2. Corporate Valuation Report

Activision

67%

Blizzard

26%

Distribution

7%

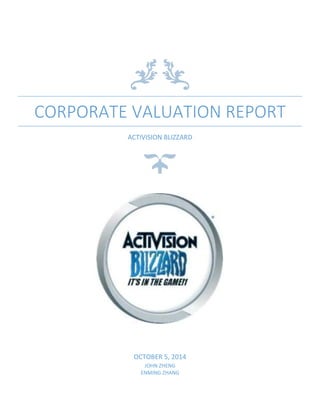

2013 Net Revenue

Activision Blizzard Distribution

0.00%

200.00%

400.00%

600.00%

800.00%

1000.00%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

ATVI S&P 500 NASDAQ 100

Activision Blizzard, Inc. (Nasdaq: ATVI) | Recommendation: HOLD

Current Price Target Price Sector: Technology

$ 21.21 $ 22.38 Industry: Software & Programming

Business description

Activision Blizzard is the currently largest and most profitable game

publisher and developer of video game, handhold game and online PC

game. It was established in 2008 by merging Activision Publishing Inc.

and Blizzard entertainment. The business of Activision Blizzard is

consisted of two separate parts, Activision Publishing, Inc. (“Activision”)

and Blizzard Entertainment, Inc. (“Blizzard”). In 2013, Activision and

Blizzard accounted to 67% and 26% of revenue of whole company

respectively.

Activision

On the Activision Publishing lnc. side, which is focus on developing and

publishing video game on various platforms, such as XBOX 360 and XBOX

ONE of Microsoft, PlayStation3 and PlayStation4 of Sony, Wii U and Wii of

Nintendo Company for home playing. All products from above platforms

are also provided in handle and mobile platform such as the Nintendo

3DS ("3DS"), Nintendo Dual Screen ("DS") and Sony PlayStation Vita

handheld game systems. There are various star products of Activision.

The main revenue of Activision is comes from Call of Duty series and

Skylander franchise. The latest version of Call of Duty, which was

released in last quarter of 2013, won the #1 best-selling game and also

the #1 best-selling game for new generation platform. Skylander

franchise is another long-term investment and profitable asset of

Activision. Since 2012, the first generation of Skylander launched in

market, it has accumulated 2 billion around the world and 175 million

Skylanders toys sales until December 31th, 2013. Also Activision

developed a new first-view shooting game-Destiny with building long-

term corporation with Bungie. In order to rich the list of products,

Activision also developed and maintained “Goldeneyes 007” and

“Transformer’ series even they held low market shares and kept low

growth rates.

Blizzard

On the other side, Blizzard entertainment is concern on developing online

ATVI Performance

All raw data used in charts, graphs and

calculations is sourced from Bloomberg

3. Corporate Valuation Report

ASAC II LP

15%

FMR LLC

7%

WELLINGTON

MANAGEMEN

T

7%VIVENDI

UNIVERSAL

SA

6%BLACKROCK

4%VANGUARD

GROUP INC

2%

DAVIS

SELECTED

ADVISERS LP

2%

INVESCO LTD

2%

activision

blazzard

36%

OTHERS

19%

game market and keeping its dominant position in subscription-based

MMORPG (massive multiple online role-play game) category and PC

online category. In the global market, Blizzard built a great reputation

among gamers through its three products; StarCraft series, World

Warcraft series and Diablo series in past 20 years. On January 2014, the

new game Heroes of the StormTM, a free-to-play digital collectible card

game, which lunched for Windows, Mac and IPAD consoles and rapidly

increased to 10 million register customers currently. Diablo III has sold

more than 20 million copies worldwide across all platforms since its

release in March 2012. World of Warcraft remains the #1 subscription-

based MMORPG, with approximately 6.8 million subscribers. In addition

Blizzard also developed an online game service, Battle.net. It plays

several roles, such as 24/7 gamer services, digital distribution and social

platform for gamers in 4 major games. Blizzard runs their business

worldwide through its 4 main products. There are various ways to

generate revenues from major products, including: sales of subscription

cards, physical and digital products of PC games; and additional charged

services in the World of Warcraft; and outsourcing software distribution

to third-party oversea companies.

Shareholder Structure

In October 11th, 2013, the ownership of Activision

Blizzard was changed. It repurchased 429 million

common shares from Vivendi by 5.83 billion cash

payment or $13.60 per share. This repurchase

transaction payment was consist of 1.2 billion of

cash, net proceeds from a $2.5 billion secured loan,

which due to October 2020, and the net proceeds

from a $1.5 billion with 5.625% unsecured senior

notes due September 2021 and $750 million of

6.125% unsecured senior notes due September

2023. This transaction made a further influence on

Activision Blizzard’s operation and financial

condition in coming years. Otherwise, this

repurchase liberate Activision Blizzard from Vivendi

by total 36% of entire shares. Additionally, Robert

A. Kotick, Activision Blizzard’s Chief Executive

Officer, and Brian G. Kelly, Chairman of Activision

Blizzard Board of Directors founded the second shareholder, ASAC II LP.

This independent structure gave Activision Blizzard more freedom to

operate their business but the heavy debts also limited its development

in the future.

4. Corporate Valuation Report

0

1

2

3

4

threat of

entry

bargaining

power of…

bargaining

power of…

subsititues

rivalry

Industry Analysis

Activision Blizzard is currently the largest and most-profitable

independent videogame publisher in North America and Europe.

Activision Blizzard is holding several most popular game series in the

world, Call of Duty Ghosts - #1 title on next-gen consoles; World of

Warcraft - #1 subscription massively multiplayer online role-playing game

as of 12/31/2013; and StarCraft II: Heart of the Swarm - #1 PC game in

North America.1 All of ATVI’s biggest franchises tend to keep gamers

engaged for significantly longer than competitive offerings. In FY2013,

ATVI had the highest revenue of $4.3B, the highest net income of $1.01B

and the highest free cash flow of $1.19B over other major competitors –

Electronic Art, Take-Two Interactive, Nintendo and Konami.2 Because the

gaming (software and programming) industry in America is mature

enough, its growth rate is estimated to be 4% based on future U.S. GDP

growth rate estimates. ATVI is going to release two sequels of Call of Duty

and World of Warcraft during November in 2014 which will definitely

stimulate ATVI’s future sales and increase its overall influence in the

marketplace.

Comparative Analysis

Porter’s Five Forces

Threat of New Entrants (Low): Due to increasing returns generated from

making games and being game agent in gaming industry, more and more

new entrants is constantly entering the market. It requires relatively low

cost to enter the market. As the largest game making and publishing

company in the world, ATVI minimizes this threat by building a large

economics of scale and a wide product differentiation and maintaining its

dominant position in the market. Comparing to entry, it is much harder to

stay in the market by maintaining quality and even better. ATVI is keeping

a high level of quality and even innovating its famous game series while

most new entrants failed maintaining good quality and got kicked out of

market. Thus, it automatically lower the company’s risk to the threat of

new entrants.

Threats of Substitute Products or Services (Low-Moderate): The

Activision Blizzard is famous for its first-person shooter game, real-time

strategies game, and massive multiplayer online role-playing game.

1

Activision Blizzard Annual Report 2013

2

http://www.fool.com/investing/general/2014/08/26/3-reasons-why-activision-blizzard-is-the-king-of-v.aspx

Porter’s Five Forces Analysis

5. Corporate Valuation Report

Blizzard benefit from first two types of games by selling game discs and

game relative products. First two types of games have long history since

the console game period. They are considered as classic game in

customers’ view. The model and market of games is mature. All

substandard products of these two types in the market will not be able to

compete with Blizzard. So far, Blizzard can be ranked as moderate in

substitute. However, World of Warcraft from Activision Blizzard make it

become the most successful MMOPG game company. It earned high

reputation from customers in world of Warcraft around world. Above all I

would like to give “low” ranking of Blizzard in substitute option.

Bargaining Power of Buyers (High): Customers’ powers have increased

since 2000. Based on the high information flow, customers can search

tremendous and relative information that is specific in their interests

through magazines, digital newsblog and social media. Customers keep

looking for high quality games and have low costs of switching. The

better quality direction from customers force industry spend high portion

of capital in developing and researching. In developing countries, the

rapidly increasing pc users’ volumes enlarge the power of customers in

local market price. On the other hand, the brand loyalty is relative low in

game market. Customers can easily move to another public games when

they can earn higher utility in others. Game companies set up building

their brand reorganization which also resulting in high cost of marketing.

Consequently, the margin power of buyers stays in high level.

Bargaining Power of Suppliers (Low-Moderate): Activision Blizzard Inc.’s

products are primarily produced by its own teams. It contains several

studios that develop and innovate new video games for ATVI to publish.

Since the majority of video games that has being published by ATVI are

made by its own teams and studios, suppliers have little influence on

developing video games’ contents other than building and packaging

video game disks. The level of supplier power is not tend to be high

because there are tons of companies that can provide building and

packaging video game disks for ATVI. Although the majority of games are

made by its own, ATVI still publishes many video games for other game

making companies. ATVI want to continue attracting and keeping the

best games from other game making companies which hold some power

here.

Rivalry (Moderate): There are tons of different software and

entertainment companies that are developing and publishing video

games like ATVI. The game industry is intensely competitive and there are

competitors competing with ATVI in every type of video games. ATVI’s

most successful game series are Call of Duty and World of Warcraft. In

6. Corporate Valuation Report

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

2008 2009 2010 2011 2012 2013

EBIT Margin EBITDA Margin

Net Profit Margin

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

3,800.0

4,000.0

4,200.0

4,400.0

4,600.0

4,800.0

5,000.0

5,200.0

Revenue

Revenue Growth Rate

Industry Average Revenue Growth Rate

these two types which are first-person shooter and massively multiplayer

online role-playing game, ATVI dominate the market and no one can

actually compete with it. Electronic Arts is the largest competitor of ATVI,

and they compete with each other in nearly every types of video games.

ATVI is dominating EA because ATVI continues its popular game series

such as Call of Duty and Guitar Hero to maintain old customers and

innovates new games such as World of Warcraft (by Blizzard

Entertainment) to attract new customers. Knowing what exactly

customers and players want is the key to build customers’ loyalty to

against rivals. As the world’s largest game developing and publishing

company, ATVI is not strictly affected by new entrants to the game

industry.

Financial Analysis

Sustainable Revenue Growth

From FY2009 to FY2012, ATVI’s revenue continued to increase from

$4,279 million to $4,856 million. The revenue growth rate are tend to be

high of more than 40% in FY2009 and the revenue was keep increasing

from FY2009 to FY2012, the reasons are because the two most popular

game series – Call of Duty and World of Warcraft have been released for

4, 5 years and have attracted tremendous amount of players until FY2009

and FY2010, plus Wold of Warcraft has reached its peak of 12 million3

subscriptions between FY2009 and FY2010. With a 4% growth rate

estimates, revenue will increase to $4,766 million in FY2014 and 4967

million in FY2015.

Low Revenue Growth Rate and Revenue Decline in FY2013

ATVI’s revenue growth rates are all lower than industry average growth

rates4 because there are so many small companies that have relative

higher revenue increases than ATVI in the software and programming

industry. Both ATVI and industry average revenue growth rate curves are

moving in a similar pattern predicts that the industry is obviously being

influenced by ATVI. In FY2013, ATVI’s revenue decreased at a rate of 5.62%

from $4,856 million to $4,583 million. The reason is that ATVI

repurchased 429 million common shares from Vivendi by paying $5.83

billion in cash in FY2013. Revenue growth rate is tend to stop declining

and start rising up in FY2014.

3

http://www.nextgeekuk.com/section/gaming/world-of-woecraft-fixing-the-warcraft-franchise

4

All industry averages were sourced from Bloomberg.

ATVI Historical Margins

ATVI Revenue and Growth

7. Corporate Valuation Report

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

EBITDTA

Margin

EBIT Margin Profit Margin

ATVI Industry Average

0

100

200

300

400

500

600

R&D Expenditure

Activision

Blizzard

Dassault

Systemes SA

Zynga

Linkedin

Cerner

Yandex

Historical Margins and Margin Comparison

ATVI’s EBIT margin, EBITDA margin, and net profit margin all rapidly

increased from FY2008 to FY2011. EBIT margin grew from -4.63% in

FY2008 to 29.94% in FY2013; EBITDA margin grew from 13.91% in FY2008

to 36.81% in FY2013; and net profit margin grew from -3.54% in FY2008

to 22.04% in FY2013. Great increasing in margins from FY2008 to FY2013

and the stabilization from FY2011 to FY2013 reflect the company’s

successful operation over the last few years. By comparing to the

industry average margins, ATVI’s FY2013 EBITDA margin of 36.81% is

greatly higher than the industry average EBITDA margin of 27.1%. ATVI’s

FY2013 EBIT margin was 29.94%, and it was also significantly above than

the industry average of 17.86%. Net profit margin for ATVI in FY2013 was

22.04% and it was also higher than the industry average which was

16.37%. All these margin comparisons show that ATVI is strictly

outperforming the industry.

Margins Increase in FY2009, FY2010, and FY2011

In FY2009, FY2010 and FY2011, ATVI’s all three margins increased by

about 10% or even more than 10% each year (shown in the table). This is

because the succession in selling World of Warcraft and Call of Duty in

FY2009 and FY2010 significantly increased the revenue during those fiscal

years. As these hot game series are tend to be constant and saturated

from FY2011 to now, the margins are also tend to be stable in these fiscal

years.

Profit Margin Decreases in FY2013

The net profit margin for ATVI dropped from 23.66% in FY2012 to 22.04%

in FY2013. Because the revenue decreased at a rate of 5.62% to $4,583

million in FY2013 from $4,856 million in FY2012 mainly caused by the

ATVI’s repurchase of common shares from Vivendi by paying $5.83 billion

in cash in FY2013.

Innovation from R&D

The R&D expenditure for ATVI was $584 million in FY2013 which was

higher than other companies’ R&D expenditures in the industry.

Maintaining a high R&D expenditure allows ATVI to perform aggressive

investment and develop innovative products. A high R&D expenditure is

necessary for a company in software and programming industry, because

high R&D expenses allow a company to research and develop new

featured products and technologies. ATVI’s high R&D expenses ensure

that ATVI is able to develop three to four qualified and innovative games

2009 2010 2011

EBIT

Margin

-0.61% 10.55% 27.93%

EBITDA

Margin

14.07% 22.17% 37.08%

Net

Profit

Margin

2.64% 9.40% 22.82%

Margin Comparison

2009-2011 Margins

Innovation from R&D

8. Corporate Valuation Report

0

500

1000

1500

2000

2500

3000

3500

Gross Profit

Activision

Blizzard

Dassault

Systemes SA

Zynga

Linkedin

Cerner

Yandex

46.09

52.19

62.73 65.77 66.59 69.07

0

10

20

30

40

50

60

70

80

Gross Margin

Gross Margin

-60

-40

-20

0

20

40

60

80

2009 2010 2011 2012 2013

Days

Cash Conversion Cycle

Activision Blizzard industry average

every year. This a major reason why ATVI can maintain its highest

revenue over other competitors every year.

High Gross Profit and Gross Margin

ATVI’s gross profit in FY2013 was $3,052 million which was the highest

among all the competitors. Gross profit increased from $1,972 million in

FY2009 to $3,052 million in FY2013. High R&D expenditures in the last

few years influenced this increase. The gross margin (Gross

Profit/Revenue) for ATVI grew from 46.09% in FY2009 to 66.59% in

FY2013 and it already increased to 69.07% currently in 2014. ATVI was

increasing the ratio (Gross Margin) over the past five years by cutting the

cost of sales year by year. The gross margin was not influenced by the

repurchase of common shares in FY2013 because the gross profit

decreased by $142 million which is less than the decline in revenue ($273

million). A high gross margin of 66.59% in FY2013 means a high ratio of

gross profit over revenue which indicates ATVI can retain 66.59% of total

sales revenue after incurring the cost of sales. High gross margin gives

ATVI a sustainable financial situation.

Cash Generating Ability

Cash conversion cycle is calculated by subtracting days payable

outstanding from the summation of days sales outstanding and days

inventory outstanding. ATVI’s average cash conversion cycle decreased

from 63.3 days in FY2009 to 8.6 days in FY2013. This is mainly caused by

reductions in days sales outstanding and increases in days payable

outstanding year by year. From FY2009 to FY2011, cash conversion cycle

for ATVI declined rapidly because ATVI greatly reduced the days sales

outstanding from 73.1 days to 50.7 days and increased the days payable

outstanding from 49.6 days to 76.2 days. Although ATVI’s cash conversion

cycle declined to 8.6 days in FY2013, it is still greater than the industry

average which means ATVI is outperforming the industry in cash

generating ability. Two similar curve patterns also indicates the dominant

position and influential power of ATVI within its industry.

Liquidity

The current ratio for ATVI was 2.6x and quick ratio for ATVI was 2.1x in

FY2013. The inventory turnover and receivable turnover for ATVI in

FY2013 were 8.1x and 7.5x. These two turnovers are not low enough to

say ATVI is very safe in meeting its short-term obligations. Another

reason for ATVI’s high current ratio and quick ratio is its currently high

debt level caused by a large debt incurred in FY2013.

High Gross Profit

9. Corporate Valuation Report

0

2

4

6

8

10

12

14

16

2010 2011 2012 2013

ROIC vs. WACC

ROIC (%) WACC (%)

2010

DPS=0.15

2011

DPS=0.17

2012

DPS=0.18

2013

DPS=0.19

2014

DPS=0.20

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

2010 2011 2012 2013 2014

Dividend Yield in 2010-2014

Sustainable Dividend per Share and Dividend Yield

The dividend per share for ATVI was $0.15 in FY2010 and it increased at a

constant rate to $0.19 in FY2013 and already approached $0.20 in 2014.

Keeping increasing in the dividend per share provides shareholders

higher and higher returns. ATVI gives its shareholders or investors a good

reason for investing and holding ATVI shares. The dividend yield

increased from 1.21% in FY2010 to 1.69% in FY2012 which was caused by

increasing in dividend per share since the share price wasn’t change a lot

from FY2010 to FY2012. The dividend yield decreased to 1.07% in FY2013

due to the repurchase of common shares. Repurchase of 429 million

common shares reduced the common shares outstanding and thus

greatly increased the price per share. Because dividend yield = dividend

per share / share price, the increase in price per share from $14 to $23

effectively reduced the dividend yield in FY2013 and 2014. However, an

increase in share price is beneficial to shareholders as well as rising in

dividend per share.

ROIC vs. WACC

Return on invested capital for ATVI rapidly increased from 9.5% to 15.11

from FY2010 to FY2011 due to the success in Call of Duty and World of

Warcraft (NOPLAT increased 64.03%). And it decreased in FY2013 to

14.31% due to the repurchase by paying a significant amount of cash

(NOPLAT decreased 8.05%). We excluded the FY2009 ROIC for ATVI

because it was negative caused by an interest tax income instead of an

interest tax expense. Weighted average cost of capital for ATVI stays

constant through the last 5 years which is a good sign for a company.

ROIC is greater than WACC means that ATVI uses it invested capital

effectively and growth will add value.

Growing DPS

10. Corporate Valuation Report

0

2,000

4,000

6,000

8,000

2014 2015 2016 2017 2018 2019

Forcast Revenue

Forcast Revenue

Valuation

Target Price

We evaluate the price of Activision Blizzard by two valuating model:

Discounted Cash Flow and relative valuation. Target price ($22.38) was

calculated by averaging price from DCF model ($20.52) and RV model

($24.24).

DCF Model

Discounted Cash flow valuation method value future target price through

future after-tax cash input company’s capital. It is consisted by present

value of future forecast cash flow and terminal value at a perpetual

growth rate, which is also predicted, and then divided by the number of

common shares outstanding after subtracting net debt of Company. In

order to find out target price in DCF model, Firm Value The discounted

rate in DCF model is taken from weight average cost of capital.

Stable Revenue Growth

Future cash flows are strongly relative to revenue growth rate and cost of

good sell rate. We forecast 4% as fixed future growth rate are depend on

the high correlation between our sales and economic condition and the

past performance of Activision Blizzard when they released new products

to market. The reverse of revenue in 2013 is the result of high-level debt

from repurchases transaction. Then we also assumed perpetual growth

rate is 4%, which is based on the industry average growth rate and future

US Real GDP growth rate estimates by research of Federal Reserve Bank,

which scope of 2.1% to 2.3% in 2014 and 2.5%-3.0% under the sluggish

recovery. Additionally, the performance of technology industry is always

better than market average. For these reasons, we predicted perpetual

growth rate is 4%. Our assumption of growth rate is equal to perpetual

growth rate because of stable revue growth and increased interests of

Activision Blizzard.

Weighted Average Cost of Capital (WACC)

We calculate WACC by Capital Assets Pricing Model (CAMP). We use 10

years treasury rate of 2.48% as risk free rate and market premium of 5.15%

by subtracting the risk free rate from the market return rate from S&P

500 index. The calculation of Beta for ATVI can be separate two parts.

First we find the Beta 0.98 from financial report and then we find the

unlevered beta by dividing 1 plus after tax D/E ratio. We averaged the

unlevered betas from ATVI and its main competitors. We used the

averaged unlevered beta for ATVI levered beta by multiplying 1plus after

10 Year Treasury 2.48%

Market Premium 5.15%

ATVI Beta 1.80

Cost of Equity 11.74%

Cost of Debt 3.52%

WACC 8.33%

WACC

Final Target Price

11. Corporate Valuation Report

1.1

7.6

2.82.1

17.6

5.7

0

5

10

15

20

PEG EV/EBITDA EV/Sales

ACTIVISION BLIZZARD Average

tax D/E ratio. ATVI beta was calculated to be 1.8. Input all relative

number into CAPM, we figure the cost of equity was 11.74%. On the

other hand, the cost of debt (before tax) was 4.6%, which was calculated

from a weighted average of interest rates. The tax rate was assumed of

23.43%. We estimated the WACC of 8.33% by combine the weighted

average of cost of equity and after-tax cost of debt.

Result of DCF

We discounted future cash flow by WACC as discounted rate and add

present value of term value at a perpetual growth rate and enterprise

value. At the end we divided the sum by outstanding shares to figure the

target price of $20.52.

Relative Valuation

The relative valuation was calculated and analyzed by using the following

three multiples: forward PEG ratio, forward EV/EBITDA, and forward

EV/Sales. We selected several US companies as peer companies. These

peer companies are all in the same industry as ATVI, and some are direct

competitors.

PEG Ratio

The first multiple used by us was PEG ratio, because we considered that

PEG ratio is a better multiple than P/E ratio. PEG ratio is a stock’s price-

to-earnings ratio divided by the growth rate of its earnings for a specified

time period. The PEG ratio is used to determine a stock’s value by taking

the earnings growth rate into account. A high P/E ratio might make a

stock look like a good buy, but it is not guaranteed without taking the

earnings growth into account. The lower the PEG ratio, the more the

stock might be undervalued given its earnings performance. ATVI’s PEG

ratio of 1.1x is the lowest among all other peer companies.

EV/Sales

The second multiple that we decided to use was EV/Sales. EV/Sales is a

valuation measure that divides the enterprise value of a company by the

company’s sales. EV/Sales is a capital-structure neutral measurement

compared to P/E ratio and PEG ratio. EV/Sales valuation is an appropriate

choice for ATVI because this multiple is indicative in the industry. We

usually can say that the lower the EV/Sales multiple a company has, the

more undervalued and attractive the company is. ATVI has the lowest

EV/Sales multiple of 2.8x among all peer companies.

Peer Companies and Multiples

Multiple Comparison

Discounted Cash Flow

12. Corporate Valuation Report

EV/EBITDA

The last multiple chosen by us for our valuation was EV/EBITDA.

EV/EBITDA multiple is used to determine the value of a company and it is

calculated by dividing enterprise value by the company’s EBITDA.

Because EV/EBITDA is also a capital-structure neutral multiple, it can be

used to directly compare peer companies with different capital structures

(different levels of debt). EV/EBITDA also excludes the influence of

different tax rates, depreciation and amortization methods. Thus,

compared to P/E ratio, EV/EBITDA is more accurate and more widely

used. Generally the lower the EV/EBITDA a company has, the more

undervalued that company is. ATVI has an EV/EBITDA of 7.6x which is the

lowest among all peer companies.

Forward Multiples and Relative Valuation Target Price

We used forward PEG ratio, forward EV/Sales, and forward EV/EBITDA to

perform the relative valuation. These three multiples for ATVI are all

lower than other peer companies and the industry average as shown in

the table. It is not reasonable to use the average multiples as our forward

multiples, therefore we directly took all these three forward multiples

from Bloomberg. By following all the calculation steps, the target price

obtained by using forward PEG (1.07x) is $26.10; the target price

obtained by using forward EV/Sales (3.30x) is $23.32; and the target price

obtained by using forward EV/EBITDA (9.64x) is $23.31. Finally, we

divided the sum of all these three target prices by three to get the

relative valuation target price which is $24.24.

Multiples Valuation

13. Corporate Valuation Report

0

50

100

150

200

250

StockPrice

ATVI SPY

68%

70%

72%

74%

76%

78%

80%

82%

2011 2012 2013

Revenue of 3 main products

0

2

4

6

8

10

12

2012 2013 2014 2015

Millions

Subscribers of World of Warcraft

Risk Analysis

Risk in Economy

Game products are not necessary to customers’ daily life, it is a

discretionary purchase of customers. Depend on high correlation

between the stock prices of Activision Blizzard and S&P 500 ETF Trust

(0.88). When the economic condition goes down, stock performance

would fall quickly, vice-versa.

Risk in Platform Transition

Most revenue of Activision is based on products, which provided for

platforms, such as Xbox, PlayStation and Wii. Every time new platform

announced or introduced to the market, the sales of Activision’s current

products would grow slowly or even decrease until the new generation

platform are achieved widely by consumers. The new-generation

products may not offset lacking of cash inflow from published products.

Conversely, Activision Blizzard has to finance fund to develop new-

generation products, which are available in new platform. During this

period, company market the current-platform products in discount price

and also incur extra cost in developing for next-platform without

immediate revenue.

Risk in Intensive Revenue

Depends on 10k of 2013, the total revenue of Activision Blizzard are

comes from 3 major products; World Warcraft, Call of Duty and Skylander.

Sales of these 3 products account 80%, 72% and 73% in 2013, 2012 and

2011 respectively. It is too risky to concentrate major revenue into

limited products. There is a potential problem about World Warcraft.

The Subscriber churn of World Warcraft brings a risk to the company. In

quarter 2 financial report, World Warcraft has 6.8million subscribers but

there were 7.6 million subscribers in 31st December,2013 and 9.6

million subscribers in 2012. The decrease subscribers or sales of each

product have significant influence on our business. Our financial

condition, results of operation, cash flow and liquidity could be materially

adversity effected.

Risk in Debt Burden

Because of Purchase Transaction, Activision Blizzard increased their debt

burden. The credit agreement include $2.5 billion secured term loan,

1.5billion unsecured senior notes with 5.625% interests rate, which due

September 2021, and 750 million unsecured senior notes with 6.125%

High Correlation with Market

14. Corporate Valuation Report

42%

25%

13%

20%

Payment Combination

long-term

loan

2021

notes

2023

notes

interests rate, which due September 2023. It increased D/E ratio to 70.8%,

which limited the adaptability of company to uncertainly changes in their

business and industry environment. In addition, the high level of debt

also limits extra financing for capital expenditures, research and

development, and present relative disadvantage to competitors with

lower capital leverage.

Risk in Foreign Business

In the past years, Activision Blizzard expanded their business around the

world. Even though net revenue in Asian market account to 7% of entire

income, the repaid growth rates of market volume attract most

company’s attention. Activision Blizzard intend to spread their game

storm to Asian market especially in China and South Korea, it have to fact

to the foreign business risks specific in regulation approval, foreign

exchange rate and foreign economic condition. In most Asian countries,

game products are not allowed to introduce to market as far as they

received authorization from national government. For instance, in China,

if Chinese government revoke its approval for our products we sold in

China in the future would make a significant adverse impact Activision

Blizzard’s business in China even reverse entire financial condition. In

additional, most of international operations are based on local currencies.

There are several currencies through Activision Blizzard global business,

including; Euro, British pound, Japanese yen, South Korean won and

Chinese Renminbi. The exchange rate of last two currencies may play

opposite fluctuation to U.S. dollar. In order to hedge the future exchange

rate risk, Activision Blizzard always enter forward currency derivative

market by forward contract, future contract or options. However no one

affirm they would keep purchasing those program and avoiding risks

from exchange rate fluctuation.

Conclusion

ATVI has a leader position in its industry, along with healthy financials

and blockbuster launches of new series of games. Although there are

several good signals to show a good prospect of ATVI, low revenue

growth, high debt burden and potential risks balance the advantages and

the overall only gives a 5.5% upside potential from $21.21 to $22.38.

Thus, we recommend to hold currently.

USD-KRW Trend

USD-CNY Trend

15. Corporate Valuation Report

Appendix A: Historical Balance Sheet

ATVI Historical Balance Sheet

$ millions 12/31/2009 12/31/2010 12/31/2011 12/31/2012 12/31/2013

Assets

Cash & cash equivalents 2,768 2,812 3,165 3,959 4,410

Short term investments 477 696 360 416 33

Accounts receivables, net 739 673 649 707 515

Inventories 241 112 144 209 171

Deferred income taxes (396) (301) 76 (10) 161

Prepaid expenses and other

assets

1,500 1,440 986 993 951

Total current assets 5,329 5,432 5,380 6,274 6,241

Net property, plant &

equipment

138 169 163 141 138

Goodwill & intangibles 8,243 7,808 7,706 7,736 7,589

Long-term marketable

securities

- - - - -

Other assets 32 38 28 49 44

Total assets 13,742 13,447 13,277 14,200 14,012

Liabilities & equity 2009 2010 2011 2012 2013

Accounts payable 302 363 390 343 355

Other Current Liabilities 779 871 694 652 661

Deferred Revenue 1,426 1,726 1,472 1,657 1,389

Total current liabilities 2,507 2,960 2,556 2,652 2,405

long term liabilities 479 284 229 231 4,985

Deferred Revenue - Non-

Current

- - - - -

Other Non-Current Liabilities

Common Stock 12,376 12,353 9,616 9,450 9,682

Retained earnings (361) 57 948 1,893 2,686

Accumulated Other Comp

Income

(1,259) (2,207) (72) (26) (5,746)

Total liabilities & equity 13,742 13,447 13,277 14,200 14,012