ETIP PV conference: 'Photovoltaics: centre-stage in the power system

•

2 j'aime•2,277 vues

Repowering Europe - 6th ETP SmartGrids General Assembly - 18 & 19 May 2016, Brussels

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

En vedette (14)

Similaire à ETIP PV conference: 'Photovoltaics: centre-stage in the power system

Similaire à ETIP PV conference: 'Photovoltaics: centre-stage in the power system (20)

Plus de Cluster TWEED

Plus de Cluster TWEED (20)

Dernier

Dernier (20)

ETIP PV conference: 'Photovoltaics: centre-stage in the power system

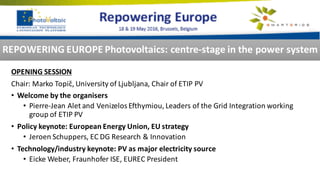

- 1. OPENING SESSION Chair: Marko Topič, University of Ljubljana, Chair of ETIP PV • Welcome by the organisers • Pierre-Jean Alet and Venizelos Efthymiou, Leaders of the Grid Integration working group of ETIP PV • Policy keynote: European Energy Union, EU strategy • Jeroen Schuppers, EC DG Research & Innovation • Technology/industry keynote: PV as major electricity source • Eicke Weber, Fraunhofer ISE, EUREC President REPOWERING EUROPE Photovoltaics: centre-stage in the power system

- 2. SESSION I: Inverters: The smart interface Chair: Nikos Hatziargyriou, NTUA, Chair of ETP SmartGrids • Next generation of smart invertersand aspects with respect to the energy transition • Jan Van Laethem, SMA • Supporting power quality in distribution networks with inverters • Andreas Schlumberger, KACO New Energy • Stability of the power system with converter-interfacedgeneration • Marie-Sophie Debry, RTE REPOWERING EUROPE Photovoltaics: centre-stage in the power system

- 3. SESSION II: StorageChair: Wim Sinke, ECN Solar Energy, Vice-Chair of ETIP PV • Storage supporting PV deployment • Veronica Bermudez, EDF - R&D • Impact of storage on PV attractiveness • Mariska de Wild-Schotten, SmartGreenScans • Market development and price roadmap • Marion Perrin, CEA INES • The virtual battery: energy management in buildings and neighbourhoods • Emanuel Marreel, Siemens REPOWERING EUROPE Photovoltaics: centre-stage in the power system

- 4. SESSION III: Electricity market and system operations Chair: Venizelos Efthymiou, University of Cyprus, Vice-Leader of the Grid Integration working group of ETIP PV • Real-time monitoring • Nikos Hatziargyriou, NTUA, Chair of ETP SmartGrids • Forecasting use cases • Marion Lafuma, Reuniwatt • Market access • Maher Chebbo, SAP REPOWERING EUROPE Photovoltaics: centre-stage in the power system

- 5. SESSION IV: PV changing the power business Chair: Pierre-Jean Alet, CSEM, Leader of the Grid Integration working group of ETIP PV • Changing roles: business models • Johannes von Clary, E.On • PV value for Europe beyond electrons • James Watson, SolarPower Europe REPOWERING EUROPE Photovoltaics: centre-stage in the power system

- 6. Jeroen SCHUPPERS European Commission, DG Research and Innovation An Energy Union for Research, Innovation and Competitiveness Repowering Europe Brussels, 18 May 2016 1

- 7. Towards an Energy Union ● The Energy Union is a top priority for this Commission ● More cooperation/coordination among MS is expected in order to better face current challenges, in particular as regards energy security and climate ● More cooperation/coordination among MS is the foundation of the European Research Area 2

- 8. 1. Energy security, solidarity and trust 2. A fully integrated European energy market 3. Energy efficiency contributing to moderation of demand 4. Decarbonising the economy 5. Research, Innovation and Competitiveness Energy Union (5 pillars): 5 The new Strategic Energy Technology Plan (SET Plan) 3

- 9. 4 Strategic Energy Technology (SET) Plan ● The technology pillar of EU energy and climate change policy ● In force since 2010/11 ● Objective: to accelerate the development of a portfolio of low carbon technologies leading to their market take-off

- 10. First links to policy agenda: 2020 targets for energy & climate Focus on individual technologies with market and target impact up to 2020 A bit of history… -20 % Greenhouse Gas Emissions 20% Renewable Energy 20 % Energy Efficiency 5

- 11. "Towards an Integrated Roadmap" - 40 % Greenhouse Gas Emissions 27 % Renewable Energy 27% Energy Efficiency Still links to policy agenda: 2030 updated targets for energy & climate From individual technologies to energy system as a whole New policy challenges: Consumer at the centre Energy efficiency (demand) System optimisation Technologies (supply) 6

- 12. Energy Union priorities Ten actions to accelerate the energy system transformation (SET Plan) No1 in Renewables 1. Performant renewable technologies integrated in the system 2. Reduce costs of technologies Smart EU energy system, with consumer at the centre 3. New technologies & services for consumers 4. Resilience & security of energy system Efficient energy systems 5. New materials & technologies for buildings 6. Energy efficiency for industry Sustainable transport 7. Competitive in global battery sector (e-mobility) 8. Renewable fuels (9) Driving ambition in carbon capture storage and use deployment (10) Increase safety in the use of nuclear energy 7

- 13. Making the SET Plan fit for new challenges A more targeted focus Stronger link with energy policy A more integrated approach Holistic view of the energy system Full research and innovation chain A new SET Plan governance 8

- 14. A new SET Plan governance model 1. Strengthened cooperation With Members States [EU 28 + Iceland, Norway, Switzerland and Turkey] With Stakeholders o Opening and widening to new actors o Bringing together all relevant stakeholders including, e.g. ETIPs, EERA, PPPs, JTIs, KET stakeholders, stakeholders from funding instruments under the Emissions Trading System… 2. More coordination between Members States: More joint actions 9

- 15. 3. Transparency, indicators and periodic reporting Annual KPIs: o Level of investments – public and private sector o Trends in patents o Number of researchers active in the sector Every 2 years, progress should be measured on: o Technology developments o Cost reduction o Systemic integration of new technologies State of the Energy Union Report 4. Monitoring and knowledge sharing A new SET Plan governance model 10

- 16. The SET Plan Actors • European Commission • Member States • Stakeholder platforms 11

- 17. The SET Plan Actors 1. Member States [EU28 + CH, IS, NO, TR] Steering Group (SG): Highest level discussion platform, chaired by the EC. The SG Bureau: smaller but balanced representation of the SG to assist the EC in the preparation of meetings, chaired by the MS. Joint Actions Working Group (JAWG): a working group of the SG open to all interested MS to discuss joint actions, chaired by the MS. 2. Stakeholder Platforms European Technology and Innovation Platforms (ETIPs): Structures gathering all relevant stakeholders. The European Energy Research Alliance (EERA) Other EU Stakeholder platforms active in/relevant to the energy sector. • 12

- 18. European Technology and Innovation Platforms (ETIPs) Participants ● Continuation of existing ETPs and EIIs in unified Platforms per technology. ● Recognised interlocutors about sector specific R&I needs ● Composition – covering the whole innovation chain: industrial stakeholders (incl. SMEs), research organisations and academic stakeholders, business associations, regulators, civil society and NGOs, representatives of MS Freedom to organise yourselves as you see fit. 13

- 19. European Technology and Innovation Platforms (ETIPs) Main Role: strategic advice to the EC and the Steering Group based on consensus ● Prioritisation within the 10 key actions both on objectives and implementation; ● Implementation: what best at EU/national/regional/industrial level; ● Prepare and update Strategic Research and Innovation Agendas; ● Identify innovation barriers, notably related to regulation and financing; ● Report on the implementation of R&I activities at European, national/regional and industrial levels; ● Develop knowledge-sharing mechanisms that help bringing R&I results to deployment. 14

- 20. SET Plan implementation in a nutshell 1. Setting targets 2. Select and monitor specific R&I actions 3. Identify and agree on Joint Actions 4. Identify Flagship Actions (at European and national levels) 15

- 21. 1. Setting targets ● 'Issues Papers' drafted by the Commission (RTD, ENER, JRC), setting the scene and proposing targets ● Publication on SETIS ● Broad stakeholder consultation ● Stakeholders submit position through 'Input Papers' ● Commission drafts 'Declaration of Intent' ● Discussion in meeting of the SET Plan Steering Group with invited stakeholders ● Agreement on targets and agree to develop an implementation plan 16

- 22. 2. Select & monitor specific R&I actions • Goals • Detail what needs to be done over the next years to achieve the targets at European and national level • Limited set of actions (technological + non-technological) • Resources + timeline for each R&I action • Putting a monitoring system in place • Work to be done in temporary Working Groups • within ETIP when there is one • Timeline: ~2-3 months 17

- 23. 3. Identify/agree on Joint Actions • Goal • Identify and decide on Joint Actions • Strategy to be developed for the SET 10 Key Actions • Joint Actions with EU (ERA-Nets) & non-EU funds • Joint Programming beyond ERA Net • Joining EU risk financing facility • Joint policy actions • Work to be done by the JAWG • Countries engaged in ERA-Nets • Results reported to SG and feed Implementation Plan 18

- 24. 4. Identify Flagship Actions • Goal • Identify Flagship Actions (at European or national levels) and specify to which actions they contribute and who implements them • When no Joint Actions are possible, Flagship Actions can fill the gap • What is a Flagship Action? A Flagship action is considered the best example of what R&I can produce in a given sector or with a specific technology in order to reach the SET Plan targets. The innovation potential and the "leading by example" features are key. A flagship action is meant to make a real change in the low-carbon energy technologies landscape. • Work to be done by the Working Groups 19

- 25. Working Groups • Mission • To develop the Implementation Plans • Aligned with Declaration of Intent • Composition (~ 30) • Experts from ETIPs • Input from SET Plan countries (= government representatives) & EC • Chaired by a champion country + champion industrial stakeholder • Which countries? • High policy interest in the sector and committed to engage in Joint Actions 20

- 26. ● WGs will join the 3 pieces together and finalize the Implementation Plans ● Plans are then reviewed by the SG and adopted when there is consensus ● "On the ground" implementation should follow Working Groups 21

- 27. Example of aggregated information 22

- 28. Example of aggregated information 23

- 29. 24 Follow the process on SETIS https://setis.ec.europa.eu/towards-an-integrated-SET-Plan More information:

- 30. Thank you for your attention 25

- 31. © Fraunhofer ISE PHOTOVOLTAICS AS MAJOR ELECTRICITY SOURCE Eicke R. Weber Fraunhofer Institute for Solar Energy Systems ISE and University of Freiburg, Germany REPOWERING EUROPE PV European Technology & Innovation Platform Brussels, Belgium, May 18, 2016

- 32. © Fraunhofer ISE 2 Cornerstones for the Transformation of our Energy System to efficient use of finally 100% renewable energy – Energy efficiency: buildings, production, transport Massive increase in renewable energies: photovoltaics, solar and geo thermal, wind, hydro, biomass... Fast development of the electric grid: transmission and distribution grid, bidirectional Small and large scale energy storage systems: electricity, hydrogen, methane, methanol, biogas, solar heat, hydro..... Sustainable mobility as integral part of the energy system: electric mobility with batteries and hydrogen/fuel cells

- 33. © Fraunhofer ISE 3 Contribution of RES to Electricity Supply in Germany Historical Development Data: BMWi 3% 30% 41 GW Wind in 25a 39 GW PV in 15a Electricity Feed-in Act: Jan. 1991 - March 2000 EEG: January 2009 1,000 roofs program: 1991-1995 100,000 roofs program: 1999-2003 EEG: August 2004 EEG: April 2000

- 34. © Fraunhofer ISE 4 Long-term utility-scale PV system price scenarios Source: Fraunhofer ISE (2015): Current and Future Cost of Photovoltaics. Study on behalf of Agora Energiewende

- 35. © Fraunhofer ISE 5 Source: Fraunhofer ISE (2015): Current and Future Cost of Photovoltaics. Study on behalf of Agora Energiewende Levelized Cost of Electricity Solar Power will soon be the Cheapest Form of Electricity in Many Regions of the World

- 36. © Fraunhofer ISE 6 Source: Solarbuzz 2014

- 37. © Fraunhofer ISE 7 Crystalline Silicon Technology Portfolio c-Si PV is not a Commodity, but a High-Tech Product! material quality diffusion length base conductivity device quality passivation of surfaces low series resistance light confinement cell structures PERC: Passivated Emitter and Rear Cell MWT: Metal Wrap Through IBC-BJ: Interdigitated Back Contact – Back Junction HJT: Hetero Junction Technology Adapted from Preu et al., EU-PVSEC 2009 material quality module efficiency Industry Standard IBC-BJ HJT PERC MWT- PERC 20% 19% 18% 17% 16% 15%14% 21% device quality BC- HJT

- 38. © Fraunhofer ISE 8 Advanced Cell Technologies Passivated Emitter and Rear PERC1 Metal Wrap-Through MWT-PERC2 2Dross et al., Proc. 4th WCPEC, 2006, pp. 1291-4 1Blakers et al., Appl. Phys. Lett. 55, pp. 1363-5, 1989 Heterojunction on Intrinsic layer HIT3 Interdigitated Back Contact/Junction IBC-BJ4 Passivating Layer Local Contacts Metal Wrap Through Contact Passivating Layer Local Contacts Lightly Doped Front Diffusion Texture+passivation Layer 3 Sanyo/Panasonic 4 Sunpower

- 39. © Fraunhofer ISE 9 High-efficiency n-type PERL Cells Lab Results Excellent performance at cell level Only very thin ALD layer necessary Best cell 705 41.1 82.5 23.9* Voc [mV] Jsc [mA/cm2] FF [%] η [%] Benick et al., APL 92 (2008) Glunz et al., IEEE-PVSC (2010) *Confirmed at Fraunhofer ISE CalLab ap = aperture area (= bus bar included in illuminated area)

- 40. © Fraunhofer ISE 10 Advanced Cell Technologies Tunnel Oxide Passivated Contact (TOPCon) TOPCon enables: Excellent carrier-selectivity High tolerance to high-temperature processes Very high Voc and FF achieved due to Excellent surface passivation 1D carrier flow pattern in base Voc Jsc FF η [mV] [mA/cm2] [%] [%] Champion 719 41.5 83.4 24.9[*] TOPCon: J0,rear 7 fA/cm² n-base [*]FZ-Si, n-type, 2x2 cm², aperture area, confirmed by Fraunhofer ISE Callab

- 41. © Fraunhofer ISE 11 NexWafe: Kerfless Wafer Production for High-Efficiency PV Product: n-type wafer for high-efficiency solar cells ISE high-throughput ProConCVD to grow the epitaxial layer Wafer thickness 150 µm “drop-in” replacement for Cz- wafer Proof-of-concept verified on small scale, upscaling under way! Wafers available 2017! Removed epitaxial wafer Seed wafer re-usable

- 42. © Fraunhofer ISE 12 High-Efficiency III/V Based Triple-Junction Solar Cells Slide: courtesy of F. Dimroth

- 43. © Fraunhofer ISE 13 GaInP 1.9 eV GaAs1.4 eV GaInAsP 1.0 eV GaInAs 0.7 eV Bonding InP engineered substrate InP based 4-Junction Solar Cell Results on Engineered Substrate One sun QuadFlash: h = 46.1 % C = 312 3.2 3.6 4.0 4.4 80 85 90 1 10 100 1000 35 40 45 Voc [V]FF[%] lot29-02-x23y08 Single Flash QuadFlash h[%] Concentration [suns]

- 44. © Fraunhofer ISE 14 BUT - how will this be achieved? - Nanowire arrays f rom EPI TAXY - Nanowire arrays f rom AEROTAXY - may bring to the market single- Xtal I I I - V solar cells to the cost of Thin Films Lars Samuelson, Lund, Sweden: “Nanowire Array Solar Cells” ! Nanowire Array Solar Cells

- 45. © Fraunhofer ISE 15 PV-Production Capacity by Global Regions 1997-2012 Will China dominate the 100 GW/a World Market 2020? Source: Navigant Consulting, Grafics: PSE AG 2013

- 46. © Fraunhofer ISE 16 World Market Outlook: Experts are Optimistic Example Sarasin Bank, November 2010 market forecast (2010): 30 GWp in 2014, 110 GWp in 2020 annual growth rate: in the range of 20 % and 30 % Newly installed (right) Annual growth rate (left) Source:Sarasin,SolarStudy,Nov2010 Growthrate 2014: ca. 40 GWp, 1/3 above forecast! Total new installations (right scale) Annual growth (left scale)

- 47. © Fraunhofer ISE 17 Global PV Production Capacity and Installations Source: Lux Research Inc., Grafik: PSE AG Outlook for the development of supply and demand in the global PV market. Production Capacity Installations Excess Capacity ModuleCapacity(GW) ExcessCapacity(GW)

- 48. © Fraunhofer ISE 18 Global PV Production Capacity and Installations Source: Lux Research Inc., Grafik: PSE AG Production Capacity Installations Excess Capacity ModuleCapacity(GW) ExcessCapacity(GW) 2008 – 2016: 1st cycle of PV

- 49. © Fraunhofer ISE 19 Global PV Production Capacity and Installations Source: Lux Research Inc., Grafik: PSE AG Production Capacity Installations Excess Capacity ModuleCapacity(GW) ExcessCapacity(GW) From 2016: Start of 2nd cycle of PV!

- 50. © Fraunhofer ISE 20 PV Market Growth: PV heading into the Terawatt Range! Source: IEA 2014 Rapid introduction of PV globally is fueled by availability of cost-competitive, distributed energy In 2050 between 4.000 and 30.000 GWp PV will be installed! By 2015, less than 300 GWp have been installed! We are just at the beginning of the global growth curve!

- 51. © Fraunhofer ISE 21 How Will the Energy System Look Like in 2050? Electricity HeatMobility Develop a model to simulate the transformation of the energy system

- 52. © Fraunhofer ISE 22 © Fraunhofer ISE Optimization of Germany’s future energy system based on hourly modeling REM od-D Renewable Energy Model – Deutschland Electricity generation, storage and end-use Fuels (including biomass and synthetic fuels from RE) Mobility (battery- electric, hydrogen, conv. fuel mix) Processes in industry and tertiary sector Heat (buildings, incl. storage and heating networks) Comprehensive analysis of the overall system Slide courtesy Hans-Martin Henning 2014

- 53. © Fraunhofer ISE 23 Renewables Fossil Renewables Fossil Renewables Fossil Renewables Fossil GW CHP HP Renewables Fossil Electricity Import Electricity Renewables Surplus Export Fossil Hydrogen Raw biomass Heat Liquid fuels Gas Electricity Hard coal PP Nuclear PP Reforming Battery stor. Pumped stor. H2-2-Fuel GT CCGT District heat Oil PP Lignite PP Processing Bio-2-el. H2-storage Electrolysis Methanation TWh GW 0 108 TWh TWh GW GW Solar thermal PV Hydro power Onshore wind Offshore wind Raw biomass 0 0 0 103 Biogas storage 0 TWh 36 TWh 18 1 85 Bio-2-Liquid 9 1 TWh TWh TWh Hard coal Lignite Petroleum TWh 144 TWh 0 0 Natural gas 37 13 7 TWh 68 27 TWh 3 TWh 485 0 0 39 10 CO2 emissions1990 (reference year) 990 Mio t CO2 CO2 emissions 196 Mio t CO2 CO2 reduktion related to 1990: TWh TWh 0 TWh TWh Uranium 0 0 10 Primary fossil energy carrier 445 384 Industry (fuel based process) Electricity (baseload) 80% TWh TWh TWh TWh GW GW 215 237 Final energy 237 TWh TWh 0 0 Conversion 0 Losses 375 Bio-2-CH4 0 0 TWh TWh TWh TWh 103 77% 15 TWhTWh 0 Losses 502 Final energy 630 TWh GW GW 125 128 TWh 120 TWh 6 5 19 Battery veh. TWh 0 TWhTWh TWh TWh TWh TWh GWh GWh 0 0 GWh 21 Consumption sector 121 TWh 3 TWh Deep geothermal Environ- mental heat Renewable energy sources Renewable raw materials Water Sun Bio-2-H2 0 176 32 TWh 0 Wind 335 TWh Biodiesel 5 TWh Energy conversion Storage 10 375 383 52 49 TWh TWh 0 0 501 Final energy 860 TWh TWh TWh TWh GW GW GW 100% GW TWh TWh TWh TWh TWh TWh 11 106 20 98 0 Heating (space heating and hot water) 237 20 Total quantity gas TWh TWh TWh TWh TWh GW GW 66 TWh TWh 17 TWh TWh 0 0 50 126 Final energy 0% 11 GW GW GW GW GW GW 20 15 GW0 TWh TWh 419 21 135 85 TWh5 0 TWh TWh TWh TWh TWh TWh TWh 23% 108 100% Conversion Losses 0 0 29% 128 Conversion Total quantity hydrogen 108 TWh 0% Total quantity raw biomass 244 TWh TWh GW GW Biogasplant 2 58 77 55 103 0 103 0 91 141 TWh0 TWh0 0 0 19 Total quantity heating 0 Conversion 17 Losses 264 Final energy 280 TWh Mobility 108 71% Conversion 0 Losses 72 Final energy 335 TWh 46 TWh 87% 13% Total quantity electricity 39% 61% Total quantity liquid fuels 271 Conversion 88 Losses © FraunhoferISE REMod-D Energy system model

- 54. © Fraunhofer ISE 24 © Fraunhofer ISE TWh Traktion H2-Bedarf 45 11 TWh TWh 39 TWh 14 TWh Einzelgebäude mit Sole-Wärmepumpe Solarthermie 11 Solarthermie 8 Gebäude 9 TWh el. WP Luft 43 TWh TWh 44 4 Einzelgebäude mit Gas-Wärmepumpe 13 TWh 14 4 W-Speicher GWth TWh 60 TWh 82 TWh 220 TWh 420 22 GWth TWh 103 GWh 51 W-Speicher14el. WP Sole Biomasse TWh 0 TWh 15 KWK-BHKW Solarthermie 13 TWh Strombedarf gesamt (ohne Strom für Wärme und MIV) 375 TWh TWh 3 GWgas 0 220 0 TWh 0Sabatier Methan-Sp. H2-Speicher 7 GWth TWh TWh 41 3 GWth Gas-WP W-Speicher 25 20 40 TWh 388 TWh 20 GWth TWh Wärmenetze mit GuD-KWK 7 GWth TWh W-Speicher TWh Wärmenetze mit BHKW-KWK Wärmebedarf gesamt TWh 26 TWh TWh 217 TWh 82 16 TWh GWel TWh 23 4 TWh 9 Pump-Sp-KW 7 TWh TWh 6 TWh Gasturbine W-Speicher Steink.-KW Braunk.-KW Öl-KW 3 GW 0 GW5 GW 0 GW 7 GW Atom-KWPV Wind On Wind Off Wasserkraft 112 TWh 103 TWh 147 Batterien 24 GWh GW 120 GW 32 GW 143 TWh 5 TWh 60 GWh TWh TWh Einzelgebäude mit Luft-Wärmepumpe GWth Gebäude 8 TWh 7 TWh 50 14 4 TWh TWh 19 GWth TWh GWh Einzelgebäude mit Gaskessel TWh Gaskessel 71 Gebäude 32 GWth 0 4 Gebäude 59 0.0 TWh 3734 Solarthermie 6 W-Speicher Gebäude 15 27 GWh 23 TWh TWh TWh 173 GWh 3 TWh ungenutzter Strom (Abregelung) TWh 0 TWh 26 TWh 12 TWh TWh 5 TWh TWh 241 TWh Gebäude 4 87 TWh 6 TWh Gebäude 59 7 GWth TWh 3 TWh WP zentral 20 KWK-GuD 27 35 GWel TWh 20 60 TWh 7 GW Einzelgebäude mit Mini-BHKW 6 46 WP zentral 23 4 8 TWh TWh Verkehr (ohne Schienenverkehr/Strom) Brennstoff-basierter Verkehr Batterie-basierter Verkehr Wasserstoff-basierter Verkehr 137 TWh TWh TWh TWh TWh TWh TWhTraktion gesamt Brennstoffe Traktion erneuerbare Energien primäre Stromerzeugung fossil-nukleare Energien 14 GWth TWh 56 GWh 86 TWh Geothermie 6 Gebäude 2 GWth 10 TWh TWh108 TWh 57 TWh 0 TWh 3 TWh TWh 173 Wärmenetze mit Tiefen-Geothermie TWh Brennstoffe TWh Erdgas 394 TWh 4 TWh 22 TWh Elektrolyse 82 33 GWel 4 21 TWh 0 TWh TWh 26 1 GW GuD-KW ungenutztWarmwasserRaumheizung 290 TWh 98 TWh 2 Solarthermie GWh Mini-BHKW 23 GWh TWh Solarthermie 13 20 GWth GWel TWh TWh 0.6 GWth TWh TWh W-Speicher TWh TWh 76 6 41 82 Strombedarf Traktion Solarthermie 12 6 TWh 73 TWh 25 TWh Brennstoffe 55 220 100% Wert 2010 335 TWh TWh Treibstoff Verkehr 55 TWh 420 TWh Brennstoff-basierte Prozesse in Industrie und Gewerbe gesamt 445 TWh Solarthermie % 41 55 ©FraunhoferISE Electricity generation Photovoltaics 147 GWel Medium and large size CHP (connected to district heating) 60 GWel Onshore Wind 120 GWel Offshore Wind 32 GWel Slide courtesy Hans-Martin Henning 2014

- 55. © Fraunhofer ISE 25 Scenario results hourly modeling 2014-2050 Cumulative total cost No penalty on CO2 emissions Stable fossil fuel prices #1 -80 % CO2, low rate building energy retrofit, electric vehicles dominant, coal until 2050 #2 -80 % CO2, low rate building energy retrofit, mix of vehicles, coal until 2050 #3 -80 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2050 #4 -80 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2040 #5 -85 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2040 #6 -90 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2040 Ref today‘s system; no change

- 56. © Fraunhofer ISE 26 Scenario results Cumulative total cost No penalty on CO2 emissions Stable fossil fuel prices #4 -80 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2040 #5 -85 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2040 Ref today‘s system; no change Cumulative cost of scenarios # 4 und # 5 approx. 1100 bn € higher than reference for the total time 2014 – 2050 (about 0.8 % of German GDP)

- 57. © Fraunhofer ISE 27 Scenario results Cumulative total cost Rising penalty cost for CO2 emissions up to 100 € per ton in 2030; then stable Price increase for fossil fuels 2 % p.a. #1 -80 % CO2, low rate building energy retrofit, electric vehicles dominant, coal until 2050 #2 -80 % CO2, low rate building energy retrofit, mix of vehicles, coal until 2050 #3 -80 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2050 #4 -80 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2040 #5 -85 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2040 #6 -90 % CO2, high rate building energy retrofit, mix of vehicles, coal until 2040 Ref today‘s system; no change With CO2 pricing, the total cost of business-as-usual till 20150 will be even higher than for the transformed system!

- 58. © Fraunhofer ISE 28 How Will the Energy System Look Like in 2050? Electricity HeatMobility Essential messages out of the model: The cost of the new Energy System is not higher than the cost for the current system! The cost for transformation is in the same order as maintaining the current system!

- 59. © Fraunhofer ISE 29 Grid stability with growing amounts of fluctuating RE: Grid in Germany today more stable than in 2006!

- 60. © Fraunhofer ISE 30 Technology development combined with rapid growth of production volumes resulted in an unprecedented reduction in PV production cost and prices, by more than an order of magnitude in the last decades! The market is dominated by crystalline-Si technologies; a multitude of further technology advances, allowing higher efficiencies at lower production costs, are ready to be implemented in c-Si PV cells and modules. The cost of PV systems will decrease further, driven by technology developments, accompanied by supportive financial and regulatory environments. PV will grow soon into the Terawatt range, making it the cheapest form of electricity in many regions of the world 2-4 ct/kWh. The key for a stable energy system based on RE is to link the electricity, heat and transport sectors. The challenge for the EU will be to maintain the current technological leadership position, by keeping a stable market, combined with local PV production along the whole food chain, from research to deployment! Photovoltaics as Major Electricity Source

- 61. © Fraunhofer ISE 31 Thank you For your attention!

- 62. The European Inverter Industry Dr Krzysztof Puczko Repowering Europe May 2016

- 63. 2 About PV Markets… Can Europe sustain industrial leadership in this area?

- 64. 3Delta Confidential PV market development • The PV installed capacity reached 100 GWp in 2012 but Europe’s leading role in the PV market came to the end • Europe remains the world’s leading region in terms of cumulative installed capacity (>70 GW) but the market gets more global • PV market globalization became a challenge for many European technology suppliers 0 10 20 30 40 50 60 70 80 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 NewPVinstallations[GW] China Japan USA UK Germany Rest of Europe India Latin America France Rest of Asia Rest of the World

- 65. 4Delta Confidential EU Market Split in 2012 Source – EPIA 2015

- 66. 5Delta Confidential Market Split outside EU in 2012 Source – EPIA 2015

- 67. 6Delta Confidential Market drivers • Incentives • Energy mix targets • CO2 savings • Growing power demand • Grid parity • New business models • Smart grid development • Energy mix demand • Technology development Changing drivers for further expansion (2016=>2020) Former drivers (200 GW): Future drivers (500 GW):

- 68. 7 Are regional variations in grid codes an opportunity or a threat to European manufacturers?

- 69. 8Delta Confidential 8 Grid code related inverter settings G.59/2 exemplary settings

- 70. 9Delta Confidential 9 Grid grid stability services Source: National Grid UK

- 71. 10Delta Confidential Grid stability services - EFR Source: National Grid UK

- 72. 11Delta Confidential Advanced inverter features- summary • Improved efficiency (>98,5%) • Country grid code compliance with new advanced features • Reactive power generation • Local utility customization still needed • Integration with smart grid environment • Virtual power plant integration to participate in energy exchange market • Most of top class inverters can deliver all required services

- 73. 12 About key drivers to future growth…

- 74. 13Delta Confidential Traditional grids vs. Smart Grids Traditional power grids: Centralized generation Limited power regulation Long distance transmission No influence on the power consumption No real time measurements Limited energy storage possibilities High risk of power outages Smart grids Distributed power generation Flexible power generation Short distance transmission Flexible load regulation Real time measurements (smart meters) Local energy storage Virtual Power Plants Low risk of power outages

- 75. 14Delta Confidential Key growth contributors Cheaper PV modules with proper efficiency (>20%) Energy storage Electric mobility Self consumption Smart grids and net zero energy buildings Smart inverter solutions

- 76. 15 How to provide increasingly "smart" inverters while reducing costs?

- 77. 16Delta Confidential RPI M50A • Integrated string fuses as well as • AC- and DC overvoltage protection Type II • Wide input voltage • Extended temperature range • High energy density, high efficiency, reduced size • 2 MPP trackers (symmetrical and asymmetrical load) • Integrated AC/DC disconnection switch

- 78. 17 Conclusions…

- 79. 18Delta Confidential Conclusions •PV market still growing but became global – different scenarios are taken into considerations •In some countries incentives dropped much faster than investment costs •PV industry got serious challenges – suppliers must diversify their business portfolio •More and more advanced features expected from inverters •PV inverter industry has to adapt for further growth

- 81. 20Delta Confidential 20 We are experts in power conversion

- 82. 21Delta Confidential 21 We are experts in power conversion… Power bricks Embedded Switching Power Supplies Rectifiers Inverters PV Inverters UPS Renewable Hybrid Solutions EV Ultra Fast Charger Wind converters Bi-directional converters

- 83. 22Delta Confidential We contribute to the Earth… 22 From 2010 to 2014, Delta’s high-efficient products enabled: Electricity Consumption Savings of 14.8 B KWh Carbon Emissions Reduction of 7.9 M Tons

- 84. Smarter. Greener. Together. To learn more about Delta, please visit www.deltaww.com

- 85. May 18th, Jan Van Laethem NEXT GENERATION OF SMART INVERTERS AND ASPECTS WITH RESPECT TO THE ENERGY TRANSITION SMA Solar Technology AGETIP PV - Photovoltaics: centre-stage in the power system

- 86. DISCLAIMER IMPORTANT LEGAL NOTICE This presentation does not constitute or form part of, and should not be construed as, an offer or invitation to subscribe for, underwrite or otherwise acquire, any securities of SMA Solar Technology AG (the "Company") or any present or future subsidiary of the Company (together with the Company, the "SMA Group") nor should it or any part of it form the basis of, or be relied upon in connection with, any contract to purchase or subscribe for any securities in the Company or any member of the SMA Group or commitment whatsoever. All information contained herein has been carefully prepared. Nevertheless, we do not guarantee its accuracy or completeness and nothing herein shall be construed to be a representation of such guarantee. The information contained in this presentation is subject to amendment, revision and updating. Certain statements contained in this presentation may be statements of future expectations and other forward-looking statements that are based on the management's current views and assumptions and involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those in such statements as a result of, among others, factors, changing business or other market conditions and the prospects for growth anticipated by the management of the Company. These and other factors could adversely affect the outcome and financial effects of the plans and events described herein. The Company does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You should not place undue reliance on forward-looking statements which speak only as of the date of this presentation. This presentation is for information purposes only and may not be further distributed or passed on to any party which is not the addressee of this presentation. No part of this presentation must be copied, reproduced or cited by the addressees hereof other than for the purpose for which it has been provided to the addressee. 2

- 87. NEXT GENERATION OF SMART INVERTER SYSTEMS AND ASPECTS WITH RESPECT TO THE ENERGY TRANSITION May 18th, Jan Van Laethem SMA Solar Technology AGETIP PV - Photovoltaics: centre-stage in the power system

- 88. SOLAR PV IS ON ITS WAY TO COMPETITIVENESS IN MORE AND MORE REGIONS AROUND THE WORLD 4 Atomic Power Plant Hinkley Point C in Somerset, UK PV Power Plant in Lackford, UK 1. Annual power production sufficient to supply c. 7.428.571 households with an average demand of 3.500 kWh 2. Annual power production sufficient to supply c. 5.762 households with an average demand of 3.500 hWh Construction time: c. 4–5 months, commissioned 2014 Operator: Low Carbon Power production p.a.: c. 20.168 MWh2 Electricity price per kWh: c. €0.09 ($0.10) Construction time: c. 10 years, to be commissioned 2025 Operator: Électricité de France (EdF) Power production p.a.: c. 26.000.000 MWh1 Electricity price per kWh: c. €0.12 ($0.13) In Germany‘s latest round of PV auctions in April 2016, €0.07 to €0.08 ($0.08 to $0.09) were granted to the bidders.

- 89. BUSINESS HAS BECOME MATURE 5 In 2010, focus was on DC to AC conversion in the best possible way. In 2016: Integration into complex systems is key. The energy market is in on the move. The energy transition is and will be a fundamental change. 2010 Installer business 2016 Systems and Project Business ETIP PV - Photovoltaics: centre-stage in the power system

- 90. BUT THE STRUGGLE REMAINS: POLITICAL DECISIONS CAN QUICKLY CHANGE A FRONTRUNNER‘S POSITION 6 In 2010, Germany had 45% of the world PV market. Today, Japan, China and the USA have taken over the pole position. 50 15 GWdc 20152010 To get back on top, Europe has to become the frontrunner again in the energy transition China Japan Germany USA ROW 45% 3% ETIP PV - Photovoltaics: centre-stage in the power system

- 91. 3 STEPS TO FACILITATE THE ENERGY TRANSITION 1.Source: EE-bus White Paper The Energy Transition (example: Germany) 1. STANDARDIZATION – being SMART about SMART HOME 2. Bring in more PV DRIVERS to ACCELERATE THE ENERGY TRANSITION 3. PROVIDE DATA SERVICES FOR GRID STABILITY and to SUPPORT the ENERGY TRANSITION ETIP PV - Photovoltaics: centre-stage in the power system

- 92. SMA IS THE CLEAR #1 IN THE GLOBAL PV INVERTER INDUSTRY 8 Key Facts Headquartered in Niestetal since 1981 Cum. nearly 50 GW installed worldwide Sales of 1 billion EUR in 2015 > 3,500 employees, thereof 500 in R&D Stock-listed since 2008 Present in 20 countries; 4 production sites ETIP PV - Photovoltaics: centre-stage in the power system

- 93. SMA’S COMPLETE PRODUCT PORTFOLIO OFFERS SOLUTIONS FOR ALL REQUIREMENTS WORLDWIDE 9 SMA’s cumulative installed power of nearly 50 GW is the basis for a successful service and storage business Utility Commercial Residential SUNNY CENTRAL SUNNY TRIPOWER SUNNY BOY Off-Grid & Storage Service O&M / WARRANTY EXTENSION 24 GW cumulative installed inverter capacity 13 GW 13 GW cumulative installed inverter capacity cumulative installed inverter capacity SUNNY BOY STORAGE SUNNY CENTRAL STORAGE SUNNY ISLAND

- 94. SMA POSITIONED ITSELF EARLY ON FOR THE DIGITIZATION OF THE ENERGY SECTOR 11 With innovations and partnerships, SMA is well-prepared for the new requirements Energy Management Storage Technology Data-based Business models Enhanced self- consumption through intelligent system technology Intelligent integration of (stationary) batteries into energy management Supply of power generation and consumption data + + TESLA DAIMLERSMA SMART HOME TenneT

- 95. 14.01.2016 TDR PGS PM Martin Volkmar SMA Solar Technology AG SMA SMART HOME

- 96. All devices interconnected in local network and via Internet cloud (IoT*) 13 WHAT IS THE MEANING OF SMART HOME? SMART HOME SMA Smart Home is a subset of the general definition of „Smart Home“ • Energy Monitoring • Energy Management • Smart Metering • HVAC control • Demand response access Home Automation Energy Efficiency Entertainment Systems Security (Peace of mind) Healthcare Systems *IoT = Internet of ThingsETIP PV - Photovoltaics: centre-stage in the power system

- 97. LOCAL ENERGY MANAGEMENT IN A SMART HOME 14 Sunny Boy Smart Energy converts direct into alternating current and buffers up to two kilowatt-hours of solar energy Sunny Home Manager ensures the temporally optimized balance of generation and consumption Sunny Places for energy forecasts, remote monitoring and household energy management Controllable loads, that do not require a specific operation time, can be activated by Sunny Home Manager Electric vehicle can be used as additional electricity storage when combined with a corresponding wallbox Thermal storages have big capacity and are more cost effective than a battery 1 3 2 4 5 6 3 1 45 2 6 Electrical and thermal storage combined with intelligent energy management is ideally suited to make distributed generation more flexible ETIP PV - Photovoltaics: centre-stage in the power system

- 98. Energy Management Basic Inverter System Sunny Home Manager System Integrated Storage System Flexible Storage System Sunny Boy Energy Management Inverter integrated battery PV inverter and battery inverter Only SunnyBoy PV inverter • “Natural” self consumption: 20% (typical) • Reduction of energy costs: 25% (typical) Sunny Home Manager + RC sockets • Self consumption: 45% (typical) • Reduction of energy costs : 45% (typical) SunnyBoy Smart Energy • Self consumption: 55% (typical) • Reduction of energy costs: 52% (typical) SunnyBoy + Sunny Island • Self consumption: 65% (typical) • Reduction of energy costs: 57% (typical) *) based on 5000kWh production per year *) based on 5000kWh production per year *) based on 5000kWh production and consumption per year, battery size: 2kWh *) based on 5000kWh production and consumption per year, battery size: 5kWh 15 SMA’S ENERGY MANAGEMENT AND STORAGE SOLUTIONS FOR OPTIMIZED SELF CONSUMPTION Increase the self-consumption rate = Use your own PV energy! ETIP PV - Photovoltaics: centre-stage in the power system

- 99. HOW MUCH POWER DOES MY HOUSE REQUIRE? … ENERGY MONITORING 16 FUNCTIONALITIES CUSTOMER BENEFIT Measure Always informed: • Total household consumption figure • Monitor and remote control of household appliances SMA Energy Meter Compatible RC-sockets Transparency and knowledge: • Where, when and how much energy does my house consume? • What did I consume in the last month? • Which devices are the ‘power hogs’in my house? Visualize Analyse and Control Suggestions to increase energy efficiency • Recommended actions, depending on energy prognosis • When is the best time to use my solar power? SMA Solar Technology AG SMA Smart Home - Energy Monitoring & Management

- 100. 18 ENERGY APPLIANCES CONNECTED … … AND NOW IT ALL WORKS TOGETHER! PARTNERS IN SMA SMART HOME (Ladestationen für Elektroautos) (Weissware)(Wärmepumpen) (Weissware via EEBUS (ab Q3 2016)) • Plug & Play • Easy does it ETIP PV - Photovoltaics: centre-stage in the power system

- 101. EEBus is an initiative to take energy management in the frame of Smart Homes from proprietary solutions (e.g. Sunny Home Manager with only Miele appliances) to a more generic level (like an Ethernet network, where any device can exchange information with other devices within the network independent from the manufacturer). 19ETIP PV - Photovoltaics: centre-stage in the power system

- 102. 20 www.eebus.org ETIP PV - Photovoltaics: centre-stage in the power system

- 103. 21 E-MOBILITY

- 104. PHOTOVOLTAICS AND E-MOBILITY ARE BEHIND SCHEDULE IN GERMANY (AND ELSEWHERE…) 23.05.2016 22 Both technologies are connected. E-mobility only makes sense if its energy originates from renewable sources Photovoltaics > Solar & Wind are main factors in energy transtion > 19,3 % of gross electricity production in 2015 > Since 2014 new installations behind plan E-cars > E-mobility is key for an ecological mobility transition > E-cars have a clearly lower CO2 footprint > Batteries solve the volatility of renewables in the Smart Grid Quelle: Fortschrittsbericht 2014, Nationale Plattform Elektromobilität, Berlin, Dezember 2014 Quelle: BSW: „Meldedaten PV Bundesnetzagentur 2014/2015“, Berlin, 1.2.2016 ETIP PV - Photovoltaics: centre-stage in the power system

- 105. VEHICLE-TO-GRID INTEGRATION 23 The first generation e-vehicles changes the car industry. The next generations will gradually change the energy transition. Utilization of the flexibility in buildings > E-vehicles connected to local EMS > „Green Area“ usables in a competitive way (in INEES about 30 %) > User settings and needs indfluence clearly the useful battery capacity Connecting buildings to the Markets > „Virtual Power Stations“ > Competitiveness strongly Regulation dependent > Many preconditions already fulfilled > Biggest obstacle: double use of the same communication network as cars *: VPP = Virtual Power Plant = Virtuelles Kraftwerk VPP* Märkte

- 106. SUPRA-REGIONAL ENERGY MANAGEMENT THROUGH AGGREGATION IN VIRTUAL POWER PLANTS • Distributed Energy Resources (DER) in current market not attractive for the energy industry • In future market design: aggregation in virtual power plants • Systems pooled in virtual power plants > provide flexibility out of generators, consumer loads and storage devices to Smart Grids > trade needed excess energy on Smart Markets Image: Vattenfall 25 Technology for a flexible, secure and cost-effective connection of DER is available ETIP PV - Photovoltaics: centre-stage in the power system

- 107. CHALLENGE FOR TRANSMISSION SYSTEM OPERATORS > Generation and consumption to be balanced at any time > Consumption predicted using standard load curves > Conventional generation scheduled according to predicted consumption and renewables generation > Renewables are volatile > Local energy management and storage tighten the situation > Schedule to reality deviations settled through expensive control power > Transmission System Operators (TSO) are responsible for the insertion of control power > They need near-time photovoltaic (PV) projections and forecasts based on measured data 26 Today no measuring network for small and medium size PV plants available Measuring network would have to be precise, secure and cost effective Mains frequency (50/60 Hz) Consumption Generation Damping through energy stored in generators and motors Load variations and forecast deviations Station blackout and forecast deviations Insertion of control power Image: TenneT TSO ETIP PV - Photovoltaics: centre-stage in the power system

- 108. DATA SUPPLY PILOT WITH TENNET TSO PROJECT OVERVIEW 30 40,000 monitored PV systems in German TenneT control area Thereof 20,000 PV systems with transmission every 5 minutes 1,500 PV systems with SensorBox Projections and forecasts Marketing of REL* electricity Reduction of control reserve need Congestion management Feed-in management validation Commercial balancing Asset management Every 5 minutes: 5 minute averages of the current PV power, irradiation and temperature aggregated to 5 digit ZIP codes REL = Renewable Energy Law (Germany) TenneT will considerably reduce the current projection delay ETIP PV - Photovoltaics: centre-stage in the power system

- 109. FURTHER DEVELOPMENT OF THE SMA ENERGY SERVICES 31 International rollout to regions with high PV penetration Measures to continuously enhance data quality and quantity ETIP PV - Photovoltaics: centre-stage in the power system

- 110. THE TIME HAS COME … … to support grid operation through near-time data out of distributed energy resources 32 … to connect e-vehicles and grid to support the energy transition … to standardize the way energy consumers and prosumers talk in a Smart Home ETIP PV - Photovoltaics: centre-stage in the power system

- 111. Thank you for your interest! Jan Van Laethem Regional Manager SMA Western Europe (Benelux, UK, France) SMA Solar Technology AG Sonnenallee 1, 34266 Niestetal, Germany +49 561 9522 0 Jan.VanLaethem@SMA-Benelux.com

- 113. Supporting Power Quality in Distribution Networks with Inverters Andreas Schlumberger / Thomas Schaupp – KACO new energy May 18th, 2016

- 114. Topics 1 Installed power today 2 Critical issues 3 Today’s solutions 4 Solutions in standardization CENELEC TS 50549 5 Looking ahead Andreas Schlumberger – KACO new energy May 18th, 2016 | 2

- 115. Topics 1 Installed power today 2 Critical issues 3 Today’s solutions 4 Solutions in standardization CENELEC TS 50549 5 Looking ahead Andreas Schlumberger – KACO new energy May 18th, 2016 | 3

- 116. Installed Power Today Integration of power into the German transport grid In mid 2016 - Approx. 40 GW PV power installed - Approx. 41 GW wind power installed The base load range significantly reduced Andreas Schlumberger – KACO new energy May 18th, 2016 | 4

- 117. Installed Power Today Andreas Schlumberger – KACO new energy May 18th, 2016 | 5

- 118. Installed Power Today Andreas Schlumberger – KACO new energy May 18th, 2016 | 6

- 119. Topics 1 Installed power today 2 Critical issues 3 Today’s solutions 4 Solutions in standardization CENELEC TS 50549 5 Looking ahead Andreas Schlumberger – KACO new energy May 18th, 2016 | 7

- 120. Critical Issues in the distribution grid Island formation Overload of equipment Voltage maintenance Andreas Schlumberger – KACO new energy May 18th, 2016 | 8

- 121. Voltage maintenance Excess voltage! Grid reinforcement necessary Andreas Schlumberger – KACO new energy PV P P P MV-Grid 20 kV Trafo 0,4 kV Line HAS 1 HAS 2 Load 1 Load 2 PV UL1 Distance P 3~ ~ 1.1 p.u. = 253 V 1.0 p.u. = 230 V high power production, low load no power production max. Load 0.9 p.u. = 207 V Transformer station May 18th, 2016 | 9

- 122. Critical Issues in the transport grid Balance between consumption and generation is necessary for frequency stability Imbalance results in frequency fluctuations Overload of equipment Sudden power drop in the GW range - resulting from frequency cut-off of distributed generation - Protective tripping in the event of short interruptions - System Split due to overloaded connections - Drop in power results in imbalance between generation and consumption Andreas Schlumberger – KACO new energy May 18th, 2016 | 10

- 123. Topics 1 Installed power today 2 Critical issues 3 Today’s solutions 4 Solutions in standardization CENELEC TS 50549 5 Looking ahead Andreas Schlumberger – KACO new energy May 18th, 2016 |

- 124. Today’s solutions Distribution System Voltage Support by reactive power Supply management (Curtailment) Island detection ( critical since contradicting power system stability) Transport System Power reduction in case of overfrequency Immunity to dips and swells Dynamic voltage support contribution to short circuit power Andreas Schlumberger – KACO new energy May 18th, 2016 | 12

- 125. Topics 1 Installed power today 2 Critical issues 3 Today’s solutions 4 Solutions in standardization CENELEC TS 50549 5 Looking ahead Andreas Schlumberger – KACO new energy May 18th, 2016 |

- 126. General assumption Standardization is required to write down state of the art Manufacturers require standardization to produce unified equipment for all countries Due to different network topology network operators have different needs to integrate dispersed generation - But the general problems are the same Andreas Schlumberger – KACO new energy May 18th, 2016 | 14

- 127. Solution Define standard behavior for dispersed generation Allow adjustment to local needs Analysis of system impact is very specific to the local topology of the grid excluded from scope Andreas Schlumberger – KACO new energy May 18th, 2016 | 15

- 128. Included topics Range of operation (not protection) Immunity to disturbance - Voltage dips - Rate of change of frequency Reactive power provision Standard control modes for reactive power Dynamic grid support Protection (voltage and frequency) Communication Andreas Schlumberger – KACO new energy May 18th, 2016 | 16

- 129. Standard range of Operation Voltage / Frequency Andreas Schlumberger – KACO new energy May 18th, 2016 | 17

- 130. Immunity to Disturbance Andreas Schlumberger – KACO new energy May 18th, 2016 | 18

- 131. Immunity to Disturbance Rate of change of Frequency – 2.5Hz/s no disconnection allowed For system stability it is mandatory that short disturbance does not lead to loss of generation Immunity is important Andreas Schlumberger – KACO new energy May 18th, 2016 | 19

- 132. Power Reduction in the Event of Overfrequency power reduction in the event of overfrequency Gradient 40% Pactual/Hz Response time as fast as possible, best below 2 seconds No automatic disconnection from the grid in the range of 47.5 Hz to 51.5 Hz Andreas Schlumberger – KACO new energy May 18th, 2016 | 20

- 133. Reactive Power Capability PD=P-Design, the maximum active power of the Plant where Qmax might be delivered Andreas Schlumberger – KACO new energy May 18th, 2016 | 23

- 134. Voltage Maintenance by means of reactive power supply Andreas Schlumberger – KACO new energy May 18th, 2016 | 24 PV P P P 20 kV Trafo 0,4 kV Line HAS 1 HAS 2 Load 1 Load 2 PV UL1 Distance P 3~ ~ 1.1 p.u. = 253 V 1.0 p.u. = 230 V High Power no load Max Load no Production 0.9 p.u. = 207 V Transformer Station Q Q as above but with reactive power consumption MV-Grid

- 135. Dynamic Grid Support with reactive Current Reactive current to feed into the grid fault (short circuit) eg. in transmission system Trigger line protection devices Increase voltage in case of remote fault Reduce region of impact Andreas Schlumberger – KACO new energy May 18th, 2016 | 25

- 136. Dynamic Grid Support with reactive Current Andreas Schlumberger – KACO new energy May 18th, 2016 | 26

- 137. Protection Available Protection Function Voltage - Over/Under-voltage Phase-Phase - Over/Under-voltage Phase-Neutral - Over/Under-voltage Positive/Negative/Zero sequence - Overvoltage Average values (eg. 10 min average RMS) Over/Under Frequency Line protection / overcurrent is considered mandatory in installation standards and is not included in TS50549 Andreas Schlumberger – KACO new energy May 18th, 2016 | 27

- 138. Topics 1 Installed power today 2 Critical issues 3 Today’s solutions 4 Solutions in standardization CENELEC TS 50549 5 Looking ahead Andreas Schlumberger – KACO new energy May 18th, 2016 |

- 139. Looking ahead The key question - Which technical features will a power system need to run stable with a penetration of 40% ... 60% ... 80% ... 100% of inverter-based power generation? - The instantaneous penetration of inverter based generation will vary during a day from 0% to 100% Features possibly necessary in the future - Provide power in negative sequence - Provide primary reserve - Provide inertia - New protection design - Black start capability Andreas Schlumberger – KACO new energy May 18th, 2016 | 29

- 140. So … How far can we go with inverters only? 100% inverter-based grid is possible - Already implemented in small scale, e.g. UPS, island grids - Research for large scale needed Andreas Schlumberger – KACO new energy May 18th, 2016 | 30

- 141. So … How can we minimize installation costs? Reduction in material costs for inverters and modules will continue Harmonization of requirements will reduce engineering costs - We’ve let go by the chance for harmonization in context of RfG, national implementation allows to many variations - The goal should be: Harmonization similar to Low Voltage Directive (2014/35/EU) or EMC-Directive (2014/30/EU) Connection procedure - a) Connection evaluation based on plant requires evaluation procedure for each plant including costs for each plant - b) Connection evaluation based on unit allows to type evaluation and faster / more cost effective connections - Some European countries use b) up to several MW plant size, some (GER) introduce a) above 100 kVA Andreas Schlumberger – KACO new energy May 18th, 2016 | 31

- 142. Thank for your attention. KACO new energy GmbH Carl-Zeiss-Str. 1 . 74172 Neckarsulm . Deutschland Fon +49 7132 3818 0 . Fax +49 7132 3818 703 info@kaco-newenergy.de . www.kaco-newenergy.com

- 143. Stability of the power system with converter-interfaced generation Moving from a system based on synchronous machines to a system based on inverters Marie-Sophie Debry, RTE

- 144. Introduction The decrease of inertia level is a subject that is currently under scrutiny: • Many studies and articles… • Possibility in the grid codes to require « synthetic inertia » from inverters In the next future, potentially very few synchronous machines connected to grids during certain seasons or certain hours of the day… From inertia to synchrony: • Going from a system driven by physical laws to a system driven by the controls of inverters • Power Electronics are fully controllable BUT they only do what is in their control system! • There is no natural behavior of inverters, this is very dependent on manufacturers.

- 145. Requirements “Inertia” is not a requirement but a possible solution! • Today’s system inertia is the consequence of the existence of large synchronous generators. Nobody ever defined the required level of inertia, which is only an uncontrolled by-product. • Emulating “synchronous generators with identical inertia” with inverter-based devices is technically possible but requires over-sized inverters. Requirement: stability at an acceptable cost • Acceptable level of stability for large transmission system while keeping costs under control • Stable operation of large transmission system should not depend on telecommunication system: we must keep something like “frequency” to synchronize inverters Still valid ? A priori, this relation is lost (linked to rotating masses equations). How to ensure that there will be no limitation of PE penetration into the grid? Check the viability of operation of a transmission grid with no synchronous machines and then add some of them!

- 146. Challenge: a grid-forming control strategy… Today inverters connected to the grid are “followers”: they measure the frequency and adapt their current injection to provide active/reactive power with the same frequency SG SG 50 Hz Synchronous machines create voltage waveforms with the same frequency. Converters measure the grid frequency. Converters provide active and reactive power at the measured frequency. What if there is nothing to “follow”? Inverters (at least some of them) need to be “grid forming”, they have to create the voltage waveform on their own.

- 147. … Taking into account the limitations of inverters Inverter over current limitation is very close to nominal capability (over current of 120% for 1 cycle) Solutions have already been developed for small isolated grids, but they are not applicable to large transmission systems which have specific features: - Meshed systems - Many operational topological changes - No knowledge of generation/load location - No master/slave relation

- 148. MIGRATE project Massive InteGRATion of power Electronic devices “MIGRATE aims at helping the pan-European transmission system to adjust progressively to the negative impacts resulting from the proliferation of power electronics onto the HVAC power system operations, with an emphasis on the power system dynamic stability, the relevance of existing protection schemes and the resulting degradation of power quality due to harmonics.” Coordinator: TenneT GmbH, 24 partners Duration 4 years (January 2016 – January 2019)

- 149. MIGRATE WP3: Control and operation of a large transmission system with 100% converter-based devices Objectives: • To propose and develop novel control and management rules for a transmission grid to which 100 % converter-based devices are connected while keeping the costs under control; • To check the viability of such new control and management rules within transmission grids to which some synchronous machines are connected; • To infer a set of requirement guidelines for converter-based generating units (grid codes), as far as possible set at the connection point and technology-agnostic, which ease the implementation of the above control and management rules.

- 150. « STORAGE SUPPORTING PV DEPLOYMENT » VERONICA BERMUDEZ EDF R&D / DPT. EFESE/ SOLAR TECHNOLOGIES REPOWERING EUROPE- 18 mai 2016

- 151. | 2 OUTLINE Photovoltaic market Photovoltaic market. Competivity?

- 152. | 3 SOLAR MARKET BRIEFLY - 10 20 30 40 50 60 70 80 90 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Supply - crystalline silicon Supply - thin-film silicon Supply - thin film non-silicon Demand - conservative Demand - optimistic Tier 1 module capacity 50.3GW Cell and module manufacturing capacity - at least 85GW Source: Bloomberg New Energy Finance Despite industry consolidation, the whole PV value chain is in oversupply and is expected to remain so until 2017

- 153. | 4 We observe 3 trypes of main photovoltaic applications, that can be (or not) grid connected. DISTRIBUTION OF PV MARKET Grid connected (but also self consuming Residential and commercial Most of installation Buildings Non- grid connected Isolated solutions, telcom antennaes, … A few % of installations. Isolated areas Grid connected Strong development where the land is available (e.g. USA, China, under transformation lands) ~36 % of installations Utility-scale Residential ≤10 kW Small Commercial 10.1-100 kW Medium Commercial 101 kW-1 MW Large Commercial 1.01 MW-5 MW Utility-Scale >5 MW Cumulative Demand by Segment 2015-2019 © 2015 IHSSource: IHS

- 154. | 5 TARGETS TO REDUCE COSTS OF PV 1. Reducing technology costs 2. Reducing grid integration costs 3. Accelerating deployment. 1. Reducing the levelized cost of electricity (LCOE) from solar PV 2. Enhancing system reliability 3. Enlarging the range of applications of PV 4. Establishing a recycling system. DOE: Sunshot (2020) target Utility-scale PV system US1$/WDC Commercial-scale PV system US1.25$/WDC Residential-scale PV system US1.5$/WDC LCOE (utility-scale system) US0.06$/WDC NEDO target year LCOE commercial-scale JPY14/kWh 2020 Module % and lifetime 22%, 25 yrs LCOE utility-scale JPY7/kWh 2030 Module % and lifetime 25%, 30yrs Technologies to support PV deployment

- 155. | 6 BUT, WHAT REALLY COST MEANS?. LCOE Source: Bloomberg New Energy Finance

- 156. | 7 Negative prices appear in the German bourse In Spain, prices are limited to 0 In California, the regulator has modified minimum prices from –30 $/MWh to –300 $/MWh. SPOT PRICE OF ELECTRICITY Costs of “fuel” CO2 cost Production means availability Hydraulic Wind Solar Temperature Daily, weekly, saison cycles Aleas Aleas Interconnection net busy Charge loadProduction load “Spot” Price

- 157. | 8 DISPATCHABILITY: BUT NOT ONLY 1. Storage of tens of seconds or a few minutes, to remove fluctuations due to cloud cover, if this is important for the electricity sales agreement or the grid connection agreement. 2. To provide ancillary services such as frequency response or reserve, if a market or a mandatory requirement exists. 3. Storage of a few hours, in order to time-shift production to times of the day when the price is higher. Electricity systems with a high penetration of PV already show a strong impact on spot prices.

- 158. | 9 Tomorrow : application of new technologies, diffuses or centralized, on board or static

- 159. | 10 …but also within the same sector: • Installations : specialised equipments (Hospitals, Swimming pools, …) • Electrical heating and/or climatization • Yearly occupancy: holydays • Building age • PV production capacity [kWh/m²] • Available roof surface The self-production/ self-consumption ratio varies as a fonction of the analysed sector : • Office • Cultural buildings • Educational buildings • Health related buildings • Sport centers • Hotels / restaurants Tier Sector : load profiled are very different from on building to another SELF-CONSUMING PV IN THE TIER RESIDENTIAL SECTOR

- 160. | 11 Cultural building: day/night out of phase Offices : Conso/production are syncronised Self-consuming ratio= 46 % Self-production ratio= 38 % Adding more PV modules will not cover the consumed power excess. Self-consuming ratio= 69 % Self-production ratio= 35 % Under consumation during WE. PV SELF-CONSUMPTION IN TIERS SECTOR

- 161. | 12 Educational building: impact of school holydays Offices : Climatization impact Offices : electrix heating impact Self-consuming ratio= 75 % Self-production ratio= 20 % Self-consuming ratio= 99 % Self-production ratio= 17 % Self-consuming ratio= 71 % Self-production ratio= 21 % PV SELF-CONSUMPTION IN TIERS SECTOR

- 162. | 13 Source : EDF R&D For a residential installation- without storage system, nor uses controller - the most we can expect to consume is 40% of our slef-produced electricity. The use of the grid will be necessary. PuissancePVproduitekW Lundi Mardi Mercredi Jeudi Vendredi Samedi Dimanche There are technical solutions that allow maximizing the ratio self- consumption/self-production : - Smart electrical control of buildings - Adding adapted storage solution. SELF-CONSUMPTION PV IN THE RESIDENTIAL SECTOR

- 163. | 14 PV SELF-CONSUMPTION STRONG IMPORTANCE For client: all kWh produced are not self-consumed: The promised « grid parity » is only theoretical if 100% of the production is not consumed…

- 164. | 15 Principle : Storage excess non consomed PV power in batteries. Multiple technological solutions in the market with limited performances, in particular in the load/unload strategies and the fitting wit loag management. SONNENBATTERIE SUNNY HOME MANAGER STORELIO POWERROUTER BOSCH V5 HYBRID SMART ENERGY SELF-CONSUMPTION PV « OPTIMISED » ADDING A STORAGE UNIT (BATTERIE,….)

- 165. | 16 CONCLUSIONS The increasing contribution of PV to the global and regional power mix has caused a number of fundamental challenges, which can largely be addressed by the addition of energy storage. PV electricity is produced only during the day; energy is often needed during the night. The ability to store energy during the day for use at night is beneficial. PV is an intermittent and unpredictable generation source. Storage allows fluctuations in supply to be reduced. Off-grid PV is not connected to the grid and therefore the only way to use electricity at night is through storage. The development of storage for PV is essential to increase the ability of PV systems to replace existing energy sources. Although introducing storage to grid-connected applications is a new development in the PV market, storage has been used in off-grid PV systems for some time. New products targeted at the PV industry, technology advances, and the availability of less expensive storage solutions, will lead to the increased use of energy storage in the PV industry. More storage solutions are becoming commercially available. They range from intelligent management systems which are coupled with a battery to large-scale turn- key solutions aimed at grid-scale applications.

- 166. | 17 Thank you

- 167. Impact of storage on PV attractiveness Mariska de Wild-Scholten Repowering Europe, 'Photovoltaics: centre-stage in the power system', 18 May 2016, Brussels

- 168. Outline How does storage affect the environmental balance of PV? Life Cycle Assessment Greenhouse gas emissions Toxicity Depletion 2

- 169. Mismatch of generation & consumption of electricity 3 Martin Braun 2009 EPVSEC24 4BO.11.2

- 170. Why storage @ home? 4 Storage to increase self- sufficiency Storage to increase self- consumption High grid electricity price?

- 171. Storage System 5 Module with battery cells ............... this presentation Energy management system Inverter Etcetera

- 172. Which battery type? 6http://www.estquality.com/technology Li-ion = dominating battery type for PV home applications

- 173. Battery technology comparison 7 Aquion Energy Li-ion = dominating battery type for PV home applications

- 174. Calculation of carbon footprint of stored electricity in life time of battery Global Warming Potential (GWP) of stored electricity g CO2-eq/kWh GWP (g CO2-eq) / kg battery .............................step 1 x Battery weight (kg) / usable capacity of battery (kWh) ....................step 2 / number of charge cycles .................................step 3 8

- 175. Global Warming Potential (GWP) of battery with LMO: Lithium Manganese Oxide (LiMn2O4) 9ecoinvent 2.2, calculated with IPCC2013 GWP100a method GWP = 5.89 kg CO2-eq/kg battery cell using IPCC2007 GWP100a

- 176. Global Warming Potential (GWP) of battery with LMO: Lithium Manganese Oxide (LiMn2O4) 10ecoinvent 2.2, calculated with IPCC2013 GWP100a method GWP = 5.39 kg CO2-eq/kg battery using IPCC2007 GWP100a Single cell, lithium-ion battery, lithium manganese oxide/graphite, at plant/CN U Unit Value % IPCC2013 GWP100a % kg CO2-eq/kg 1.050 100.0% 5.390 100.0% Transport, freight, rail/RER U tkm 0.167 6.63E-03 0.1% Transport, lorry >16t, fleet average/RER U tkm 0.028 3.73E-03 0.1% Chemical plant, organics/RER/I U p 0.000 4.97E-02 0.9% Electricity, medium voltage, at grid/CN U kWh 0.106 1.28E-01 2.4% Heat, natural gas, at industrial furnace >100kW/RER U MJ 0.065 4.73E-03 0.1% Inert atmosphere: Nitrogen, liquid, at plant/RER U kg 0.010 4.37E-03 0.1% Electrolyte salt: LiPF6 Lithium hexafluorophosphate, at plant/CN U kg 0.019 1.8% 4.75E-01 8.8% Electrolyte solvent: Ethylene carbonate Ethylene carbonate, at plant/CN U kg 0.160 15.2% 2.35E-01 4.4% Separator: Coated polyethylene film Separator, lithium-ion battery, at plant/CN U kg 0.054 5.1% 3.23E-01 6.0% Cathode: LiMn2O4 Cathode, lithium-ion battery, lithium manganese oxide, at plant/CN Ukg 0.327 31.1% 2.68E+00 49.7% Anode: Graphite Anode, lithium-ion battery, graphite, at plant/CN U kg 0.401 38.2% 1.04E+00 19.3% Electrode tab: Al Aluminium, production mix, wrought alloy, at plant/RER U kg 0.016 1.6% 1.80E-01 3.3% Package: Polyethylene Polyethylene, LDPE, granulate, at plant/RER U kg 0.073 7.0% 1.60E-01 3.0% Processing: Processing of input materials: Extrusion, plastic film/RER U kg 0.073 3.87E-02 0.7% Sheet rolling, aluminium/RER U kg 0.016 1.00E-02 0.2% Emissions to air: Heat, waste MJ 0.380 Waste to treatment: Ecoinvent assumption 5% Disposal, Li-ions batteries, mixed technology/GLO U kg 0.053 4.91E-02 0.9%

- 177. Global Warming Potential (GWP) of battery with LFP: Lithium Iron Phosphate (LiFePO4) 11 Hiremath (March 2014) Master Thesis Carl von Ossietzky University of Oldenburg, Germany GWP = 11.2 kg CO2-eq/kg using IPCC2007 GWP100a

- 178. Number of cycles depend on depth of discharge 12Saft

- 179. Carbon footprint of stored electricity Lowest value from my preliminary analysis: 12 g CO2-eq/kWh stored electricity How much kWh storage needed / kWh generated? 13

- 180. Carbon footprint - gram CO2-eq/kWh hydropower / UCTE 0 10 20 30 40 50 mono-Si multi-Si a-Si μm-Si CdTe CIGS 2011 2011 2008-2011 2013 estimate 2010-2011 2011 14.8% 14.1% 7.0% 10.0% 11.9% 11.7% 33-45 MWp 120 MWp 963 MWp 20-66 MWp Carbonfootprint (gCO2-eq/kWh) poly-Si: hydropower wafer/cell/module: UCTE electricity glass-based modules %: total area module efficiencies ecoinvent 2.2 database 25 August 2013 mariska@smartgreenscans.nl on-roof installation in Southern Europe 1700 kWh/m2.yr irradiation on optimally-inclined modules inverter mounting + cabling frame laminate cell ingot/crystal + wafer Si feedstock China electricity mix 14 0 10 20 30 40 50 60 70 80 90 100 mono-Si mono-Si multi-Si multi-Si 2011 2011 2011 2011 14.8% 14.8% 14.1% 14.1% hydro/UCTE China/China hydro/UCTE China/China Carbonfootprint (gCO2-eq/kWh) poly-Si: hydropower/CN wafer/cell/module: UCTE /CNelectricity glass-based modules %: total area module efficiencies ecoinvent 2.2 database 25 August 2013 mariska@smartgreenscans.nl on-roof installation in Southern Europe 1700 kWh/m2.yr irradiation on optimally-inclined modules inverter mounting + cabling frame laminate cell ingot/crystal + wafer Si feedstock CN CN mono multi Status of inventory data 2011 World average carbon footprint ≈ 55 g CO2-eq/kWh

- 181. Many uncertainties GWP value based on 2010 or older inventory data of the battery Reliable manufacturer data missing Number of charging cycles depend on depth of discharge Only battery calculated, not a complete storage system How much storage is needed / kWh electricity generated from PV? 15

- 182. Toxicity N-methyl-2-pyrrolidone (NMP) solvent in electrolyte Alternative: Water based is not possible because some electrodes are moisture sensitive Alternative: Electrovaya SuperPolymer® 2.0 Polyvinylidene fluoride-based binders in electrolyte Replace with chlorine 16

- 183. Critical Raw Materials: cobalt 17 Cobalt in LiCoO2 cathodeLithium

- 184. Depletion of materials Cobalt in LiCoO2 electrode replace Co with Mn, Fe, Ti LiFePO4 Lithium Titanate (Li4Ti5O12) Lithium replacement with Na, Ka, Mg, Ca... recycling 18

- 185. Cradle to cradle battery Aquion Energy 19 NaSO4 solution (AHI™)

- 186. Recommendations To get a reliable evaluation of the environmental impact of current storage systems it is recommended that LCA studies are performed with data collected by manufacturers of Battery Storage Systems, in EU / National projects. 20

- 187. References / Funding References: D. Larcher, J-M. Tarascon (2014) Towards greener and more sustainable batteries for electrical energy storage, Nature Chemistry 7: 19-29 PV Magazine Storage Special July 2015 with Market Survey of Batteries Funding: none 21

- 188. Thank you for your attention! mariska@smartgreenscans.nl La Duna, Casas Bioclimáticas ITER, Tenerife

- 189. STORAGE MARKET DEVELOPMENT AND PRICE ROADMAP Repowering Europe May 2016 | Marion PERRIN

- 190. | 2 • Need for electricity storage: applications • Market evolution • Present prices • Storage learning curve / Price roadmap • European storage? AGENDA LITEN Days 2015 | Marion PERRIN

- 191. | 3 STORAGE STILL THE LAST FLEXIBILITY OPTION?

- 192. | 4 Need for storage: scenario ADEME 100% renewables FR 2050

- 193. | 5 Need for storage: scenario Germany 100% renewables 2050

- 194. | 6 Concordant / non concordant conclusions NO NEED OF STORAGE FOR THE ELECTRICAL SYSTEM IN THE SHORT TERM • Long term storage (e.g. power to gas) only needed with RE shares higher than 70 to 80% FR • First need is weekly storage • From 40% share on, need of intraday storage • At 80% RE, 8GW weekly, 7GW short term storage needed • The focus is put on « distribution grid support » (hundreds of kW/kWh) • water heaters represent a 13 to 20 TWh intra-day flexibility DE • First need is on short term storage (frequency regulation) • At 80% RE, 5GW weekly, 7GW short term storage needed • Focus is put on larger scale storage (MW) for frequency regulation and on residential storage for PV self- consumption

- 195. | 7 • Need for electricity storage: applications • Market evolution • Present prices • Storage learning curve • European storage? AGENDA LITEN Days 2015 | Marion PERRIN

- 196. | 8 Market in MWh

- 197. | 9 Market in $

- 198. | 10 What is the optimal management ? Use profile Performances begining of life Performances during operation MULTIPLE TECHNOLOGIES FOR PV STORAGE ? Which technology to select for my application ?

- 199. | 11 What about the residential PV + battery market?

- 200. | 13 • ”IMS Research predicts that energy storage sales will jump from only $200 million in 2012 to a massive $19 billion as early as 2017.” • California Public Utility Commission (CPUC) in its Sept. 3 2013 proposed decision on energy storage…mandated 1.3 GW of energy storage into the grid by 2020. ENERGY STORAGE MARKET FORECAST

- 201. | 14 • Need for electricity storage: applications • Market evolution • Present prices • Storage learning curve • European storage? AGENDA LITEN Days 2015 | Marion PERRIN

- 202. | 15 • NMC « low-cost » : less than 1.5€ for one 18650 (2x3.6=7.2Wh) => 200€/kWh • NCA : 2.8€ (3.1x3.65=11.3Wh) => 250€/kWh • LFP base 26650 : less than 3€ (3x3.2= 9.6Wh) => 300€/kWh • LTO no price for volumes, pas de prix sur les volumes, sampling of 18650 at 3.4€ (1x1.8=1.8Wh) => 1900€/kWh End of 2015 on small cells LI-ION COST AT CELL LEVEL 18650 - 26650

- 203. | 16 Retail price of residential PV storage system

- 204. | 17 • Need for electricity storage: applications • Market evolution • Present prices • Storage learning curve • European storage? AGENDA LITEN Days 2015 | Marion PERRIN

- 205. | 18 LEARNING CURVE OF LI-ION 15% cost decrease for each doubling of the installed capacity 100€/kWh once 1TWh reached Possible in 2030 provided market growth of 31% per year Source Winfried Hoffmann 2014

- 206. | 19 How cheap can Li-ion become?

- 207. | 20 • Need for electricity storage: applications • Market evolution • Present prices • Storage learning curve • European storage? AGENDA LITEN Days 2015 | Marion PERRIN

- 208. | 21 Where do Li-ion batteries come from?

- 209. | 22 GOOD NEWS FOR PV STORAGE?

- 210. | 23 Conclusions Storage is one of the flexibility options for grid integration of renewables Expected growth of the market until 2025 according to Avicenne + 4% for lead-acid + 10 % for Li-ion in vehicles + 11% for Li-ion in “energy storage” => 2 major technologies with lead- acid still dominating in 2025

- 212. siemens.com 18 May, 2016 The virtual battery: energy management in buildings and neighbourhoods

- 213. Siemens focuses on electrification, automation and digitalization – and is actively supporting Smart City/Neighbourhood development Digital transformation Digitalization Globalization Automation Urbanization Demographic change Climate change Electrification Power and Gas Wind Power and Renewables Mobility Digital Factory Process Industries and Drives Healthcare Enablers • Sensors • Computing power • Storage capacities • Data analytics • Networking ability TODAY Energy Management Building Technologies

- 214. Digital Grid Ahead of the challenge, ahead of the change

- 215. The energy systems are changing dramatically

- 216. From monopoly power …

- 217. From monopoly power …… to deregulated markets.

- 218. From downstream power delivery …

- 219. From downstream power delivery …… to smart distribution and bidirectional power flows.

- 220. From top-down topologies …

- 221. From top-down topologies …… to autonomous local structures.

- 222. From predictable long-term value streams …

- 223. From predictable long-term value streams …… to versatile, value-based transactions.

- 224. Germany: Energiewende 2.0 – Future energy systems: Decoupling of generation and consumption Past Production follows consumption Today Consumption vs. production Future Production decoupled from consumption 500 MW 0 MW -500 MW 250 MW -250 MW 80% share of renewable energy in 2035+ ‒ 2035+: Installed capacity of renewable energy systems: >220 GW ‒ Electrical energy produced: 446 TWh ‒ Electricity generation is occasionally 2.4 times higher than maximum consumption! ‒ Excess energy in northern states of Germany ‒ More than 7,000 MW for over 3,000 hours per year ‒ Grid stability is the highest priority Reducing uncertainties is a major challenge for research and development!

- 225. Digitalization enables you to turn challenges into opportunities Digital services Vertical software Digitally enhanced electrification and automation Challenges Digitalization with Siemens delivers answers ALERT! Balancing Peak avoidance Resilience Business models CO2 and cost avoidance Loss prevention Distributed optimization Customer focus

- 226. Siemens Digital Grid masterplan architecture for a smooth transition to agility in energy CIM – Common Information Model (IEC 61970) Enterprise IT IVR GIS Network planning Asset management WMS/mobile Weather Forecasting Web portals CIS/CRM Billing Enterprise Service Bus Cloud enabled applications Public cloud Smart communication Gridcybersecurity Managed/cloudservices OT-ITintegration,consulting Smart transmission Smart distribution Smart consumption and microgrids Smart distributed energy systems Smart markets $ €₹ Business applicationsGrid control applicationsGrid planning and simulation CIM CIM

- 227. Siemens.com/answers Intelligent Compact Substations for a Smarter Grid - The modular concept out of one hand

- 228. Web of Systems for distributed autonomous control – Example: The Intelligent Secondary Substation in a Smart Grid + Minimized engineering effort Plug-and-Play capabilities, remote software update and feature enhancements, asset monitoring + Reliable system operation at lower cost Supervised autonomous local control enables reliable and stable smart grid operation while making use of internet connections to an operation center which are highly cost efficient but have lower quality of service Internet Dramatic change of power flow in substations 2003 today SensorsStep-Trafo Feeders Smart Networked Device Controller Intelligent Secondary Substation Control Center

- 229. The modular energy storage system for a reliable power supply SIESTORAGE

- 230. Energy storage technologies and application areas Electrical storage Mechanical storage Electrochemical storage Chemical storage Source: Study by DNK/WEC “Energie für Deutschland 2011“, Bloomberg – Energy Storage technologies Q2 2011 CAES – Compressed Air Energy Storage 1 kW 10 kW 100 kW 1 MW 10 MW 100 MW 1,000 MW Dual film capacitor Superconductor coil MinutesSecondsHoursDays/months Li-ion NaS batteries Redox flow batteries H2 / methane storage (stationary) Diabatic adiabatic CAES Water pumped storage TechnologyFlywheel energy storage SIESTORAGE Time in use • Know-how in different battery technologies and chemistries • Designed for the use of various battery suppliers • Technical data depending on supplier • Maximum savings through optimized plant operation