japan is

also in the midst of their own quantitative easing programs. The quick growth of the United States’

economy paired with a globally strengthening dollar simply does not justify a rate hike. Raising rates will

likely result in an even stronger dollar which will discourage exports.

Swap Rationale

By looking at figure II you can see that MGM is trading well below its average yield to maturity (YTM)

of 6.94%. The YTM has demonstrated profound cyclicality and typically decreases from December to

March until it spikes in June. MGM’s YTM is currently 4.08% so swapping the bond prior to an expected

yield increase in June makes sense for the portfolio. Looking at the YTM of CHC Helicopter, we see that

the average yield is 8.31%, well below its YTM today of 10.73%. From September to January YTM

rapidly increased largely due to falling oil prices. Further, MGM’s bond matures on 3/1/2018 so it is

behaving exactly as a bond of its maturity should. As oil continues to find stability it becomes apparent

from figure III that HELI’s yield is trending downward and will be more beneficial to our portfolio.

Figure II. MGM Yield Chart

4. Figure III. HELI Yield Chart

Indicative of strong gross domestic product projections, the United States’ economy is expected to

continue improving at a sustainable rate. I predict that the interest rate will fluctuate and ultimately

increase at year end by 25 basis points due to falling consumer price index numbers resulting in a

consistently low inflation rate largely due to deflationary pressure from falling oil prices. I decided to

increase interest rate risk because I do not believe interest rates will be interfered with by the Federal

Reserve until at least year end. MGM Resorts International has a fairly low modified duration of 2.51

when compared to that of CHC Helicopter at 4.03. By swapping these bonds total portfolio duration

increases from 4.14 to 4.26. Staying consistent with my interest rate forecast, I added 25 basis points to

the YTM of MGM Resorts International and CHC Helicopter to calculate the results for my most

probable scenario. As displayed in figure IV, by switching from MGM to HELI we will realize a 384.3

basis point pickup with a $49,839 resulting profit. This results in a wide spread of 629.8 basis points.

Figure IV. Horizon Analysis

Figure V shows that switching from consumer discretionary to the basic materials sector will benefit our

portfolio. The consumer discretionary yield spread has increased while the basic materials sector has

decreased resulting in a narrowing of the spread and room for profit by switching sectors. Companies in

5. the basic materials sector, specifically those with implications or a correlation to the price of oil recently

experienced their YTM’s increase significantly from September until January. Now that oil is closer to

stability and shedding some of its volatility we are seeing these yields regress back to their mean resulting

in significant gains to bond prices resulting in increased profit. Switching from consumer discretionary to

the basic materials sector will increase our YTM allowing us to realize profit from these higher but

decreasing yields.

Figure V. Sector Comparison

Fair Value for MGM International Resorts

In order to calculate a fair value for MGM International Resorts I found three comparable bonds that

demonstrated similar characteristics to MGM. I then took an average of the comparable bonds’ yields to

maturity which resulted in 4.10%. I subtracted this figure from MGM’s YTM and found a yield spread of

-0.06%. I multiplied the spread by negative MGM’s modified duration and found that the company is

overvalued by 14.2 basis points. This figure is right in line with my expectations, as I had anticipated that

MGM would be either fairly priced or overvalued. The calculated fair value for MGM Resorts

International further solidifies why I think we should swap the bond for CHC Helicopter.

Mispricing = duration * change in interest rate

Mispricing = 2.51 * -0.06%

Mispricing = 14.2 Basis Points

I also utilized the Bloomberg fair value function which compared MGM to an interpolated B value curve

and found that Bloomberg has MGM overvalued by 25.5 basis points. The fair value function plots the

yield of MGM against an interpolated yield curve of similar rating. I then derived that the spread was 25.5

basis points, signifying an overvaluation.

6. Company

MGM International

Resorts

Standard Pacific

Corp

American

Airlines

United Continental

Holdings

Coupon 11.38% 8.38% 6.13% 6.38%

Maturity 3/1/2018 5/15/2018 7/15/2018 6/1/2018

YTM 4.04% 3.76% 4.51% 4.02%

Modified

Duration

2.51 2.743 2.97 2.85

Convexity 0.083 0.095 0.108 0.101

Price $120.50 $113.62 $104.94 $107.00

Rating B+ B+ B+ B+

Optionality Straight Straight Straight Straight

Sector

Consumer

Discretionary

Consumer

Discretionary

Consumer

Discretionary

Consumer

Discretionary

Fair Value for CHC Helicopter

In order to calculate a fair value for CHC Helicopter I found three comparable bonds that demonstrated

similar characteristics to HELI. I then took an average of the comparable bonds’ yields to maturity which

resulted in 9.96%. I subtracted this figure from HELI’s YTM and found a yield spread of 0.77%. I

multiplied this spread by negative HELI’s modified duration and found that the company is undervalued

by 310.2 basis points. Similarly, this figure is right in line with my basis point pickup anticipated from

adding 25 basis points to each company’s yield of 384.3 basis points. The calculated fair value for CHC

Helicopter is very close to the pickup that would be received by swapping bonds under my most probable

scenario and further demonstrates why this recommendation would be highly beneficial to the portfolio.

Mispricing = duration * change in interest rate

Mispricing = 4.029 * 0.77%

Mispricing = 310.2 Basis Points

I also utilized the Bloomberg fair value function which compared HELI to an interpolated B value curve

and found that Bloomberg has HELI undervalued by 499.1 basis points. The fair value function plots the

yield of MGM against an interpolated yield curve of similar rating. I then derived that the spread was

499.1 basis points, signifying an undervaluation.

Company CHC Helicopter

Graftech

International

First Quantum

Minerals

Grupo Papelero

Scribe

Coupon 9.25% 6.38% 6.75% 8.88%

Maturity 10/15/2020 11/15/2020 2/15/2020 4/7/2020

YTM 10.73% 10.79% 9.13% 9.96%

Modified

Duration

4.029 4.376 4.01 3.804

Convexity 0.213 0.24 0.197 0.188

Price $120.50 $81.63 $90.75 $95.75

Rating B+ B+ B+ B+

7. Optionality Callable Callable Callable Callable

Sector Basic Materials Basic Materials Basic Materials Basic Materials

Interest Rate Stress Test

I performed an interest rate stress test in which I manipulated the yield of each bond to simulate the likely

impact that a similar movement in interest rates would have upon the bonds’ yields to maturity. I did this

by generating 42 probable scenarios and adding or subtracting the expected interest rate movement to

each yield. I then performed a horizon analysis in which I tested swapping the bonds with the yields of

each respective scenario. This testing was very important to understand how the bonds move in relation to

their spread as well as how sensitive the yields are to interest rate changes and their resulting impact upon

the portfolio. The results of my interest rate stress test are displayed below.

MGM HELI Spread MGM YTM HELI YTM Net P&L BPS

No Move No Move 629.8 4.437 10.735 $ 53,459 412.1

No Move Down 25 604.8 4.437 10.485 $ 61,936 477.3

No Move Down 50 579.8 4.437 10.235 $ 70,521 543.4

No Move Down 75 552.1 4.437 9.985 $ 80,146 617.3

No Move Up 25 654.8 4.437 10.985 $ 45,049 347.4

No Move Up 50 679.8 4.437 11.235 $ 36,746 283.4

No Move Up 75 704.8 4.437 11.485 $ 28,533 220.1

Up 25 No Move 604.8 4.687 10.735 $ 58,235 448.9

Up 25 Down 25 579.8 4.687 10.485 $ 66,726 514.2

Up 25 Down 50 554.8 4.687 10.235 $ 75,311 580.2

Up 25 Down 75 529.8 4.687 9.985 $ 83,992 646.9

Up 25 Up 25 629.8 4.687 10.985 $ 49,839 384.3

Up 25 Up 50 654.8 4.687 11.235 $ 41,535 320.3

Up 25 Up 75 679.8 4.687 11.485 $ 33,323 257

Up 50 No Move 579.8 4.937 10.735 $ 62,993 485.5

Up 50 Down 25 554.8 4.937 10.485 $ 71,483 550.8

Up 50 Down 50 529.8 4.937 10.235 $ 80,068 616.7

Up 50 Down 75 504.8 4.937 9.985 $ 88,750 683.4

Up 50 Up 25 604.8 4.937 10.985 $ 54,596 420.9

Up 50 Up 50 629.8 4.937 11.235 $ 46,293 357

Up 50 Up 75 654.8 4.937 11.485 $ 38,080 293.7

Up 75 No Move 554.8 5.187 10.735 $ 67,724 521.9

Up 75 Down 25 529.8 5.187 10.485 $ 76,214 587.1

Up 75 Down 50 504.8 5.187 10.235 $ 84,799 653.1

8. Up 75 Down 75 479.8 5.187 9.985 $ 93,481 719.8

Up 75 Up 25 579.8 5.187 10.985 $ 59,327 457.3

Up 75 Up 50 604.8 5.187 11.235 $ 51,023 393.4

Up 75 Up 75 629.8 5.187 11.485 $ 42,811 330.1

Down 25 No Move 654.8 4.187 10.735 $ 48,639 375

Down 25 Down 25 629.8 4.187 10.485 $ 57,130 440.4

Down 25 Down 50 604.8 4.187 10.235 $ 65,715 506.4

Down 25 Down 75 579.8 4.187 9.985 $ 74,396 573.2

Down 25 Up 25 679.8 4.187 10.985 $ 40,243 310.4

Down 25 Up 50 704.8 4.187 11.235 $ 31,939 246.4

Down 25 Up 75 729.8 4.187 11.485 $ 23,727 183.1

Down 50 No Move 679.8 3.937 10.735 $ 43,800 337.8

Down 50 Down 25 654.8 3.937 10.485 $ 52,291 403.1

Down 50 Down 50 629.8 3.937 10.235 $ 60,876 469.2

Down 50 Down 75 604.8 3.937 9.985 $ 69,558 536

Down 50 Up 25 704.8 3.937 10.985 $ 35,404 273.1

Down 50 Up 50 729.8 3.937 11.235 $ 27,100 209.1

Down 50 Up 75 754.8 3.937 11.485 $ 18,888 145.8

The previous table shows a stress test on potential interest rate movements on both bonds’ yields. The

most likely scenarios are italicized and were selected based upon my interest rate forecast. The spread for

my most likely scenarios only incorporates a basis point increase due to volatility and fluctuations among

the market up to 50 basis points while allowing for the interest rate to drop 25 basis points. Proportional

to my interest rate forecast, my most probable scenario anticipates a 25 basis point increase to the interest

rate resulting in a 25 basis point increase to both company’s yields generating a 384.3 basis point pickup

or $49,839 in profit. The stress test generated no negative scenarios and found an average basis point

pickup of 431.7 basis points while accruing $56,016 of profit. As evidenced by figure VI the historical

spread has been relatively stable until roughly September 2014 when falling oil prices significantly

increased CHC Helicopter’s YTM and boosted the spread. It is also very important to analyze what the

potential impact would be if my forecast were completely wrong. To project my most unlikely scenario I

decided to decrease MGM’s YTM by 50 basis points and decrease HELI’s YTM by 75 basis points. Even

in my least anticipated scenario the swap results in a 536 basis point increase equal to a profit of $69,558.

9. Figure VI. Spread Summary

Source of Swap Profit

BPS Pickup = Interest Rate + Credit Risk + Sector + Optionality + Mispricing

Interest Rate Pickup: +152.6

I found a bond with very similar characteristics to MGM Resorts International, except with duration

comparable to that of CHC Helicopter. I ran a horizon analysis and added 25 basis points to each bonds’

yield in order to stay consistent with my interest rate forecast. As evidenced by increasing the duration

from 2.51 to 3.79, I realized a 152.6 basis point pickup by raising duration. Increasing our risk appetite

during a time when low inflation and consistently improving unemployment levels are present in the

economy should boost returns.

Sell Candidate Buy Candidate

MGM International Resorts Company Tri Pointe Holdings

11.38% Coupon 4.38%

3/1/2018 Maturity 6/15/2019

4.04% YTM 4.64%

2.51 Modified Duration 3.79

0.083 Convexity 0.171

$120.50 Price $98.99

B+ Rating B+

Straight Optionality Straight

Consumer Discretionary Sector Consumer Discretionary

Basis Point Pickup 152.6

10. Credit Risk Pickup: +0

Both MGM Resorts International and CHC Helicopter currently have a B+ credit rating. While we would

not gain any basis points from the swap, it is important to do a stress test to understand how significantly

credit downgrades could affect the company. I chose three bonds that each varied in their credit rating but

maintained similar characteristics to CHC Helicopter. I then subtracted the comparable companies’ yields

to maturity from that of CHC and found the yield change. I multiplied the resulting figures by CHC’s

negative modified duration and found the loss or gain that would be realized from incurring the

corresponding yield change. Moody’s recently mentioned that if the company can demonstrate more

sustainable cash flow growth while decreasing their financial leverage below 5.5x then they could

possibly experience a ratings upgrade. Conversely, if Moody’s financial leverage were to exceed 7x for

an extended period of time then they could face a potential downgrade. The results from my scenarios are

depicted below. If a single downgrade were to occur, HELI would only lose 63 basis points worth of

profit from changes to its yield to maturity. Conversely, if the company is able to improve its efficiency

and generate more sustainable cash flow growth then they could reap the results of a credit upgrade. In

projecting this scenario I found that a credit rating upgrade would result in a 13.26% gain in profit. CHC

Helicopter is far more sensitive to credit upgrades than downgrades, making them a much safer play.

CHC Helicopter Grupo Idesa Iamgold Corp TPC Group

Coupon 9.25% 7.88% 6.75% 8.75%

Maturity 10/15/2020 12/18/2020 10/1/2020 12/15/2020

YTM 10.73% 7.44% 10.89% 11.73%

Modified

Duration

4.03 3.86 4.22 4.20

Convexity 0.21 0.19 0.23 0.23

Price $92.95 $102.38 $83.12 $87.75

Rating B+ BB- B B-

Optionality Callable Callable Callable Callable

Sector Basic Materials Basic Materials Basic Materials Basic Materials

Credit Rating Yield Change Loss/ Gain in Profit from Yield Changes

BB- -3.29% 13.26%

B 0.16% -0.63%

B- 1.00% -4.04%

Sector Pickup: +20.2

I chose to compare MGM International Resorts with United States Steel in order to determine how many

basis points would be picked up by switching sectors. Both bonds have very similar characteristics

except, like CHC Helicopter, United States Steel belongs to the basic materials sector. In order to stay

consistent with my interest rate forecast I ran a horizon analysis and added 25 basis points to each bonds’

yield. I found that switching sectors will contribute roughly 20.2 basis points to my overall pick up.

11. Sell Candidate Buy Candidate

MGM International Resorts Company United States Steel

11.38% Coupon 7.00%

3/1/2018 Maturity 2/1/2018

4.04% YTM 4.74%

2.51 Modified Duration 2.58%

0.083 Convexity 0.083

$120.50 Price $106.00

B+ Rating B+

Straight Optionality Straight

Consumer Discretionary Sector Basic Materials

Basis Point Pickup 20.2

Optionality Pickup: +265.4

I compared MGM Resorts International with Pacific Emerald PTE in order to determine how many basis

points we would be compensated for switching sectors. Both of these bonds have very similar

characteristics except, similar to HELI, Pacific Emerald PTE is callable. Being sure to stay consistent

with my interest rate forecast I added 25 basis points to each company’s yield to simulate a 25 basis point

increase to the interest rate. I found that in switching to optionality I picked up 265.4 basis points. It is

important to consider that in gaining this pickup we are taking on the risk of the bond being called. The

buy candidate (CHC Helicopter) bond is to be called if the price is at $104.63 on October 15, 2015. While

the possibility remains, it is unlikely considering the bond currently trades at $92.95.

Sell Candidate Buy Candidate

MGM International Resorts Company Pacific Emerald PTE

11.38% Coupon 9.75%

3/1/2018 Maturity 7/25/2018

4.04% YTM 7.72%

2.51 Modified Duration 2.81

0.083 Convexity 0.100

$120.50 Price $105.88

B+ Rating B+

Straight Optionality Callable

Consumer Discretionary Sector Consumer Discretionary

Basis Point Pickup 265.4

Mispricing: -53.9

After conducting several different methods to find the fair value of each bond, I found that MGM is

overvalued by 14.2 basis points and HELI is undervalued by 310.2 basis points. When I compared my

12. raw calculations with those of the Bloomberg fair value function I found that my projections were right in

line with what other analysts are saying. In swapping these bonds we would be exchanging a company

possessing a low yield (MGM) with a company possessing a high yield that is regressing back toward its

mean (HELI).

Sources of Swap Profit

I have conducted a number of simulations, stress tests, and comparable analyses to determine how much

pickup I am generating from each source of the swap. A bond with modified duration comparable to that

of CHC Helicopter was used to determine how much of a pickup I would receive from interest rate risk. I

performed a stress test to determine relative impacts if the bond were to receive a change in credit rating

in order to determine credit risk. A comparable bond was found and put through horizon analysis in order

to determine what the pickup would be from changing sectors. Finally, I found a comparable bond to

MGM with the same optionality as HELI In order to determine how much of a pickup would be generated

from switching maturity types. The chart below displays my results.

Sources of Swap Profit (Basis Points)

Interest Rate Risk 152.6

Credit Risk 0

Sector Risk 20.2

Optionality Risk 265.4

Mispricing -53.9

Total 384.3

Credit Analysis

Analyzing the credit rating of both companies is very important when determining whether to make a

swap or not. MGM International Resorts currently has a credit rating of B+ from S&P and B3 from

Moody’s. This is slightly different than that of CHC Helicopter which has a credit rating of B+ from S&P

and a B1 from Moody’s. On October 1, 2014, Moody’s upgraded HELI’s previous rating of stable to

positive. This was largely due to the approval of a $600 million private placement issuance of preferred

shares by private equity firm Clayton, Dubilier & Rice. If CHC Helicopter can demonstrate more

sustainable cash flow growth while decreasing their financial leverage below 5.5x they could see an

upgrade. By getting into HELI we take on more risk due to higher financial leverage but we also get a

slight ratings and outlook upgrade with the swap. Conversely, if market conditions are poor and result in

less activity and increase financial leverage beyond 7x for an extended period of time then the company

could face a downgrade.

Generating revenues has been a problem for both MGM and HELI as of recently. MGM’s most recent

quarterly revenues were -4% year-over-year while HELI’s were up 4% with their next earnings due to be

released on March 16, 2015. HELI has had difficulty translating their top line to the bottom line, resulting

in a net loss for the past several years. This business has significant capital expenditures and has been

actively growing their fleet of helicopters which now total 234. In April 2014 the company purchased a

65,000 square foot hangar in Poland which will predominantly be used by heli-one to promote efficiency

all along the supply chain. By gaining market share and streamlining their efficiency HELI is well

positioned to begin generating sustainable cash flows. Year-over-year revenue growth was positive for

quarters 1 and 2 of 2015 being 11% and 3.3%. Projected third quarter revenues will likely end the trend of

13. positive year-over-year growth, as falling oil prices caused many oil companies to scale back their

production and thus need for employee transportation. HELI currently has $107.9 million in cash while

recently having a $600 million private placement of preferred shares approved. Further, on January 23,

2014, CHC Helicopter entered into a senior secured revolving credit facility for $375 million. The

company was also able to raise $317.8 million when it had its IPO on the New York Stock Exchange on

the same day.

MGM Resorts Resorts & Casinos CHC Helicopter Oil & Gas Equipment

Total Debt $14.2 B - $1.53 B -

Debt / Equity 3.16 4.4 4.49 0.77

Coverage Ratio 1.5 2.03 0.2 2.63

Current Ratio 0.89 1.19 0.95 1.64

ROA -0.57% -2.24% 1.45% 1.41%

Profit Margin -1.55% 0.10% -18.63% 1.71%

When contemplating the swap it is important to analyze how both companies’ ratios compare against each

other and their respective industries. MGM has a 3.16 debt to equity ratio which is less than 4.49 of

HELI. While HELI has a higher ratio it is because they have more capital expenditures and have recently

committed to buying 22 new helicopters. CHC Helicopters is more efficient at generating earnings with

its assets than MGM and both comparable industries as evidenced with a 1.45% return on assets. HELI’s

current ratio of 0.95 is better than 0.89 of MGM. Neither of these ratios is fairly impressive but this is

only the first quarter that HELI has been below 1. While HELI has more debt and a much lower coverage

ratio, it is due to high financial leverage in order to cover significant capital expenditures to increase fleet

size and promote efficiency. HELI is better positioned for the future than MGM and offers a higher yield

as companies highly correlated with oil prices already took their hit and are now priced much cheaper.

Conclusion

Swapping MGM Resorts International for CHC Helicopter would help ensure that our performance

remains in line with the investment policy statement objective of maximizing total return. I predict that

interest rates will likely increase by 25 basis points simply due to market volatility since there is

essentially no reason to merit a rate hike. The United States’ economy continues to expand without

demonstrating any negative side effects and thus should not result in any government intervention. Due to

my interest rate forecast I have decided that increasing our modified duration and exposure to interest rate

risk will be beneficial to our portfolio during the workout period. Projected stability in oil prices should

result in higher revenues for HELI which will allow them to pay down larger volumes of debt and

improve their ratios. Switching from consumer discretionary to the basic materials sector will only help to

benefit our portfolio. HELI’s yield has significantly risen since September because of falling oil prices. Its

maturity date paired with projected stability in oil prices should result in the yield to maturity regressing

back toward its mean. By swapping these two bonds we will pick up 384.3 basis points or $49,839. I

highly recommend that the Roland George Investments Program swap MGM Resorts International’s bond

for CHC Helicopter’s bond.