Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

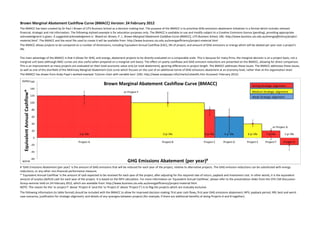

Brown Marginal Abatement Cashflow Curve (BMACC)

1. Brown Marginal Abatement Cashflow Curve (BMACC) Version: 24 February 2012

The BMACC has been created by Dr Paul J Brown of UTS Business School as a decision making tool. The purpose of the BMACC is to prioritise GHG emissions abatement initiatives in a format which includes relevant

financial, strategic and risk information. The following stylised example is for education purposes only. The BMACC is available to use and modify subject to a Creative Commons licence (pending), providing appropriate

acknowledgment is given. A suggested acknowledgment is: 'Based on: Brown, P. J., Brown Marginal Abatement Cashflow Curve (BMACC), UTS Business School, URL: http://www.business.uts.edu.au/energyefficiency/project‐

material.html'. The BMACC and the excel file used to create it will be available from: http://www.business.uts.edu.au/energyefficiency/project‐material.html

The BMACC allows projects to be compared on a number of dimensions, including Equivalent Annual Cashflow (EAC), life of project, and amount of GHG emissions or energy which will be abated per year over a project's

life.

The main advantage of the BMACC is that it allows for GHG, and energy, abatement projects to be directly evaluated on a comparable scale. This is because for many firms, the marginal decision is on a project basis, not a

marginal unit basis (although MAC curves are also useful when prepared on a marginal unit basis). The effect on yearly cashflows and GHG emission reductions are presented on the BMACC, allowing for direct comparison.

This is an improvement as many projects are evaluated on their total economic value only (or total abatement), ignoring differences in project length. The BMACC addresses these issues. The BMACC addresses these issues,

as well as one of the shortfalls of the McKinsey Marginal Abatement Cost curve which focuses on the cost of an additional tonne of GHG emissions abatement at an economy level, rather than at the organisation level.

The BMACC has drawn from Andy Pope's worked example 'Column chart with variable bars' (URL: http://www.andypope.info/charts/colwidth.htm Accessed: February 2012).

better160

Brown Marginal Abatement Cashflow Curve (BMACC) Strong Strategic alignment

140

Equivalent Annual Cashflow*

or Project F Medium Strategic alignment

120 Weak Strategic alignment

100

80

60

40

or Project A

20

2 yr life 3 yr life 4 yr life 5 yr life 6 yr life 7 yr life 1 yr life

0

Project A Project B Project C Project D Project E Project F Project G

‐20

‐40

‐60

worse GHG Emissions Abatement (per year)#

# 'GHG Emissions Abatement (per year)' is the amount of GHG emissions that will be reduced for each year of the project, relative to alternative projects. The GHG emission reductions can be substituted with energy

reductions, or any other non‐financial performance measure.

* 'Equivalent Annual Cashflow' is the amount of cash expected to be received for each year of the project, after adjusting for the required rate of return, payback and investment cost. In other words, it is the equivalent

amount of surplus (deficit) cash for each year of the project. It is based on the NPV calculation. For more information on 'Equivalent Annual Cashflow', please refer to the presentation slides from the CPA CSR Discussion

Group seminar held on 24 February 2012, which are available from: http://www.business.uts.edu.au/energyefficiency/project‐material.html

NOTE: The reason for the 'or project F' above 'Project A' (and the 'or Project A' above 'Project F') is to flag the projects which are mutually exclusive.

The following information (in table format) should be included with the BMACC to allow for improved decision making: first year cash flows; first year GHG emissions abatement; NPV; payback period; IRR; best and worst

case scenarios; justification for strategic alignment; and details of any synergies between projects (for example, if there are additional benefits of doing Projects A and B together).

This work is licensed under the Creative Commons Attribution 3.0 Australia License. To view a copy of this license, visit http://creativecommons.org/

licenses/by/3.0/au/ or send a letter to Creative Commons, 444 Castro Street, Suite 900, Mountain View, California, 94041, USA.