1. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

Consumer Discretionary

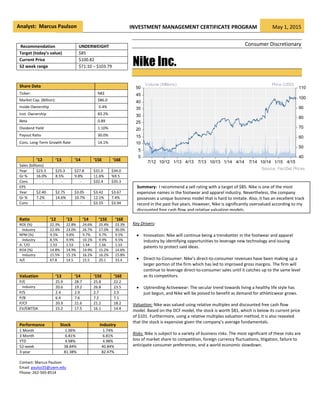

Nike Inc.

7/12 10/12 1/13 4/13 7/13 10/13 1/14 4/14 7/14 10/14 1/15 4/15

40

50

60

70

80

90

100

110

0

5

10

15

20

25

30

35

40

45

50

Source: FactSet Prices

Volume (Millions) Price (USD)

Key Drivers:

Innovation: Nike will continue being a trendsetter in the footwear and apparel

industry by identifying opportunities to leverage new technology and issuing

patents to protect said ideas.

Direct-to-Consumer: Nike’s direct-to-consumer revenues have been making up a

larger portion of the firm which has led to improved gross margins. The firm will

continue to leverage direct-to-consumer sales until it catches up to the same level

as its competitors.

Uptrending Activewear: The secular trend towards living a healthy life style has

just begun, and Nike will be poised to benefit as demand for athleticwear grows.

Valuation: Nike was valued using relative multiples and discounted free cash flow

model. Based on the DCF model, the stock is worth $81, which is below its current price

of $101. Furthermore, using a relative multiples valuation method, it is also revealed

that the stock is expensive given the company’s average fundamentals.

Risks: Nike is subject to a variety of business risks. The most significant of these risks are

loss of market share to competition, foreign currency fluctuations, litigation, failure to

anticipate consumer preferences, and a world economic slowdown.

Recommendation UNDERWEIGHT

Target (today’s value) $85

Current Price $100.82

52 week range $71.10 – $103.79

Share Data

Ticker: NKE

Market Cap. (Billion): $86.0

Inside Ownership 0.4%

Inst. Ownership 83.2%

Beta 0.89

Dividend Yield 1.10%

Payout Ratio 30.0%

Cons. Long-Term Growth Rate 14.1%

‘12 ‘13 ‘14 ‘15E ‘16E

Sales (billions)

Year $23.3 $25.3 $27.8 $31.0 $34.0

Gr % 16.0% 8.5% 9.8% 11.6% %9.5

Cons - - - $32.4 $35.3

EPS

Year $2.40 $2.75 $3.05 $3.42 $3.67

Gr % 7.2% 14.6% 10.7% 12.1% 7.4%

Cons - - - $3.55 $3.94

Ratio ‘12 ‘13 ‘14 ‘15E ‘16E

ROE (%) 22.3% 22.8% 24.6% 25.4% 23.3%

Industry 22.4% 23.0% 26.7% 27.0% 30.0%

NPM (%) 9.5% 9.8% 9.7% 9.7% 9.5%

Industry 8.5% 9.9% 10.1% 9.9% 9.5%

A. T/O 1.53 1.53 1.54 1.56 1.53

ROA (%) 14.8% 14.9% 14.9% 15.2% 14.6%

Industry 15.5% 15.1% 16.2% 16.2% 15.8%

A/E 67.8 14.5 15.5 20.1 33.4

Valuation ‘13 ‘14 ‘15E ‘16E

P/E 25.9 28.7 25.8 22.2

Industry 20.6 19.2 26.8 23.5

P/S 2.4 2.9 2.7 2.5

P/B 6.4 7.6 7.2 7.1

P/CF 20.9 21.6 21.2 18.2

EV/EBITDA 15.2 17.5 16.1 14.4

Performance Stock Industry

1 Month 1.06% 1.74%

3 Month 6.81% 6.81%

YTD 4.98% 4.98%

52-week 38.84% 40.84%

3-year 81.38% 82.47%

Contact: Marcus Paulson

Email: paulso35@uwm.edu

Phone: 262-565-8514

Analyst: Marcus Paulson

Summary: I recommend a sell rating with a target of $85. Nike is one of the most

expensive names in the footwear and apparel industry. Nevertheless, the company

possesses a unique business model that is hard to imitate. Also, it has an excellent track

record in the past five years. However, Nike is significantly overvalued according to my

discounted free cash flow and relative valuation models.

2. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

2

Company Overview

From its humble beginnings in 1964, Nike Incorporated (NKE) has transformed into the world’s leading athletic

footwear, apparel, and equipment company. The firm is involved in the design, development, manufacturing,

and worldwide marketing in eight different sports categories: running, basketball, soccer, mens training,

womens training, sportswear, action sports, and golf. Nike also has two wholly-owned subsidiary brands.

Converse manufacturers classic athletic and casualwear, and Hurley is world-renowned for its surfwear. The

majority of Nike’s revenue comes from United States and Western Europe, yet the firm operates worldwide and

conducts business in nearly every country. Nike’s co-founder Phil Knight still oversees the board of directors at

the firm’s headquarters in Beaverton, Oregon.

Nike generates revenue through normal retail operations and using direct-to-consumer transactions. Revenue is

derived from five product segments including:

Footwear: Nike was the creator of the first modern athletic shoe, so it’s no surprise that the firm’s

footwear segment is the bread-and-butter of the brand as it makes up 70% of total revenues.

Although Nike’s footwear merchandise is predominantly designed for athletic use, large portions are

worn for casual purposes as well.

Apparel: Like its footwear segment, Nike has established itself among the leading players in the global

sports apparel market. It is the official outfitter for many collegiate and professional sports

teams/leagues.

Equipment: Sports equipment is a fragmented sector that contains a large variety of products. As with

Footwear and Apparel, Nike attempts to revolutionize athletic equipment and focus on technical

superiority.

Converse: Converse, the once the essential sports brand of the 1960’s, was purchased by Nike in

2003. The vintage-style leisure wear are reported separately from the Nike Brand.

Global Brands Divisions: Nike assigns its operations into six geographic segments: North America,

Western Europe, Central & Eastern Europe, Greater China, Japan, and Emerging Markets. The Global

Brands Division accounts for any business outside these segments. Typically this compromises of

brand licensing revenue, and demand creation and operating overhead expenses.

Figures 1 and 2: Revenue Sources of Nike for year end 2014 (left) and Revenue History since 2010 (right)

Footwear

70.6%

Apparel

20.6%

Equipment

4.2%

Converse

4.3%

Global

Brands

0.3%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2010 2011 2012 2013 2014 2015E 2016E

(inmillions)

Footwear Apparel Equipment Converse

Source: Company Report Source: Company Report

3. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

3

2009 2010 2011 2012 2013 2014

125 211 277 337 579 466

Business Drivers

Though several factors may contribute to Nike’s future success; the following are the most

important business drivers:

1) Permanent Innovation

2) Direct to Consumer Development

3) Brand Strength

4) Uptrending Activewear

5) Opportunities in Undeveloped Markets

Permanent Innovation

In the athletic industry, technical innovation in the design and manufacturing process is essential to

commercial success. Not only do technological advancements allow firms to maintain prices, it also

keeps consumers loyal to a brand. Nike has always emphasized the importance of its research &

development department since its inception. The firm has its own sport research lab with scientists

to help design advanced products, while professional athletes engaged under sports market

contracts wear-test and evaluate said creations.

Quantifying Nike’s amount of innovation is challenging since it does not disclose R&D expenses. As

an alternative, it can be measured by analyzing the number of patents granted annually. A 2014

patent study by Macquarie showed that ROE of firms with large patent portfolios “improve(s)

substantially going forward despite short-term research spending impact.” Due to the recession, the

number of Nike’s patents granted fell in 2007 and 2008. Since then, NKE patent growth has

increased substantially, as shown in figure 3.

Figure 3: Amount of Nike Patents Granted Annually since 2009

Comparatively, the sheer number of patents Nike pumps out is astronomical. A MarketWatch study

that scoured the US Patent Office’s database from 1976-2014 showed that Nike was granted more

than 4,000 patents, which contrasted to 51 for Under Armor, 275 for Adidas, and 482 for Reebok.

These numbers represent how NKE has expressed the importance of creating and protecting

intellectual property since its inception. However, rivals are beginning to follow suit as technological

development is invading the sporting goods industry. The total number of patents granted per year

has increased continuously since 2005.

Source: United States Patent and Trademark Office

Digital

technology will

continue to drive

patent growth in

the sportswear

industry.

4. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

4

Figure 4: Breakdown of Nike’s Granted Patents from 2006 & 2014 (right)

Using market research to respond to consumer

preferences, Nike identifies opportunities to

leverage new technologies in existing categories.

Figure 4 (right) compares 2006, Nike’s peak year of

granted patents prior to the recession, to 2013.

Note that the number of footwear related patents,

while still around the same number, shrunk from

76% to half of the company’s patent portfolio. As

NKE diversified its business beyond footwear to

golf products and fitness tracking devices, its

patents granted showcased the change as well. I

believe Nike’s ability to spark consumer interest

through product innovations should continue going

forward. This was stated in the firm’s last annual

report in which it expressed plenty of untapped

potential involving digital initiatives with products

that provide real-time personalized feedback.

Direct to Consumer Development

Nike’s Direct to Consumer (DTC) business consists of sales through company-owned retail stores and

internet websites. It allows the firm to bypass wholesalers and sell its products directly to end users

at a higher margin. Figure 5 shows how closely correlated Nike’s DTC revenues are with its gross

margins with an R-squared of 85%. Therefore, the firm’s focus on the DTC segment is a vital

component of its strategy to achieve long-term earnings growth targets.

Figure 5: Quarterly Direct-to-Consumer Revenues and Gross Margin since 2012

Revenue growth from Nike’s DTC business has been outpacing growth in the wholesale business.

Figure 6 shows that DTC revenues have more than doubled in the past five years, and have been

making up a larger portion of Nike’s total sales. However, as of now DTC is but a small portion of

Nike’s overall business with a revenue contribution of only 19% in 2014. When contrasted to

comparable firms in Figure 7, Nike has been lagging behind DTC and gross margins indicating there is

further room for improvement in the DTC business. I believe that DTC growth will continue to

Source: Macquarie

Source: Company Report

Direct to

Consumer growth

will accelerate

margin growth.

5. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

5

outpace wholesale business and make up a larger portion of Nike’s overall sales, thus improving

profitability.

Figure 6 & 7: Annual DTC Revenue since 2010 (left) & Comparable Firm’s Annual DTC vs Gross Margin since 2010 (right)

Brand Strength

Through decades of sponsoring high-profile athletic celebrities, top sporting events, and professional

athletic leagues, the Nike swoosh has become one of the most recognizable logos in the world. Sales

have been driven by building a high perceived brand quality in the minds of consumers.

Nike refers to marketing expenses as “demand creation” which consists of advertising, promotional,

and endorsement contract expenses. Below, figure 8 shows how demand creation is closely linked to

total revenues with an R-squared of 78%.

Figure 8 & 9: Quarterly Demand Creation Expense since 2010 (left) & Demand Creation Expense as % of Revenues (right)

Even though the expense has been trending upward, Nike has been able to hold the line on demand

creation around 11% percent of revenue as shown in figure 9 (above). The problem is the

inconsistent nature of it all. When there’s a championship or major tournament, Nike tends to call

for a surge in marketing. On top of that, the firm tends to release products at said events to enhance

brand exposure, further increasing expenses. According to Nike reports, demand creation will likely

remain flat for the rest of 2015 due to no irregular sporting events. However, I expect that to change

in 2016 as the firm ramps up sponsorships for the Summer Olympics in Rio, thus drastically

increasing revenues.

0%

5%

10%

15%

20%

25%

0

1,000

2,000

3,000

4,000

5,000

6,000

2010 2011 2012 2013 2014

DTCRevenues(InMillions)

Nike DTC Revenues (left) % of DTC to Total Revenues (right)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Q1

2010

Q3

2010

Q1

2011

Q3

2011

Q1

2012

Q3

2012

Q1

2013

Q3

2013

Q1

2014

Q3

2014

Q1

2015

Q3

2015

% of Demand Creation to Total Revenues Average

Source: Company Report Source: Company Reports

Source: Company Report Source: Company Report

6. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

6

Uptrending Activewear

Retail has begun to target the activewear market as the concept of a healthy and active lifestyle has

gained significant traction among consumers. Statistics show that inactivity levels across the US have

been dropping (figure 10), especially among women (figure 11). This lifestyle movement presents an

opportunity to capitalize for the athleticwear industry as its customer base continues to increase.

Figure 10 & 11: Inactivity Levels of Total US Population (left) and US Females (right)

*Inactivity Levels determined by the 2008 Physical Activity Guidelines for Americans*

Additionally, activewear sales are picking up due to more and more consumers accepting sports-

inspired clothing as street wear. The mixing of fitness and casual wear has been universally

attributed to the push by many Americans toward a more active lifestyle. In a market where

performance once trumped all, fashion is beginning to emerge as a vital component to activewear.

The recent uptick in athletic-wear sales has brought forth a lot of competitive attention. Aside from

new players entering the market, some of the world’s largest fashion firms are also moving into

activewear. Top designers such as Calvin Klein, Stella McCartney, and Alexander Wang have rolled

out fitness clothing lines along with large nationwide retailers such as Gap, Victoria Secret and

Macy’s. Nike has tapped into the fashion aspect as well by teaming up with Givenchy’s Riccardo Tisci,

an Italian based luxury fashion designer.

Nike is poised to benefit from the snowballing activewear trend since it has a well-established

foothold in the athletic apparel & footwear market. Yet, it will also have to defend market share

from the onslaught of new players.

Geographic Expansion

Nike generates over 66% of its revenue from its developed geographies (North America and Western

Europe) as shown in Figure 12 (below). However, as those areas edge closer to saturation Nike has

expressed plans to aggressively pursue greener pastures in developing markets (Greater China,

Central & Eastern Europe, and Emerging Markets). The driving force behind that decision is due to

the growing middle class in those regions.

30%

40%

50%

60%

70%

80%

18-24 25-44 45-54 55-64 65-74 75+

2009 2010 2011 2012

30%

40%

50%

60%

70%

80%

18-44 45-54 55-64 65-74 75+

2009 2010 2011 2012

Source: Centers for Disease Control and Prevention Source: Centers for Disease Control and Prevention

The increase in

people exercising

greater for females

than males.

7. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

7

Figure 12 & 13: Nike’s 2014 Sales by Geographic Region and Historical Revenue Breakdown by Region since 2010

Looking into the future, population will be the next big asset to drive growth. Transitioning from

lower to middle class brings about a rise in purchasing power and therefore a change in

consumption patterns. A report by Reuters, figure 14, shows that the middle class will expand

tremendously over the next fifteen years, and Nike is aiming to use that leverage to kindle growth.

Figure 14: Global Population by Income (in billions)

*Middle Class determined by annual per capita expenditure between $3,650 and $36,500 effective with 2005 CPI data*

The projected geographical shift in middle class consumption represented by figures 15 and 16

shows that the opportunity for growth is more abundant in the Asia Pacific. Nike has already

identified targeting Greater China and Emerging Markets. As long as it is set up to capture the

market share in the growing middle class, Nike has a great chance to capitalize.

North America

47%

Central &

Eastern Europe

5%

Emerging

Markets 15%

Greater China

10%

Japan 3%

Western

Europe 19%

Global Brand

Divisions 1%

Source: Reuters; Rohde and the US Census Bureau

Source: Company Reports Source: Company Reports

8. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

8

Figure 15 & 16: Projected Middle Class Consumption for 2010 (left) and Projected 2020 (right)

Financial Analysis

I project 2015 segment sales to be exceptionally strong in the US, Western Europe, and China

whereas sales in undeveloped areas will lag due to the strengthening dollar. I don’t expect the trend

to last long however, as the divisions will revert back to the mean in 2016. Margins are anticipated

to increase as DTC business strengthens, and SG&A will become more costly as overhead rises.

Quantification of Drivers

I expect Nike’s EPS to rise from $3.05 to $3.42 in 2015. I believe that Nike will experience an increase

in sales through improving economic conditions and new innovative products. An estimated 11%

increase in revenues should boost the EPS in multiple categories: $0.26 in footwear, $0.08 in

apparel, and $0.04 in converse. Furthermore, increasing gross margins due to Nike improving its DTC

channel will grow EPS by an additional $0.10. Also, I estimate that the company’s SG&A will increase

by five basis points. I am attributing the increase in SG&A to the company’s higher operating

overhead expenses, reflecting the growth in DTC business and investments in infrastructure. As a

result, I believe that SG&A will grow 13.2% for 2015 which will adversely affect EPS by $0.12.

Figure 17: Quantification of 2015E EPS Drivers

North

America

Europe

Central and

South

America

Asia Pacific

Sub-Saharan

Africa

Middle East

and North

Africa

North

America

Europe

Central &

South

America

Asia Pacific

Sub-Saharan

Africa

Middle East

and North

Africa

$0.26 $0.08 ($0.00) $0.04 ($0.00) $0.10 $0.06

$3.42

($0.12)

$3.05

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

Source: The World Bank; Kharas and Gertz, 2010. Source: The World Bank; Kharas and Gertz, 2010.

Source: Company Reports, IMCP

2015 EPS

grew 12.1%

to $3.42

9. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

9

In 2016, I expect EPS to grow to $3.67 from $3.42 in 2015. I expect trends from the year before to

continue. Increased revenues will begin to slow and will only result in a total combined EPS impact of

$0.33. Meanwhile, an amplified DTC business will add another $0.10 while increased SG&A will

lower EPS by $0.12. Please note: I assumed a reasonable share buyback of $200 million.

Figure 18: Quantification of 2016E EPS Drivers

Comparison Estimates to Consensus

My revenue expectations are more conservative compared to the 29-analyst average on Factset, and

thus earnings estimates lag behind the consensus as well. However, my estimates on free cash flow

are more bullish than consensus.

Figure 19: Estimated Revenues, EPS, FCF versus Consensus

$0.19

$0.10 $0.01 $0.03 $0.00 $0.10 $0.01

$3.67

($0.15)

$3.42

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

2015 2016 2015 2016

Revenue 31,037$ 33,993$ 32,402$ 35,344$

EPS 3.42$ 3.67$ 3.55$ 3.94$

FCF 3,119$ 4,029$ 2,786$ 3,223$

Estimates Consensus

Source: Company Reports, IMCP

2016 EPS

grew 7.3% to

$3.67

Source: Factset, IMCP

10. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

10

Revenues

Since 2010, Nike has experienced a steady growth in its total revenue. In the base case, I expect

operating revenues to grow 11.6% and 9.5% for 2015 and 2016, respectively. The increase of 2015

growth is sensible due to the world cup driving sales in the 1

st

quarter. In 2016, I believe sales

development will taper back to 2013-2014 levels. Eventually, I predict Nike operating revenue to

continue to grow at 8% after 2016.

Figure 20: Nike’s Revenue versus YoY Revenue Growth, 2010-2016E

Figure 21: 2010-2016E Operating Revenues and Estimates

I expect Nike revenues to increase with new sportswear demand due to new innovative products,

and an increased consumer base due to uptrending fitness trends in the US and an increasing middle

class internationally. The firm’s footwear segment has been its anchor over the past five years never

dropping below 5.8% YoY growth. I expect Nike’s footwear sales to continue increasing over the next

few years. With the ever-increasing demand in activewear, I believe Nike’s high growth divisions in

the future will be Converse and Apparel. In 2014, they grew 16% and 8% respectively. While sales of

apparel and shoes have hummed along, Nike’s smaller sports equipment segment hasn’t performed

well. Granted the division only makes up 5% of revenues, I believe equipment revenues will lag due

to increased competition.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2010 2011 2012 2013 2014 2015E 2016E

(InMIllios)

Nike Annual Revenues (left) YoY Revenue Growth (right)

Items 2010 2011 2012 2013 2014 2015E 2016E

Sales 17,340 19,188 23,224 25,215 27,671 30,958 33,887

Growth 10.7% 21.0% 8.6% 9.7% 11.9% 9.5%

Footwear 10,301 11,519 13,513 14,635 16,208 18,477 20,140

Apparel 5,026 5,516 6,958 7,491 8,109 8,798 9,678

Equipment 1,030 1,022 1,429 1,640 1,670 1,662 1,745

Converse 983 1,131 1,324 1,449 1,684 2,021 2,324

Global Brand Divisions 86 96 111 115 125 121 127

Corporate 1,588 833 (4) (17) 3 (42) (21)

Source: Company Reports, IMCP

Source: Company Reports, IMCP

11. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

11

Operating Income and Margins

Figure 22 shows growth of operating margins for NKE from 2011 to 2016 estimates. Growth margins

have been increasing since 2012 due to DTC business lowering cost of goods sold. However, increase

costs to demand creation and SG&A have caused operating and net margins to remain steady over

the past few years. I project the YoY change in net margins will remain flat so long as the increase in

gross margin can offset the increase in operating expenses in 2015. I believe net margins in 2016 will

eventually decrease due to increased demand creation expenses for the summer Olympics in Rio.

Figure 22: Nike Operating Margins, 2010-2016E

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2011 2012 2013 2014 2015E 2016E

Gross Margin Operating Margin Net Margin

Source: Company Reports, IMCP

An increase in DTC

sales has improved

gross margins while

negatively impacting

net margins

temporarily.

12. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

12

Five Stage Du Pont ROE

Currently, Nike’s return on equity is at an all-time high. The improvement of the company’s ROE can

be attributed to a slight improvement in asset turnover and higher level of financial leverage. As I

mentioned earlier, the company issued $1 billion senior notes in April of 2013. The higher level of

leverage gave a huge boosts to the company’s ROE. In 2015, ROE may improve further as asset

turnovers, operating profit margin, and leverage all moderately rise. Figure 23 (below) illustrates

Nike’s calculation in detail.

Figure 23: DuPont ROE Calculation

The current footwear industry ROE is 22.4%, which is in line with its five-year average of 21.9%.

However, it should be noted that the industry ROE was above 26% at the end of 2014 and sharply

fell while Nike has continued trending up.

Free Cash Flow

Nike’s free cash flow for 2014 was $1,592 million which increased 8.2% from 2013. Although, in the

prior year Nike had a huge decrease in free cash flow of -29.1%. That is attributable to a large

increase in NWC and net fixed assets leading to a sharp increase in uses of cash. Going into the near

future, I expect Nike’s to have no problems growing FCFE. Without cash and debt, NKE would grow

FCFE 25.6% and 23.0% in 2015 and 2016. However, I anticipate the firm to use any extra cash to pay

down debt, increase its dividend, and continue to buy back shares. Even so, cash is projected to

increase $899 and $910 million in 2015 and 2016 respectively. Looking into the future, NKE’s NOPAT

will outpace NWC and NFA growth to allow free cash flow to increase to $1,849 in 2015 and $2,110

in 2016.

DuPont ROE Calculation

5-stage 2011 2012 2013 2014 2015E 2016E Average

EBIT/Sales 14.2% 12.9% 12.9% 12.9% 13.0% 12.7% 13.2%

Sales/Avg Assets 1.37 1.53 1.53 1.54 1.56 1.53 1.49

EBT/EBIT 99.9% 99.9% 100.1% 99.1% 99.2% 99.5% 99.7%

Net Income/EBT 75.9% 75.0% 75.3% 76.0% 75.6% 75.6% 75.5%

ROA 14.8% 14.8% 14.9% 14.9% 15.2% 14.6% 14.8%

Avg Assets/Avg Equity 1.50 1.51 1.54 1.65 1.67 1.60 1.55

ROE 22.2% 22.3% 22.8% 24.6% 25.4% 23.3% 23.0%

Source: Company Reports, IMCP

13. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

13

Figure 24: FCF Analysis (2010 – 2016E)

Valuation

Nike was valued using multiples relative to its industry, and a 3-stage discounting cash flow model.

Based on both the relative valuation and DCF model, NKE is overvalued, which differs significantly

from market expectations. The current price is $100 and I value the stock to be worth $85.

Free Cash Flow Analysis 2011 2012 2013 2014 2015E 2016E

Without cash and debt

NOPAT $2,175 $2,260 $2,449 $2,718 $3,039 $3,252

Growth 13.8% 3.9% 8.4% 11.0% 11.8% 7.0%

NWC* 5,384 5,646 6,331 6,449 7,013 7,474

Net fixed assets 3,701 3,620 3,915 4,898 5,351 5,666

Total net operating capital* $9,085 $9,266 $10,246 $11,347 $12,364 $13,139

Growth 13.9% 2.0% 10.6% 10.7% 9.0% 6.3%

- Change in NWC* 868 262 685 118 564 461

- Change in NFA 241 (81) 295 983 453 314

FCFF* $1,066 $2,079 $1,469 $1,617 $2,022 $2,477

Growth 95.0% -29.4% 10.1% 25.0% 22.5%

- After-tax interest expense 3 3 (2) 25 23 18

FCFE** $1,063 $2,076 $1,471 $1,592 $1,999 $2,460

Growth 95.3% -29.1% 8.2% 25.6% 23.0%

+ Net new debt/other cap (170) (48) 982 (11) (150) (350)

Sources of cash $893 $2,028 $2,453 $1,581 $1,849 $2,110

Uses of cash

Other expense 39 46 (21) - - -

Increase cash and mkt sec (1,124) 362 1,020 (1,117) 899 910

Dividends 555 619 703 799 900 1,050

Share buyback (503) (697) (543) (681) 50 150

Change in other equity 1,992 1,751 1,612 2,832 - (0)

$959 $2,081 $2,771 $1,833 $1,849 $2,110

Change in other liab 66 53 318 252 - -

Total $893 $2,028 $2,453 $1,581 $1,849 $2,110

FCFF per share $1.12 $2.26 $1.64 $1.83 $2.29 $2.81

Growth 101.6% -27.6% 11.8% 25.1% 22.7%

FCFE per share $1.12 $2.26 $1.64 $1.80 $2.26 $2.79

Growth 101.9% -27.4% 9.9% 25.6% 23.2%

Per Share Basis

Free Cash Flow Analysis 2011 2012 2013 2014 2015E 2016E

With cash and debt

NOPAT $2,175 $2,260 $2,449 $2,718 $3,039 $3,252

Growth 13.8% 3.9% 8.4% 11.0% 11.8% 7.0%

NOWC 7,339 7,963 9,668 8,669 10,132 11,502

Net fixed assets 3,701 3,620 3,915 4,898 5,351 5,666

Total net operating capital $11,040 $11,583 $13,583 $13,567 $15,483 $17,168

Growth -0.1% 4.9% 17.3% -0.1% 14.1% 10.9%

- Change in NOWC (256) 624 1,705 (999) 1,463 1,370

- Change in NFA 241 (81) 295 983 453 314

FCFF $2,190 $1,717 $449 $2,734 $1,123 $1,568

Growth -21.6% -73.9% 509.3% -58.9% 39.6%

- After-tax interest expense 3 3 (2) 25 23 18

+ Net new debt (170) (48) 982 (11) (150) (350)

FCFE $2,017 $1,666 $1,433 $2,698 $950 $1,200

Growth -17.4% -14.0% 88.3% -64.8% 26.3%

Sources of cash (FCFE) $2,017 $1,666 $1,433 $2,698 $950 $1,200

Uses of cash

Other expense $39 $46 ($21) $0 $0 $0

Increase mkt sec - - - - - -

Dividends 555 619 703 799 900 1,050

Share buyback (503) (697) (543) (681) 50 150

Change in other equity 1,992 1,751 1,612 2,832 - (0)

$2,083 $1,719 $1,751 $2,950 $950 $1,200

Change in other liab 66 53 318 252 - -

Total $2,017 $1,666 $1,433 $2,698 $950 $1,200

FCFF per share $2.30 $1.87 $0.50 $3.09 $1.27 $1.78

Growth -18.9% -73.2% 518.9% -58.9% 39.8%

FCFE per share $2.12 $1.81 $1.60 $3.05 $1.08 $1.36

Growth -14.6% -11.8% 91.2% -64.8% 26.5%

Per Share Basis

Source: Company Reports, IMCP Source: Company Reports, IMCP

14. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

14

Trading History

As figure 25 shows (below), Nike is trades at an average P/E (NTM) of 19.85. Recently NKE has been

following the consumer discretionary trend of being richlyvalued compared to its historical numbers.

NKE is currently trading at 25.87 P/E. Over the next 7 years, I would expect NKE’s P/E to normalize

back to 23x. I believe we are coming to a peak in another economic cycle, and that the majority of

securities in the market are overvalued at this moment in time.

Figure 25: P/E (NTM) trading history, 04/2010 - 04/2015

Assuming the firm maintains a 26 P/E at the end of 2015, it should trade at $88.92 by the end of the

year.

26 X 2016 EPS of $3.42 = $88.92

Discounting $88.92 back to today at a 9.60% cost of equity yields a price of $86.49.

Figure 26: Nike’s current and five year averages for P/E, P/S, and P/B

Figure 26 exhibits the fact that all of NKE multiples are trading higher than its 5 year averages.

Relative Valuation

Figure 27 (below) shows Nike vs its peers on a number of financial and valuation metrics. As

mentioned earlier, although the industry is fragmented, it is hard to find a direct comparable to NKE

because of its diversification in brands. Compared to its peers, Nike trades at a price to earnings

multiple slightly above the average (NTM P/E of 26.7 vs 23.5). This reflects expectations of high

growth (14.1 LTG vs 10.3 for the industry) as the company penetrates more markets and increases

its top line revenue by double digits.

0

5

10

15

20

25

30

Apr-10 Nov-10 Jun-11 Jan-12 Aug-12 Mar-13 Oct-13 May-14 Dec-14

Historical P/E-NTW Average P/E-NTW

Current

Five Year Average

Price/Earnings Price/Sales Price/Book

25.87

19.85

1.81

1.16 2.15

2.71

Source: FactSet

Source: Factset

NKE P/E has

historically traded

for a premium

relative to its

comparable

15. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

15

Figure 27: Comps Sheet

P/B vs ROE

Figure 28 (below) shows the relationship between P/B and ROE of the stocks in the footwear and

apparel industry. There is a strong relationship between price-to-book and return on equity, as

shown by the calculated R-squared that indicates 79% of the change in P/B can be explained through

NTM ROE. In comparison to its peers, Nike has the second highest P/B and the highest ROE, so it

appears to be fairly valued versus the broad spectrum of peers. Assuming the relationship holds

going forward, the fair value for NKE is $81.76 at the end of the year or about $79.54 now.

Estimated P/B = 2015 ROE (24.7%)* 24.031 – 0.3405 = 5.60

Target Price = Estimated P/B * 2015 BVPS ($14.60) = $81.76/share.

Figure 28 & 29: P/B vs ROE (left) and P/S vs Net Profit Margin (right) for footwear and apparel industry

Comp Sheet (5/1/2015)

Current Market Price Change Earnings Growth LT Debt/ S&P LTM Dividend

Ticker Name Price Value 1 day 1 Mo 3 Mo 6 Mo 52 Wk YTD LTG NTM 2014 2015E 2016E Pst 5yr Beta Equity Rating Yield Payout

NKE NIKE INC $100.95 $86,792 (0.2) 0.3 5.0 11.1 37.6 5.0 14.1 8.4% 19.5% 11.0% 16.2% 17.6% 0.53 8.7% A+ 1.04% 29.7%

ADS-DE ADIDAS AG $80.85 $16,520 1.6 4.6 22.9 28.9 (3.0) 29.1 4.8 17.4% -33.0% 14.6% 15.4% 13.5% 1.29 28.3% 2.04% 63.8%

SKX SKECHERS U S A INC $89.66 $4,664 3.2 23.3 56.2 77.9 124.5 62.3 33.2% 151.9% 50.0% 25.0% 18.6% 1.28 1.2% B 0.00% 0.0%

SHOO MADDEN STEVEN LTD $41.52 $2,641 8.3 9.4 23.5 38.7 18.1 30.4 13.4% -10.7% 9.1% 20.3% 16.8% 0.72 0.0% B 0.00% 0.0%

COLM COLUMBIA SPORTSWEAR CO $62.84 $4,423 1.2 5.1 47.8 74.8 55.0 41.1 10.4 13.4% 39.7% 15.8% 13.2% 14.5% 1.51 0.0% B+ 0.72% 22.7%

HBI HANESBRANDS INC $32.22 $12,914 (6.8) (5.6) 12.6 17.7 70.9 15.5 11.0 67.5% 43.9% 16.3% 14.0% 49.0% 1.08 140.7% 0.97% 31.9%

LULU LULULEMON ATHLETICA INC $66.94 $9,503 0.7 5.8 1.1 61.7 42.1 20.0 15.0 16.3% -1.0% 2.1% 20.2% 32.3% 1.03 3.2% B+ 0.00% 0.0%

DECK DECKERS OUTDOOR CORP $75.06 $2,595 (0.7) 2.2 (4.2) (8.0) (4.4) (17.6) 12.3 10.0% 11.5% 13.8% 17.4% 1.03 3.2% B+ 0.00% 0.0%

VFC VF CORP $73.70 $31,358 (0.3) (2.2) 3.6 10.8 22.6 (1.6) 10.8 35.0% 12.8% 4.2% 15.3% 18.3% 1.06 25.3% A 1.55% 48.9%

WWW WOLVERINE WORLD WIDE $34.33 $3,539 3.1 7.0 21.9 29.6 27.7 16.5 19.6% 13.3% -3.7% 12.8% 16.0% 0.95 91.5% A- 0.72% 18.5%

7936-JP ASICS CORP $25.97 $4,929 (0.3) (6.2) 8.8 28.3 53.9 6.7 3.9 21.0% 1.0% 26.3% 4.8% 0.65 0.72% 27.7%

Average 0.9 4.0 18.1 33.8 40.4 18.9 10.3 24.9% 24.3% 12.0% 17.5% 19.9% 1.01 30.2% 0.70% 22.1%

Median 0.7 4.6 12.6 28.9 37.6 16.5 10.9 17.4% 13.3% 11.0% 15.4% 17.4% 1.03 6.0% 0.72% 22.7%

SPX S&P 500 INDEX $2,118 0.2 1.3 3.2 7.8 12.7 2.9 8.7% 3.2% 7.6%

2014 P/E 2014 2014 EV/ P/CF P/CF Sales Growth Book

Ticker Website ROE P/B 2013 2014 2015E TTM NTM 2016E NPM P/S OM ROIC EBIT Current 5-yr NTM STM Pst 5yr Equity

NKE http://www.nike.com 24.7% 7.02 34.0 28.4 25.6 28.9 26.7 22.0 10.0% 2.85 13.6% 22.1% 22.7 4.2% 9.5% 7.8% $14.38

ADS-DE http://www.adidas-group.com 12.5% 2.74 14.7 21.9 19.1 25.9 22.1 16.6 4.3% 0.94 5.7% 8.3% 14.4 16.4 14.1 -11.5% 4.7% 7.0% $29.56

SKX http://www.skechers.com 12.8% 4.23 83.0 33.0 22.0 27.9 21.0 17.6 6.0% 1.96 9.3% 13.0% 13.5 17.7% 10.6% $21.18

SHOO http://www.stevemadden.com 16.7% 3.95 21.1 23.6 21.6 23.6 20.8 18.0 8.4% 1.98 11.5% 16.6% 12.4 17.8 13.1 10.0% 21.5% $10.52

COLM http://www.columbia.com 9.9% 3.27 46.2 33.1 28.6 32.4 28.6 25.2 6.4% 2.11 9.2% 10.5% 14.2 22.7 14.7 8.6% 8.3% 11.0% $19.24

HBI http://www.hanesbrands.com 40.8% 9.31 32.9 22.9 19.6 31.6 18.9 17.2 10.6% 2.43 13.5% 14.2% 17.1 23.7 12.7 10.1% 2.6% 6.5% $3.46

LULU http://www.lululemon.com 24.6% 8.72 35.0 35.4 34.7 40.3 34.7 28.9 14.9% 5.29 20.6% 21.9% 24.1 12.0% 14.1% 31.7% $7.68

DECK http://www.deckers.com 15.4% 2.51 18.0 16.3 14.6 18.4 15.2 12.9 8.8% 1.44 17.4% 13.2 13.4 12.2 17.7% $29.89

VFC http://www.vfc.com 23.7% 5.67 27.0 23.9 23.0 31.0 22.9 19.9 10.7% 2.55 15.1% 14.4% 17.7 18.7 15.0 3.1% 7.9% 11.2% $13.01

WWW http://www.wolverineworldwide.com 17.7% 3.75 24.0 21.2 22.0 26.4 22.1 19.5 6.0% 1.28 9.8% 7.0% 13.2 15.1 13.7 3.4% 5.2% 20.2% $9.17

7936-JP http://www.asics.co.jp 14.1% 3.73 32.1 26.5 26.2 36.4 25.2 20.8 5.9% 1.57 7.2% 8.6% 15.1 36.6 14.4 6.4% $6.96

Average 19.3% 4.99 33.4 26.0 23.4 29.4 23.5 19.9 8.4% 2.22 11.5% 14.0% 16.1 20.5 13.7 6.4% 7.5% 13.8%

Median 16.7% 3.95 32.1 23.9 22.0 28.9 22.1 19.5 8.4% 1.98 10.7% 14.2% 14.4 18.2 13.9 8.6% 7.9% 11.0%

spx S&P 500 INDEX 19.5 17.9 17.3 16.1

Nike

y = 24.031x + 0.3405

R² = 0.7869

0

2

4

6

8

10

12

0% 10% 20% 30% 40% 50%

P/B

ROE

P/B vs ROE

Nike

y = 33.833x - 0.6132

R² = 0.79

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0.0% 5.0% 10.0% 15.0% 20.0%

P/S

NPM

P/S vs NPM

Source: Factset

Source: Factset Source: Factset

16. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

16

P/S vs NPM

Figure 29 (above) shows the relationship between P/S and NPM of the stocks in the footwear and

apparel industry. There is a strong relationship between price-to-sales and net profit margin, as

shown by the calculated R-squared that indicates 79% of the change in P/S can be explained through

NPM. In comparison to its peers, Nike has the second highest P/S and third highest NPM, so it

appears to be fairly valued versus the broad spectrum of peers. Assuming the relationship holds

going forward, the fair value for NKE is $94.04 at the end of the year or about $91.49 now.

Estimated P/S = Estimated 2015 NPM (9.72%)* 33.833 – 0.6132 = 2.76

Target Price = Estimated P/S * 2015 SPS ($35.15) = $94.04/share.

Composite Ranking

As final comparison, I created a composite ranking of several valuation and fundamental metrics.

The analysis is shown below. Each metric was standardized to a percentile (100% reflects best

fundamentals or more expensive) before determining the composite score. A 50% weight composite

of 2014 ROE and NPM was compared to a 100% weight of P/B.

Figure 30: Composite Relative Valuation

Based on this analysis, NKE should trade a valuation of 63% of the maximum; however, it is at 75%.

This indicates it is overvalued.

Weight

Ticker Name

NKE NIKE INC

ADS-DE ADIDAS AG

SKX SKECHERS U S A INC

SHOO MADDEN STEVEN LTD

COLM COLUMBIA SPORTSWEAR CO

HBI HANESBRANDS INC

LULU LULULEMON ATHLETICA INC

DECK DECKERS OUTDOOR CORP

VFC VF CORP

WWW WOLVERINE WORLD WIDE

7936-JP ASICS CORP

50.0% 50.0% 100.0%

2014 2014

ROE NPM P/B Fund Value Diff

61% 67% 75% 64% 75% -12%

31% 29% 29% 30% 29% -16%

32% 40% 45% 36% 45% -23%

41% 56% 42% 49% 42% -1%

24% 43% 35% 33% 35% -16%

100% 71% 100% 86% 100% -5%

60% 100% 94% 80% 94% -7%

38% 59% 27% 48% 27% 14%

58% 71% 61% 65% 61% 4%

43% 41% 40% 42% 40% -9%

35% 40% 40% 37% 40% -16%

Fundamental

Percent of

Max

Valuation

Percent of

Max

Weighted Target

Value

63%

14%

22%

41%

19%

95%

87%

41%

65%

32%

25%

Source: Factset, IMCP

17. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

17

Figure 31: Composite Relative Valuation

Discounted Cash Flow Analysis

A three stage discounted cash flow model was also used to value Nike.

For the purpose of this analysis, the company’s cost of equity was calculated to be 9.60% using the

Capital Asset Pricing Model. The underlying assumptions used in calculating this rate are as follows:

The risk free rate, as represented by the ten year Treasury bond yield, is 1.92%.

A five year adjusted Beta of 0.95 was utilized since the company has similar risk as the market.

A long term market rate of return of 10% was assumed, since historically, the market has

generated an annual return of about 10%.

Given the above assumptions, the cost of equity is 9.60% (1.92 + 0.95 (10.0 – 1.92)).

Stage One - The model’s first stage simply discounts fiscal years 2015 and 2016 free cash flow to

equity (FCFE). These per share cash flows are forecasted to be $2.26 and $2.79, respectively.

Discounting these cash flows, using the cost of equity calculated above, results in a value of $2.07

and $2.32 per share in 2015 and 2016 respectively. Thus, stage one of this discounted cash flow

analysis contributes $4.39 to value.

Stage Two - Stage two of the model focuses on fiscal years 2017 to 2021. During this period, FCFE is

assumed to begin growing at an annual rate of 9% and then falls to 8%. The resulting cash flows are

then discounted using the company’s 9.60% cost of equity.

Figure 32: FCFE and Discounted FCFE for

When added together, these discounted cash flows total $14.53.

Stage Three – For the terminal value of the company, you may recall, fiscal year 2015 and 2016

earnings per share are forecasted to be $3.42 and $3.67, respectively. It was then assumed that

earnings per share would grow, from these forecasted numbers, at an annual rate of 9% for 2017,

and 8

th

for the next four years (figure 33).

Nike

R² = 0.8577

y = 1.2291x - 0.1003

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0.0 0.2 0.4 0.6 0.8 1.0

Valuation

Fundamental

2015 2016 2017 2018 2019 2020 2021

FCFF/share $2.26 $2.79 $2.81 $3.03 $3.27 $3.54 $3.82

Discounted FFCF $2.07 $2.32 $2.13 $2.10 $2.07 $2.04 $2.01

Source: IMCP

18. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

18

Figure 33: EPS estimates for 2012-2018

Stage three of the model also requires an assumption regarding the company’s terminal price-to-

earnings ratio. For the purpose of this analysis, it is assumed that as the company grows larger and

matures, its price-to-earnings ratio will converge near to the historical average of the S&P 500.

Therefore, a price-to-earnings ratio of 23 is assumed at the end of Nike’s terminal year. While this

may be high at the end of 2021, one must also consider what the market will price in today. A lower

multiple may be better to calculate fair value, but the stock will likely trade above as this value since

the market will be slow to price in NKE’s slowing growth.

Given the assumed terminal earnings per share of $5.44 and a price to earnings ratio of 23, a

terminal value of $125.16 per share is calculated. Using the 9.60% cost of equity, this number can be

discounted to a present value of $65.91.

Total Present Value – Given the above assumptions and utilizing a three stage discounted cash flow

model, an intrinsic value of $80.65 per share is calculated ($4.39 + $10.14 + $65.91). Given Nike’s

current price of $100, this model indicates that the stock is significantly overvalued.

Figure 34: 3-stage DCF model

2015 2016 2017 2018 2019 2020 2021

Earnings/share $3.42 $3.67 $4.00 $4.32 $4.67 $5.04 $5.44

3 Stage DCF P/E Terminal Value Model

Cost of equity FCFE1 (better def) $2.26 2015 Terminal year P/S

Risk free rate 1.92% FCFE2 (better def) $2.79 2016 2021 2.87

Beta 0.95 Terminal year P/B

Market return 10.0% EPS1 $3.42 2015 2021 7.03

Market risk premium 8.1% EPS2 $3.67 2016 Terminal year P/E

Stock risk premium 7.7% 2021 23.00

r = rf+ stock RP 9.60%

2nd Stage Growth (option to enter 1 rate for years 3-7) 8.0%

Source: IMCP

19. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

19

First Stage Second Stage

Cash flows 2015 2016 2017 2018 2019 2020 2021

Sales $31,037 $33,993 $37,052 $40,017 $43,218 $46,675 $50,410

Growth 9.5% 9.0% 8.0% 8.0% 8.0% 8.0%

NOPAT $3,039 $3,252 $3,545 $3,829 $4,135 $4,466 $4,823

% of sales 9.8% 9.6% 9.6% 9.6% 9.6% 9.6% 9.6%

- Change in NWC 564 461 598 646 697 753 813

NWC EOY 7013 7474 8071 8717 9415 10168 10981

Growth NWC 6.6% 8.0% 8.0% 8.0% 8.0% 8.0%

NWC / S (EOY) 22.6% 22.0% 21.8% 21.8% 21.8% 21.8% 21.8%

- Chg NFA 453 314 453 490 529 571 617

NFA EOY 5,351 5,666 6,119 6,608 7,137 7,708 8,325

Growth NFA 5.9% 8.0% 8.0% 8.0% 8.0% 8.0%

S / NFA (EOY) 5.80 6.00 6.06 6.06 6.06 6.06 6.06

Total inv in op cap 1017 775 1051 1135 1226 1324 1430

Total net op cap 12364 13139 14190 15325 16552 17876 19306

S / IC (EOY) 2.51 2.59 2.61 2.61 2.61 2.61 2.61

ROIC (EOY) 24.6% 24.8% 25.0% 25.0% 25.0% 25.0% 25.0%

FCFF $2,022 $2,477 $2,494 $2,694 $2,909 $3,142 $3,393

% of sales 6.5% 7.3% 6.7% 6.7% 6.7% 6.7% 6.7%

Growth 22.5% 0.7% 8.0% 8.0% 8.0% 8.0%

- Interest (1-tax rate) 23 18 19 21 22 24 26

Growth -22.2% 8.0% 8.0% 8.0% 8.0% 8.0%

FCFE $1,999 $2,460 $2,475 $2,673 $2,887 $3,117 $3,367

% of sales 6.4% 7.2% 6.7% 6.7% 6.7% 6.7% 6.7%

Growth 23.0% 0.6% 8.0% 8.0% 8.0% 8.0%

/ No Shares 882.9 881.5 881.5 881.5 881.5 881.5 881.5

Growth -0.2% 0.0% 0.0% 0.0% 0.0% 0.0%

FCFE $2.26 $2.79 $2.81 $3.03 $3.27 $3.54 $3.82

Growth 23.2% 0.6% 8.0% 8.0% 8.0% 8.0%

* Discount factor 0.91 0.83 0.76 0.69 0.63 0.58 0.53

Discounted FCFE $2.07 $2.32 $2.13 $2.10 $2.07 $2.04 $2.01

Third Stage

Terminal value P/E

Net income $3,016 $3,235 $3,526 $3,808 $4,113 $4,442 $4,797

EPS $3.42 $3.67 $4.00 $4.32 $4.67 $5.04 $5.44

Growth 7.4% 9.0% 8.0% 8.0% 8.0% 8.0%

Terminal P/E 23.00

* Terminal EPS $5.44

Terminal value $125.16

* Discount factor 0.53

Discounted terminal value $65.91

Summary

First stage $4.39 Present value of first 2 year cash flow

Second stage $10.36 Present value of year 3-7 cash flow

Third stage $65.91 Present value of terminal value P/E

Value (P/E) $80.65 = value at beg of fiscal yr 2015

Source: IMCP

20. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

20

Market Expectations

The current market price of $100.82 is vastly different from the $80.65 determined from the 3-stage

DCF model previously created. In order to determine the differences between my expectations and

the market, a sensitivity table was created below.

Figure 35: Sensitivity Table

To achieve the $100 market price, the terminal P/E and growth rate are expected to be 25 and 14%

respectively, represented by the bold $101.16. When looking at consensus data from Factset, the

long term growth rate is 14.1% and 2015E P/E is 25. Notice that the both the consensus and

sensitivity table data are nearly the exact same.

Bull/Bear Case

Nike’s future sales could improve or decline. However, if everything went right for the company for

the next two years, I believe that the firm will see a sales growth of 12% and 10% in 2015 and 2016

respectively. Also, in the bull case, gross margin should settle at 10.5% for both 2015 and 2016. If the

bull case were to materialize, I estimate the company’s EPS to reach $3.48 in 2015 and $3.76 in

2016.

On the other hand, if Nike does not fare well in the next two years, I expect the sales to grow at 11%

and 6.5% for 2015 and 2016 respectively. Also, the gross margin should decline and settle in at 6.5%

for the next two years. If the bear case were to materialize, I estimate the company’s EPS to be

$3.13 in 2014 and $3.07 in 2015.

$80.65 2% 4% 6% 8% 10% 12% 14%

19 59.96$ 62.89$ 65.96$ 69.19$ 72.57$ 76.12$ 79.83$

20 62.24$ 65.35$ 68.62$ 72.06$ 75.66$ 79.43$ 83.38$

21 64.53$ 67.82$ 71.28$ 74.92$ 78.74$ 82.74$ 86.94$

22 66.81$ 70.28$ 73.94$ 77.79$ 81.82$ 86.06$ 90.49$

23 69.09$ 72.75$ 76.60$ 80.65$ 84.91$ 89.37$ 94.05$

24 71.37$ 75.21$ 79.26$ 83.52$ 87.99$ 92.68$ 97.61$

25 73.65$ 77.68$ 81.92$ 86.38$ 91.07$ 96.00$ 101.16$

26 75.93$ 80.14$ 84.58$ 89.25$ 94.16$ 99.31$ 104.72$

27 78.21$ 82.61$ 87.24$ 92.11$ 97.24$ 102.62$ 108.28$

Terminal Growth Rate

TerminalP/E

2015E 2016E

Base 3.42 3.67

Consensus 3.55 3.94

Bull 3.48 3.76

Bear 3.13 3.07

EPS Projection

21. INVESTMENT MANAGEMENT CERTIFICATE PROGRAM May 1, 2015

21

Business Risks

Nike is subject to a variety of business risks. The most significant risks are described below.

(Source: Company 10k)

Exposure to currency fluctuations

The majority of Nike’s products are manufactured and sold outside of the US, resulting in

transactions with various currencies. Increased exposure to currency fluctuation could result in

lower revenues and higher costs which would further lead to decreased margins and earnings.

Competitive marketplace

The footwear, apparel, and equipment industry is highly competitive on a global basis. Nike faces

intense competition for both sales and independent manufactures that produce products. It is vital

for Nike to timely anticipate and respond to competitors in order to remain intact.

Continue recruiting high quality endorsers

Nike develops sentiment with consumers through its relationships with professional athletes, sports

teams and leagues. If certain endorsers were to stop using Nike products, or perform actions that

would harm its reputation, it could seriously harm Nikes brand image with consumers. Furthermore,

failure to identify and sign promising athletes could adversely affect the firm.

Unable to anticipate consumer preferences

Consumer preferences could shift rapidly to different types of performance products. The future

success of Nike depends on its ability to anticipate and respond to those consumer demands. If not,

Nike could experience lower sales, excess inventories, or lower profit margins.

Protecting and enforcing intellectual property

Protecting the Nike brand requires the firm to protect its patents by preventing imitation products.

Nike may also be subjected to liability if it infringes on other firm’s intellectual property.

Infringement claims could be expensive and time consuming, and may result in significant damages

or decreased sales of certain products. Also, the laws of some countries may not protect or allow

enforcement of intellectual property rights to the extent of the US. Foreign affairs can cause

considerable expenses and still not be successful.

Direct to Consumer operations

Nike’s high profile DTC venues have required capital expenditures that require substantially more

investment than other stores. The firm is now associated with many factors of risk that are

associated with brick-and-mortar stores due to the high fixed cost structure.