MGT101 - Financial Accounting- Lecture 34

•Télécharger en tant que PPT, PDF•

0 j'aime•519 vues

Virtual University Course MGT101 - Financial Accounting Lecture No 34 Instructor's Name: Mr. Mujahid Eshai Course Email: mgt101@vu.edu.pk

Recommandé

Contenu connexe

Tendances

Tendances (17)

En vedette

En vedette (20)

Similaire à MGT101 - Financial Accounting- Lecture 34

Similaire à MGT101 - Financial Accounting- Lecture 34 (20)

Plus de Bilal Ahmed

Plus de Bilal Ahmed (20)

Dernier

Dernier (20)

MGT101 - Financial Accounting- Lecture 34

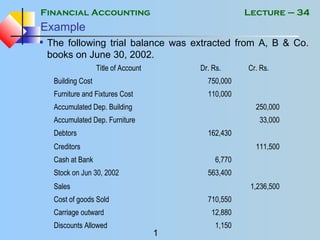

- 1. Financial Accounting 1 Lecture – 34 Example • The following trial balance was extracted from A, B & Co. books on June 30, 2002. Title of Account Dr. Rs. Cr. Rs. Building Cost 750,000 Furniture and Fixtures Cost 110,000 Accumulated Dep. Building 250,000 Accumulated Dep. Furniture 33,000 Debtors 162,430 Creditors 111,500 Cash at Bank 6,770 Stock on Jun 30, 2002 563,400 Sales 1,236,500 Cost of goods Sold 710,550 Carriage outward 12,880 Discounts Allowed 1,150

- 2. Financial Accounting 2 Lecture – 34 Example Title of Account Dr. Rs. Cr. Rs. Markup on Bank Loan 40,000 Office Expenses 24,160 Salaries and Wages 189,170 Bad Debts 5,030 Provision for Bad Debts 4,000 Bank Loan (Long Term) 400,000 Capital – A 350,000 B 295,000 Current Account – A 13,060 B 2,980 Drawings – A 64,000 B 56,500 2,696,040 2,696,040

- 3. Financial Accounting 3 Lecture – 34 Example Notes: • Expenses to be accrued, Office Expenses Rs. 960, Wages Rs.2,000. • Depreciate Fixtures 10% and Building 5% on straight line. • Reduce provision for doubtful debts to Rs. 3,200 • Partnership salary of A Rs. 8,000 is to be accrued. • A and B share profit and loss equally.

- 4. Financial Accounting 4 Lecture – 34 Solution A, B, & Co Profit and Loss Account for the Year Ending June 30, 20-2 Particulars Note Rs. Rs. Sales Less: Cost of Goods Sold (material consumed) 1,236,500 (710,550) Gross Profit Less: Expenses Wages and Salaries 1 Office Expenses 2 Carriage Out Discount Allowed Markup on Loan Provision for Doubtful Debt 3 Depreciation 4 191,170 25,120 12,880 1,150 40,000 4,230 48,500 525,950 (323,050) Net Profit 202,900

- 5. Financial Accounting 5 Lecture – 34 Solution A, B, & Co Profit and Loss Account for the Year Ending June 30, 20-2 Particulars Note Rs. Rs. Sales Less: Cost of Goods Sold (material consumed) 1,236,500 (710,550) Gross Profit Less: Expenses Wages and Salaries 1 Office Expenses 2 Carriage Out Discount Allowed Markup on Loan Bad Debts Provision for Doubtful Debts not required 3(a) Depreciation 4 191,170 25,120 12,880 1,150 40,000 5,030 (800) 48,500 525,950 (323,050) Net Profit 202,900

- 6. Financial Accounting 6 Lecture – 34 Solution A, B, & Co Profit Distribution Account Particulars Note Rs. Rs. Net Profit Less: Partner’s Salary – A 202,900 (8,000) Distributable Profit Less: Partner’s Share in Profit A (50% of 194,900) B (50% of 194,900) 97,450 97,450 194,900 (194,900) 0

- 7. Financial Accounting 7 Lecture – 34 Solution A, B, & Co Balance Sheet As At June 30, 2002 Particulars Note Amount Rs. Amount Rs. Fixed Assets at WDV 4 Current Assets 5 Current Liabilities 6 729,400 (114,460) 528,500 Working Capital 614,940 614,940 Total 1,143,440 Financed By: Capital – A B 350,000 295,000 645,000 Current Account – A 7 B 8 54,510 43,930 98,440 Long Term Loan 400,000 Total 1,143,440

- 8. Financial Accounting 8 Lecture – 34 Solution • Notes • (1) Salaries • (2) Office Expenses Salaries and Wages Debit side. Paid 189,170 Payable 2,000 Credit side. Bal. 191,170 Office Exp. Debit side. Paid 24,160 Payable 960 Credit side. Balance 25,120

- 9. Financial Accounting 9 Lecture – 34 Solution • Notes • (3) Provision for Doubtful Debts Provision Debit side. B. Debt 5,030 Balance 3,200 Credit side. O/B 4,000 P&L A/c 4,230

- 10. Financial Accounting 10 Lecture – 34 Solution • Notes • (3-a) Provision for Doubtful Debts (4) Acc. Dep. WDV Cost Rate Opening For the Yr Closing Building 750,000 5% 250,000 37,500 287,500 462,500 Furniture 110,000 10% 33,000 11,000 44,000 66,000 48,500 528,500 Provision Debit side. Prov. not required 800 Balance 3,200 Credit side. O/B 4,000

- 11. Financial Accounting 11 Lecture – 34 Solution • Notes • (5) Current Assets Stocks 563,400 Debtors 162,430 Less: Provision (note3) 3,200 159,230 Bank 6,770 729,400 • (6) Current Liabilities Creditors 111,500 Exp. Payable: Salaries 2,000 Off. Exp 960 2,960 114,460

- 12. Financial Accounting 12 Lecture – 34 Solution • Notes • (7) A’s current Account • (8) B’s Current Account A’s Current A/c Debit side. Drawing 64,000 Balance 54,510 Credit side. O/B 13,060 Profit 97,450 Salary 8,000 B’s Current A/c Debit side. Drawing 56,500 Balance 43,930 Credit side. O/B 2,980 Profit 97,450

- 13. Financial Accounting 13 Lecture – 34 Presentation of Partners’ Accounts Partners’ Capital Account Dr. Side Cr. Side A B A B Bal. On Jul 01 350,000 295,000 Bal. June 30 350,000 295,000

- 14. Financial Accounting 14 Lecture – 34 Presentation of Partners’ Accounts Partners’ Current Account Dr. Side Cr. Side A B A B Drawings 64,000 56,500 Bal. On Jul 01 13,060 2,980 Salary 8,000 Share of Profit 97,450 97,450 Bal. June 30 54,510 43,930