1. 427 Naubuc Avenue Suite 103 Glastonbury, Connecticut 06033 www.diblife.com

The

The Strategy

During a wealth transfer, you can take assets that your

client won't need in their lifetime and position them for

an efficient transfer to the next generation. An effective

strategy transfers the wealth to the client's heirs in a

financially sound and, in some cases, tax-advantaged --

manner.

The Case

A couple in their 70’s who have more money than they

are going to use. They wanted to pass funds along to

their daughters. Their net worth is approximately

$2.5MM.

The Solution

The Solution

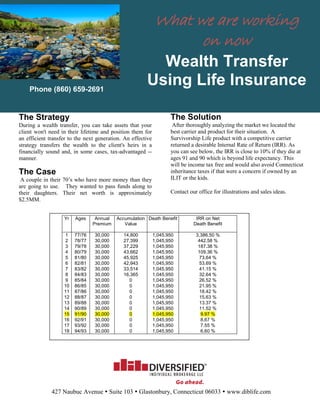

After thoroughly analyzing the market we located the

best carrier and product for their situation. A

Survivorship Life product with a competitive carrier

returned a desirable Internal Rate of Return (IRR). As

you can see below, the IRR is close to 10% if they die at

ages 91 and 90 which is beyond life expectancy. This

will be income tax free and would also avoid Connecticut

inheritance taxes if that were a concern if owned by an

ILIT or the kids.

Contact our office for illustrations and sales ideas.

What we are working

on now

Wealth Transfer

Using Life InsurancePhone (860) 659-2691

Yr Ages Annual

Premium

Accumulation

Value

Death Benefit IRR on Net

Death Benefit

1 77/76 30,000 14,800 1,045,950 3,386.50 %

2 78/77 30,000 27,399 1,045,950 442.58 %

3 79/78 30,000 37,229 1,045,950 187.38 %

4 80/79 30,000 43,662 1,045,950 109.36 %

5 81/80 30,000 45,925 1,045,950 73.64 %

6 82/81 30,000 42,943 1,045,950 53.69 %

7 83/82 30,000 33,514 1,045,950 41.15 %

8 84/83 30,000 16,365 1,045,950 32.64 %

9 85/84 30,000 0 1,045,950 26.52 %

10 86/85 30,000 0 1,045,950 21.95 %

11 87/86 30,000 0 1,045,950 18.42 %

12 88/87 30,000 0 1,045,950 15.63 %

13 89/88 30,000 0 1,045,950 13.37 %

14 90/89 30,000 0 1,045,950 11.52 %

15 91/90 30,000 0 1,045,950 9.97 %

16 92/91 30,000 0 1,045,950 8.67 %

17 93/92 30,000 0 1,045,950 7.55 %

18 94/93 30,000 0 1,045,950 6.60 %