GUWAHATI 💋 Call Girl 9827461493 Call Girls in Escort service book now

Chapter 11 first half

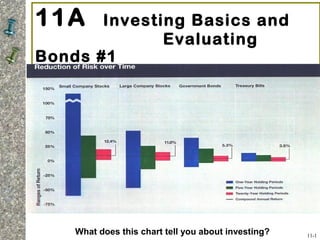

1. 11A Investing Basics and

Evaluating

Bonds #1

11-1

What does this chart tell you about investing?

2. Why People Invest

• To achieve financial goals, such as the

purchase of a new car, a down payment

on a home, or paying for a child’s

education.

• To increase current income.

• To gain wealth and a feeling of financial

security.

• To have funds available during

retirement years.

3. Objective 1

Explain Why You Should Establish

an Investment Program

Establishing Investment Goals

• Financial goals should be:

–Specific

–Measurable

–Tailored to your financial needs

–Aimed at what you want to accomplish

• Financial goals should be the driving

force behind your investment plan

11-3

4. Establishing Investment

Goals

1. What will you use the money for?

2. How much money do you need to satisfy your investment goals?

3. How will you obtain the money?

4. How long will it take you to obtain the money?

5. How much risk are you willing to assume in an investment program?

6. What possible economic or personal conditions could alter your

investment goals?

7. Considering your economic circumstances, are your investment goals

reasonable?

8. Are you willing to make the sacrifices necessary to ensure that you meet

your investment goals?

9. What will the consequences be if you don’t reach your investment goals?

11-4

5. Performing a Financial

Checkup

• Work to balance your budget

– Do you regularly spend more than you make?

– Pay off high interest credit card debt first

• Obtain adequate insurance protection

• Start an emergency fund you can access quickly

– Three months of living expenses

• Have access to other sources of cash for emergencies

– Pre-approved line of credit

– Cash advance on your credit card 11-5

6. Surviving a Financial Crisis

1. Establish a larger than usual emergency fund

2. Know what you owe

• Identify debts that must be paid

1. Reduce spending

2. Pay off credit cards

3. Apply for a line of credit at your bank, credit

union, or financial institution

4. Notify credit card companies and lenders if

you are unable to make payments

5. Monitor the value of your investment and

retirement accounts

11-6

7. Getting the Money Needed to

Start an Investing Program

• Pay yourself first

• Take advantage of employer-

sponsored retirement programs

• Participate in elective savings programs

• Make a special savings effort one or two

months each year

• Take advantage of gifts, inheritances,

and windfalls

11-7

8. The Value of Long-Term

Investing Programs

• Even small amounts invested regularly

grow over a long period of time

• If you begin saving $2,000 each year.

depending on the rate of return, you could

have over $1 million by the time you are age

65 (See Exhibit 11-1 on page 356)

• The higher the rate of return, the greater the

investment risk

11-8

9. Objective 2

Describe How Safety, Risk, Income,

Growth, and Liquidity Affect Your

Investment Decisions

Factors Affecting the Choice of Investments

• Safety and risk

– Risk = uncertainty about the outcome

– Investment Safety = minimal risk of loss

– Risk-Return Trade-Off

• The potential return on any investment should

be directly related to the risk the investor

assumes

– Speculative investments are high risk, made by

those seeking a large profit in a short time

11-9

10. Components of the Risk

Factor

• Inflation Risk during periods of high inflation,

your investment return may not keep pace with

inflation; lose purchasing power

• Interest Rate Risk the value of bonds or

preferred stock may increase or decrease with

changes in interest rates

• Business Failure Risk affects stocks and

corporate bonds (when business is not profitable)

• Market Risk the risk of being in the market

versus in a risk-free asset (stocks follow market cycle)

11-10

11. Investment Income, Growth

and Liquidity

• Investment Income

– A predictable source of income (dividends

or interest)

– Most conservative = passbook savings,

CDs and government securities

– Other choices:

• Municipal and corporate bonds

• Preferred stock

• Utility stocks

• Selected common stocks

• Selected Mutual funds

• Rental real estate

11-11

12. Investment Income, Growth

and Liquidity

• Investment Growth

– Growth in value (price appreciation)

– Common stock usually offers the greatest potential for

growth

– Mutual funds and real estate offer growth potential

• Investment Liquidity

– 2 Dimensions:

• Ability to buy or sell investment quickly

• Without substantially affecting the investment’s

value

• Bank accounts VERY liquid; CDs have penalties;

stocks and bonds could lose money upon sale

11-12

14. Objective 3

Identify the Factors That Can

Reduce Investment Risk

Asset Allocation = The process of spreading your

assets among several different types of investments

(choose % weightings in each)

• The ratio of stocks, bonds, cash assets, other securities

in your portfolio (Conservative, Moderate, Aggressive portfolios

with different asset weights: conservative portfolio = less stock)

• Most important determinant of overall investment

success

= Diversification (“eggs in different baskets”)

11-14

15. Portfolio Management & Asset

Allocation

Other Factors to Consider:

– Your Tolerance for Risk

• At what point can you no longer sleep easily?

• See http://njaes.rutgers.edu/money/riskquiz/

– Your Investment Time Horizon

• When will you need the money?

• How long can your money continue to grow?

– Your Age

• Growth vs. income (older people more conservative)

• Recovery time if investments nosedive

• One guideline: 110 – age = % of portfolio in stock

11-15

16. Your Role in the Investment

Process

1. Evaluate potential Investments

2. Monitor the value of your investments

3. Keep accurate records

4. Other factors

Seek help from personal financial

planner

Consider the tax consequences of

selling investments

11-16

17. Objective 4

Understand Why Investors

Purchase Government Bonds

• Government bonds = written pledge to:

– Repay a specified sum of money (face value)

– At maturity

– Along with periodic interest (coupon payments)

• Sold to fund the national debt and the ongoing

costs of government

• Three levels of government issues:

– Federal

– State

– Local municipalities

11-17

18. U.S. Treasury Bills, Notes and

Bonds

Treasury Bills (T-Bills)

• $100 minimum

• 4, 13, 26 and 52 weeks to maturity

• Sold at a discount

• Federal, but no state, tax on interest earned

• “Reciprocal immunity” doctrine

Treasury Notes

• $100 units

• Typical maturities = 2, 3, 5, 7, and 10 years

• Interest paid every six months

• Higher rate than T-bills (Why?)

• Federal, but no state, tax on interest earned

11-18

19. U.S. Treasury Bills, Notes and

Bonds

Treasury Bonds

• Issued in minimum units of $100

• 30 year maturity dates

• Interest rates higher than Treasury notes & bills

• Interest paid every six months

Treasury Inflation-Protected Securities

(TIPS)

• Sold in minimum units of $100

• Sold with 5, 10 or 20 year maturities

• Principal changes with inflation (measured by CPI)

• Pays interest twice a year at a fixed rate

11-19

20. Federal Agency Debt Issues

• Essentially risk free

• Slightly higher interest rates than Treasury

securities (Why?)

• Minimum investment may be as high as $10,000

to $25,000

• Maturities range from 1 – 30 years

• Average maturity = 12 years

• Issuing agencies sample:

– Fannie Mae

– Freddie Mac

– GNMA

– TVA

11-20

21. State and Local Government

Securities

Municipal Bonds (“Munis”)

• Issued by a state or local government

– Cities

– Counties

– School districts

– Special taxing districts

• Funds used for ongoing costs and to build major

projects such as schools, airports, and bridges

• General Obligation Bonds

– Backed by the full faith, credit and taxing authority of the

issuing state or local government

• Revenue Bonds

– Repaid from money generated by the project the funds finance,

such as a toll bridge

11-21

22. State and Local Government

Securities

Municipal Bonds (“Munis”)

• Key characteristics:

– Interest exempt from federal taxes

– Capital gains may NOT be tax exempt

– Usually exempt from state and local taxes in

state where issued

– Exempt status determined by use of funds

– Lower rate of return than on taxable bonds

• Insured municipal bonds

– Private insurance to reduce risk

11-22

24. Wrap Up

• Concept Check 11-1- Why Develop Specific

Investment Goals? Why Participate in

Employer Retirement Savings Plan? How

the TVoM Affects Investing.

• Exhibit 11-2- A Quick Test to Measure

Investment Risk

• Concept Check 11-2- Four Components of

Risk

• Concept Check 11-4- Taxable Equivalent

Yields