Conventional vs FHA Loans Guide

•Télécharger en tant que PPT, PDF•

0 j'aime•298 vues

Performance School of Real Estate FHA CA Class

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Conventional vs FHA Loans Guide

Similaire à Conventional vs FHA Loans Guide (20)

Plus de JTtheCoach.com

Plus de JTtheCoach.com (7)

Dernier

Dernier (20)

Conventional vs FHA Loans Guide

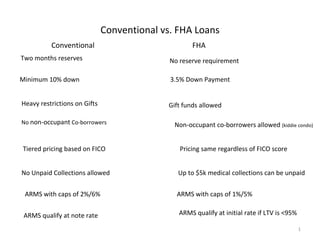

- 1. Conventional vs. FHA Loans Conventional FHA No reserve requirement Two months reserves Minimum 10% down 3.5% Down Payment Heavy restrictions on Gifts Gift funds allowed No non-occupant Co-borrowers Non-occupant co-borrowers allowed (kiddie condo) Tiered pricing based on FICO Pricing same regardless of FICO score No Unpaid Collections allowed Up to $5k medical collections can be unpaid ARMS with caps of 2%/6% ARMS with caps of 1%/5% ARMS qualify at note rate ARMS qualify at initial rate if LTV is <95%

- 2. Conventional vs. FHA Loans Conventional FHA Private MI required (over 80% LTV) Government insured Must have DU/LP approval Loan can be manually approved 2 years after Chapter 7 4 years out of Chapter 7 2 yrs. after payoff on Chapter 13 1 yr. of on-time payments after Chapter 13 7 yrs. after Foreclosure 3 yrs. After Foreclosure

- 4. FHA Flexible Credit Guidelines Minimum FICO score is 640 * Minimum time after a Chapter 7 Bankruptcy is 2 years (12 Mos minimum with extenuating circumstances-see below) Minimum time period after a Chapter 13 bankruptcy is one year from creditor settlement date with proof of on time payments for that year On Short Sale, it is possible to purchase a home one day after closing* If little credit history is available, alternative credit can be used. Payments on items such a car insurance, Utility bills or Cell phones can be used to create the credit required Minimum time period after a foreclosure is 3 years, unless extenuating circumstances: Death of wage earner Serious Illness Consumer Credit Counseling –must have paid payments on time for 12 mo. *In some exceptional cases, a score lower than 640 may be acceptable

- 5. Condominiums 234 (c ) Subdivision must be FHA approved Spot approval no longer available Do NOT trust MLS data-verify approval with Amerifirst LO

- 7. Appraisal Valuation Conditions These Valuation Conditions and protocol help the appraiser evaluate the standards required by the General Acceptability Criteria. The criteria are described below. It is helpful & facilitates the process if the following items are addressed prior to the appraiser viewing the property.