Avoidable Errors in Payroll Compliance for Payroll Services Providers - Globu...

Kec International

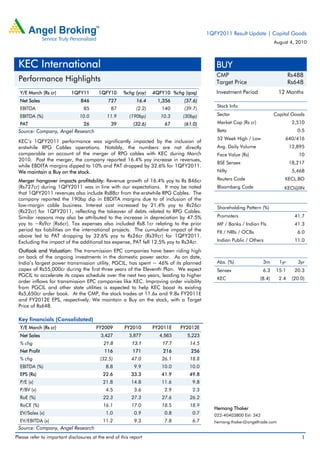

1. 1QFY2011 Result Update | Capital Goods

August 4, 2010

KEC International BUY

CMP Rs488

Performance Highlights Target Price Rs648

Y/E March (Rs cr) 1QFY11 1QFY10 %chg (yoy) 4QFY10 %chg (qoq) Investment Period 12 Months

Net Sales 846 727 16.4 1,356 (37.6)

Stock Info

EBITDA 85 87 (2.2) 140 (39.7)

EBITDA (%) 10.0 11.9 (190bp) 10.3 (30bp) Sector Capital Goods

PAT 26 39 (32.6) 67 (61.0) Market Cap (Rs cr) 2,510

Source: Company, Angel Research Beta 0.5

52 Week High / Low 640/416

KEC’s 1QFY2011 performance was significantly impacted by the inclusion of

erstwhile RPG Cables operations. Notably, the numbers are not directly Avg. Daily Volume 12,895

comparable on account of the merger of RPG cables with KEC during March Face Value (Rs) 10

2010. Post the merger, the company reported 16.4% yoy increase in revenues,

BSE Sensex 18,217

while EBDITA margins dipped to 10% and PAT dropped by 32.6% for 1QFY2011.

We maintain a Buy on the stock. Nifty 5,468

Merger hangover impacts profitability: Revenue growth of 16.4% yoy to Rs 846cr Reuters Code KECL.BO

(Rs727cr) during 1QFY2011 was in line with our expectations. It may be noted Bloomberg Code KECI@IN

that 1QFY2011 revenues also include Rs88cr from the erstwhile RPG Cables. The

company reported the 190bp dip in EBDITA margins due to of inclusion of the

low-margin cable business. Interest cost increased by 21.4% yoy to Rs26cr Shareholding Pattern (%)

(Rs22cr) for 1QFY2011, reflecting the takeover of debts related to RPG Cables.

Similar reasons may also be attributed to the increase in depreciation by 47.5% Promoters 41.7

yoy to ~Rs9cr (Rs6cr). Tax expenses also included Rs8.1cr relating to the prior MF / Banks / Indian Fls 41.3

period tax liabilities on the international projects. The cumulative impact of the FII / NRIs / OCBs 6.0

above led to PAT dropping by 32.6% yoy to Rs26cr (Rs39cr) for 1QFY2011.

Excluding the impact of the additional tax expense, PAT fell 12.5% yoy to Rs34cr. Indian Public / Others 11.0

Outlook and Valuation: The transmission EPC companies have been riding high

on back of the ongoing investments in the domestic power sector. As on date,

India’s largest power transmission utility, PGCIL, has spent ~ 46% of its planned Abs. (%) 3m 1yr 3yr

capex of Rs55,000cr during the first three years of the Eleventh Plan. We expect Sensex 6.3 15.1 20.3

PGCIL to accelerate its capex schedule over the next two years, leading to higher

KEC (8.4) 2.4 (20.0)

order inflows for transmission EPC companies like KEC. Improving order visibility

from PGCIL and other state utilities is expected to help KEC boost its existing

Rs5,650cr order book. At the CMP, the stock trades at 11.6x and 9.8x FY2011E

and FY2012E EPS, respectively. We maintain a Buy on the stock, with a Target

Price of Rs648.

Key financials (Consolidated)

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net Sales 3,427 3,877 4,563 5,223

% chg 21.8 13.1 17.7 14.5

Net Profit 116 171 216 256

% chg (32.5) 47.0 26.1 18.8

EBITDA (%) 8.8 9.9 10.0 10.0

EPS (Rs) 22.6 33.3 41.9 49.8

P/E (x) 21.8 14.8 11.6 9.8

P/BV (x) 4.5 3.6 2.9 2.3

RoE (%) 22.3 27.3 27.6 26.2

RoCE (%) 16.1 17.0 18.5 18.9

Hemang Thaker

EV/Sales (x) 1.0 0.9 0.8 0.7 022-40403800 Ext: 342

EV/EBITDA (x) 11.2 9.3 7.8 6.7 hemang.thaker@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. KEC International | 1QFY2011 Result Update

Exhibit 1: 1QFY2011 Performance (Consolidated)

Y/E March (Rs cr) 1QFY2011 1QFY2010 yoy (%) 4QFY2010 qoq (%) FY2010 FY2009 yoy (%)

Net Sales 846 727 16.4 1,356 (37.6) 3,907 3,429 14.0

Raw Material 414 325 27.4 781 (47.0) 2,013 1,976 1.9

(% of Net Sales) 48.9 44.7 57.6 51.5 57.6

Erection & Sub contracting 209 222 (5.9) 284 (26.4) 958 575 66.6

(% of Net Sales) 24.7 30.5 20.9 24.5 16.8

Employee Cost 48 38 26.3 45 6.4 169 142 18.9

(% of Net Sales) 5.7 5.2 3.3 4.3 4.1

Other Expenses 90 55 63.8 106 (14.4) 371 341 8.7

(% of Net Sales) 10.7 7.6 7.8 9.5 10.0

Total Expenditure 761 640 18.9 1,216 (37.4) 3,511 3,034 15.7

EBITDA 85 87 (2.2) 140 (39.7) 396 395 0.4

EBITDA (%) 10.0 11.9 10.3 10.1 11.5

Interest 26 22 21.4 19 36.2 87 100 (13.5)

Depreciation 9 6 47.5 7 28.6 27 23 17.4

Other Income 0 0.0 0.6 1 1 66.7

Profit before Tax 49 59 (16.1) 114 (56.8) 284 272 4.3

(% of Net Sales) 5.8 8.1 8.4 7.3 7.9

Total Tax 23 20 16.2 47 (50.9) 100 94 6.4

(% of PBT) 46.8 33.8 41.1 35.2 34.5

Adjusted PAT 26 39 (32.6) 67 (61.0) 184 178 3.1

(% of Net Sales) 3.1 5.3 4.9 4.7 5.2

Extraordinary items - - (5) 6 (61) (109.8)

Reported PAT 26 39 (32.6) 72 (63.6) 190 117 62.3

Source: Company, Angel Research

Order backlog: The company’s order intake for the quarter was ~Rs1,000cr.

Order backlog at the end of 1QFY2011 stood at Rs5,650cr equally split across the

reporting geographies of International and South Asia. Of the total order backlog,

transmission accounted for 76%, distribution & substation 18%, railways 4% and

cables 2%.

Exhibit 2: Order book (Rs cr)

Particulars International South Asia Total

Transmission 2,461 1,811 4,272

Distribution 316 699 1,015

Railway 30 217 247

Cable - 113 113

Telecom - 3 3

Total 2,807 2,843 5,650

Source: Company, Angel Research

Capex guidance: KEC intends to spend ~ Rs100cr on its tower business in the

current fiscal. Capex planned for the cable plant at Vadodara is ~Rs120cr over

the next two years. Management expects the Vadodara facility to commence

production from FY2012E generating ~Rs400cr in revenues with EBDITA margins

of ~7-8%

August 4, 2010 2

3. KEC International | 1QFY2011 Result Update

Investment Arguments

Huge opportunity for transmission EPC players: The government has envisaged

investment of Rs140,000cr in the transmission segment during the Eleventh plan,

an increase of over two times from the investments made in the Tenth Plan. The

scale gets even bigger for the Twelfth Plan, with planned investment of around

Rs240,000cr. As per our estimates, this had opened up a potential US $14-15bn

opportunity for the transmission EPC players during the Eleventh Plan period

alone. Besides, Power Grid Corporation of India (PGCIL), India's largest

transmission utility, having spent only ~46% of its planned capex of Rs 55,000cr

during the first three years of the Eleventh Plan, is all set to accelerate its capex

during the remaining two years, which in turn, would translate into higher order

inflows for the transmission EPC sector.

Overseas orders to improve: KEC has a Strong international presence across

geographies compared to its domestic peers who have generally restricted

themselves to local operations. Notably, the company has executed large number

of T&D projects in over forty countries. With its footprint spread across continents,

KEC is adequately hedged against slow-down in any particular region. On the

other hand, any delay or deferment in the release of domestic T&D orders would

adversely impact the revenue projections of many domestic EPC companies.

Amidst such a scenario, we believe that KEC would be the least impacted owing to

its high exposure to international orders.

Diversification into railways and telecom sectors a major positive: KEC has forayed

into the telecom and railway sectors. Although these divisions currently account for

small portion of the company's total revenues, future prospects of the segments are

very bright. KEC also plans to enter tracking, signaling and platform construction

works in the railway segment.

Outlook and Valuation: The transmission EPC companies have been riding high

on back of the ongoing investments in the domestic power sector. As on date,

India’s largest power transmission utility, PGCIL, has spent ~ 46% of its planned

capex of Rs55,000cr during the first three years of the Eleventh Plan. We expect

PGCIL to accelerate its capex schedule over the next two years, leading to higher

order inflows for transmission EPC companies like KEC. Improving order visibility

from PGCIL and other state utilities is expected to help KEC boost its existing

Rs5,650cr order book. At the CMP, the stock trades at 11.6x and 9.8x FY2011E

and FY2012 EPS, respectively. We maintain a Buy on the stock, with a Target Price

of Rs648.

Exhibit 3: Actual v/s Angel estimates – 1QFY2011

Particulars (Rs cr) Actual Estimates Var (%)

Revenues 846 844 0.2

Operating Profit 85 85 -

PAT 26 35 (25.7)

EPS (Rs) 5.1 6.9 (26.1)

Source: Company, Angel Research

August 4, 2010 3

4. KEC International | 1QFY2011 Result Update

Exhibit 4: Angel EPS Forecast v/s Consensus

Year Angel forecast (Rs) Bloomberg consensus (Rs) Var (%)

FY2011E 41.9 40.1 4.4

FY2012E 49.8 49.6 0.4

Source: Bloomberg, Angel Research

Exhibit 5: Key assumptions

Particulars FY2011E FY2012E

Order Inflow (Rs cr) 5,111 5,878

Order Inflow Growth (%) 20.0 15.0

Order Backlog (Rs cr) 5,995 6,589

Order Backlog Growth (%) 9.0 10.0

Order Book to Sales (%) 43.5 44.5

Source: Company, Angel Research

Exhibit 6: One-year forward P/E band

1,000

800

600

400

200

0

Jan-09

Jul-10

Apr-06

Aug-07

Dec-06

May-08

Oct-09

Share Price (Rs) 6x 10x 14x 18x

Source: Company, Angel Research

August 4, 2010 4

10. KEC International | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement KEC International

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

August 4, 2010 10