3 Keys to Operating an Exceptional Bank

•Download as PPTX, PDF•

14 likes•7,862 views

In order to maximize long-term returns, a bank must operate efficiently and balance revenue growth against robust risk management.

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

3 Keys to Operating an Exceptional Bank

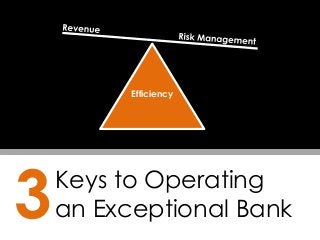

- 1. Keys to Operating an Exceptional Bank Efficiency 3

- 2. There are three interrelated challenges to operating an exceptional bank:a (1) revenue growth, (2) robust risk management, and (3) efficiency. (1) (2) (3) Efficiency

- 3. The first two, revenue growth and risk management, work against each other, as the fastest way for a bank to increase revenue is to lower credit standards. This allows a bank to write more loans, but exposes it to higher credit risk down the road. Efficiency

- 4. Efficiency Revenue Risk Management A bank accordingly must balance these two imperatives, generating enough revenue in the short-run to meet profitability targets (usually an ROE of 10% or more) w/out jeopardizing profitability over a longer stretch, during which the credit cycle is likely to turn down. =

- 5. Banks can make this balancing act easier by keeping operating costs low. This is captured by the efficiency ratio, which reflects the percentage of a bank’s net revenue that’s consumed by expenses. Efficiency

- 6. Because a bank with a low efficiency ratio presumably has a higher profit margin than its less efficient peers, it can afford to compete more aggressively for the most creditworthy borrowers. As such, efficient banks are able to reduce credit risk and dial up revenue growth. Efficiency

- 7. Thus, if there’s one thing bankers and bank investors should keep at the forefront of their minds, it’s the importance of a low efficiency ratio. As the diagram illustrates, this serves as the foundation upon which exceptional banks are built. Efficiency

- 8. Looking for more information like this? The Motley Fool’s mission is to help the world invest better. We’ve done this over the past 20 years by thinking long term and outside the box – even if that means turning Wall Street on its head. To learn more about what The Motley Fool thinks about current investment trends, and receive a special free report about what might be the next big industry to come out of Silicon Valley, just click here now.