1. Prepared by Eric McNew and Michael Schopler 1

Hi-Crush LP

Current Price $36.83 Intrinsic Value $48 Target Price $76 Market Cap 1.1B

Company Profile

Investment Thesis Catalyst

Price Performance

Recommendation

Hi-Crush Partners LP (Hi-Crush) is a pure play, low-cost, domestic producer of premium

monocrystalline sand, a specialized mineral that is used to enhance the recovery rates of hy-drocarbons

from oil and natural gas wells. Its reserves consist of “Northern White” sand, a re-source

existing predominantly in Wisconsin and limited portions of the upper Midwest region

of the United States.

The focus on domestic energy has given rise to E&P firms

resorting to unconventional extraction techniques know as

hydraulic fracturing or “fracking” in the oil and natural gas

industry. Demand for materials or “proppants” used in the

process of extraction have seen a tremendous surge in the

amount required through the extraction process because of

the increases in drilling domestically. The amount of prop-pant

used in fracking is expected to increase substantially

over the next decade. Hi-Crush is in the position to capitalize

from this megatrend.

Given its current price and our valuation , we consider Hi-

Crush to be undervalued and a great investment opportunity

to add alpha to the SMIF.

Significant increase in demand for proppants

Ample supply of high quality raw frac sand

Logistic and infrastructure advantages

Superior operating cost structures

M&A possibilities

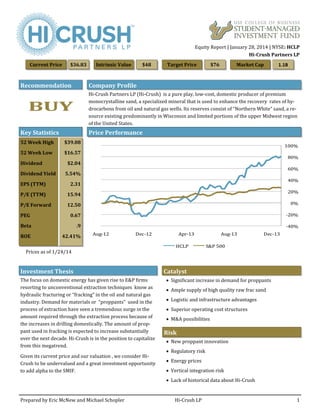

Prices as of 1/24/14

Key Statistics

$39.08

$16.57

$2.04

5.54%

2.31

15.94

12.50

0.67

.9

42.41%

52 Week High

52 Week Low

Dividend

Dividend Yield

EPS (TTM)

P/E (TTM)

P/E Forward

PEG

Beta

ROE

BUY

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

Aug-12 Dec-12 Apr-13 Aug-13 Dec-13

HCLP S&P 500

Risk

New proppant innovation

Regulatory risk

Energy prices

Vertical integration risk

Lack of historical data about Hi-Crush

2. Prepared by Eric McNew and Michael Schopler

2

Hi-Crush LP

Industry Overview

Proppant Consumed by Volume

The oil and natural gas proppant industry is associated with the businesses of drilling oil and natural gas wells. The pro- cess of extracting these fossil fuels involves pumping fluids that are mixed with proppants which are then pumped into the geologic formation to cause fractures and stresses into hydrocarbon bearing rock. These proppant-filled fractures create channels through which the hydrocarbons can flow freely from the well to the surface.

The hydraulic fracturing “fracking” industry has been expe- riencing a boom as a result of oil and natural gas shale explo- ration domestically. Unconventional fracking, more specifi- cally horizontal drilling, is becoming more and more promi- nent. A well lateral is the mining channel created by horizon- tal drilling, and as well laterals become deeper, frac sand per well will increase exponentially. Hi-Crush’s frac sand is de- sired by its customers because of the sand’s high crush strength relative to its cost.

The existing supply of raw frac sand has not kept pace with the exploding demand, which resulted in a supply-demand disparity. Suppliers of frac sand will be dependent on many catalysts to make a profit in the future. The growth in Mar- cellus and Utica shale fields in the NE will be key for the in- dustry, as well as the ability to create a network to distribute this commodity to its customers.

According to Hi-Crush the need for raw frac sand will nearly double from 2011-2021. The drilling activity in the industry is expected to remain flat. However, fracs per well and hori- zontal drilling are projected to increase, which will increase the demand for raw frac sand. The industry has high barri- ers for entry with many small players who have limited ca- pabilities. The possibility of vertical integration in the indus- try remains high.

Company Overview

Hi-Crush had its IPO in mid 2012 and is a master limited partnership (MLP) that produces monocrystalline sand which is a special material used as a proppant in oil and nat- ural gas wells. Hi-Crush owns and operates the Wyeville fa- cility which is located in Wisconsin. Hi-Crush also owns a preferred interest in its sponsor’s Augusta facility which is also located in Wisconsin. Both facilities have proven recov- erable Northern White sand reserves of 54 and 48 million tons, respectively. Hi-Crush wants to be a one stop shop for its customers. Hi-Crush is showing its ability to execute on those statements through their acquisition of D&I, which is its distribution arm for the frac sand. This gives Hi-Crush a competitive advantage over its competitors who are able to produce the frac sand but not at the same effectiveness at which Hi-Crush can.

The frac sand Hi-Crush produces is sold to pressure pump- ing service companies, which are comprised of subsidiaries of premier North American oilfield companies. The majority of its production is sold freight on board (FOB) at the mine site under long-term, take-or-pay contracts that require cus- tomers to pay a specified price for a specified volume of frac sand each month. Hi-Crush maintains adequate supply and flexibility to meet customer needs, with access to different variations or mesh sizes of Northern White raw frac sand.

Hi-Crush’s Wyeville facility has a capacity of mining 1.6 mil- lion tons of raw frac sand per year. At both facilities, there are three 5,000 foot rail spurs which connect to Union Pacif- ic rail lines that allow for cost effective transportation to its customers.

Company Expansion

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

UITY REPORT

Source: Hi-Crush Partners LP.

UITY REPORT

Source: Hi-Crush Partners LP.

3. Prepared by Eric McNew and Michael Schopler 3

Hi-Crush LP

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

Proppant Price and Crush Resistance

Hi-Crush

Northern White

Brandy Brown

Resin Coated

Ceramics

0

2500

5000

7500

10000

12500

15000

$- $250 $500 $750 $1,000

Crush Resistance (lbs/in2)

Price($/Ton)

Types of Proppant

Northern White Brandy Brown Resin Coated Ceramics

Northern White frac sand is considered the highest

quality frac sand in the nation, if not the world. This

type of sand generally does not require blasting or

crushing. Relative to the sand’s crush strength, of

between 11,000 - 12,000 psi, Northern White frac

sand is most cost efficient option currently available.

This type of sand is known for its roundness, spheric-ity,

and uniform grains which allow it to capture the

greatest market demand relative to supply.

Brandy Brown frac sand is the least expensive of all

proppants but also has the lowest crush strength.

Brandy Brown sand is less desirable than Northern

White sand in high stress applications but is

How it Works Hydraulic Fracturing

Hydraulic fracturing is used as a means to crack open, or fracture, a

hydrocarbon based reserve in order to allow the hydrocarbons to flow

freely to the surface. Once the rock is fracked, a mixture of water,

chemicals, and proppant is used to greatly increase the flow of hydro-carbons

to the surface. Once the mixture is pumped in, the proppant is

used to hold open these cracks. Since the sand is highly permeable it

allows the flow of hydrocarbons to go to the surface, thereby expo-nentially

increasing the yield from wells. In the case of Hi-Crush,

Northern White sand is the most desired form of proppant because of

its cost and effectiveness.

UITY REPORT

Source: Hi-Crush Partners LP.

considered high quality frac sand.

Resin-coated sand is sand that has been treated with resin to increase its strength and allow for the fissures to be open

longer increasing the flow of hydrocarbons. It is roughly 5 times the price of Northern White sand as a result of the resin

coating process.

Ceramic is the best proppant in regards to strength, but it also is the most expensive of the three main proppants. On aver-age

it is ten times more expensive than Northern White frac sand and about 50% more expensive than resin coated. Ceramic

sand is man made, so it has been engineered to have the best strength, and porous capabilities because they are almost per-fectly

spherical.

4. Prepared by Eric McNew and Michael Schopler

4

Hi-Crush LP

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

Demand

The demand for raw frac sand through 2016 is ex- pected to grow 7.2% annually and double by 2021. Demand will increase because the number of fracs per well is increasing from 8-12 to 12-16 while the number of new wells being introduced is expected to remain flat. The increase in horizontal drilling is what will be causing the demand of sand per well to increase. Improvements in horizontal drilling tech- nologies will allow for horizontal laterals to go deep- er into the rock.

Tons of Proppant / Well

Supply

Hi-Crush’s Facilities

UITY REPORT

Source: Hi-Crush Partners LP.

Customers

Another factor that affects demand for raw frac sand is a breakeven price of oil and natural gas. The breakeven prices for oil and natural gas vary depending on the shale basin. Utica and Marcellus locations tend to have lower breakeven prices as drilling is more cost effective in these low price environments. Natural gas prices would have to fall to around $2.50 in order to create pressure for companies. Breakeven oil prices vary depending on the region and are anywhere from $50-$80BBl. Hi-Crush customers’ operate in locations such as Eagle Ford and Permian where there are breakeven prices of $65 and $75 re- spectively.

In 2012 Hi-Crush had 3 customers. Most recently that number has increased eight fold to 25 customers. This growth shows the rapidly increasing demand for raw frac sand in the industry, and particularly Northern White sand which is the type sup- plied by Hi-Crush. Hi-Crush has contracted 90% of its supply to these various customers in order to secure revenue. The remaining 10% is sold in the spot market, which could help the company develop new customers through product place- ment.

For the past few years the under supply of raw frac sand has caused a vast range of prices for raw frac sand because the demand has far ex- ceeded the supply available. As a result of this high margin business, new suppliers have entered the market and are in the processes of be- ing incorporated or are still in the organizational process. Competition is coming into the market but Hi-Crush is the dominant supplier in raw frac sand and will be the company to survive competition through the large barriers to enter the industry because of its current market posi- tion. Furthermore, Hi-Crush has two facilities through which they have access to raw frac sand. The Wyeville location is its primary facility that generates 90% of their revenues. Another facility that it has access to is Augusta, in which it owns a preferred interest.

The company’s supply of raw frac sand has limited-to-no overburden and allows it to cut costs in the excavating process. Gerke Excavating is a third-party contractor that is responsible for this process and has contracted agreements with Hi-Crush for every ton of sand that is exca- vated.

UITY REPORT

Source: Hi-Crush Partners LP.

Augusta Facility

33 Year Life

Wyeville Facility

37 Year Life

5. Prepared by Eric McNew and Michael Schopler

5

Hi-Crush LP

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

Competitive Advantage

Risks and Mitigants

New competition will be entering the market soon but we expect Hi-Crush to be able to stay the dominant market supplier for the following reasons.

Proven Reserves

Based on the research done by a third party independent reserve engineer, Hi-Crush has proven reserves of Northern White frac sand that amount to 54 million tons or an implied 37 year reserve life at its Wyeville facility. Augusta’s facility contains 48 million tons of proven reserves or an im- plied 33 year reserve life.

Cost Structure

Hi-Crush also has a superior cost structure. This is a result of its most recent acquisition of D&I at the beginning of 2013. D&I, which is a distribution system used by Hi-Crush to transport the sand to its customers directly from the facility, is a major catalyst for this company. Hi-Crush is well on its way to becoming a one stop shop for its customers. Its most recent earnings call reported that it costs the company just $13.10 per ton to produce the sand as compared to $13.28 a quarter earlier showing that the company is becoming more efficient at managing costs.

Transportation

Much of this low cost per ton is attributable to D&I because it does not need to hire trucks to trans- fer the sand to its transportation site which on average adds another $5 per ton. Hi-Crush has a strong relationship with Union Pacific and is able to use “unit trains” to capitalize on just-in-time shipments to its customers.

Contracted Revenue

Hi-Crush’s contracted revenues are also a major intangible. It is advantageous on both sides be- cause it allows for Hi-Crush to better judge its cash flows and its costs as compared to other compa- nies that do not have contracts who would experience large cyclical shifts in its cash flows. It is also advantageous for its customers because all customers are locked in at a much lower price than the current price of Northern White frac sand. Of those contracts, the earliest one is set to expire in the summer of 2014.

Product Innovation

Naturally, there is a possibility in the future that a new product will arise that will take the place of raw frac sand as the pre- ferred proppant. If this new product offers superior crush strength at an even lower cost it would affect Hi-Crush’s future earning potential.

Regulatory Risk

Any litigation that adversely would effect the fracking industry would impact Hi-Crush. There are also health concerns in mining the sand. Hi-Crush hires a third party excavating contractor that is highly skilled in this industry and well trained in safety regulations.

Energy Prices

If oil and natural gas prices fall below break even we would expect there to be a receding trend in the short term. Hi-Crush has mitigated this risk through its contracts that allow for litigation against its customers if they refuse shipments of sand.

Vertical Integration Risk

There are risks from M&A possibilities as well as pressure from its sponsor who holds the majority ownership of Hi-Crush.

Lack of Historical Data

Hi-Crush had its IPO in mid-2012. Therefore there is a lack of financial data associated with this investment.

6. Prepared by Eric McNew and Michael Schopler

6

Hi-Crush LP

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

2012

2013E

2014E

Liquidity

Current

5.19

5.21

5.86

Quick

4.54

4.00

4.26

Solvency

Debt/Equity

0.07

1.05

1.33

Interest Coverage

13.4

15.6

10.0

Efficiency

Receivables Turnover

12.37

8.73

9.37

Asset Turnover

0.74

0.46

0.50

Profitability

Gross Margin %

73%

56%

52%

Operating Margin %

62%

46%

41%

Net Margin %

58%

43%

37%

Financial Health

2012

2013E

2014E

2015E

2016E

Net Margin

58%

43%

37%

39%

38%

Asset Turnover

0.74

0.46

0.50

0.40

0.35

Equity Multiplier

1.07

2.05

2.33

2.29

2.21

Return on Equity %

46%

40%

43%

36%

30%

Time Series DuPont

Liquidity

Financial strength is increasing showing the company is well able to repay its short term liabilities in the future.

Quick ratio is remaining around 4.25x showing that the company is able to repay $4.25 for every dollar of liabilities. The company is in a highly liquid position.

Solvency

Hi-Crush began leveraging returns to common unit holders through the use of debt in 2013. Since the company has no re- tained earnings, the only way to finance its operations is through long term debt or limited partner ownership.

Interest coverage remains high, showing the company is able to repay its interest payments on average 12 times.

Ratio Analysis

Efficiency

Receivables turnover is decreasing which is showing Hi-Crush is collecting from its customers more efficiently.

Asset turnover is decreasing, we expect Hi-Crush to not generate as much sales from its assets but instead focus on high profit mar- gins. This focus leads to a lower asset turnover figure.

Profitability

Margins are decreasing over a three year period because we ex- pect more suppliers to enter the market. Therefore, Hi-Crush’s once astronomical margins will begin to recede. We expect mar- gins to remain at a very respectable level across all metrics in our scenarios.

7. Prepared by Eric McNew and Michael Schopler 7

Hi-Crush LP

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

Valuation Dividend Discount Scenario

3-Year Price Target Sensitivity Schedule

Methodology

We utilized a dividend discount model (DDM) to evalu-ate

the intrinsic value of Hi-Crush. Since Hi-Crush is an

MLP, 90% of its earnings are paid out as distributions.

Below are different scenarios that could happen to the

stock’s price based on a multi-stage DDM employed to

produce the different scenarios. There are several as-sumptions

in the model:

Risk-Free Rate: We used a 10 year Treasury bond rate

for our riskless rate (3%).

Hi-Crush’s Equity Beta: We evaluated Hi-Crush’s equi-ty

beta based on regression analysis modified for for-ward-

looking convergence. Since there is limited data

we adjusted the equity beta in each scenario to fully

represent a bear, base, and bull scenario.

Equity Risk Premium: We estimated the equity risk

premium at different values in each scenario for the

purposes of our model. See each scenario below for

further explanation.

Value Drivers: Having access to more supplies, secur-ing

more contracts, cutting costs, partaking in M&A

activities.

2013E 2014E 2015E 2016E 2017E

0.00 $2.02 $2.82 $3.55 $4.32 $5.10

14.50 $29.29 $40.89 $51.48 $62.64 $73.92

15.50 $31.31 $43.71 $55.03 $66.96 $79.01

16.50 $33.33 $46.53 $58.58 $71.28 $84.11

P/E 17.50 $35.35 $49.35 $62.13 $75.60 $89.21

18.50 $37.37 $52.17 $65.68 $79.92 $94.31

19.50 $39.39 $54.99 $69.23 $84.24 $99.40

20.50 $41.41 $57.81 $72.78 $88.56 $104.50

$0

$10

$20

$30

$40

$50

$60

$70

Projected Intrinsic Values

$60 (62%)

$48(30%)

$30(-23%)

Bear (Equity Beta: 1.2, Equity Risk Premium: 7%)

In the bear case, we expect that Hi-Crush is not able to meet its target low-double-digit distributions as stated by manage-ment.

We also assume that the expected return on the market expands to 10% because of macroeconomic performance. This

scenario could occur if management does not manage costs well. Moreover, this scenario could be the result of not adding

value to the company through acquisitions of other competitors or other facilities, which will then lead to lower increases in

its distributions. Intrinsic value: $30

Base (Equity Beta: .9, Equity Risk Premium: 6%)

In the base case, we expect that Hi-Crush is able to meet its target distributions of low double digit growth over the next few

years. The equity beta becomes less aggressive than the market to .9, and the expected return on the market decreases to 9%.

In this scenario, Hi-Crush’s management continues to keep costs at current levels and moderately participates in acquisitions

that lead to higher profits, boosting distributions to unit holders. Intrinsic Value $48

Bull (Equity Beta: .8, Equity Risk Premium: 5.5%)

In the bull case, we expect that management increases distributions in the low double digits for a longer period of time and

then to high single digits. We also assume the equity beta decreases even further to .8, and our expected return on the market

decreases to 8.5%. In this scenario, we expect management to actively partake in acquiring other companies that will lower

input and operating costs as well as acquiring and consolidating with nearby facilities that have supply of Northern White

frac sand. The actions will further boost top and bottom line numbers. Intrinsic value $60

$36.83

8. Prepared by Eric McNew and Michael Schopler

8

Hi-Crush LP

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

INCOME STATEMENT ($ MILLIONS)

2011

2012

2013E

2014E

2015E

2016E

Revenues

20,353

75,634

136,141

217,826

261,391

326,739

Cost of goods sold

6,447

20,481

60,000

105,000

118,650

148,313

Gross profit

13,906

55,153

76,141

112,826

142,741

178,426

Operating costs and expenses:

General and administrative expenses

2,324

7,426

13,614

21,783

26,139

32,674

Exploration expense

381

630

58

600

600

600

Accretion of asset retirement obligation

28

72

120

120

120

120

Income from operations

11,173

47,025

62,349

90,323

115,882

145,032

Interest expense

1,893

3,503

4,000

9,000

13,500

20,250

Net income (loss)

9,280

43,522

58,349

81,323

102,382

124,782

Earnings per unit

$1.60

$2.02

$2.82

$3.55

$4.32

INCOME STATEMENT (% OF REVENUE)

2011

2012

2013E

2014E

2015E

2016E

Revenues

100%

100%

100%

100%

100%

100%

Cost of goods sold

32%

27%

44%

48%

45%

45%

Gross Margin

68%

73%

56%

52%

55%

55%

Operating costs and expenses:

General and administrative expenses

11%

10%

10%

10%

10%

10%

Exploration expense

2%

1%

0%

0%

0%

0%

Accretion of asset retirement obligation

0%

0%

0%

0%

0%

0%

Operating Margin

55%

62%

46%

41%

44%

44%

Interest expense

9%

5%

3%

4%

5%

6%

Profit Margin

46%

58%

43%

37%

39%

38%

9. Prepared by Eric McNew and Michael Schopler

9

Hi-Crush LP

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

BALANCE SHEET ($ MILLIONS)

2011

2012

2013E

2014E

2015E

2016E

Current assets:

Cash

11,054

10,498

25,000

30,000

30,000

30,000

Restricted cash

30

0

0

0

0

0

Accounts receivable

4,026

8,199

23,000

23,500

24,000

24,500

Inventories

2,374

3,541

15,000

20,000

25,000

30,000

Due from sponsor

0

5,615

1,615

0

0

0

Prepaid expenses and other current assets

294

393

0

0

0

0

Total current assets

17,778

28,246

64,615

73,500

79,000

84,500

Property, plant and equipment, net

52,708

72,844

112,290

209,065

418,130

689,915

Preferred interest in Augusta

0

0

47,043

47,043

47,043

47,043

Goodwill

0

0

73,598

106,717

106,717

106,717

Deferred charges, net

1,743

1,095

0

0

0

0

Total assets

72,229

102,185

297,546

436,325

650,890

928,175

10. Prepared by Eric McNew and Michael Schopler

10

Hi-Crush LP

Equity Report | January 28, 2014 | NYSE: HCLP

Hi-Crush Partners LP

BALANCE SHEET ($ MILLIONS)

2011

2012

2013E

2014E

2015E

2016E

Current liabilities:

Accounts payable

4,954

1,977

8,000

8,100

8,200

8,300

Accrued liabilities

866

1,755

4,400

4,450

4,500

4,550

Deferred revenue

9,178

1,715

0

0

0

0

Total current liabilities

14,998

5,447

12,400

12,550

12,700

12,850

Long term debt

0

0

138,250

235,025

352,538

493,553

Asset retirement obligation, net

832

1,555

1,643

1,643

1,643

1,643

Total liabilities

61,942

7,002

152,293

249,218

366,881

508,046

Partners' capital:

Limited partner interest

10,287

95,183

135,000

175,000

270,000

410,000

Other equity items

0

0

10,253

12,107

14,009

10,129

Total equity

10,287

95,183

145,253

187,107

284,009

420,129

Total liabilities and partners' capital

72,229

102,185

297,546

436,325

650,890

928,175