2. April 7, 2011 Global Strategy

Investment Recommendation 2

S&P Equity Research has a positive view on the global energy sector and as

of Apr. 1, 2011, we are Overweight the sector in all three regions (US, Europe

and Asia).

Within the sub-industries, we have a preference for the integrated oil & gas

and exploration & production companies. We see underlying strength in oil

prices underpinned by improving global demand as conducive for the

sector’s income performance over the near to mid term.

For Greater China, our preference lies with PetroChina, given the company’s

upstream leverage, balanced integrated operations, and its status as a

potential beneficiary of a long-touted gas price reform. We also like E&P

player CNOOC Ltd, but given its strong outperformance YTD, we would

recommend investors to buy on dips.

A quick resolution to MENA conflicts could send near term oil prices down

and lead to a pullback in energy sector share prices but the improving

demand outlook should provide support.

An increasingly pertinent issue for Greater China O&G stocks is rising cost

pressures; given the regulated nature of China’s refined product market,

pricing adjustments tend to lag increases in crude prices. This explains our

cautious view on Sinopec, which we see will incur refining losses over the

short-term as crude prices remain elevated.

While the US gas market remains soft, we see a more stable gas market

globally, particularly with the potential interest in natural gas and LNG for

thermal power generation. This follows recent worries over radiation

contamination in the aftermath of the Great Tohoku earthquake’s impact on

Japan’s Fukushima Daiichi nuclear power plant. Greater concern on the

safety of nuclear power will also boost demand for natural gas in China, in

our view, further pushing the agenda for pricing reform.

Our global views on the drilling and fabrication segments are more cautious.

While the higher prices should boost confidence, capacity pressure remains

on rig day rates. Still, we expect continuing strength in offshore China

activity, signified by CNOOC Ltd’s +55% YoY increase in planned capex in

2011, to result in an increase in dayrates for 2011, potentially benefiting

offshore services player COSL.

Risks to our recommendations and risks would come from slowdown in US

economic growth that dampens the outlook for global demand. Higher than

expected cost pressures that cannot be passed on will also dampen our

earnings expectations. The sector is also subject to government regulatory

risk particularly in the form of increased windfall taxes and heightened

environmental charges.

Standard & Poor’s Equity Research

3. April 7, 2011 Global Strategy

Outlook: Oil Market 3

Fundamentals

USD115/bbl level (Brent), indicates to us a world uncertain of itself. On the one

hand, worries over a potential supply disruption from MENA remain; on the

Rising prices tempered by inflation

other, a prolonged and significant rise in crude oil prices could ultimately push

impact worries

back the global economy into a recession and result in lower energy demand.

S&P Economics thinks a USD10/bbl rise in oil prices would lower US real GDP by

0.5% after a two-year period.

Oil markets tightened significantly in 4Q10… …and OECD inventories are approaching five-year average

mbpd USD/bbl mbpd

5 160 2,900

4 140 2,800

3 2,700

120

2 2,600

100

1 2,500

80

0 2,400

Jan-01

Jan-03

Jan-05

Jan-07

Jan-09

Jan-11

60

-1 2,300

40 2,200

-2

-3 20 2,100

Jan-01

Jan-04

Jan-07

Jan-10

-4 0

Implied stock draws WTI (RHS) OECD commercial inventories Five-year average

Source: EIA, S&P Equity Research estimates Source: EIA, S&P Equity Research estimates

To a certain extent, we believe there is a fundamental basis for the current crude

Market began to tighten in Sept 2010 run-up. Oil fundamentals had begun to shift as early as September 2010. As the

global economy rebounded, there was a significant increase in demand for oil,

especially in 2H10, but the supply response from OPEC lagged, hence pushing up

crude oil prices (excluding WTI, which is plagued by high Cushing inventories).

Implied stock draw for September 2010, according to data from the International

Energy Agency (IEA), was the largest since November 2007, indicating a

significant tightening of the global crude demand & supply. Events in MENA

further aggravated the tightening market, as market participants began pricing in

a risk premium on a potential MENA supply disruption.

Standard & Poor’s Equity Research

4. April 7, 2011 Global Strategy

OPEC spare capacity off its seven-year high… … leading to potentially the highest stock draw since 4Q07 4

mbpd USD/bbl Net stock draw, mbpd

8 160 3.0

7 140 2.5

2.0

6 120

1.5

5 100

1.0

4 80

0.5

Five-year average

3 60

0.0

1Q06

4Q06

3Q07

2Q08

1Q09

4Q09

3Q10

2Q11F

1Q12F

4Q12F

2 40

-0.5

1 20

-1.0

0 0 -1.5

Jan-94

Jan-97

Jan-00

Jan-03

Jan-06

Jan-09

-2.0

OPEC Spare Capacity WTI (RHS) US Other OECD Non-OECD

Source: EIA, S&P Equity Research estimates Source: EIA, Bloomberg S&P Equity Research estimates

S&P Global Crude Oil Price Outlook

Based on a combination of data from EIA, IHS Global Insight and S&P Equity

Research estimates, we expect 2011 oil consumption growth to average about

1.51 mbpd (+1.7% YoY), while 2012 oil consumption is expected to increase by

1.69 mbpd (+1.9% YoY). In 2010, much of the growth was accounted for by non-

OECD countries, while the US was the only OECD country that saw significant

growth.

We expect this trend to continue into 2011-12, as non-OECD countries, including

China, Brazil and countries in the Middle East region, are expected to lead world

Growth to be led by non-OECD

economic growth, albeit at a slower pace vs. 2010. Asia Pacific ex-Japan countries

countries, in particular China, Brazil and

are likely to record GDP growth rates double that of the US and Eurozone, which

Mid-East countries

will remain hampered by slow consumption growth and high unemployment.

OECD countries are not expected to show any significant growth in oil demand

between now and 2012.

Oil supply is expected to increase 0.97 mbpd (+1.1% YoY) in 2011, vs. a 2.12

mbpd growth in 2010. The slower growth is due a decline in OECD production, on

2011 oil supply growth crimped by

declines in Canadian and North Sea production. US production is expected to see

OECD production declines…

a slight YoY contraction due to the lingering effects of the GoM drilling

moratorium, while Mexico is expected to see a sharp 7.3% YoY decline in

production due its ageing oilfields and infrastructure. Non-OECD production is

expected to pick up the slack, with OPEC incremental production driving much of

the YoY growth.

OPEC production is expected to grow by 0.8 mbpd in 2011 (mainly from

unregulated non-crude production such as NGL), with much of Libya’s lost oil

…and aggravated by lost Libyan capacity

production capacity (total production capacity of 1.8 mbpd) to be offset by

Standard & Poor’s Equity Research

5. April 7, 2011 Global Strategy

inventory drawdown and higher production from other OPEC members. 2012

5

production is expected to increase by a bumper 2.19 mbpd, mainly on higher

OPEC production as lost production capacity in Libya come back online.

World YoY demand and supply balance

A tighter energy market in 2011 on

mbp

rebounding demand and supply shocks

3.0

2.5

2.0

1.5

1.0

0.5

0.0

2006 2007 2008 2009 2010 2011F 2012F

-0.5

-1.0

-1.5

-2.0

Incremental supply Incremental demand

Source: EIA, S&P Equity Research estimates

Overall, we see a relatively tight year for crude oil demand & supply in 2011, and

Overall, a tight year ahead, before supply

inventory drawdowns should be fairly high during the year, on Libyan production

eases in 2012

cuts and higher demand from quake-afflicted Japan. OPEC spare capacity is

expected to decline to about 4 mbpd by end-2011, the lowest level since July

2009, indicating a significantly tighter market. Barring any further geopolitical

disruptions, the situation should ease in 2012 as lost Libyan production comes

back online and/or other OPEC countries boost supply. Our 2011 crude price

assumption for WTI currently stands at USD99/bbl for 2011 and USD96/bbl for

2012.

Standard & Poor’s Equity Research

6. April 7, 2011 Global Strategy

Potentially Tighter Supply – Heightened MENA Risks

6

Political flare ups in the Middle East that impact supply send global oil prices up

Oil prices reflect supply risks and stock markets down are not new. There have been around five such major

events since 1967. In fact, the big 1973/1974 stock market crash and recession was

triggered in part by the Yom Kippur War that led to a mass embargo in oil exports

to then Arab unfriendly states by Arab members of OPEC. For the most part,

however, the shortfall in supplies is offset by other producing countries, albeit

not without a significant oil price rise in the short term.

We see the latest events to have a similar path in terms of impact to the market to

the more recent oil supply shocks of 1990 and 2000. These had more subdued

impact relative to the 1973 and 1979 supply shocks, according to economists,

because of reduced US dependency on oil and the availability of stock piles. We

also don’t expect political upheavals to spread to key oil producers – namely Iran,

Saudi Arabia and the United Arab Emirates. Ongoing Yemeni and Syrian protest

should have little fundamental impact while Bahrain is a small, albeit high

quality, producer.

According to a Mar. 15 report from the IEA, OPEC spare capacity was estimated at

around 4.28 mbpd. Platts quotes sources as saying that Libyan production has

Current OPEC spare capacity may be

trickled to 100,000-120,000 bpd. Libya normally produces 1.6 mbpd of

below 3 mbpd, lowest level since 2008

predominantly light, sweet crude or around 2% of global production. This would

mean that OPEC’s EIA estimated spare capacity should now be reduced to around

2.8 mbpd from over 4 mln bpd in February, the lowest level since 2008. At the

peak oil price of USD147/bbl, it was estimated that spare capacity at the time was

around 1.5 mbpd. Current spare capacity, therefore, remains relatively

comfortable above 2003-2008 levels.

We believe current oil prices therefore reflect heightened risk of further supply

shortfalls, more so than actual supply:demand fundamentals. But it should be

Oil prices are therefore reflecting lesser

noted that OPEC excess capacity tends to be in heavy, sour crude which is not a

supply flexibility, raising risk, implying

direct substitute for light, sweet crude and not all refineries can adapt to take

upside to our oil price forecast

sour crude. Also, oil prices are also reacting to economic data showing a stronger

US demand recovery. We note that as current OPEC capacity is below our base

case scenario of 4 mbpd, if Libyan production remains compromised, there may

be upside to our oil price assumptions.

Japan’s Great Tohoku earthquake is also likely to add demand factors in the

short-mid term as the country relies more heavily on thermal power plants to

Demand may also rise more than

make up for the closures at some of its nuclear power plants. Platts’ sources

expected – Japan to import more crude

indicate that they expect utility company Tokyo Electric Power Corp. (TEPCo)

and fuel oil for power generation

crude and fuel oil consumption to jump 60% in April from March levels. This has

sent the prices of Asian burning oils – namely Minas – soaring.

Standard & Poor’s Equity Research

7. April 7, 2011 Global Strategy

Higher Crude Prices & the Impact on China Energy Players

7

Stronger YoY crude oil prices benefit upstream-heavy players like PetroChina and

Upstream-heavy operators to benefit, but CNOOC Ltd. Despite the latter’s pure upstream exposure, and hence greater

CNOOC Ltd may see ASP dilution on leverage to oil prices, we see the impact of higher oil prices on CNOOC Ltd to be

increased Bridas contribution somewhat diluted by its Argentinian arm, 50%-owned Bridas, especially upon the

consolidation of the additional 60% stake in Pan American Energy (Bridas’ main

asset) purchased from BP plc in Nov 2010. We estimate Argentinian crude pricing

(nett of sales tax and Petroleo Plus tax credits) to be some USD12-15/bbl below

WTI prices, and this will dilute CNOOC Ltd’s ASPs from 2011 onwards, in our

view.

With Asian gas prices generally moving in line with crude oil (vs. depressed

Henry Hub natural gas prices which are more linked to local US demand/supply

Higher international gas prices to spur

conditions), and a tightening in the Asian spot LNG market as Japan deals with

domestic gas price reform?

the impact of the Tohoku earthquake, we expect increasing pressure on the

Chinese government to revise its pricing formula on natural gas, which at this

point is fixed by government decree. Other push factors include the setting up of

at least another 37.6 bl cu m annual LNG importing capacity till 2014,

PetroChina’s ramp-up of gas imports via the WEP2 pipeline (the company targets

to increase natural gas production to 50% of total oil equivalent production by

2015, from 30% currently) and increasing demand for the fuel (we estimate China

consumed some 110 bln cu m in 2010, and this should increase to 135-140 bln cu

m in 2011).

Still, increasing inflationary concern is likely to be a weighty counterbalance to

any potential pricing reform, which will push gas costs higher and eventually hit

Or will inflationary pressures hold sway?

the population via higher power, heating, fertiliser and food costs. Hence, in

place of a general increase in wellhead gas price, we see the potential for a one-

off subsidy by the government in 2011 to compensate PetroChina’s gas pipeline

business (similar to that granted to refiners in 2008), before a long-term solution

is put in place. Over the longer term, reform of the gas pricing mechanism

(potentially set at the end-user level via a reference basket of alternative fuels,

with a net-back formula used to calculate wholesale and wellhead gas prices,

according to industry sources) will benefit PetroChina, given its dominance in gas

production, and will also increase the monetisation of its unrivalled gas

distribution network.

The combination of higher input costs and price controls on the end product will

also hit China’s refiners, although the impact will be lessened by the refined

Refining losses likely in 2011

product price mechanism currently in place. The mechanism allows for price

adjustments to be made by the government based on a specified formula, but as

can be seen in the two adjustments already made since the beginning of the year

(including the 4.9%-5.6% increase for diesel and gasoline respectively, announced

yesterday), in practice the adjustments can lag crude prices and hence depressing

short-term margins. We expect both PetroChina and Sinopec’s refining arm to

suffer losses this year, although we do not expect the quantum to match 2008’s

losses.

We expect marketing profits for China’s integrated oils to perform in line China’s

economic growth, which we expect to reach 9.4% in 2011 (vs. 10.3% in 2010).

Marketing and chemical profits should

Chemical demand should also grow in line with the economy, although margins

grow in line with economy

may be under some pressure, due to increasing feedstock costs.

Standard & Poor’s Equity Research

8. April 7, 2011 Global Strategy

Higher crude prices will also boost confidence in oilfield services companies,

8

although we believe the key driver for companies such as COSL remains the

Higher crude prices to boost confidence

bullish prospects for offshore China. This will be driven by higher capex

in oilfield services companies

spending, mainly from parent CNOOC Ltd, and focusing on higher exploration

work (+45% YoY increase in exploration budgets) and deepwater development.

Strong M&A Environment to Continue Despite Volatility

Global upstream transacted value for 2010 rose to USD228.2 bln, breaching the

Global upstream M&A value reached a previous all time high of USD200.7 bln set in 1998, with much of the transactions

new record of USD228.2 bln in 2010 being done at the asset level and led by national oil companies (NOCs), and

mainly from China. Cross-border NOC & sovereign wealth fund (SWF)

transactions reached close to USD44.2 bln in our estimates, or 19% of total global

M&A transaction in 2010, while Chinese NOC’s were involved in USD24.6 bln

worth of M&A deals, or 11% of the total global transaction in 2010.

Given the strength in crude prices in 2010 vs. 2009, worldwide deal pricing for P2

(proved + probable) increased substantially, up 18% YoY to USD6.55/boe, based

Implied values increased in line with

on data from IHS Herold. North American pricing dipped from USD16.45/boe in

crude price strength

2009 to USD10.50/boe in 2010, but this was skewed by opportunistic purchases of

conventional gas assets in Canada.

NOC/SWF purchases driving worldwide M&A… … as implied values climb on higher crude prices

USD/boe

Chinese

NOC 18

11%

16

Other

NOC/SW Fs 14

9%

12

10

8

6

4

2

0

Other 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

buyers

World US

80%

Source: IHS Herold, S&P Equity Research estimates Source: IHS Herold, S&P Equity Research estimates. Values are based on 2P reserves.

Despite increasing crude price and geopolitical volatility, we expect global M&A

Expect continuing strength in global activity to continue to remain strong, driven by ample liquidity and cashed-up

M&A in 2011 balance sheets at oil majors and NOCs, especially those with large oil exposures

worldwide and/or gas exposure outside North America. Further, slow organic

reserve growth and, especially for NOCs, increasing energy security concerns

amidst greater resource nationalism and restricted access to acreage will

continue to spur the global search for available assets.

Standard & Poor’s Equity Research

9. April 7, 2011 Global Strategy

9

Global upstream M&A breaches previous record on ample liquidity

USD mln

250,000

200,000

150,000

100,000

50,000

0

2011 YTD

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Source: IHS Herold, S&P Equity Research estimates

Top 10 M&A deals by transaction value in 2010

Transaction Reserve Reserve Implied

value (USD Value size value

Date Buyer Seller Deal level Region bln) (USD bln) (mmboe) % gas R/P ratio (USD/boe)

Sep-10 Petrobras Brazil Government Asset LatAm 42.5 42.5 5,000 0% N/A 8.50 ^

Aug-10 Vedanta Cairn Energy Corporate Asia Pacific 9.9 8.0 204 1% 12.5 39.03 *

Nov-10 Bridas, CNOOC Ltd BP plc Asset LatAm 7.1 7.1 858 33% 17.3 8.23

Mar-10 AFK Sistema Sberbank Rossii Corporate FSU 6.1 4.6 1,300 0% 6.6 3.53

May-10 Royal Dutch Shell East Res, KKR Corporate United States 4.7 4.3 2,000 100% N/A 2.16 #

Apr-10 Apache Corp Mariner Energy Corporate United States 4.7 3.4 181 53% 9.6 18.76

Apr-10 Sinopec Group ConocoPhillips Asset Canada 4.7 3.5 248 0% 29.5 14.02

Nov-10 Chevron Corp Atlas Energy Corporate United States 4.3 1.5 141 99% 27.9 10.33

Oct-10 Sinopec Group Repsol YPF Asset LatAm 4.3 4.0 480 25% N/A 8.24 ^

Mar-10 PetroChina, Shell Arrow Energy Corporate Asia Pacific 3.9 1.9 590 100% 183.1 3.24 *

Source: IHS Herold, S&P Equity Research estimates. Reserve size and metrics based on 1P reserves, unless otherwise noted. *based on 2P reserves. ^based on contingent resources.

#based on total recoverable reserves.

Standard & Poor’s Equity Research

10. April 7, 2011 Global Strategy

10

Notable deals so far in 2011

Transaction Reserve Reserve Implied

value (USD Value size value

Date Buyer Seller Deal level Region bln) (USD bln) (mmboe) % gas R/P ratio (USD/boe)

Jan-11 Rosneft BP plc Corporate Diversified 11.8 5.9 619 54.3% 9.1 9.57 @

Jan-11 BP plc Rosneft Corporate FSU 9.0 5.6 1,325 0.0% 15.3 4.26 @

Feb-11 BP plc Reliance Industries Asset South Asia 7.2 5.3 582 96.0% 17.7 9.02 *

Feb-11 PetroChina Encana Asset Canada 5.5 4.4 217 92.5% 10.7 20.25 *

Feb-11 BHP Billiton Group Chesapeake Energy Asset United States 4.8 4.0 400 100.0% 15.8 9.98

Mar-11 Total SA Novatek OAO Corporate FSU 4.1 4.1 1,512 91.5% 29.7 2.70 *

Mar-11 KNOC Anadarko Asset United States 1.6 1.6 150 27.0% N/A 10.33 #

Mar-11 CNOOC Limited Tullow Oil plc Asset Africa 1.5 1.5 333 0.0% N/A 4.41 #

Mar-11 Total SA Tullow Oil plc Asset Africa 1.5 1.5 333 0.0% N/A 4.41 #

Source: IHS Herold, S&P Equity Research estimates. Reserve size and metrics based on 1P reserves, unless otherwise noted. *based on 2P reserves. ^based on contingent resources.

#based on total recoverable reserves. @ Transaction blocked by Russian arbitration body. Excludes CNOOC acquisition of 33.3% stake in Chesapeake’s 800,000 acre Niobrara Shale acreage

for USD1.27 bln due to lack of reserve value and information.

The M&A focus for 2011, in our view, will be in onshore North America, due to a

number of reasons:

North American onshore assets to be in

prime focus

Continuing strife in the MENA region will move investments by risk-averse

majors and independents away from the area. NOCs with deeper pockets and

potentially higher risk tolerance (especially given energy security concerns)

may see expansionary opportunities in MENA, albeit at a higher risk level

and potential overall cost than previous excursions.

Similarly, ongoing regulatory concerns on the Gulf of Mexico operations will

push oil majors and independents into onshore US.

Depressed North American gas prices provide an opportunity for oil majors

and NOCs to snap up weaker prey in the onshore US gas market. This is a

particularly attractive proposition for gas-hungry NOCs e.g. those from

China, given their deep pockets, access to cheap funding, the potential to

secure cheap gas for their LNG imports and their long-run bullish view on

gas.

Development of unconventional plays such as tight oil/gas and oil sands are

streets ahead in the US and Canada compared to the rest of the world. With

increasing risk aversion on MENA plays, we believe the virtually zero

exploratory risks and large resources in place for tight oil/gas and oil sands

will make it an attractive proposition for asset buyers, especially at current

crude prices.

Given these attractions and looking into 2011, we expect deal pricing for onshore

North America acreage to remain at a premium to worldwide pricing. We expect

the Chinese companies to continue to cautiously inch their way into North

America via joint-ventures and equity stakes, to avoid potential political backlash

(e.g. Unocal).

Standard & Poor’s Equity Research

11. April 7, 2011 Global Strategy

Stock Recommendations 11

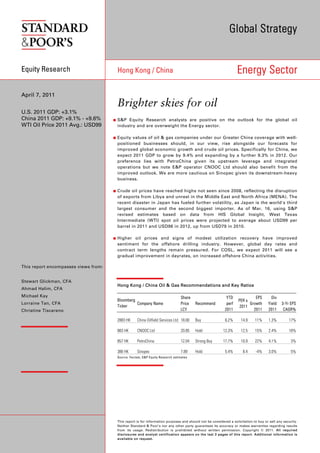

S&P Hong Kong / China Oil & Gas Recommendations and Key Ratios

EPS

Bloomberg Share Price YTD perf PER x

Company Name Recommend Growth Div Yield 3-Yr EPS P/BV ROE Net Gearing

Ticker LCY 2011 2011

2011 2011 CAGR% 2011 2011 2011

2883 HK

China Oilfield Services Ltd 18.00 Buy 6.2% 14.9 11% 1.3% 17% 2.3 17% 86%

883 HK

CNOOC Ltd 20.85 Hold 12.3% 12.5 15% 2.4% 18% 3.0 26% Net Cash

857 HK

PetroChina 12.04 Strong Buy 17.7% 10.9 22% 4.1% 3% 1.8 17% 26%

386 HK

Sinopec 7.89 Hold 5.4% 8.4 -4% 3.0% 5% 1.2 15% 51%

Source: S&P Equity Research estimates

COSL (HKD18.00, 4-STARS, 12-mo TP: HKD18)

Despite lower revenue recorded in 2010 (primarily due to a one-off reversal of

deferred revenue booked in 2009 for the cancellation of the drilling contract for

COSL Pioneer), greater integration synergies with Awilco and lower asset

impairment charges vs. 2009 meant margins and net profit improved

significantly. We expect 2011 will see more strength on a significant increase in

parent CNOOC Ltd's capex investments (+55.5% YoY), stronger dayrates on

increased offshore activities, new capacity deliveries (2 jackups and 1 semi), and

a new management contract for the ultra-deepwater HYSY981 (owned by CNOOC

Ltd). Risks to our recommendation and target price may arise from a fall in crude

prices and financial difficulties at clients that may hurt returns. In addition,

COSL’s acquisition of Awilco in 2008 has raised the group’s net gearing to close

to 100%, reducing flexibility on future investment. An issuance of new A-shares

remains pending, but the impact should already be discounted by the market. /

Ahmad Halim, CFA

CNOOC Ltd (HKD20.85, 3-STARS, 12-mo TP: HKD19)

2010 was a record year for CNOOC Ltd, both in terms of profits and production

growth. We expect 2011 production growth to moderate from +45% YoY in 2010

to about 11% YoY. While this remains strong vs other E&P players, other

headwinds should limit outperformance for the year: costs are expected to

increase on greater deepwater activities, higher DDA charges as newer, more

costly fields commence operations and crude ASPs should see some dilution

effect from greater Bridas contribution. Recent acquisition of a 33.3% stake in

Tullow’s Uganda blocks is positive for reserve replacement but production impact

during the forecast period is negligible. Funding remains ample, with CNOOC Ltd

carrying a net cash balance. Risks to our target price and recommendation come

from potentially lower U.S. product consumption that would send oil prices

lower. Further, higher-than-expected lifting costs will eat into CNOOC Ltd's

Standard & Poor’s Equity Research

12. April 7, 2011 Global Strategy

margins. In addition, with its oil primarily sold to Sinopec, pricing power may be

12

more limited. / Ahmad Halim, CFA

PetroChina (HKD12.04, 5-STARS, 12-mo TP: HKD14)

2010 results indicate some pressure on margins for both its refining and chemical

(R&C) unit and its pipeline unit. For 2011, we expect its R&C unit will book losses

in 2011, if product prices are not adjusted more aggressively vs. current levels.

Pipeline profits could continue to be pressured in 2011, before a rebound in 2012,

as we do not expect city gate prices to respond quickly enough to cover higher

input costs. Still, we think that PetroChina should benefit from higher oil prices

given its substantial upstream leverage, while a possible wellhead gas price hike

could also boost E&P profits. Risks to our recommendation and earnings

forecasts include prolonged reluctance by the PRC government to address pricing

inefficiencies. Policy uncertainty may also diminish earnings quality, and at

worst, destroy value for PetroChina. The company’s share price may also be

subject to swings in the oil price, despite the greater balance in its downstream

earnings. / Ahmad Halim, CFA

Sinopec (HKD7.89, 3-STARS, 12-mo TP: HKD8)

Slow product price adjustments hit Sinopec’s earnings hard in 2010; despite a

significant 97% EBIT growth from the E&P division on new Puguang gas

production, overall net profit only grew by 13.7% YoY due to substantially lower

refining margins. We expect Sinopec will book in refining losses in 2011, as short-

term concerns on inflation will cap aggressive price adjustments, in our view,

although over the longer term we expect Sinopec’s refining arm to return to

profitability as China slowly moves more toward a market-based price

mechanism. Risks to our target price and recommendation would come from

national interests that may supersede shareholder interests. The potential for

higher marketing competition may also eat into profitability, while Sinopec's

status as a net buyer of oil means a higher risk premium is warranted. / Ahmad

Halim, CFA

Standard & Poor’s Equity Research

13. April 7, 2011 Global Strategy

FFO- Funds From Operations

Glossary FY- Fiscal Year

P/E- Price/Earnings

13

PEG Ratio- P/E-to-Growth Ratio

S&P STARS - Since January 1, 1987, Standard & Poor’s Equity Research Services PV- Present Value

has ranked a universe of U.S. common stocks, ADRs (American Depositary Receipts), R&D- Research & Development

and ADSs (American Depositary Shares) based on a given equity’s potential for ROE- Return on Equity

future performance. Similarly, Standard & Poor’s Equity Research Services has used ROI- Return on Investment

STARS® methodology to rank Asian and European equities since June 30, 2002. ROIC- Return on Invested Capital

Under proprietary STARS (STock Appreciation Ranking System), S&P equity analysts ROA- Return on Assets

rank equities according to their individual forecast of an equity’s future total return SG&A- Selling, General & Administrative Expenses

potential versus the expected total return of a relevant benchmark (e.g., a regional WACC- Weighted Average Cost of Capital

index (S&P Asia 50 Index, S&P Europe 350® Index or S&P 500® Index)), based on a

12-month time horizon. STARS was designed to meet the needs of investors looking Dividends on American Depository Receipts (ADRs) and American Depository

to put their investment decisions in perspective. Shares (ADSs) are net of taxes (paid in the country of origin).

S&P Quality Rankings (also known as S&P Earnings & Dividend Rankings)-

Growth and stability of earnings and dividends are deemed key elements in

establishing S&P’s earnings and dividend rankings for common stocks, which are

Disclosures/Disclaimers

designed to capsulize the nature of this record in a single symbol. It should be noted,

Required Disclosures

however, that the process also takes into consideration certain adjustments and

modifications deemed desirable in establishing such rankings. The final score for

each stock is measured against a scoring matrix determined by analysis of the scores

In contrast to the qualitative STARS recommendations covered in this report, which

of a large and representative sample of stocks. The range of scores in the array of

are determined and assigned by S&P equity analysts, S&P’s quantitative

this sample has been aligned with the following ladder of rankings:

evaluations are derived from S&P’s proprietary Fair Value quantitative model. In

A+ Highest B+ Average C Lowest particular, the Fair Value Ranking methodology is a relative ranking methodology,

A High B Below Average D In Reorganization whereas the STARS methodology is not. Because the Fair Value model and the

A- Above Average B- Lower NR Not Ranked STARS methodology reflect different criteria, assumptions and analytical methods,

quantitative evaluations may at times differ from (or even contradict) an equity

S&P Issuer Credit Rating - A Standard & Poor’s Issuer Credit Rating is a current analyst’s STARS recommendations. As a quantitative model, Fair Value relies on

opinion of an obligor’s overall financial capacity (its creditworthiness) to pay its history and consensus estimates and does not introduce an element of subjectivity

financial obligations. This opinion focuses on the obligor’s capacity and willingness as can be the case with equity analysts in assigning STARS recommendations.

to meet its financial commitments as they come due. It does not apply to any specific

financial obligation, as it does not take into account the nature of and provisions of

the obligation, its standing in bankruptcy or liquidation, statutory preferences, or the

S&P Global STARS Distribution

legality and enforceability of the obligation. In addition, it does not take into account In North America

the creditworthiness of the guarantors, insurers, or other forms of credit As of March 31, 2011, research analysts at Standard & Poor’s Equity Research

enhancement on the obligation. Services U.S. recommended 37.5% of issuers with buy recommendations, 54.9%

with hold recommendations and 7.6% with sell recommendations.

S&P Core Earnings - Standard & Poor's Core Earnings is a uniform methodology for

adjusting operating earnings by focusing on a company's after-tax earnings In Europe

generated from its principal businesses. Included in the Standard & Poor's definition As of March 31, 2011, research analysts at Standard & Poor’s Equity Research

are employee stock option grant expenses, pension costs, restructuring charges from Services Europe recommended 35.6% of issuers with buy recommendations, 47.0%

ongoing operations, write-downs of depreciable or amortizable operating assets, with hold recommendations and 17.4% with sell recommendations.

purchased research and development, M&A related expenses and unrealized

In Asia

gains/losses from hedging activities. Excluded from the definition are pension gains,

As of March 31, 2011, research analysts at Standard & Poor’s Equity Research

impairment of goodwill charges, gains or losses from asset sales, reversal of prior-

Services Asia recommended 46.7% of issuers with buy recommendations, 46.7%

year charges and provision from litigation or insurance settlements.

with hold recommendations and 6.6% with sell recommendations.

S&P 12 Month Target Price – The S&P equity analyst’s projection of the market

Globally

price a given security will command 12 months hence, based on a combination of

As of March 31, 2011, research analysts at Standard & Poor’s Equity Research

intrinsic, relative, and private market valuation metrics.

Services globally recommended 38.0% of issuers with buy recommendations,

Standard & Poor’s Equity Research Services – Standard & Poor’s Equity Research 52.9% with hold recommendations and 9.1% with sell recommendations.

Services U.S. includes Standard & Poor’s Investment Advisory Services LLC;

5-STARS (Strong Buy): Total return is expected to outperform the total return of a

Standard & Poor’s Equity Research Services Europe includes Standard & Poor’s LLC-

relevant benchmark, by a wide margin over the coming 12 months, with shares

London; Standard & Poor’s Equity Research Services Asia includes Standard &

rising in price on an absolute basis.

Poor’s LLC’s offices in Singapore, Standard & Poor’s Investment Advisory Services

4-STARS (Buy): Total return is expected to outperform the total return of a relevant

(HK) Limited in Hong Kong, Standard & Poor’s Malaysia Sdn Bhd, and Standard &

benchmark over the coming 12 months, with shares rising in price on an absolute

Poor’s Information Services (Australia) Pty Ltd.

basis.

Abbreviations Used in S&P Equity Research Reports 3-STARS (Hold): Total return is expected to closely approximate the total return of

CAGR- Compound Annual Growth Rate a relevant benchmark over the coming 12 months, with shares generally rising in

CAPEX- Capital Expenditures price on an absolute basis.

CY- Calendar Year 2-STARS (Sell): Total return is expected to underperform the total return of a

DCF- Discounted Cash Flow relevant benchmark over the coming 12 months, and the share price is not

EBIT- Earnings Before Interest and Taxes anticipated to show a gain.

EBITDA- Earnings Before Interest, Taxes, Depreciation and Amortization 1-STARS (Strong Sell): Total return is expected to underperform the total return of

EPS- Earnings Per Share a relevant benchmark by a wide margin over the coming 12 months, with shares

EV- Enterprise Value falling in price on an absolute basis.

FCF- Free Cash Flow

Standard & Poor’s Equity Research

14. April 7, 2011 Global Strategy

Relevant benchmarks: In North America the relevant benchmark is the S&P 500 organizations, including organizations whose securities or services they may

Index, in Europe and in Asia, the relevant benchmarks are generally the S&P Europe recommend, rate, include in model portfolios, evaluate or otherwise address. 14

350 Index and the S&P Asia 50 Index.

S&P and/or one of its affiliates has performed services for and received

For All Regions: compensation from this company during the past twelve months.

All of the views expressed in this research report accurately reflect the research

analyst's personal views regarding any and all of the subject securities or issuers. No S&P has received compensation from one or more institutions, each in the range of

part of analyst compensation was, is, or will be, directly or indirectly, related to the HKD 78,000 to HKD 390,000, for the right to distribute and co-brand S&P’s research

specific recommendations or views expressed in this research report. on this company.

S&P Global Quantitative Disclaimers

Recommendations Distribution With respect to reports issued to clients in Japan and in the case of inconsistencies

between the English and Japanese version of a report, the English version prevails.

In Europe

With respect to reports issued to clients in German and in the case of

As of March 31, 2011, Standard & Poor’s Quantitative Services Europe recommended

inconsistencies between the English and German version of a report, the English

46.2% of issuers with buy recommendations, 21.4% with hold recommendations and version prevails. Neither S&P nor its affiliates guarantee the accuracy of the

32.4% with sell recommendations.

translation. Assumptions, opinions and estimates constitute our judgment as of the

In Asia date of this material and are subject to change without notice. Past performance is

not necessarily indicative of future results.

As of March 31, 2011, Standard & Poor’s Quantitative Services Asia recommended

47.0% of issuers with buy recommendations, 18.0% with hold recommendations and

Standard & Poor’s, its affiliates, and any third-party providers, as well as their

35.0% with sell recommendations.

directors, officers, shareholders, employees or agents (collectively S&P Parties) do

not guarantee the accuracy, completeness or adequacy of this material, and S&P

Globally

As of March 31, 2011, Standard & Poor’s Quantitative Services globally Parties shall have no liability for any errors, omissions, or interruptions therein,

recommended 46.7% of issuers with buy recommendations, 19.3% with hold regardless of the cause, or for the results obtained from the use of the information

provided by the S&P Parties. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR

recommendations and 34.0% with sell recommendations.

IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF

MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR

Additional information is available upon request.

USE. In no event shall S&P Parties be liable to any party for any direct, indirect,

Other Disclosures incidental, exemplary, compensatory, punitive, special or consequential damages,

costs, expenses, legal fees, or losses (including, without limitation, lost income or

This report has been prepared and issued by Standard & Poor’s and/or one of its lost profits and opportunity costs) in connection with any use of the information

affiliates. In the United States, research reports are prepared by Standard & Poor’s contained in this document even if advised of the possibility of such damages.

Investment Advisory Services LLC (“SPIAS”). In the United States, research reports

Ratings from Standard & Poor’s Ratings Services are statements of opinion as of

are issued by Standard & Poor’s (“S&P”); in the United Kingdom by Standard &

the date they are expressed and not statements of fact or recommendations to

Poor’s LLC (“S&P LLC”), which is authorized and regulated by the Financial Services

purchase, hold, or sell any securities or to make any investment decisions.

Authority; in Hong Kong by Standard & Poor’s Investment Advisory Services (HK)

Standard & Poor’s assumes no obligation to update its opinions following

Limited, which is regulated by the Hong Kong Securities Futures Commission; in

publication in any form or format. Standard & Poor’s ratings should not be relied

Singapore by Standard & Poor’s LLC, which is regulated by the Monetary Authority

on and are not substitutes for the skill, judgment and experience of the user, its

of Singapore; in Malaysia by Standard & Poor’s Malaysia Sdn Bhd (“S&PM”), which

management, employees, advisors and/or clients when making investment and

is regulated by the Securities Commission; in Australia by Standard & Poor’s

other business decisions. Standard & Poor’s rating opinions do not address the

Information Services (Australia) Pty Ltd (“SPIS”), which is regulated by the Australian

suitability of any security. Standard & Poor’s does not act as a fiduciary. While

Securities & Investments Commission; and in Korea by SPIAS, which is also

Standard & Poor’s has obtained information from sources it believes to be reliable,

registered in Korea as a cross-border investment advisory company.

Standard & Poor’s does not perform an audit and undertakes no duty of due

The research and analytical services performed by SPIAS, S&P LLC, S&PM, and SPIS diligence or independent verification of any information it receives.

are each conducted separately from any other analytical activity of Standard &

Standard & Poor’s keeps certain activities of its business units separate from each

Poor’s.

other in order to preserve the independence and objectivity of their respective

Standard & Poor's or an affiliate may license certain intellectual property or provide activities. As a result, certain business units of Standard & Poor’s may have

pricing or other services to, or otherwise have a financial interest in, certain issuers of information that is not available to other Standard & Poor’s business units.

securities, including exchange-traded investments whose investment objective is to Standard & Poor’s has established policies and procedures to maintain the

substantially replicate the returns of a proprietary Standard & Poor's index, such as confidentiality of certain non-public information received in connection with each

the S&P 500. In cases where Standard & Poor's or an affiliate is paid fees that are tied analytical process.

to the amount of assets that are invested in the fund or the volume of trading activity

Standard & Poor’s Ratings Services did not participate in the development of this

in the fund, investment in the fund will generally result in Standard & Poor's or an

report. Standard & Poor’s may receive compensation for its ratings and certain

affiliate earning compensation in addition to the subscription fees or other

credit-related analyses, normally from issuers or underwriters of securities or from

compensation for services rendered by Standard & Poor’s. A reference to a particular

obligors. Standard & Poor’s reserves the right to disseminate its opinions and

investment or security by Standard & Poor’s and/or one of its affiliates is not a

analyses. Standard & Poor’s public ratings and analyses are made available on its

recommendation to buy, sell, or hold such investment or security, nor is it considered

Web sites, www.standardandpoors.com (free of charge), and

to be investment advice.

www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may

Indexes are unmanaged, statistical composites and their returns do not include be distributed through other means, including via Standard & Poor’s publications

payment of any sales charges or fees an investor would pay to purchase the and third-party redistributors. Additional information about our ratings fees is

securities they represent. Such costs would lower performance. It is not possible to available at www.standardandpoors.com/usratingsfees.

invest directly in an index.

This material is not intended as an offer or solicitation for the purchase or sale of

Standard & Poor's and its affiliates provide a wide range of services to, or relating to, any security or other financial instrument. Securities, financial instruments or

many organizations, including issuers of securities, investment advisers, broker- strategies mentioned herein may not be suitable for all investors. Any opinions

dealers, investment banks, other financial institutions and financial intermediaries, expressed herein are given in good faith, are subject to change without notice, and

and accordingly may receive fees or other economic benefits from those are only current as of the stated date of their issue. Prices, values, or income from

Standard & Poor’s Equity Research

15. April 7, 2011 Global Strategy

any securities or investments mentioned in this report may fall against the interests

of the investor and the investor may get back less than the amount invested. Where 15

an investment is described as being likely to yield income, please note that the

amount of income that the investor will receive from such an investment may

fluctuate. Where an investment or security is denominated in a different currency to

the investor’s currency of reference, changes in rates of exchange may have an

adverse effect on the value, price or income of or from that investment to the

investor. The information contained in this report does not constitute advice on the

tax consequences of making any particular investment decision. This material is not

intended for any specific investor and does not take into account your particular

investment objectives, financial situations or needs and is not intended as a

recommendation of particular securities, financial instruments or strategies to you.

Before acting on any recommendation in this material, you should consider whether

it is suitable for your particular circumstances and, if necessary, seek professional

advice.

This document does not constitute an offer of services in jurisdictions where

Standard & Poor’s or its affiliates do not have the necessary licenses.

For residents of the U.K. –this report is only directed at and should only be relied on

by persons outside of the United Kingdom or persons who are inside the United

Kingdom and who have professional experience in matters relating to investments or

who are high net worth persons, as defined in Article 19(5) or Article 49(2) (a) to (d) of

the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005,

respectively.

For residents of Singapore - Anything herein that may be construed as a

recommendation is intended for general circulation and does not take into account

the specific investment objectives, financial situation or particular needs of any

particular person. Advice should be sought from a financial adviser regarding the

suitability of an investment, taking into account the specific investment objectives,

financial situation or particular needs of any person in receipt of the

recommendation, before the person makes a commitment to purchase the

investment product.

For residents of Malaysia - All queries in relation to this report should be referred to

Ching Wah Tam.

For residents of Indonesia - This research report does not constitute an offering

document and it should not be construed as an offer of securities in Indonesia, and

that any such securities will only be offered or sold through a financial institution.

For residents of the Philippines - The securities being offered or sold have not been

registered with the Securities and Exchange Commission under the Securities

Regulation Code of the Philippines. Any future offer or sale thereof is subject to

registration requirements under the Code unless such offer or sale qualifies as an

exempt transaction.

STANDARD & POOR’S, S&P, S&P 500, S&P Europe 350 and STARS

are registered trademarks of Standard & Poor’s Financial Services

LLC.

Standard & Poor’s Equity Research

16. April 7, 2011 Global Strategy

16

Standard & Poor’s Equity Research