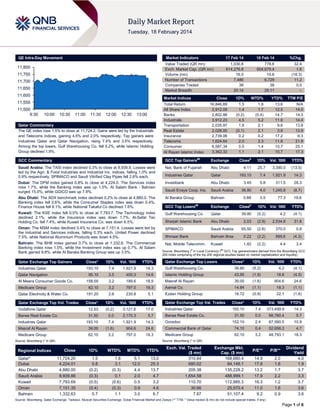

1. QE Intra-Day Movement

Market Indicators

11,800

11,750

11,700

11,650

11,600

16 Feb 14

%Chg.

1,030.8

614,276.8

16.0

7,486

38

20:14

778.6

604,679.4

19.6

6,729

38

25:11

32.4

1.6

(18.3)

11.2

0.0

–

Market Indices

11,550

11,500

9:30

17 Feb 14

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 1.5% to close at 11,724.2. Gains were led by the Industrials

and Telecoms indices, gaining 4.5% and 2.0% respectively. Top gainers were

Industries Qatar and Qatar Navigation, rising 7.4% and 3.5% respectively.

Among the top losers, Gulf Warehousing Co. fell 5.2%, while Islamic Holding

Group declined 1.9%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

16,846.89

2,912.09

2,802.86

3,912.23

2,035.97

2,028.00

2,739.06

1,624.64

6,587.34

3,362.32

1.5

1.4

(0.2)

4.5

1.8

(0.1)

0.2

2.0

0.5

1.1

1.8

1.7

(0.4)

5.2

2.1

2.1

0.2

2.3

1.4

2.1

13.6

12.5

14.7

11.8

9.6

3.8

17.2

11.8

10.7

10.7

N/A

14.0

14.3

14.4

13.8

13.9

6.3

21.9

25.1

17.3

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Vol. ‘000

Saudi Arabia: The TASI index declined 0.3% to close at 8,939.9. Losses were

led by the Agri. & Food Industries and Industrial Inv. indices, falling 1.0% and

0.9% respectively. SPIMACO and Saudi Vitrified Clay Pipes fell 2.6% each.

Nat. Bank of Fujairah

Abu Dhabi

4.11

25.7

3,390.0

(13.5)

Industries Qatar

Qatar

193.10

7.4

1,921.9

14.3

Dubai: The DFM index gained 0.8% to close at 4,224.0. The Services index

rose 1.7%, while the Banking index was up 1.5%. Al Salam Bank - Bahrain

surged 15.0%, while GGICO was up 7.9%.

Investbank

Abu Dhabi

Saudi Enaya Coop. Ins.

Saudi Arabia

Abu Dhabi: The ADX benchmark index declined 0.2% to close at 4,880.0. The

Banking index fell 0.6%, while the Consumer Staples index was down 0.4%.

Finance House fell 8.1%, while National Takaful Co declined 7.6%.

Al Baraka Group

Bahrain

GCC Top Losers

Exchange

Kuwait: The KSE index fell 0.5% to close at 7,793.7. The Technology index

declined 2.1%, while the Insurance index was down 1.7%. Al-Safat Tec

Holding Co. fell 7.4%, while Kuwait Insurance Co. was down 6.5%.

Gulf Warehousing Co

Qatar

Sharjah Islamic Bank

Abu Dhabi

Oman: The MSM index declined 0.4% to close at 7,151.4. Losses were led by

the Industrial and Services indices, falling 0.3% each. United Power declined

7.5%, while National Aluminium Products was down 4.5%.

SPIMACO

Ithmaar Bank

Nat. Mobile Telecomm.

Bahrain: The BHB index gained 0.7% to close at 1,332.6. The Commercial

Banking index rose 1.0%, while the Investment index was up 0.7%. Al Salam

Bank gained 9.8%, while Al Baraka Banking Group was up 3.5%.

##

YTD%

3.45

5.8

311.5

28.3

36.80

4.0

1,245.8

(8.7)

0.89

3.5

77.3

19.6

#

Close

1D% Vol. ‘000

YTD%

39.80

(5.2)

4.2

(4.1)

2.03

(2.9)

2,534.6

31.8

Saudi Arabia

65.50

(2.6)

370.0

0.8

Bahrain Brse

0.22

(2.2)

899.6

(4.3)

Kuwait

1.82

(2.2)

4.4

3.4

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Gainers

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Vol. ‘000

YTD%

Industries Qatar

193.10

7.4

1,921.9

14.3

Gulf Warehousing Co.

39.80

(5.2)

4.2

(4.1)

43.95

(1.9)

18.6

(4.5)

Qatar Exchange Top Losers

95.10

3.5

400.3

14.6

Islamic Holding Group

158.00

3.2

189.6

18.5

Masraf Al Rayan

39.00

(1.6)

904.6

24.6

62.10

3.2

797.0

18.3

Aamal Co.

14.84

(1.1)

18.3

(1.1)

Qatar Electricity & Water Co.

191.20

2.6

230.8

5.1

Ezdan Holding Group

16.72

(0.9)

22.1

(1.6)

Qatar Exchange Top Vol. Trades

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

Industries Qatar

193.10

7.4

373,499.9

14.3

31.50

0.0

68,760.4

5.7

152.10

2.4

67,590.5

10.9

Qatar Navigation

Al Meera Consumer Goods Co.

Medicare Group

Close*

1D%

Vol. ‘000

YTD%

Vodafone Qatar

12.53

(0.2)

3,121.6

17.0

Barwa Real Estate Co.

31.50

0.0

2,170.3

5.7

Industries Qatar

193.10

7.4

1,921.9

14.3

Ooredoo

Masraf Al Rayan

39.00

(1.6)

904.6

24.6

Commercial Bank of Qatar

74.10

0.4

52,656.3

4.7

Medicare Group

62.10

3.2

797.0

18.3

Medicare Group

62.10

3.2

48,793.1

18.3

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Barwa Real Estate Co.

Close

1D%

WTD%

MTD%

YTD%

11,724.20

4,224.01

4,880.00

8,939.88

7,793.69

7,151.35

1,332.63

1.5

0.8

(0.2)

(0.3)

(0.5)

(0.4)

0.7

1.8

3.1

(0.3)

0.1

(0.6)

(0.3)

1.1

5.1

12.0

4.4

2.0

0.5

0.9

3.0

13.0

25.3

13.7

4.7

3.2

4.6

6.7

Exch. Val. Traded

($ mn)

310.64

680.02

205.38

1,654.58

110.70

30.66

7.87

Exchange Mkt.

Cap. ($ mn)

168,680.4

84,148.1

135,228.2

488,999.1

112,885.3

25,570.4

51,107.4

P/E**

P/B**

14.9

17.8

13.2

17.9

16.3

11.0

9.2

2.0

1.6

1.7

2.2

1.2

1.6

0.9

Dividend

Yield

4.0

1.9

3.7

3.3

3.7

3.6

3.6

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index rose 1.5% to close at 11,724.2. The Industrials

and Telecoms indices led the gains. The index declined on the

back of selling pressure from non-Qatari shareholders despite

buying support from Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

70.78%

70.17%

6,206,505.02

Non-Qatari

Industries Qatar and Qatar Navigation were the top gainers,

rising 7.4% and 3.5% respectively. Among the top losers, Gulf

Warehousing Co. fell 5.2%, while Islamic Holding Group declined

1.9%.

Buy %*

29.22%

29.82%

(6,206,505.02)

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Monday fell by 18.3% to 16.0mn

from 19.6mn on Sunday. However, as compared to the 30-day

moving average of 12.1mn, volume for the day was 32.2%

higher. Vodafone Qatar and Barwa Real Estate Co. were the

most active stocks, contributing 19.5% and 13.6% to the total

volume respectively.

Ratings, Earnings and Global Economic Data

Ratings Updates

Company

Agency

Market

Emaar Properties

(Emaar)

Moody's

Dubai

Type*

Old Rating

Rating Change

Outlook

Outlook Change

Ba3/Ba3

CFR/PDR

New Rating

Ba1/Ba1

–

Stable

–

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency, CFR – Corporate Family Rating, PDR – Probability of Default Rating)

Earnings Releases

Company

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

–

–

94.3

-29.2%

113.9

-18.2%

–

–

50.9

8.9%

34.0

20.9%

465.7

17.1%

–

–

92.2

-17.1%

10328.0

25.3%

–

–

2568.0

21.2%

48.2

160.3%

–

–

-17.4

9.6%

AED

3183.8

12.4%

–

–

420.7

0.3%

Bahrain

BHD

30.4

-9.1%

–

–

8.3

200.1%

Bahrain

BHD

8.8

3.0%

11.2

-3.5%

2.9

856.5%

Market

National Gas &

Industrialization Co. *

RAK Insurance *

Gulf Medical Project Co.

(GMPC) *

Emaar Properties *

Takaful Emarat – Insurance

*

Air Arabia *

United Gulf Investment

Corporation (UGIC) *

Seef Properties *

Currency

Saudi Arabia

SR

UAE

AED

UAE

AED

Dubai

AED

Dubai

AED

Dubai

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

02/17

UK

Rightmove

Rightmove House Prices MoM

February

3.30%

–

1.00%

02/17

UK

Rightmove

Rightmove House Prices YoY

February

6.90%

–

6.30%

02/17

Japan

ESRI

GDP SA QoQ

4Q2013

0.30%

0.70%

0.30%

02/17

Japan

ESRI

GDP Annualized SA QoQ

4Q2013

1.00%

2.80%

1.10%

02/17

Japan

ESRI

GDP Nominal SA QoQ

4Q2013

0.40%

0.80%

0.20%

02/17

Japan

ESRI

GDP Deflator YoY

4Q2013

-0.40%

-0.20%

-0.40%

02/17

Japan

ESRI

GDP Consumer Spending QoQ

4Q2013

0.50%

0.80%

0.20%

02/17

Japan

ESRI

GDP Business Spending QoQ

4Q2013

1.30%

1.80%

0.20%

02/17

Japan

METI

Industrial Production MoM

December

0.90%

–

-0.10%

02/17

Japan

METI

Industrial Production YoY

December

7.10%

–

4.80%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

MDPS: Qatar's CPI at lowest level since August 2012 –

According to the Ministry of Development Planning & Statistics

(MDPS), Qatar's Consumer Price Index (CPI) for January 2014

rose up by only 2.3% year-on-year, the lowest level since

August 2012. On a month-on-month based, it rose 0.3% as

compared to December 2013. Food prices were the key factor

behind the slowdown falling 0.7% month-on-month (1.6% year-

on-year, which is the slowest rate of increase since August

2010). Housing and rents (the largest weight of overall inflation

with a 32.2% share) rose 1.0% month-on-month but were steady

at 2.8% year-on-year in January 2014. (Peninsula Qatar, QNB

Group)

IQCD plans QR5.4bn capital expenditure over five years –

Industries Qatar’s (IQCD) five-year business plan envisages

accumulated capital spend of an estimated QR5.4bn from 2014

Page 2 of 6

3. to 2018. The plan includes completing the construction of all its

current projects, including a 2.0mn MTPA integrated steel mill in

Algeria, and a mixed-feed steam cracker & petrochemical

complex. IQCD’s Chief Coordinator Abdulrahman Ahmad Al

Shaibi said that this expenditure may increase with the

determination of final construction costs for existing projects,

approval of projects currently under evaluation and the

implementation of the group’s 10-year growth strategy. In

2Q2011, the group’s subsidiary, Qatar Steel, commenced work

on its EF5 project consisting of a QR1.2bn green-field steel melt

shop built adjacent to its main facility in Mesaieed Industrial City,

Qatar. Commercial operations at the facility commenced in

February 2014, which is expected to boost the group’s billets

capacity by an additional 1.1mn. (GulfBase.com)

GWCS’ Logistics Village to be ready by June – The Gulf

Warehousing Company's (GWCS) Chairman Fahad bin Hamad

bin Jassim Al Thani announced that the fourth phase expansion

of GWC's Logistics Village Qatar will be completed by June

2014. Addressing GWC's ordinary annual general assembly,

Fahad said that the logistics village matters a lot for both the

company’s future success as well as the future of logistics

services in Qatar. The original master plan for the logistics

village was completed in April 2013, with all the warehouses and

services fully reserved. The company began the additional

fourth phase expansion, which acts as a complement to the

master. (Peninsula Qatar)

Qatari LNG exports to Argentina cross $1bn in 2013 –

Argentina's LNG imports from Qatar reached an all-time high of

$1bn in 2013 and are set to increase further over the coming

years. Argentina's Undersecretary for Investment Development

& Trade Promotion, Agustin Wydler said that while imports from

Qatar were huge, Argentina's volume of trade with Qatar

amounted to just around $5mn. He also added that talks are on

with major oil & gas companies in Qatar to boost energy

cooperation between the two countries. About the imbalance of

trade between the two countries, Wydler said that Argentina

imported LNG from Qatar worth around $400mn in 2012 which

grew to more than $1bn in 2013. While the country exporting to

Qatar only around $4-5mn worth of goods. (Gulf-Times)

GWCS’ AGM approves agenda, 15% cash dividends – The

Gulf Warehousing Company (GWCS) has approved its board’s

proposal in the AGM held on February 16 to distribute a cash

dividend of QR1.5 per share among others. (QE)

QE suspends trading in IHGS, QNCD shares on February 18

– The Qatar Exchange (QE) has announced trading suspension

in the shares of the Islamic Holding Group (IHGS) and Qatar

National Cement Company (QNCD) on February 18, 2014 due

to their AGM being held on that day. (QE)

International

Germany, France seek to revive FTT plan – Germany and

France will lead a face-saving bid this week to revive a flagging

project to tax financial transactions (FTT) in 11 Eurozone

countries and allay fears it could hamper economic recovery.

The tax is expected to be scaled back from an original plan to

introduce it from January to raise €35bn ($48bn) annually to

make banks pay back some of the money received in the 200709 financial crisis. The idea of a financial transaction tax failed to

win backing globally due to the US opposition, and a panEuropean Union tax or even one covering all 18 Eurozone

countries also found no support. Britain, Ireland, the Netherlands

and Sweden are among countries that have opposed it on

grounds that it would encourage banks and finance firms to

relocate trading activities. (Reuters)

Hollande offers tax stability to foreign businesses – French

President Francois Hollande appealed to foreign business

leaders to invest in France, offering them simpler and more

stable tax policies as his unpopular government tries to spur

growth and create jobs. Hosting a meeting of 30 heads of

French units of foreign companies, Hollande pledged to

guarantee that taxes on investments would not rise later – as

has happened in the past – and VAT and duty for firms would be

streamlined this year. Hollande, who last month announced

France would phase out €30bn in charges on companies by

2017 to reverse its slide in trade competitiveness, said French

business taxes would be harmonized with those of its neighbors,

especially Germany, by 2020. (Reuters)

Eurozone regulators gather for detail on ECB bank review

plans – Banks in the Eurozone are about to get greater insight

into the European Central Bank’s (ECB) landmark review of their

books, as national experts and their advisers meet in Frankfurt

to hammer out details of the next phase of the stress tests. The

ECB is carrying out a wide-ranging review of 128 regional banks

in an effort to address lingering doubts about their health before

it becomes their overall supervisor in November 2014. Banks

have already been asked for extensive amounts of data on their

loan books and trading assets for the 'Asset Quality Review', but

know little about the ECB’s methodology and data interpretation.

(ET, Reuters)

China January FDI rises in sign of confidence – The Chinese

Commerce Ministry stated that China received $10.76bn worth

of foreign direct investments (FDI) in January, up 16.1% from a

year earlier. The ministry said this is a sign that confidence in

the world's second-largest economy remains firm even as

growth cools. The majority of the new investment worth $6.33bn,

went into China's services industry, however, investment in

manufacturing fell 21.7%. (Reuters)

Regional

CDSI: Kingdom’s inflation falls to 2.9% in January –

According to data released by the Central Department Of

Statistics & Information (CDSI), the Kingdom’s annual inflation

eased marginally to 2.9% in January, the lowest level since April

2007, from 3% in the previous month. Prices of food &

beverages rose 5% YoY in January, but dipped 0.1% from the

previous month, while housing & utility costs climbed 3.7% on

an annual basis and 0.4% MoM. (GulfBase.com)

Kingdom exports SR96bn oil in January – Saudi Arabia

exported 240mn barrels of oil in January 2014, which amounted

to SR96.4bn. Domestic consumption during the month stood at

58.9mn barrels, or 20% of the total output. The International

Energy Agency (IEA) has predicted that global oil demand would

go up by 1.3mn bpd in 2014, or 92.5 mbpd. The average global

demand is expected to hover around 29.58mn bpd this year due

to over-supply from non-OPEC member countries. Oil

production in the US will increase by 782,000 bpd to reach

8.3mn bpd in 2014. Meanwhile, the US Energy Information

Administration has predicted that oil production in the country

would jump from 7.5mn bpd in 2013 to 8.5mn bpd in 2014.

(GulfBase.com)

Saudi Aramco likely to restart Yanbu plant by February-end

– Saudi Aramco is expected to restart its 240,000 bpd refinery in

Yanbu around end of February after it was shut down earlier this

month for planned maintenance. The refinery exports around

50,000-75,000 tons of naphtha per month, and the volumes lost

from the maintenance will be offset by large inflows of cargoes

from Europe and the Mediterranean region. Saudi Aramco

operates another 400,000 bpd refinery in Yanbu in partnership

with ExxonMobil, which is running normally. (Reuters)

Page 3 of 6

4. TAI declares SR17.5mn dividend for 2013 – Takween

Advanced Industries’ (TAI) board of directors has recommended

distributing dividends worth SR17.5mn to its shareholders for

2013. The dividend per share will be SR0.5, representing 5% of

the face value. Those shareholders who are registered with the

Securities Depository Center on the day of the general assembly

will be eligible for this dividend (to be announced later).

(Tadawul)

MCC declares SR72.36mn dividend for 2013 – Methanol

Chemicals Company’s (MCC) board of directors has

recommended the distribution of dividends worth SR72.36mn to

its shareholders for 2013. The dividend per share will be SR0.6,

representing 6% of the face value. The eligibility of dividends

shall be for the shareholders registered with the Securities

Depository Center at the closing of the general assembly

meeting’s day (to be announced later). (Tadawul)

Etihad Etisalat announces results, approves SR962.5mn

dividend for 4Q2013 – Etihad Etisalat Company held its

general assembly meeting and approved its board’s

recommendation for distributing cash dividends worth

SR962.5mn for 4Q2013. The dividend per share will be SR1.25

(12.5% of the nominal share value), in addition to interim

dividends of SR2,733.5mn distributed to shareholders for the 1,

2 and 3Q2013 i.e. SR3.55 per share. The dividends will be paid

to those shareholders, who are registered in the company

shareholder register at the end of trading on the day of the

general assembly. The 4Q2013 dividend brings the total

dividends for entire FY2013 to SR3,696mn, i.e. SR4.8 per

share, representing 55.36% of the net profits in 2013. The

dividend will be paid on February 26, 2014. (Tadawul)

Saudi hardware retailer Saco plans maiden IPO – The Saudi

Company for Tools & Hardware (Saco) – a pioneer in the

hardware retail & wholesale business and home improvement

superstores in the Kingdom – is set to launch its first IPO soon.

The company has appointed HSBC Saudi Arabia as the

financial adviser, lead manager and underwriter for its planned

IPO. Saco currently operates 21 retail outlets, including 3 Saco

World superstores in 12 cities across the Kingdom. The

company sells over 45,000 different hardware products in stores

ranging from 2,500 to 24,000 square meters. (GulfBase.com)

Mashreq raises foreign ownership limit to 49% – Dubaibased Mashreq's CEO said that the bank has increased the limit

on foreign ownership to 49% shares, in line with a wider move

by other companies in the UAE to open up to international

investors. Companies and banks in the UAE and Qatar are

reviewing their foreign ownership caps ahead of an upgrade by

the international index compiler MSCI to emerging market status

for these countries in May 2014, which is expected to attract

fresh foreign money. Earlier in September, Mashreq had raised

its foreign ownership limit to 20%. (Gulf-Times)

MAF launches AED100mn fashion district at Mall of the

Emirates – Majid Al Futtaim Group (MAF) has launched a

fashion district worth AED100mn at its flagship destination, Mall

of the Emirates. The fashion district, spread across 5,000

square meters with 30 new stores, is the first phase of the mall's

AED1bn redevelopment program, which is set for completion by

the end of 2015. Fuad Mansoor Sharaf, Senior Director of

Property Management, Shopping Malls said that Saudi citizens

are the mall's major visitors and customers. (GulfBase.com)

GMS plans to raise $100mn through London IPO – Abu

Dhabi-based oil services provider Gulf Marine Services (GMS)

intends to raise $100mn in an IPO in London, which is expected

to value the company at more than $1bn. Private equity firm Gulf

Capital currently owns 79% of GMS, which will offer shares in

the IPO through two subsidiaries. Horizon Energy and Al Ain

Capital also have minor holdings. While the price of shares will

be set at a later date, GMS was targeting a market capitalization

of $1bn. Given that a minimum of 25% shares must be listed for

inclusion in FTSE indices, this would indicate the company’s

IPO will be worth at least $250mn. (Reuters)

ADPC invests AED27m in Al Gharbia Region in 2013 – Abu

Dhabi Ports Company (ADPC) has invested around AED27mn

in the Al-Gharbia region in the UAE during last year. ADPC has

five ports in the region — Marfa, Al Sila, Sir BaniYas, Mugharrag

and Delma. Being the master developer of the non-oil & gas

maritime assets in the Emirate, ADPC is leading an investment

program designed to boost local industries and support the port

communities. The Al-Gharbia region is an area of exceptional

natural beauty occupying a vast area of 60,000 square

kilometers — 60% of the total area of Abu Dhabi, with a

coastline stretching for 350 kilometers. Rich in natural resources

such as palm trees, pearls, oil, gas and solar energy, Al Gharbia

contributes 45% of the Emirate’s GDP. ADPC’s investments in

the region, including AED7.5mn in Mugharrag Port, AED17mn at

Marfa Port and most recently AED2.5mn for the first phase of

development at Delma Port. (GulfBase.com)

GIH appoints head for $600mn distressed assets –

According to sources, Global Investment House (GIH) has

appointed Orhan Osmansoy to head its $600mn distressed

asset-management business. Osmansoy, a former CEO of Abu

Dhabi-based the National Investor, will lead the Special

Situations Asset-Management Business at GIH, dealing with

distressed assets and restructuring. (GulfBase.com)

MSM: Oman Oil to offer shares in Businesses – The Muscat

Securities Market (MSM) said that the Oman Oil Company is

planning to sell shares in some of its businesses to the public.

MSM’s Director General Ahmed Saleh Al Marhoon said that one

of its businesses is expected to be listed in the market this year.

Oman Oil has numerous subsidiaries that are diversified in oilrelated sectors. Al Marhoon said that some GCC countries are

selling shares in state-owned companies to spur stock-market

trading and citizens’ participation in the economy. (Bloomberg)

OUIS’ BoD recommends 35% cash dividend – Oman United

Insurance Company’s (OUIS) board of directors has

recommended a cash dividend of 35% of the paid-up capital i.e.

35 baizas per share. Meanwhile, the company’s AGM is

scheduled on March 30, 2014. (GulfBase.com)

Dolphin gas imports to cease once Omani output rises –

According to a top official of the Ministry of Oil & Gas, Oman

aims to phase out imports of Qatari gas supplied via the Dolphin

network once the projected jump in domestic gas production is

deemed sufficient enough to meet demand. The Ministry’s

Under-Secretary Salim al Aufi said that imports of natural gas

through the Dolphin network – averaging 5-7mn standard cubic

meters per day (mmscmd) – represent just a small percentage

of the total domestic production of around 85 mmscmd.

(Bloomberg)

UGIC not to distribute dividends for 2013 – The United Gulf

Investment Corporation’s (UGIC) board of directors has decided

not to distribute dividends to its shareholders for the financial

year ended December 31, 2013. (GulfBase.com)

SEEF’s BoD recommends 10% cash dividend – SEEF

Properties Company’s board of directors recommended a cash

dividend of 10% (i.e 10 fils per share) to its shareholders, who

are registered on the date of the AGM. (Bahrain Boursse)

BMMI’s BoD recommends cash dividend – Bahrain Maritime

& Mercantile International Company’s (BMMI) board of directors

Page 4 of 6

5. recommended a cash dividend of 50 fils per share (of which 20

fils per share was already distributed as interim dividend) to its

shareholders, who are registered on the date of the AGM.

(Bahrain Bourse)

Page 5 of 6

6. Rebased Performance

Daily Index Performance

180.0

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

1.5%

1.5%

143.6

1.0%

130.6

0.8%

0.5%

0.7%

0.0%

May-13

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu*

North American Spot LPG

Propane Price*

North American Spot LPG

Normal Butane Price*

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,328.79

0.8

0.8

10.2

DJ Industrial*

16,154.39

0.0

0.0

(2.5)

21.69

1.0

1.0

11.4

S&P 500*

1,838.63

0.0

0.0

(0.5)

109.18

0.1

0.1

(1.5)

NASDAQ 100*

4,244.03

0.0

0.0

1.6

5.54

0.0

0.0

27.4

STOXX 600

334.56

0.4

0.4

1.9

155.00

0.0

0.0

22.8

DAX

9,656.76

(0.1)

(0.1)

1.1

138.50

0.0

0.0

1.5

FTSE 100

6,736.00

1.1

1.1

(0.2)

1.37

0.1

0.1

(0.3)

CAC 40

101.92

0.1

0.1

(3.2)

Nikkei

GBP

1.67

(0.2)

(0.2)

0.9

MSCI EM

CHF

1.12

0.2

0.2

0.2

SHANGHAI SE Composite

AUD

0.90

(0.0)

(0.0)

1.3

USD Index*

80.14

0.0

0.0

RUB

35.25

0.2

0.2

BRL

0.42

(0.2)

(0.2)

(1.1)

Yen

Dubai

Oct-12

(0.2%)

Abu Dhabi

QE Index

Mar-12

Bahrain

Aug-11

Kuwait

Jan-11

(0.4%)

(0.5%)

Oman

(0.3%)

(1.0%)

Qatar

(0.5%)

Saudi Arabia

Jun-10

2.0%

168.5

4,335.17

(0.1)

(0.1)

0.9

14,393.11

0.6

0.6

(11.7)

964.29

0.7

0.7

(3.8)

2,135.42

0.9

0.9

0.9

HANG SENG

22,535.94

1.1

1.1

(3.3)

0.1

BSE SENSEX

20,464.06

0.5

0.5

(3.3)

7.2

Bovespa

47,576.33

(1.3)

(1.3)

(7.6)

1,347.41

0.3

0.3

(6.6)

Source: Bloomberg (*Market closed on February 17, 2014)

RTS

Source: Bloomberg (*Market closed on February 17, 2014)

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (―QNBFS‖) a wholly-owned subsidiary of Qatar National Bank (―QNB‖). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6