ECA Alert - IND AS 1 Presentation of Financial Statements

•Télécharger en tant que PPTX, PDF•

0 j'aime•116 vues

Summary of IND AS 1

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à ECA Alert - IND AS 1 Presentation of Financial Statements

Similaire à ECA Alert - IND AS 1 Presentation of Financial Statements (20)

Dernier

Dernier (20)

ECA Alert - IND AS 1 Presentation of Financial Statements

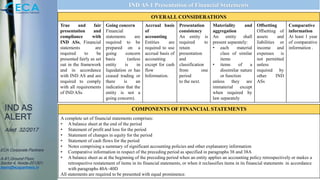

- 1. IND AS ALERT Alert 32/2017 ECA Corporate Partners A-81,Ground Floor, Sector 4, Noida-201301. team@ecapartners.in IND AS 1 Presentation of Financial Statements OVERALL CONSIDERATIONS True and fair presentation and compliance with IND ASs, Financial statements are required to be presented fairly as set out in the framework and in accordance with IND AS and are required to comply with all requirements of IND ASs Going concern Financial statements are required to be prepared on a going concern basis (unless entity is in liquidation or has ceased trading or there is an indication that the entity is not a going concern). Accrual basis of accounting Entities are required to use accrual basis of accounting except for cash flow Information. Presentation consistency An entity is required to retain presentation and classification from one period to the next. Materiality and aggregation An entity shall present separately: • each material class of similar items • items of a dissimilar nature or function unless they are immaterial except when required by law separately Offsetting Offsetting of assets and liabilities or income and expenses is not permitted unless required by other IND ASs Comparative information At least 1 year of comparative information . COMPONENTS OF FINANCIAL STATEMENTS A complete set of financial statements comprises: • A balance sheet at the end of the period • Statement of profit and loss for the period • Statement of changes in equity for the period • Statement of cash flows for the period • Notes comprising a summary of significant accounting policies and other explanatory information • Comparative information in respect of the preceding period as specified in paragraphs 38 and 38A • A balance sheet as at the beginning of the preceding period when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements in accordance with paragraphs 40A–40D All statements are required to be presented with equal prominence.

- 2. IND AS ALERT Alert 32/2017 ECA Corporate Partners A-81,Ground Floor, Sector 4, Noida-201301. team@ecapartners.in STRUCTURE AND CONTENT IDENTIFICATI ON OF THE FINANCIAL STATEMENTS Financial statements must be clearly identified and distinguished from other information in the same published document, and must identify: • Name of the reporting entity • Whether the financial statements cover the individual entity or a group of entities • The date of financial statements (or the period covered) • The presentation currency • The level of rounding used BALANCE SHEET Present current and non-current items separately; or Present items in order of liquidity- if reliable and more relevant Current assets Expected to be realised in, or is intended for sale or consumption in the entity’s normal operating cycle Held primarily for trading Expected to be realised within 12 months Cash or cash equivalents. All other assets are required to be classified as non-current Current liabilities Expected to be settled in the entity’s normal operating cycle Held primarily for trading Due to be settled within 12 months The entity does not have an unconditional right to defer settlement of the liability for at least 12 months. All other liabilities are required to be classified as non-current. Information required to be presented on the face of the balance sheet is detailed in IND AS 1.54 Further information required to be presented on the face or in the notes is detailed in IND AS 1.79 – 80. STATEMENT OF PROFIT & LOSS An entity shall present a single statement of profit and loss, with profit or loss and other comprehensive income presented in two sections. The sections shall be presented together, with the profit or loss section presented first followed directly by the other comprehensive income section Entities shall present an analysis of expense recognised in profit or loss using a classification based on the nature of expense method Information required to be presented in the: - Statement of profit and loss is defined in IND AS 1.82A - 87 - Profit or loss as defined in IND AS 1.88 and 89 - Other comprehensive income in INDAS 1.82A and 90-96. - Further information required to be presented on the face or in the notes to the Statement of Profit and loss is detailed in IND AS 1.97 Line items within other comprehensive income are required to be categorised into two categories: - Those that could subsequently be reclassified to profit or loss - Those that cannot be re-classified to profit or loss. STATEMENT OF CASH FLOWS Provides users of financial statements with cash flow information – refer IND AS 7 Statement of Cash Flows.

- 3. IND AS ALERT Alert 32/2017 ECA Corporate Partners A-81,Ground Floor, Sector 4, Noida-201301. team@ecapartners.in STRUCTURE AND CONTENT STATEMENT OF CHANGES IN EQUITY Information required to be presented: • Total comprehensive income for the period, showing separately attributable to owners or the parent and non-controlling interest • For each component of equity, the effects of retrospective application / restatement recognised in accordance with IND AS 8 Accounting Policies, Changes in Accounting Estimates and Errors • For each component in equity a reconciliation between the carrying amount at the beginning and end of the period, separately disclosing each change. • Amount of dividends recognised as distributions to owners during the period (can alternatively be disclosed in the notes. • Analysis of each item of OCI (alternatively to be disclosed in the notes). NOTES TO THE FINANCIAL STATEMENTS • Statement of compliance with IND ASs. • Significant accounting policies, estimates, assumptions, and judgements must be disclosed • Additional information useful to users understanding / decision making to be presented • Information that enables users to evaluate the entity’s objectives, policies and processes for managing capital THIRD BALANCE SHEET An entity shall present a third balance sheet as at the beginning of the preceding period in addition to the minimum comparative financial statements required in paragraph 38A if: • it applies an accounting policy retrospectively, makes a retrospective restatement of items in its financial statements or reclassifies items in its financial statements; and • the retrospective application, retrospective restatement or the reclassification has a material effect on the information in the balance sheet at the beginning of the preceding period. REPORTING PERIOD • Accounts presented at least annually • If longer or shorter, entity must disclose that fact.