Keynote capitals india morning note 25 september-12

1.

India Morning Note

a

Tuesd

day, Septem

mber 25, 201

12

Dom

mestic Markets Snapshot

t V

Views on ma

arkets today

y

• The Sensex erased initial gains and closed 79 points

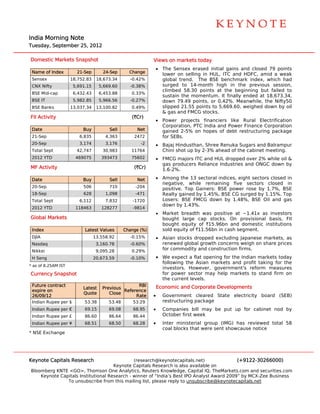

Nam of Index

me 21-Sep 24-Sep Change

lower on selling in H

n HUL, ITC and HDFC, am a weak

mid

Sens

sex 18,752.83 18,673.34

1 -0.42% global tr

rend. The B BSE benchm mark index, which had

CNX Nifty 5,691.15 5,669.60 -0.38% surged to 14-month high in t

t the previou session,

us

climbed 58.30 point at the be

ts eginning but failed to

BSE Mid-cap 6,432.43 6,453.88 0.33%

sustain t

the moment tum. It finally ended at 18,673.34,

y

BSE IT 5,982.85 5,966.56 -0.27% down 79 9.49 points, or 0.42%. Meanwhile, t

M the Nifty50

BSE Banks 13,037.34 13,100.82

1 0.49% slipped 21.55 points to 5,669.60 weighed d

2 0, down by oil

& gas an FMCG stoc

nd cks.

FII Ac

ctivity (`Cr)

• Power p projects fina

anciers like Rural Electrification

e

Corporattion, PTC Ind and Powe Finance C

dia er Corporation

Date

e Buy Sell Net gained 2-5% on hop

2 pes of debt restructuring package

21-Se

ep 6,835 4,363 2472 for SEBs.

20-Se

ep 3,174 3,176 -2 • Bajaj Hin

ndusthan, Sh

hree Renuka Sugars and Balrampur

Total Sept

l 42,747 30,983 11764 Chini sho up by 2-3% ahead of the cabinet m

ot % t meeting.

2012 YTD

2 469075 393473 75602 • FMCG majors ITC and HUL dropp

d ped over 2% while oil &

gas prod

ducers Relian

nce Industrie and ONGC down by

es C

MF A

Activity (`Cr) 1.6-2%.

Date

e Buy Sell Net • Among t the 13 sectoral indices, e

eight sectors closed in

negative while remaining fiv

e, ve sectors closed in

20-Se

ep 506 710 -204

positive. Top Gainer BSE pow

rs: wer rose by 1.7%, BSE

18-Se

ep 628 1,098 -471 Realty gaained by 1.4

45%, BSE CG surged by 1 1.15%. Top

Total Sept

l 6,112 7,832 -1720 Losers: BBSE FMCG d down by 1.448%, BSE O and gas

Oil

down by 1.43%.

2012 YTD

2 118463 128277 -9814

• Market bbreadth was positive at ~1.41x as investors

s t s

Global Markets bought large cap s stocks. On provisional basis, FII

bought equity of `1

e 15.96bn and domestic i

d institutions

Index

x Latest Values

t Change (%) sold equity of `11.56

6bn in cash s

segment.

DJIA 13

3,558.92 -0.15% • Asian sto

ocks droppe excluding Japanese m

ed markets, as

Nasd

daq 3,160.78

3 -0.60% renewed global grow concerns weigh on sh

d wth s hare prices

Nikke

ei 9,095.28

9 0.29%

for comm

modity and c

construction firms.

H Seng 20

0,673.59 -0.10% • We expe a flat ope

ect ening for the Indian mar

e rkets today

following the Asian markets and profit taking for the

g d

* as of 8.25AM IST

f

investors However, governmen

s. nt's reform measures

Curre

ency Snapsh

hot for powe sector ma help mar

er ay rkets to stan firm on

nd

the curre levels.

ent

Future contract RBI Economic a

and Corporate Developm

ments

Latest Previous

expir on

re Reference

R

Quote Close

26/09/12 Rate • Governmment cleared State ele

ectricity bo

oard (SEB)

India Rupee per $

an 53.38 53.48 53.29 restructu

uring packag

ge

India Rupee per €

an 69.15 69.08 68.95 • Companies bill may be put up for cabine nod by

y p et

India Rupee per £

an 86.60 86.64 86.44 October first week

India Rupee per ¥

an 68.51 68.50 68.28 • Inter ministerial gro

oup (IMG) h

has reviewed total 58

d

coal bloc that were sent showc

cks e cause notice

e

* NSE Exchange

Keyno Capitals Research

ote (research h@keynotecapitals.net) (+9122-3026 66000)

Keyno Capitals R

ote Research is also available on

Bloom

mberg KNTE <GO>, Thom mson One Ana alytics, Reute Knowledge, Capital IQ, TheMarkets.com and sec

ers , curities.com

Keynote Capi

K itals Institutio

onal Research - winner of “India’s Best IPO Analyst Award 2009” by MCX-Zee Business

h t ” e

To unsubscrib from this m

T be mailing list, p

please reply to unsubscribe@keynotecaapitals.net

2.

TOP GAINERS

G Buzzing Stocks

(BSE A-Group) • Governm

ment defers call on hiki

s ing sugar pr

rices

Previous Current Change

Company Name • Maruti t hike car p

to prices within a week

n

Close(`) Price(`) (%)

Lanco Infra 13.74 15.06 9.61% • Honda t raise prices of top selling mod

to dels Brio,

Ober Realty

roi 232.8 255.05 9.56% Jazz and City from O

d October 1

ADAN POWER

NI 46.9 50.6 7.89% • Adani P

Power pled

dges additio

onal 7 cror shares

re

Suzlo Energy

on 17.25 18.46 7.01% (3.25% stake)

Torre Power

ent 157.45 168.1 6.76% • Jindal S

Steel raises Rs 660 c

s crore bridge loan to

e

(BSE Mid-Cap)

E finance its CIC Ener

rgy Acquisit

tion

Previous Current Change • Oil India in talks w

a with Carrizo Oil & Gas to acquire

o

Company Name

Close(`) Price(`) (%) stake in Shale gas a

n assets

Lanco Infra 13.74 15.06 9.61%

• Tata Steeel ruled ou any plan to exit from Dhamra

ut m

ABG Shipyard 348.55 380.05 9.04% Port in O

Odisha

Suzlo Energy

on 17.25 18.46 7.01%

• Two bid

dders eye M

Mallya’s 30% stake in M

% Mangalore

INDIA POWER

AB 13.15 14.07 7.00%

Chemica and Fert

als tilisers

Greaves Cotton 68.8 73.4 6.69%

• Idea Cellular rules out further tariff hikes for now

TOP LOSERS

L • Alok Inddustries bo

oard to mee today to consider

et

(BSE A-Group) rights is

ssue

Previous Current Change • Officials from IRDA will meet FM to dis

s A t scuss tax

Company Name

Close(`) Price(`) (%) relief measures for the life insu

urance industry

Ruch Soya

hi 77.65 69.7 -10.24% • BPCL, Oman Oil JV t list IPO by next year

O to y

Apoll Tyres

lo 97.2 92.95 -4.37%

Exide Inds

e 148.95 142.85 -4.10%

Cadil Health

la 860.3 830 -3.52%

Bhar Elect

rat 1225.55 1185 -3.31%

(BSE Mid-Cap)

E

Previous Current Change

Company Name

Close(`) Price(`) (%)

Ruch Soya

hi 77.65 69.7 -10.24%

Elant Beck-$

tas 1475.4 1399.95 -5.11%

Gujarat StateFert 83.55 79.3 -5.09%

Tulip Telecom

p 54.15 51.45 -4.99%

Anan Raj Inds-$

nt 56.95 54.15 -4.92%

Keyno Capitals Research

ote (research

h@keynotecapitals.net) (+9122-3026

66000)

3.

India and Global Economic C

Calendar

Cou

untries / Tuesd

day Wednesday Thursda

ay Friday

Reg

gions 25/Se

ep 26/Sep 27/Sep

p 28/Sep

Fe

ederal Fiscal

India

De

eficit, INR (Au

ug)

Ex

xternal Debt (Q2)

FX Reserves, U

X USD

(Se 16)

ep

Co Personal

ore

S&P/Case-Sh hiller MBA Mortgag

M ge

Durable Goodds Coonsumption

US Home Price Indices Applications (Sep

A

Orders (Aug)

O Exxpenditure - Prices

(YoY) (Jul) 21)

2

Inddex (YoY) (Aug)

Gross Domesttic Chhicago Purchasing

Consumer New Home Sales

N

Pr

roduct Annualized Maanagers' Indeex

Confidence (Sep) (MoM) (Aug)

(Q

Q2) (Seep)

Richmond Feed

EIA

E Crude Oil Stocks nitial Jobless Claims

In

Manufacturing Index

change (Sep 21)

c (S

Sep 22)

(Sep)

Germany Gf fk

Ch

hina HSBC

Consumer Euro Consum Price

E mer EU Unemplo

UR oyment

Global Maanufacturing PMI

g

Confidence Survey Index (MoM) (Sep) Change (Sep)

(Se

ep)

(Oct)

China UBS Fra

ance Gross

Euro Retail S

E Sales EU M3 Mone

UR ey

Consumption Doomestic Prod

duct

(MoM) (Aug) Su

upply (3m) (

(Aug)

Indicator (Au

ug) (Yo (Q2)

oY)

Euro Wage Inflation Japan Foreign bond

n GBP Gross Do

omestic

(MoM) (Jul) investment (Sep 21) Pr

roduct (QoQ) (Q2)

ECB Presideent

Draghi's Speeech

KEYNOTE CAPITALS LTD.

E

The Ruby, 9th Floor, Senapati Ba

, S apat Marg, Dadar (W), M

D Mumbai – 40 028

00

Tel. : +912

22-30266000

0 • www.ke

eynotecapita

als.com

Disclaim

mer: This repo is purely for informatio purpose an is based on public infor

ort f on nd o rmation. News content is a attributable to

o

various media, unles specified ot

s ss therwise. All m

market related statistical da pertains to the immedia

d ata o ately preceding trading dayy,

unless stated otherw

wise. Neither the information nor any opin

nion expresse in this repo constitutes an offer, or a invitation to

ed ort an o

make an offer, to bu or sell the s

a uy securities menntioned herein We or any o our directors, officers or employees sh

n. of hall not in any

y

way be responsible for any loss a

e arising from th use of this report. Inves

he s stors are advi

ised to apply their own jud

dgment before e

acting o the conten of this repo The report has not been edited due t time constraints.

on nts ort. t n to