Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

En vedette (20)

Similaire à Is Break-Even Analysis Useful? Understanding the Pros and Cons

Similaire à Is Break-Even Analysis Useful? Understanding the Pros and Cons (20)

Plus de Patrick Rubix

Plus de Patrick Rubix (18)

Dernier

Dernier (20)

Is Break-Even Analysis Useful? Understanding the Pros and Cons

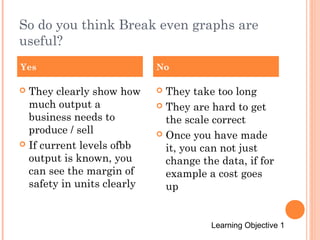

- 1. So do you think Break even graphs are useful? Yes No They clearly show how much output a business needs to produce / sell If current levels ofbb output is known, you can see the margin of safety in units clearly They take too long They are hard to get the scale correct Once you have made it, you can not just change the data, if for example a cost goes up Learning Objective 1

- 2. ESF Year 11 IGCSE BREAK – EVEN ANALYSIS CONTRIBUTION METHOD MR AHERN

- 3. Learning Objectives Recap and analyse the use of break even charts as a tool Introduce Break Even contribution method Calculate break even through contribution method Complete break even scenario tasks by using contribution method

- 4. CALCULATING THE BREAK – EVEN POINT There are two ways to calculate the break-even point. You have just demonstrated your competence by producing break-even chart, I’ll see how good they are over the weekend. I will want to collect your books at the end of the lesson But there is also another way….. The contribution method

- 5. Advantages to the method Contribution Quite simply its quicker than producing a graph If companies sell lots of different products and have lots of different processes internally such as ford, it would take up a lot of managers time to produce a graph every time the supplier price, demand or production quantity changed. Time is money, and manager time is not cheap, think about it, it could possibly effect the fixed cost of the product. Making it more expensive, and in turn less competitive

- 6. Disadvantages of the contribution method Limited data. Only displays one point, no future inclinations. Only determines output in units needed to break-even Doesn’t demonstrate margin of safety When altering price, or possibilities of change in variable costs, this is demonstrated a lot less clearly.

- 7. Contribution Essentially the difference between revenue (sales) and variable costs. For example if a jumper sells at £45 (revenue) and it costs £12 for the material and £8 for the logos and designs the variable costs of the jumper would be £20. The contribution per unit would be £25 £45 revenue - £20 = £25 - V.C. = contribution

- 8. Contribution Method (per unit) This involves a two part calculation: Revenue (selling price) per unit – variable cost per unit = contribution (towards fixed costs). AND Fixed costs / contribution = break-even point. Learning Objective 2

- 9. Learning Objectives Recap and analyse the use of break even charts as a tool Introduce Break Even contribution method Calculate break even through contribution method Complete break even scenario tasks by using contribution method

- 10. Example If fixed costs = £5000, variable costs = £12 per unit, selling Price per unit =£20. Then break-even would be: Price per unit – variable cost per unit = contribution (towards fixed costs). £20 - £12 = £8 (contribution, towards fixed costs) Fixed costs / contribution = break-even point. £5000 / 8 = 625 625 products will need to be sold in order to breakeven and cover all their costs.

- 11. Task Dave has set up a business to print T-shirts. The fixed costs of premises and the T-shirt printers are £6000. The variable costs per T-shirt (the Tshirt, ink, wages) are £10. Each printed T-shirt sells for £25. NOW YOU TRY!

- 12. Task Answer Dave has set up a business to print T-shirts. The fixed costs of premises and the T-shirt printers are £6000. The variable costs per T-shirt (the T-shirt, ink, wages) are £10. Each printed Tshirt sells for £25. Revenue per unit – Variable Cost Per Unit = Contribution £25 - £10 = £15 (Contribution per unit) Fixed Costs / Contribution per unit = Break-even Point. £6000 / 15 = 400 Dave must sell 400 T-shirts to brake even

- 13. Task 2 Tina starts a business making and selling shoes and has the following costs: Fixed Costs Variable Costs Selling Price £80,000 per year £25 per pair £75 pair Calculate the break-even point?

- 14. Answer Revenue – Variable Cost = Contribution £75- £25 = £50 (Contribution) Fixed Costs / Contribution = Break-even Point. £80,000 / £50 = 1600 Tina has to sell 1600 pairs of shoes to brake even.

- 15. Task 1 Revenue Variable Costs Fixed costs Item 1 30 18 15,000 Item 2 120 65 95,700 Item 3 315 206 192,712 Item 4 22 19 22,554 Item 5 25.00 12.50 3,750 Item 6 11.50 6.12 3,228 Item 7 116.25 51.16 32,550 Contributi on Break-even (Units)

- 16. Learning Objectives Recap and analyse the use of break even charts as a tool Introduce Break Even contribution method Calculate break even through contribution method Complete break even scenario tasks by using contribution method for next lesson

- 17. OK You have task 2 (the scenarios) First thing to do here is work out what is a FC what is a VC and what is R (revenue) You can get the answers to this in your book After doing that you should find the task relatively easy, well at least to start with I want to see at least the first one completed today and the rest handed in next lesson

- 18. Feedback time I will give you a post-it Please stick them on the board on your way out with any comments you have for me You do not need to put your name on these And if you leave it blank you can put it at the top of the board if you enjoyed the lesson, and the bottom of the board if you did not. If you find it hard please let me know